Chapter 2: Private sector development in fragile states

PSD in Africa

PSD in fragile states

Rationale for public sector support of the private sector

Existing multilateral efforts—the World Bank Group

Promoting business growth—policy goals in fragile states

Private sector development policy design in fragile states

Note

Chapter 3: Constraints to business growth in African fragile states

World Bank Doing Business Reports

World Bank Enterprise Surveys

World Bank Group alignment with business constraints

Conclusion

Notes

Chapter 4: Government priorities in fragile states

Methodology

Country government priorities

Economic sector priorities

World Bank Group alignment with government priorities

Conclusion

Notes

Chapter 5: What works—proven PSD successes in fragile environments

IDA alignment with what works

IFC alignment with what works

Notes

Chapter 6: Country case study—South Sudan

Contextual overview

Private sector overview

Major business constraints

Government priorities

Existing donor programs

Conclusion

Notes

Chapter 7: Conclusion

Moving forward

Note

Appendixes

Appendix 1: IFC investments in African fragile state sample, 2000–11

Appendix 2: MIGA guarantees in African fragile state sample, 2011

Appendix 3: Traditional aid modality limitations in fragile states

Appendix 4: Private sector–related donor projects, South Sudan, as of end-2010

Appendix 5: Country case study—Zimbabwe

Appendix 6: Country case study—Somaliland

Appendix 7: Fragile states and World Bank CPIA scores, 2005–09

Appendix 8: Other private sector development initiatives in fragile states

Appendix 9: Methodology for reclassifying IDA PSD-related projects

Appendix 10: Top PSD-related constraints and economic sectors, African fragile states

Appendix 11: IDA IEG project outcome ratings and distributions, 1980–2006

Appendix 12: Correlation analysis of IDA IEG project rating components

Figures

1: Policy design framework for fragile states

1.1: Per capita World Bank Group disbursements by income category, 2010

2.1: Policy design framework for fragile states

3.1 Most frequently cited business constraints in African countries

3.2: IDA alignment, fragile state commitments

3.3 IFC alignment with business constraints, selected measures, 2000–11

4.1: World Bank Group alignment with countries’ PSD priorities

5.1: PSD-related project rating distribution in fragile states, 1980–2006

5.2: Historical IDA prioritization and outcome ratings, by PSD subsector

5.3: Current PSD subsector prioritization and outcome ratings, African fragile states

5.4: DOTS development outcome ratings by sector, weighted and unweighted

5.5: IFC investment return versus portfolio share, 2009–10

6.1: Donor alignment with major business constraints

6.2: Donor alignment with what works

A5.1: GDP and sector growth, 2005–10

A5.2: Change in Doing Business scores, 2006–11

A5.3: “Protecting investors” score, Zimbabwe and comparator economies

A5.4: Deposits and credit to private sector

A5.5: Deposits (left axis) and loan-to-deposits ratio (right axis), 2008–10

A11.1: Project outcome ratings by sector, fragile and nonfragile states, 1980–2006

Tables

1: Criteria to build roads in the Republic of Congo

1.1: African fragile states sample and selected indicators

3.1: Fragile states compared with other developing countries, Doing Business indicators

3.2: Most frequently cited business constraints in African fragile states (percent)

3.3: IDA alignment with “major constraints,” by country, selected measures

3.4: IFC alignment with constraints, 2000–11 (percent)

3.5: IFC investments in African fragile states by sector, 1980–2000

3.6: MIGA investments in African fragile states by sector, 1990–2011

4.1: Country PSD constraint priorities, by frequency

4.2: Country economic sector priorities, by frequency

4.3: IDA project alignment with government priority constraints

4.4: IFC investments and priority sector mapping

4.5: MIGA PSD project and priority sector mapping

5.1: IDA PSD-related project evaluation data, 1980–2006

5.2: IDA project outcome ratings by PSD-related sector, 1980–2006

5.3: IFC loan and equity portfolio income, 2009–10

6.1: Private enterprises in South Sudan, by number and distribution of employees

6.2: Commercial bank exposure, by sector (SDG millions)

6.3: Use of banking services among households, by state (percent)

6.4: Distribution of commercial banking services, by state (number of branches)

6.5: Price comparison of select intermediate inputs, Malakal and other cities

6.6: Time and cost to import a container, Juba and comparator cities

6.7: Donor funding for private sector–related projects, 2010

6.8: Donor alignment with government priorities

References

Supporting Private Business Growth in African Fragile States

A Guiding Framework for the World Bank Group in South Sudan and Other Nations

Benjamin Leo, Vijaya Ramachandran, and Ross Thuotte April 2012

About the authors

Benjamin Leo is a former Research Fellow at the Center for Global Development and the Global Policy Director at the ONE Campaign. Vijaya Ramachandran is a Senior Fellow at the Center for Global Development. Ross Thuotte is a Research Assistant at the Center for Global Development. The authors would like thank the Government of Denmark for generous financial support. We are also grateful to James Emery for his detailed reading of several drafts and his comments on our interpretation of the IFC data. In addition, Alan Gelb, Alvaro Gonzalez, Charles Kenny, Todd Moss, and Gaiv Tata provided extensive comments on various drafts of this report, and we would like to thank them for their efforts. John Osterman was of great help in guiding this manuscript through to publication, and Julie Walz provided excellent research assistance. The authors are solely responsible for any errors in fact or judgment.

The Center for Global Development is grateful for contributions from the Royal Danish

Embassy in support of this work.

Preface

Fragile and post-conflict states pose a daunting challenge to the World Bank Group. They suffer from a combination of harsh business environments, unstable and corrupt political regimes, and rent-seeking actors. These barriers prevent private businesses from generating much-needed services, economic growth, and jobs. Viewing the private sector as the key to economic and social progress in fragile states, the authors of this report assess the programs and projects supported by the three major arms of the World Bank active in those states (the International Development Association, the International Finance Corporation, and the Multilateral Investment Guarantee Agency) and propose a strategy to improve the overall effectiveness of the Bank’s work.

Though the World Bank Group and its shareholders have made fragile states a priority in recent years, their private sector–oriented programs in the past decade have not yielded many concrete development results. Bank Group staff has been asked to improve project outcomes and to help increase the absorptive capacity of fragile states while targeting priority sectors. But there has not been a clear World Bank Group-wide strategy for fragile states operations.

Using project documents and other sources of information, the authors have compiled a comprehensive dataset on the Bank Group’s work in 14 African states (Sudan, Central African Republic, Democratic Republic of Congo, Togo, Guinea Bissau, Guinea, Liberia, Angola, Côte d'Ivoire, Republic of Congo, Zimbabwe, Eritrea, Chad, and Burundi) which are classified as fragile by the World Bank Group. The dataset describes 5,000 IDA projects, 3,700 IFC projects and 700 MIGA projects over the period 1980–2011 that focus on building the private sector in these states. These data are available for the first time in an easily accessible format and will likely serve as a valuable resource for policymakers, donors and other interested actors. Analysis of the data shows that there often does not appear to be a clear strategy driving the interventions and that they are sometimes at odds with the stated needs of policymakers and the public.

Policymakers at the World Bank and those in its shareholder countries should heed the authors’ findings if they hope to help private sector businesses grow in Africa’s most challenging investment environments. The authors’ methodical and exhaustive assessment allows them to deliver a clear message. The World Bank should design and implement projects that a) alleviate the growth constraints most identified by businesses, b) target sectors that governments have explicitly made priorities, and c) align with proven, country-specific successes. Adherence to this framework could greatly increase the chances of successful future private sector–oriented interventions in fragile states.

Nancy Birdsall

President

Center for Global Development

Acronyms

AfDB

African Development Bank

CPIA

Country Policy and Institutional Assessment

DOTS

Development Outcome Tracking System

FCS

Fragile and conflict situation

FIAS

Financial Investment Advisory Service

FY

Fiscal year

ICT

Information and communication technology

IDA

International Development Association

IEG

World Bank Independent Evaluation Group

IFC

International Finance Corporation

IFI

International financial institution

IRAI

IDA Resource Allocation Index

IRR

Internal rate of return

MDC

Movement for Democratic Change

MIGA

Multilateral Investment Guarantee Agency

PPIAF

Public-Private Infrastructure Advisory Facility

PPP

Public-private partnership

PSD

Private sector development

SME

Small and medium enterprise

USAID

U.S. Agency for International Development

WFP

World Food Programme

ZANU-PF

Zimbabwe African National Union–Patriotic Front

This document is fully functional in Chrome, Safari, Firefox, and Internet Explorer 9

Supporting Private Business Growth in African Fragile States

A Guiding Framework for the World Bank Group in South Sudan and Other Nations

Benjamin Leo, Vijaya Ramachandran, and Ross Thuotte April 2012

The World Bank Group faces significant operational changes over the near to medium term. More than half of poor countries are projected to graduate

from the World Bank’s International Development Association (IDA) concessional assistance over the next 15 years.[1] As a result, IDA’s country client

base is projected to become dominated by African fragile states. To its credit, the World Bank Group recognizes these coming changes and the unique

needs and constraints present in fragile environments. It has publicly expressed a plan to develop an organization-wide strategy tailored specifically

for fragile and conflict-affected situations.

At the same time, private businesses often are able to operate in the absence of stable, well-established governments and therefore can present donor

organizations with an attractive pro-growth opportunity in fragile states. After all, the overwhelming majority of African jobs come from the private

sector, and private businesses are responsible for some of the most dramatic improvements in the African economic landscape over the past decade.

Perhaps most impressively, the mobile telecommunications sector, comprised almost entirely of private firms, generated more than 300 million mobile

phone subscribers between 2000 and 2008. Recognizing these issues, the World Bank Group must make business growth a central objective of its future

strategy for fragile and conflict-affected states. The most recent World Development Report and its subsequent implementation report partially

reflect this sentiment. They argue that the organization must “position fragility, conflict, and violence at the core of its development mandate” and

that the Bank must “significantly adjust its operations model” to reflect this priority shift.[2] Currently, the World Bank Group is

devising a new strategy that will set the tone for Group-wide strategic changes.

Scope and key findings

First, we examine three key private sector–related factors in African fragile states: what businesses cite as the most binding constraints to private

sector growth; what government priorities are for business climate improvements or strategic economic sectors; and what types of projects have been

more effective over time. This analysis draws upon World Bank Enterprise Survey data, a newly assembled database of African fragile state government

priorities, and World Bank Independent Evaluation Group project outcome rating data. Our summary findings include:

Business constraints.

On average, the most frequently cited business constraints in African fragile states include electricity (68 percent of survey respondents), access

to finance (56 percent), political instability (56 percent), corruption (48 percent), and tax rates (40 percent).

Government priorities.

African fragile state governments have prioritized the following issues: regulatory framework reforms (100 percent of sample countries), transport

infrastructure (100 percent), electricity (92 percent), access to and cost of finance (83 percent), and macroeconomic stability (75 percent). Our

analysis seeks to identify government priorities in a defined set of African fragile states. A separate comparison between fragile and nonfragile

low-income country priorities could be useful to World Bank project design staff.

Project outcome performance.

The private sector–related subsectors with the highest project outcome ratings include: telecommunications, oil and gas, transport infrastructure,

and trade policy reform. At least half of IDA projects had at least “satisfactory” outcome ratings in these subsectors. The worst-performing

subsectors include: port infrastructure; banking; micro, small, and medium enterprise finance; rail infrastructure; and mining.

Subsequently, we assess the alignment of World Bank Group operations within these three areas over the last decade. For this analysis, we have

assembled a new database covering all World Bank Group operations in fragile states since 1980, which includes current and past fragile states (both

African and non-African). Overall, we find that project alignment varies widely across the World Bank Group’s three largest subsidiaries—IDA, the

International Finance Corporation (IFC), and the Multilateral Investment Guarantee Agency (MIGA). Despite several bright spots, our analysis suggests

that strategic changes in the World Bank Group’s operations are needed—particularly for IFC and MIGA. Our summary findings include:

IFC and MIGA alignment performance

. IFC and MIGA projects are only modestly aligned with the private sector’s most binding constraints or government priorities. Instead, projects

have been heavily concentrated in low-risk sectors, such as the extractive sector (between 1980 and 2000). In recent years, this concentration has

shifted toward the financial sector (on a project count basis) and the telecommunications sector (on a project value basis). Taken

together, IFC activities over time suggest that the organization chooses its investments on a project-by-project basis, rather than implementing a

comprehensive, systematic strategy in African fragile states.

IDA alignment performance

. IDA exhibits very strong alignment with government priorities and reasonably good prioritization in sectors with higher project outcome ratings.

But it has a more mixed performance with respect to focusing on what businesses cite as the most binding private sector–related constraints. By

illustration, it has focused a disproportionate share of private sector–related projects on transport infrastructure, which businesses cite less

frequently as a “major constraint.” On the other hand, IDA has pursued fewer projects focusing on the most binding constraints, such as electricity

and access to finance.[3]

Recommendations

Based on this analysis, we propose a new guiding framework for the World Bank Group and other donor institutions for prioritizing private

sector–related projects in fragile states. We recommend that private sector promotion policies prioritize three key issues: addressing the most severe

constraints to private sector growth; matching the host government’s stated priorities; and targeting sectors and subsectors with proven track records,

relative to other sectors (figure 1). Moreover, donor policies and projects should also contribute to broader development goals, including job

creation, economic growth, broadening and strengthening of the tax base, and positive spillover effects into other economic sectors.

Ideally, donor institutions would pursue projects in sectors or areas where all three components intersect (what the private sector needs, what the

government wants, and what donors do effectively). For example, a project to build roads in the Republic of Congo would meet all three criteria (table

1).

Table 1: Criteria to build roads in the Republic of Congo

Component

Rationale

Constraints

According to a 2010 World Bank Business Enterprise survey, 57 percent of Congolese businesses cite transport as a “major constraint” togrowth

Government priorities

Transport infrastructure is cited as a major constraint to business by the Republic of Congo’s most recent Poverty Reduction StrategyPaper

Track record

Between 1980 and 2006, road projects in fragile and conflict-affected countries received an average rating of 2.4 of 5—a relativelyhigh score for projects in these countries

Development goals

Building roads would create near-term jobs for workers while providing a public good for other sectors over the medium to long term.Eventually, the tax base could be strengthened if tax-paying businesses benefited from the road network improvements

To be most effective, this framework could be applied to all segments of the World Bank Group project cycle—including policy design, ongoing

operations, and exit evaluations. Operational implementation of the proposed approach clearly should be customized across subsidiaries and individual

countries. But without a concerted and consistent strategy both within and across subsidiaries, World Bank Group projects will continue to perform at a

suboptimal level in fragile and conflict-affected states.[4]

To help implement this framework, the World Bank Group should consider ways of addressing three central issues: improving managerial capacity to enable

a bolder approach to fragile states; revising human resource strategies to attract and retain staff who are willing to take risks and understand the

operating conditions in fragile states; and improving staff incentives to reward greater risk-taking and innovation. Each of these areas is enormously

challenging, but must be tackled in order to successfully implement an ambitious fragile states agenda.

[2]

World Bank Group Development Committee (2011).

[3]

World Bank Group project decisions are complex and consider a broad array of issues. Promoting private sector business growth is just one of

the many priorities of the World Bank Group; this may be reflected in its project portfolio.

[4]

Fragile states are often affected by violence and conflict and generally suffer from poor governance. Furthermore, large elements of the

private sector in these countries may be criminalized, dominated by rent-seeking actors, or entirely informal and unregulated. As such,

expectations for project effectiveness in these countries should be lower relative to non-fragile countries. However, adherence to the proposed

framework would address some of the pitfalls involved in fragile state private sector growth promotion efforts and might improve their

effectiveness.

Overview

In recent years, international financial institutions (IFIs) have dramatically increased their worldwide investments in the private sector—from $10

billion in 1998 to more than $35 billion in 2008.[1] In Sub-Saharan Africa, donor

financing for private sector–related activities through loans, guarantees, and advisory services has also increased at a fast pace. By contrast,

African fragile states overall have experienced little growth in donor projects targeting private sector activities and continue to receive

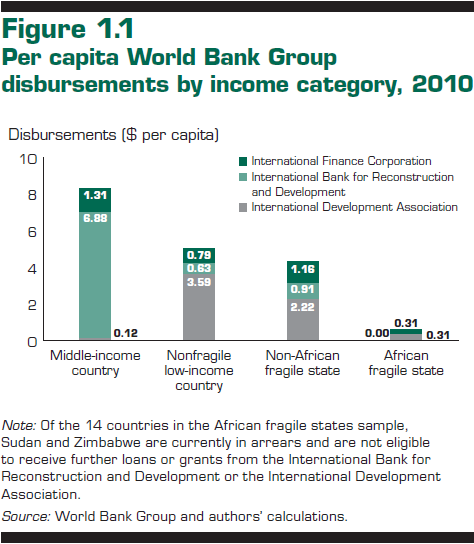

infinitesimal (albeit slowly increasing) portions of World Bank Group disbursements in recent years (figure 1.1) on a per capita basis.[2] The time period for the data in

figure 1.1 is 2010, which the World Bank Group considers to be a “postcrisis” period. Some disbursements in this year are countercyclical measures to

mitigate the negative impact of the financial crisis. Therefore, we cannot assume that this is entirely indicative of World Bank Group disbursements in

a typical year. However, countercyclical lending policies are mostly likely not the sole cause of the large discrepancy between disbursements to

middle-income countries, low-income countries, and African fragile states.

There are a number of factors driving these low investment levels, such as small market size, high political risk, poor infrastructure, and weak legal

and regulatory frameworks. Moreover, International Development Association (IDA) projects are roughly twice as likely to fail as those in nonfragile

states.[3],[4] Institutional factors within

IFIs themselves also have contributed to underinvestment over time. For example, the International Finance Corporation’s (IFC) risk-averse culture and

mandate to earn a profit are just two factors that have led to very few investment deals in African fragile states outside of enclave sectors.[5] The current World Bank Group

project portfolio reflects the realities of investing in fragile states. It also reveals some of the challenges that the World Bank Group and other

IFIs might consider when scaling up their activities in fragile states over the near to medium term.

Definition of fragile states

For the purposes of our analysis, we define African fragile states according to countries’ respective IDA Resource Allocation Index (IRAI) score

between 2005 and 2009.[6]

Specifically, countries are defined as fragile if they fall into one of two categories:[7],[8]

All core.

Country has remained below a score of 3.0 for all years.[9]

All marginal.

Country has remained below a score of 3.2 for all years.

Based on this approach, the countries of interest (in order of 2009 IRAI scores from lowest to highest) include: Zimbabwe, Eritrea, Sudan, Chad,

Guinea-Bissau, the Central African Republic, the Democratic Republic of Congo, Togo, the Republic of Congo, Liberia, Angola, Côte d’Ivoire, Guinea, and

Burundi. These 14 countries provide a variety of case studies spanning geographic regions, income groups, and natural resource endowments (table 1.1).

Our diverse group of African fragile states also allows us to formulate a policy framework that may be relevant to a wider range of fragile

environments.

Table 1.1: African fragile states sample and selected indicators

Country

Population (millions)

GDP

(USD millions)

GDP per Capita

CPIA (2010)

Conflict-Affected

In Arrears

Oil Exporter

Angola

19.0

25,901

1,364

2.8

✓

✓

Burundi

8.5

966

113

3.1

✓

Central African Republic

4.5

1,054

234

2.8

✓

Chad

11.5

3,097

269

2.4

✓

✓

Congo, Dem. Rep.

67.8

6,851

101

2.7

✓

✓

Congo, Rep.

3.8

5,067

1,348

2.9

✓

✓

Côte

d'Ivoire

21.6

11,666

541

2.7

✓

✓

Eritrea

5.2

692

133

2.2

✓

Guinea

10.3

4,108

398

2.8

Guinea-Bissau

1.6

244

148

2.7

Liberia

4.1

619

151

2.9

✓

Sudan

43.6

22,819

524

2.4

✓

✓

✓

Togo

6.8

1,719

254

2.9

Zimbabwe

12.6

4,082

323

2.0

✓

Total

221.0

88,887

421

2.7

-

-

-

In its latest World Development Report, the World Bank stresses the importance of integrating security and development activities in

conflict-affected and fragile state environments.[10] In operational terms, the

report suggests that the World Bank Group plan to make country strategies more fragility-focused; prioritize private sector development (PSD) and job

creation; realign results and risk-based frameworks; and reduce volatility in financing levels. The World Bank’s concessional financing entity—the

IDA—has already been pursuing a number of evolving strategies customized for fragile state environments. While modest progress has been achieved,

significant work remains. In contrast with IDA, the World Bank Group’s other subsidiaries—IFC and the Multilateral Investment Guarantee

Agency—currently do not have operational strategies for fragile states. So the World Bank Group faces a number of challenges in translating the new World Development Report directives into effective programs on the ground.

Against this backdrop, we consider a range of issues and options that may help the World Bank Group and other donor organizations streamline operations

and improve their effectiveness in African fragile states. First, we examine whether the World Bank Group implemented its projects in African fragile

states over the last decade in order to address the most significant obstacles to business growth; country government priorities; and areas where the

World Bank Group has a proven track record. In this manner, we gauge how well the World Bank Group is focusing on what is needed, what is wanted, and

what works. Second, we apply this approach to assess donors’ PSD support in the newly independent nation of South Sudan.[11] Taken together, our findings

suggest a somewhat mixed picture about the World Bank Group’s alignment and effectiveness in promoting PSD in African fragile states. Finally, drawing

upon this analysis, we propose a number of strategic and operational policy recommendations for the World Bank Group to consider as it seeks to

prioritize and improve its PSD programs in African fragile states.

[2]

In this report, we use several metrics to demonstrate the relative size of World Bank Group commitments to fragile states. First, to reduce the

bias of countries with larger populations receiving more commitments, we use per capita figures. Second, to gain the perspective of fragile

state commitments versus commitments in other countries, we use commitment values in fragile states as a percentage of total commitment values

in all countries. Third, for countries in which high-value projects are simply not feasible, we use project count metrics in relation to total

Group projects in all countries.

[4]

While IDA’s supply-driven resource allocation model ensures that fragile states receive substantial assistance volumes, poor project

performance levels have a significant influence on the sectors targeted by IDA funding. IDA’s performance-based allocation (PBA) system does

include a project portfolio quality component, which has a modest impact on each respective recipient country’s resource allocation.

[5]

Of the numerous private sector–related programs and funding sources listed later in this paper, investments in fragile states constitute a

small portion of overall investments. For a complete breakdown of multilateral development banks’ investments, see Perry (2011).

[6]

IRAI scores are based on the World Bank’s annual Country Policy and Institutional Assessment (CPIA) exercise. They are calculated as the

average of country ratings across four distinct categories: economic management; structural policies; policies for social inclusion/equity; and

public sector management and institutions. The CPIA/IRAI is the principal determinant of a given country’s IDA allocation. For additional

details, see www.worldbank.org/ida.

[7]

Appendix 7includes a full list of existing African “fragile states,” their IRAI scores, and categorizations. To maintain close

relevance with our target countries, we have omitted island nations and non-African countries.

[8]

This report’s definition of fragile states tracks largely with that of the World Bank, which defines “core” and “marginal” states as those

countries with IRAI scores of below 3.0 and 3.2, respectively. Our only departure from the Bank’s definition is that we extend the period to

2005–09.

[9]

This categorization also includes countries that are missing data for one or more years, but that lie below 3.0 when scored.

[11]

Appendixes 5 and 6 provide further analysis on the case studies of Zimbabwe and Somaliland.

Private sector development in fragile states

PSD in Africa

In recent years, the majority of investment in the African private sector has flowed toward the rapidly expanding telecommunications and extractive

industry sectors. Between 2005 and 2008, private investors contributed 62 percent of total funding to the telecommunications industry, which has

resulted in the rapid expansion of networks and profitability, as well as prospects for continued growth.[1] By illustration, African

telecommunications firms generated more than 316 million mobile phone subscribers between 2000 and 2010.[2] The rapid 43 percent annual

growth rate leaves plenty of room for upward movement in the sector, as mobile penetration only reached 44 percent in 2009.[3] Unlike other sectors,

telecommunications growth has spanned the gamut of Sub-Saharan countries, ranging from middle-income economies to fragile states.[4] The natural resources and

extractive industries have also accounted for a significant portion of African growth, contributing roughly a quarter of Africa’s growth between 2002

and 2007.[5]

While progress in the telecommunications and extractive industry sectors is promising, current signals indicate that private investors’ appetite for

other sectors continues to grow and that private sector expansion could provide a valuable boost to capital- and capacity-starved fragile states.

Private sector investment projects in infrastructure could provide high investment returns (as in telecommunications) for both investors and customers

in fragile states. For example, “bankable” investments in electricity generation capability and infrastructure (for which there is significant consumer

demand) could greatly decrease costs for businesses while generating revenue for power providers.[6]

PSD in fragile states

Theoretically, the private sector has many opportunities to thrive in environments in which traditional aid cannot succeed. For instance, the private

sector can exist (and even thrive) even when there is no central government that is stable enough to accept foreign aid (for example, Somaliland). This

could make the private sector a particularly viable and valuable target for economic development interventions in fragile states. Therefore, promoting

private sector growth in fragile states could be one tangible first step toward better governance and more diverse, robust economies. However, despite

a sound rationale for public sector intervention in the private sector, private sector development (PSD)–focused activities in fragile state

environments remain vulnerable to a range of binding or limiting constraints.

Fragile states generally are categorized by very weak business climates that often restrict individual firm activities through several channels. In

particular, the indirect costs of poor infrastructure, regulatory challenges (such as excessive licensing fees, bribes, and so forth), and low labor

productivity can reduce profit margins and reduce incentives for business owners and prospective entrepreneurs.[7] These effects can be

exacerbated in fragile states, in which governments and institutions routinely fail to administer services, enforce contracts, and reduce corruption.

Political risk also is a major concern for multilateral institutions that wish to invest in the African private sector. This illustrates African

fragile states’ acute need for customized financing instruments, such as political risk guarantees.

Fragile states also lack the human capital needed to operate scalable business ventures. While skilled micro-entrepreneurs may exist en masse in

countries like Chad and Burundi, many of the most skilled businesspeople (such as those with formal skills in accounting, personnel management,

strategic planning, risk analysis, marketing, and the like) have often left these hostile business environments for more lucrative and/or secure

opportunities abroad. Although these highly skilled workers often send home substantial remittances, they frequently do not maintain local businesses

in the fragile-state environment from where they came.[8]

Many firms in fragile states are also heavily constrained by what Ramachandran, Gelb, and Shah (2009) refer to as “external costs.”[9] These external or indirect

costs—such as those stemming from failures in electricity service provision, transport infrastructure, and supplier networks—often erode individual

businesses’ profit-making capabilities. In other words, many African firms’ “ability to produce value beyond the cost of their direct and indirect

inputs is heavily constrained by the magnitude of the cost of the latter.”[10] Finally, markets for goods

in nearly all of our 14 fragile states are particularly disparate and weak. Even with strong support from multilateral development banks on the supply

side, the private sector will not thrive without predictable and steadily increasing demand from local consumers.

Rationale for public sector support of the private sector

Before launching into a more in-depth discussion of PSD initiatives in fragile states, we shall examine several broad theoretical rationales for public

sector support of the private sector. First, it is believed that PSD activities help to create jobs and foster economic growth (the private sector

accounts for roughly 90 percent of jobs in the developing world).[11] Second, many argue that the

public sector should support the private sector because individual businesses are constrained by numerous government-driven limitations, ranging from

corruption to lack of physical infrastructure. Third, many of these constraints result from market deficiencies that theoretically can be rectified by

public sector initiatives. For example, imperfect capital markets hinder businesses—notably small and medium enterprises—by not investing in profitable

projects. This often occurs because of imperfect information regarding profitability, high transaction costs, and insufficient legal frameworks and

enforcement mechanisms. Relatedly, informal and small firms are often unable to pledge collateral and lack formal title rights to physical property.[12] Another example relates to

governance. PSD requires an appropriate institutional framework that the private sector cannot provide for itself. While there are several examples of

private sector firms joining together to help stabilize the governance environment (such as in Somaliland), most firms in fragile states are unwilling

or unable to create the institutional framework necessary to promote PSD by themselves.[13]

Existing multilateral efforts—the World Bank Group

The World Bank Group and others donor organizations’ PSD goals in African fragile states broadly mirror those in other low-income countries. The key

differences relate to developing policies and projects that are tailored to the more difficult operating environments.

The World Bank’s soft loan facility (the International Development Association, or IDA) has a significant presence in fragile states. All of the

African fragile states are IDA-eligible borrowers, though several countries (namely, Sudan and Zimbabwe) currently are inactive due to World Bank Group

loan arrears. Oil-producing African fragile states (Angola and the Republic of Congo) are above the IDA lending income cutoff, but still have access to

IDA loans on “hardened terms.”[14] Although one of IDA’s

specific foci is PSD, its projects in many sectors such as infrastructure and regulatory reform result in positive spillover effects for private sector

businesses. Indeed, much of IDA’s contribution to the private sector may result from indirect benefits from non-PSD–focused IDA projects. IDA’s current

eligibility requirements have significant implications for the institution’s future. A recent study estimates that by 2025, most IDA-eligible countries

will be African fragile states—a reality that may compel IDA to restructure its strategy around fragile lending environments in the coming years.[15] By extension, adapting to

the specific constraints of fragile states will be essential to IDA’s continuing success.

The efforts of the World Bank Group’s private sector arm are of particular interest. The International Finance Corporation (IFC) is a leading global

player in the PSD spectrum and makes nearly 40 percent of all investments that originate from development finance institutions.[16] However, IFC’s 2010 project

disbursements to African fragile states, on a per capita basis, were four times smaller than commitments to middle-income countries.[17] The smaller levels of

investment in African fragile states reflect investment conditions characterized by volatility and high levels of risk, limited private sector

partners, and few choices for viable investment projects. And if IFC hopes to scale up its investments in African fragile states (a World Bank

Group–wide measure has been proposed in the most recent World Development Report), it must innovate its investment model.

Taken together, the World Bank Group has shown an increased level of commitment toward fragile states in recent years. During the World Bank’s spring

2011 Development Committee meeting, shareholders agreed on the following commitments:[18]

Make fragile and conflict situation (FCS) strategies more fragility-focused by preparing new strategies for FCS countries.

Increase attention to jobs and PSD by promoting a common World Bank Group approach to employment and introducing new IFC/Multilateral Investment

Guarantee Agency (MIGA) instruments.

Realign results and risk frameworks for FCS countries through the development of results metrics that are sensitive to conflict and fragility.

Strive for “global excellence in FCS” by establishing a new FCS hub in Nairobi by the end of fiscal year (FY) 2011 and further revising human

resource policies that reflect FCS priorities and needs.

Since this World Bank Group strategy was approved only recently, it has yet to be operationalized by the individual World Bank subsidiary organizations

such as IFC and IDA. However, the IFC launched its five-yearConflict Affected States in Africa Initiative in 2008 to help design and implement

integrated strategies that support economic recovery in conflict-affected countries. Roughly 18 percent of total IFC advisory service expenditures

worldwide are committed to World Bank–classifiedfragile states, which include non-African countries. Specifically, the Conflict Affected States

in Africa program has four main elements: improving the business environment through regulatory reform; strengthening small and medium enterprises and

support institutions (such as chambers of commerce); rebuilding financial markets and other financial institutions; and increasing private sector

involvement in rebuilding infrastructure.[19] The IFC has implemented

Conflict Affected States in Africa projects in several postconflict countries with severe business climate constraints, such as Burundi, the Central

African Republic, the Democratic Republic of Congo, Liberia, and Sierra Leone. It continues its extensive advisory service operations in many African

fragile states. IFC emphasizes the importance of these services in lieu of larger investment project operations, which it says are especially difficult

in fragile environments.[20]

Although there are numerous efforts aimed at promoting African infrastructure growth (one result of which would be private sector growth), few of these

initiatives have the capability and/or audacity to commit resources to fragile states. Although examined for this report, many private sector and

infrastructure initiatives were not included because they do not focus on fragile states. These initiatives/institutions include NEPAD’s Infrastructure

Investment Fund, DevCo (a fund overseen by the Private Infrastructure Development Group), and InfraCo (also funded by the Group). A list of selected

PSD initiatives in fragile states is located in appendix 8. Of particular interest is the Public-Private Infrastructure Advisory Facility (PPIAF),

which was established in 1999 to increase private sector participation in emerging markets. PPIAF provides grants to help governments create a sound

enabling environment for private participation in infrastructure through activities such as framing infrastructure development strategies, organizing

stakeholder consultation workshops, and designing pioneering projects.[21] PPIAF, committing about $20

million a year globally, has sponsored projects in fragile states such as the Democratic Republic of Congo, Guinea, Guinea-Bissau, Liberia, and Sierra

Leone.[22] The projects often

have a regional focus, and PPIAF’s 2011–13 work plan cites fragile states as one of four major cross-cutting themes for future projects.

The World Bank Group’s Financial Investment Advisory Service (FIAS) is a multidonor investment climate program that assists developing and transition

economies to improve their business environments with an emphasis on regulatory simplification and investment generation.[23] FIAS also coordinates with

IFC Advisory Services and other World Bank Group departments. Forty-five percent of FIAS activities in FY10 occurred in Sub-Saharan Africa, including

31 percent of its implementation expenditures in fragile and postconflict states.[24] FIAS completed five business

reforms in three fragile states, including business taxation reform in Sierra Leone, construction permits in the Democratic Republic of Congo, and

investment policy reforms in Guinea-Bissau. In 2011, FIAS began designing a methodology to estimate the savings accrued to firms resulting from its

business climate reform support. FIAS’s client satisfaction rating has hovered around 90 percent in recent years.[25] Moreover, FIAS released a Rough Field Guide to Investment Climate Reform in Conflict-Affected Countries in 2010, which explicitly links investment climate improvement

with peace-building efforts in postconflict countries. The report also provides highly detailed instructions on the design, implementation, and

evaluation of investment climate reforms, including laws, regulations, and procedures that govern industry competiveness, bureaucratic efficiency, and

institutional governance.[26]

The World Bank’s Doing Business project provides absolute and relative measurements of business regulations and obstacles across 183 economies. These

annual reviews contain extensive data on constraints to business growth, including time and costs required to start a business, licensing fees,

construction permits, and trading across borders. Unlike most private sector–oriented diagnostics, Doing Business collects data annually for nearly all

of the world’s economies.[27]

While the Doing Business program does not support specific business reform activities, its field analysis and findings feed into IFC, FIAS, and

non–World Bank Group programs assisting fragile states (and other countries) with business climate reforms.

Promoting business growth—policy goals in fragile states

The next chapters describe the World Bank Group’s projects in some detail. But first, with a view to evaluating the efforts of the World Bank Group, we

describe four key business growth–related objectives in fragile states: supporting broad-based economic growth, job creation, tax mobilization, and

positive spillovers. We also introduce a conceptual framework to guide support operations that could be adapted and applied to a variety of African

fragile state environments.

Broad-based economic growth

Sustained, broad-based economic growth is the critical driver for significant poverty reduction in low-income countries, particularly in view of the

limited scope for income redistribution. But as the World Bank’s Commission on Growth and Development states, economic growth is not an end in itself.

Rather, it is the spark to create resources and social services to support health, education, job creation, and other development goals. By

illustration, one study estimated that a 2 percent rise in average household income resulted in a 1.2–7.0 percent decline in poverty rates.[28] Therefore, economic growth

has major implications for poverty reduction in African fragile states.[29] Over the last 30 years,

poverty levels have fallen significantly, with much of the progress being attributable to economic growth. Globalization has provided the platform to

expand markets, import ideas and technology, and facilitate the movement of human capital and investment to regions that were previously largely closed

off from the global economy. Although there is not one common success story, countries that have achieved sustained economic growth have maintained

macroeconomic and political stability, raised investment and savings, and opened their markets. The overriding policy challenge is to determine how to

apply these success stories to the poorest and most fragile countries.

The World Bank’s Commission on Growth and Development outlines several types of countries that face dramatic challenges in achieving sustained economic

growth. These include Sub-Saharan countries still contending with postcolonial resource extraction models and negative spillovers from unstable and

violent neighbors; small states with significant concentration in a few economic sectors highly vulnerable to exogenous shocks; governments facing

comparatively high per capita costs of social services; and countries rich in natural resources facing Dutch disease and rent-seeking risks. Most

African fragile states examined in this report fall into one of these categories.

Job creation

The labor market is deeply entwined with both economic growth and poverty reduction. Many African fragile states face high, persistent unemployment

levels, particularly among youth and demobilized combatants, which can contribute to increased rates of violence, political instability, and higher

levels of poverty.[30] Therefore,

supporting job creation opportunities should be a central objective of any World Bank Group operation that aims to promote business growth. The

relationship between jobs and growth is largely a two-way street: sustainable economic growth depends at least partly on the underlying labor market

structure and a flexible labor force, while employment growth often depends on growth of output in the formal sector. But a key characteristic of

African labor markets is the very high ratio of informal to formal sector employment.[31] Thus, although formal sector

growth is essential in the long term, the informal sector often has greater capacity to absorb the ever-expanding labor force—especially in economies

constrained by low formal output growth.[32] Therefore, African fragile

state governments and donor organizations often need to pursue two-track approaches for supporting increased productivity within the informal sector

while simultaneously improving the operating environment for formal enterprises.

Tax mobilization

A third PSD-related objective is fostering a broad, stable tax base, which contributes to improved governance, accountability, and economic growth.

Domestic tax policies have the potential to strengthen government legitimacy in the eyes of constituents through increased accountability and

transparency, perceived fairness, and a clear political commitment to shared prosperity.[33] Government revenues are also

necessary for providing social services and can be used to support economic growth and diversification. There is considerable variation in African

countries’ tax bases, with the lowest tax bases often corresponding to almost exclusive dependence on natural resource rents. Tax revenues average

roughly 14 percent of GDP in African fragile states, with oil exporters Chad and the Republic of Congo on the low end with slightly higher than 5

percent of GDP and Liberia and Zimbabwe on the high end with approximately 30 percent of GDP.[34] Due to large informal

sectors, most fragile states have relatively narrow tax bases. Thus, the government’s “fiscal-social contract” with the private sector is an important

step toward reform. Formalizing the informal sector of the economy creates not only a broader tax base and larger stream of revenue to provide

necessary services, it provides an incentive for expanded political participation.[35]

Positive spillovers and multipliers

Another driver of success is growth spillovers—when growth in one part of the country or some subset of firms impacts the growth of other firms or

regions. At the country level, open borders for the flow of goods and services, along with increasing migration and flow of human capital, lead to

increasingly positive spillovers. Within countries, knowledge and technology are key ingredients in the development of industry, and can be shared

across firms. Also, firms in fragile states may be able to “borrow” knowledge cheaply, helping to “leapfrog” the historic development process. Mobile

phone technology is a prime example.[36] Finally, some types of

investments can also spur the growth of related industries, either upstream or downstream in the production process.[37]

Private sector development policy design in fragile states

In light of these policy goals, how should the World Bank Group best prioritize its PSD-related support programs in African fragile states? Upon

careful review of the diagnostics of each economy and the tools available to donors, we propose that good policies are drawn from the intersection of

three elements—the private sector’s most severe constraints, the stated priorities of governments, and policy interventions with an acceptably

effective track record (figure 2.1). The policies emerging from the intersection of these areas must also support the above-mentioned goals of economic

growth, job creation, tax mobilization, and positive spillovers.

Our conceptual model brings together these three fundamental areas for policy design. First, to generate growth, policymakers must create a conducive

environment for business owners and managers of small, medium, and large firms. Extensive survey data on the problems reported by businesses are

available on the World Bank’s website and from other sources.[38] We analyze these data to

identify the most critical problems facing businesses that are trying to survive in fragile environments. Understanding their constraints is the

crucial first step toward good policy design. Whether it is the basics (infrastructure and public services), regulations (taxes, licensing rules), or

labor shortages, we need to know what the private sector believes is holding back growth.

The second area is understanding government priorities. Policymakers in fragile states operate in very difficult environments, often trying to address

various constraints simultaneously with very few resources. Understanding their perspective and primary objectives is important, especially for

policymakers in multilateral institutions. By searching through public documents, speeches, and other data, we try to identify what African fragile

state governments perceive to be their most binding PSD-related obstacles. There may well be some overlap between their perspective and that of the

private sector, as we will see in next chapters.

Third, we must use the lessons learned from past policy interventions. Understanding what has worked in fragile environments will be useful to the

design of new policies, programs, and projects, particularly when these findings are referenced against public and private sector constraints and

priorities. To accomplish this task, we analyze past policy interventions using a database of IDA projects and other sources to identify successful

projects by sector, type, and location.

When considered together, these three analytical components can help multilateral organizations prioritize PSD-related programs in fragile states. As

noted previously, donor institutions ideally would pursue projects in sectors or areas where all three components intersect (what the private sector

needs, what the government wants, and what donors do effectively). This is the “priority action” zone of the conceptual framework. But there will be

situations or environments in which multilateral organizations may wish or need to pursue projects or investments that do not meet this condition. In

this instance, we recommend that multilateral organizations then prioritize projects in sectors or areas where two of the three components intersect.

Careful attention should be given to why one of the components does not meet this condition and what types of remedial actions would be required. For

each of the omitted policy prioritization components, potential remedial steps could include the following in different situations:

Major PSD constraints (need to tread carefully).

Multilateral organizations should proceed very cautiously in the absence of private sector buy-in. However, there could be instances when

proceeding could be justified—such as a prioritization overlap with informal and/or small and medium enterprises, though not with the business

elite.

Government priorities (need to get buy-in).

Multilateral organizations should determine why the private sector and national government priorities are not consistent. After this, steps should

be taken to encourage government buy-in as appropriate—particularly in areas where direct or indirect government involvement is likely. But

multilateral organizations may want to deprioritize the need for buy-in in failed or highly repressive states.

Proven results (need to innovate)

: Multilateral organizations will need to consider innovative or alternative implementation models to ensure that project or investment results

exceed historical performance patterns. Moreover, careful attention should be given to programmatic factors that are significantly predictive of

project outcome performance ratings, such as quality-at-entry and supervision (these issues are examined in greater detail in chapter 4).

The next chapters explore each of these areas—constraints reported by businesses, priorities of governments, and understanding what works—in

significant detail. Each chapter examines the available data, and then compares them with the project portfolio of the three relevant World Bank Group

entities—IDA, IFC, and MIGA (when possible). The aim of this analysis is to understand whether these institutions have operated with a consistent,

well-defined strategy and whether their projects have met needs identified by either the government or the private sector (or ideally both). Finally,

our conceptual model is used to identify priorities for Africa’s newest country, South Sudan (chapter 6). Case studies for Somaliland and Zimbabwe are

included as well.

[4]

For example, Zain (a Kuwaiti mobile telecommunications company) has made major investments in South Sudan since 2008. To date, Zain has

invested more than $300 million in their South Sudan network.

[5]

Government spending from resource-generated revenue contributed an additional 8 percentage points. See McKinsey & Company (2010).

[6]

In a 2010 interview with the Infrastructure Consortium for Africa, Bobby J. Pittman Jr., African Development Bank Vice President for

Infrastructure, Private Sector Development, and Regional Integration, noted the AfDB’s strong interest in high-return investments in African

infrastructure projects.

[8]

Fragile states record significant amounts of remittances from abroad. World Bank estimates for 8 of the 14 countries in the sample are that

remittances counted for an average of nearly 4 percent of GDP in 2009. During that year, the average for Sub-Saharan Africa was roughly 2.5

percent.

[13]

See appendix 6 for more in-depth information on how the Somaliland private sector helped stabilize an otherwise volatile business environment

in the subnational territory.

[16]

IFC (2010a). This includes institutions such as IFC, the European Bank for Reconstruction and Development, and MIGA.

[17]

Of IFC capital, 89 percent is invested in middle-income countries (DfID 2010). According to authors’ calculations, IFC’s 2010 commitments to

MICs were roughly $1.31 per capita, while commitments to African fragile states were only $0.31 per capita.

[18]

World Bank Group Development Committee (2011).

[20]

The developmental and financial returns gained from advisory service projects are far more ambiguous than returns gained from investment

projects (for instance, IFC received a 16.5 percent return on its organizationwide manufacturing equity investments in 2010). Therefore, much

of IFC’s work in African fragile states is difficult to quantify, and the full impact of IFC in these countries may not necessarily be

presented by the data analysis contained in this report. But the IFC’s own evaluation report completed by the World Bank Group’s Independent

Evaluation Group determined that advisory projects in “high-risk” business climates tend to have higher development effectiveness than those in

their non-high-risk counterparts. This same assessment applies to IFC investment projects in high-risk climates.

[22]

The PPIAF also manages the Private Participation in Infrastructure Database, which houses data on more than 4,600 infrastructure projects in

137 countries, including the Central African Republic, Sierra Leone, and Zimbabwe. The database has project-level reports on energy,

telecommunications, transport, and water and sewage sectors, which allow trend identification in the private infrastructure space.

[24]

FIAS implementation expenditures for 2010 totaled $18.5 million.

[25]

Another positive indicator is FIAS’s recent improvements (from 48 percent in 2008 to 77 percent in 2010) in the World Bank’s own Development

Effectiveness ratings.

[26]

Also in 2010, FIAS launched the Investing Across Borders report, which provides objective data on the climate for foreign direct

investment in 21 African countries, including Liberia and Sierra Leone. The report presents numerous indicators under the following four

categories: friendliness to foreign investors (that is, the percent of ownership allowed), ease of starting a foreign business, ease of

accessing industrial land, and complexity and length of the commercial arbitration process. See World Bank(2010b).

[27]

The only African fragile state without Doing Business coverage is Somalia.

[29]

Over the past decade, the average oil-exporting African fragile state’s GDP grew at a pace of between 3 and 11 percent, while the average

non-oil-exporting African fragile state grew at a pace of –1 to 5 percent (measured on an annual basis).

Constraints to business growth in African fragile states

One of the public sector’s primary objectives in assisting the private sector is to relieve constraints that may stifle businesses’ ability to grow,

expand employment opportunities, and generate profits. Recognizing this, donor organizations have increased funding over the last decade for private

sector development (PSD) diagnostics that help to identify these binding constraints. While there are a number of instruments available, we focus

primarily on two World Bank surveys: the Doing Business reports, which provide comprehensive assessments on regulatory, financial, and political

constraints through a top-down methodology; and the Enterprise Surveys, which gauge firms’ views about business environment constraints.

World Bank Doing Business Reports

Doing Business country (and subnational) reports provide relative and absolute measures of business environment constraints across eight distinct

categories, such as the ease and cost of starting a new business, enforcing contracts, and trading across borders. The Doing Business methodology

scores countries according to both the attractiveness of their current business environment (the number of days it takes to secure an import license)

and their progress toward delivering more private sector–friendly policies (the number of regulatory reforms that have been completed in a given year).

Overall, the Doing Business reports, providing the most comprehensive country coverage, are completed on an annual basis—which allows for more dynamic

monitoring of business environment changes and trends.

With few exceptions, African fragile states lag far behind their higher income and non-African fragile counterparts on nearly every Doing Business

measure. On average, African fragile states have an ease of doing business ranking of 171 (of 182 countries) compared with an average ranking of 125

for other low-income countries (table 3.1). Importing a standardized container of goods costs nearly three times more in African fragile states than in

middle-income countries.[1] And

starting a new business costs more than three times as much in African fragile states than in other low-income countries. These exorbitant operating

costs have a profound impact on businesses’ ability to generate profits, expand, and compete in a globalized marketplace.[2] Moreover, they contribute to

broader economic effects, such as inflation, large informal sectors, and rent-seeking behavior.

Table 3.1: Fragile states compared with other developing countries, Doing Business indicators

Income category

Overall ranking

Cost to import container ($)

Cost to start a business (percentage of GDP per capita)

Time to register property (days)

Time to enforce a contract (days)

Middle-income country

96

1,443

26

49

635

Low-income country

125

2,308

61

68

545

Africa nonfragile state

117

1,972

47

54

629

Non-African fragile state

125

1,968

69

132

650

African fragile state

171

3,596

184

96

722

Source: World Bank 2011b.

While Doing Business reports provide a useful assessment of business environment issues, they also omit several factors that impact PSD, such as

macroeconomic stability, security, quality of infrastructure, and corruption. As such, they should be used with other diagnostic instruments to

identify the most binding constraints on business growth in African fragile states.

World Bank Enterprise Surveys

The World Bank Enterprise Surveys compile individual firms’ opinions and concerns to assess national and regional business environments. The surveys

fill in many of the gaps in the Doing Business reports, such as corruption, physical infrastructure (including transport), crime, informality,

competition, and access to finance. Private contractors administer the surveys to firms largely in the manufacturing and service sectors, including

construction, transport, and information and communication technology. As of mid-2011, World Bank Enterprise Surveys were available for 12 of our

sample of 14 African fragile states.[3]

Despite their significant strengths, World Bank Enterprise Surveys have two key weaknesses. First, they are fairly expensive, time-consuming, and

infrequently completed (not annually or according to a clearly defined timetable). So they are not an ideal instrument for identifying country trends

over time. Second, the surveys focus almost exclusively on firms in the formal sector.[4] Since the informal sector

accounts for the overwhelming majority of businesses and employment in low-income countries, enterprise surveys may not adequately reflect constraints

impacting the broader business sector. Even so, while World Bank Enterprise Surveys may have limitations, they remain a very useful tool in gauging

firms’ views about major constraints.[5]

Ramachandran (2010) summarizes in detail the available survey data for African countries, along with analyzing trends between countries and income

groups.[6] Businesses in the

poorest African countries—in which most fragile states are included—tend to cite basic infrastructure deficiencies, access to financing, and lack of

macroeconomic stability as the primary constraints to profitability and expansion.[7] Other constraints, such as

weak governance, low administrative and bureaucratic capacity, and official corruption are cited more frequently in the next highest income tier of

Sub-Saharan countries (such as Kenya and Senegal). Businesses in the highest income group (such as Gabon and South Africa), on average, cite the lack

of job skills and labor regulation as more binding constraints.

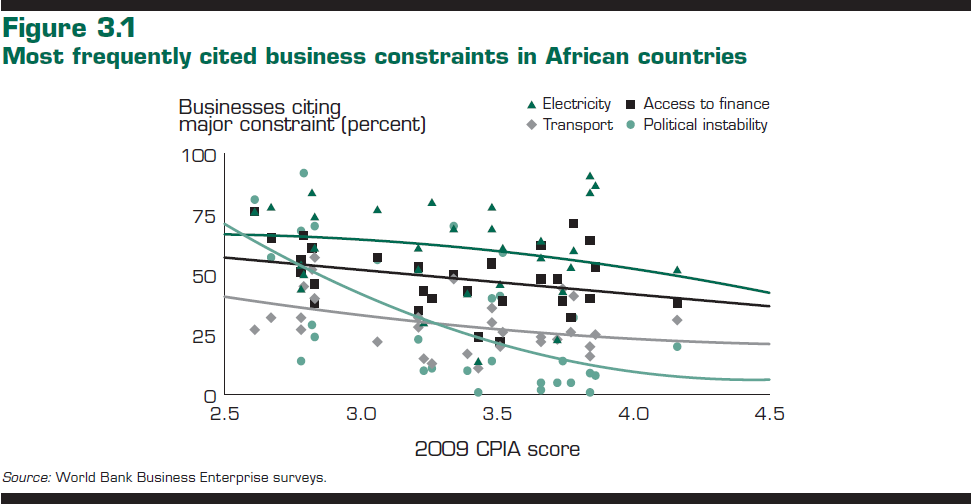

Since country fragility is defined according to policy and institutional quality measures, we also examine business constraints in relation to IDA

Resource Allocation Index (IRAI) scores (as opposed to income per capita levels). Figure 3.1 illustrates several of the most frequently cited business

constraints in African countries—political instability, transport infrastructure, electricity, and access to finance.[8] Across the board, the

percentage of firms reporting these issues as “major constraints” declines as countries’ IRAI scores increase. Not surprisingly, concerns about

political instability decline the most dramatically across our country sample. Nearly twice as many African firms cite concerns about electricity as a

“major constraint” compared with concerns about transport infrastructure. And access to finance is also cited more frequently as a “major constraint”

than transport infrastructure is.

For African fragile states, the most frequently cited business constraints include: electricity (68 percent), access to finance (56 percent), political

instability (56 percent), corruption (48 percent), taxation rates (40 percent), competition from informal firms (40 percent), transport (38 percent),

crime (35 percent), customs regulations (28 percent), and worker skills (27 percent; table 3.2).

Table 3.2: Most frequently cited business constraints in African fragile states (percent)

Country

Electricity

Access to finance

Political instability

Corruption

Tax rate

Competition from informals

Transport

Crime

Customs regulations

Worker skills

Angola

43.9

55.8

13.6

35.0

22.6

25.4

27.0

35.5

21.6

20.6

Burundi

76.5

56.6

56.3

18.1

33.6

39.8

22.1

21.2

20.4

15.5

Chad

81.6

47.4

68.9

66.9

54.4

71.3

45.9

51.5

58.1

59.7

Congo, Dem. Rep

78.4

64.9

56.7

21.3

52.6

45.5

32.0

20.6

19.8

16.2

Congo, Rep.

74.4

45.5

70.4

66.4

42.9

49.2

57.0

47.1

49.1

53.9

Côte d'Ivoire

50.1

66.2

92.2

71.7

40.8

32.8

44.7

54.9

27.3

37.7

Guinea

84.2

61.4

28.8

53.8

38.0

25.0

52.2

34.8

12.0

14.1

Guinea-Bissau

75.7

75.7

80.6

40.0

47.9

32.9

27.1

31.4

26.4

15.0

Liberia

60.8

37.7

23.5

38.2

26.0

22.7

40.3

30.6

17.4

13.0

Togo

53.8

50.8

68.3

66.1

40.5

52.0

32.3

22.2

30.2

19.5

Average

68.0

56.2

55.9

47.8

39.9

39.7

38.1

35.0

28.2

26.5

Other Sub-Saharan countries

51.0

41.0

17.0

32.0

39.0

34.0

25.0

27.0

20.0

22.0

Source: World Bank Business Enterprise surveys.

World Bank Group alignment with business constraints

The aforementioned surveys and analysis provide programmatic prioritization insights for respective donor organizations.

Since the World Bank Group expends significant resources on business diagnostics, we would expect International Development Association (IDA),

International Finance Corporation (IFC), and Multilateral Investment Guarantee Agency (MIGA) activities to direct their projects toward those factors

that pose a “major constraint” to PSD in fragile states.[9] Put differently, the World

Bank Group should be drawing upon individual firms’ opinions before developing and implementing sizable support programs and investments for

PSD-related activities.[10]

Methodology

To gauge the World Bank Group’s alignment, we focus on a subset of major business constraints that can be mapped clearly to World Bank Group projects

and investments, including electricity, access to finance, and transport infrastructure. The multifaceted dimension of other constraints—such as

political instability and crime—makes it difficult to identify overlap with donor programs in a concise manner.[11] For projects and

investments, we examine all IDA, IFC, and MIGA activities between 2000 and 2010 in 11 African fragile states with business enterprise survey data.[12] Moreover, we use each

institution’s classifications to determine the priority sector or area for each project, investment, or guarantee.[13]

IDA

As seen in a number of different measures, IDA projects over the last decade exhibit a significant level of alignment with firm views concerning

electricity and transport constraints. The correlation between the number of IDA projects targeting these sectors (measured as the percentage ofall IDA PSD-related projects) and the percentage of firms citing them as “major constraints” is 0.54 and 0.52, respectively.[14] As expected, there is

almost no correlation between the total value of IDA projects targeting these sectors (measured as the percentage of all IDA projects).

Put differently, IDA has prioritized electricity and transport projects within its PSD-related portfolio while not necessarily prioritizing them with

respect to its overall project portfolio value in African fragile states. Given broader development priorities that commonly exist in African

fragile states—such as social service delivery and security sector reform—this is not particularly surprising. By contrast, IDA’s alignment with firms’

concerns about access to finance is strikingly low. The correlation between IDA projects targeting this constraint (measured as a percentage of all PSD

projects) is only 0.04, suggesting that IDA has deprioritized financial sector projects in African fragile states—in the form of either regulatory

reform or support for local financial institutions (table 3.3).[15] ,[16] IDA’s low level of access

to finance projects could also be attributed to the comparative advantage of other World Bank Group subsidiaries (IFC) in this sector, which may be

better-equipped to promote access to finance.

Table 3.3: IDA alignment with “major constraints,” by country, selected measures [CLICK TO VIEW]

Figure 3.2 provides another illustration of IDA’s prioritization across the examined sectors according to the percentage of individual firms citing

them as “major constraints.” As the aforementioned correlation analysis suggests, IDA appears to prioritize PSD projects in electricity and transport

in African fragile states where they present the greatest constraints. Alternatively, IDA appears to pursue fewer financial sector projects when firms

cite access to finance more frequently as a “major constraint.”

IFC

Unlike IDA, IFC investment services focus on economic sectors (such as manufacturing and services companies) rather than broader constraints to PSD

growth. Conversely, IFC advisory services often work with governments to improve the overall investment climate in fragile states such as the

Democratic Republic of Congo and South Sudan. Neither investment nor advisory services focus explicitly on electricity and transport constraints, and

thus we expect that very few investments have targeted those obstacles to private business growth. However, we could expect IFC investments in the

financial services sector (to counteract the “access to finance” constraint).

IFC investments in recent years. Based on a number of different measures, IFC investments in African fragile states over the last decade exhibit almost no alignment with firm

concerns about binding electricity and transport constraints (figure 3.3 and table 3.4).[17] Indeed, the correlation

between the number of IFC investments targeting these sectors (measured as the percentage of total number of IFC investments) and the percentage

of firms citing them as “major constraints” is –0.25 and 0, respectively.[18] For electricity, possible

reasons for the misalignment are the highly regulated nature of electricity sectors in African countries and the limited openings for private

investment in public power projects. IFC has been successful in investing in Togo’s power sector, and it has been able to contribute to the

electricity-related regulatory dialogue in Liberia.

Table 3.4:IFC alignment with constraints, 2000–11 (percent)

Electricity

Transport

Access to finance

Firms citing as major obstacle

In-country project value

In-country project count

Firms citing as major obstacle

In-country project value

In-country project count

Firms citing as major obstacle

In-country project value

In-country project count

Angola

43.9

0.0

0.0

27.0

0.0

0.0

55.8

4.4

50.0

Burundi

76.5

0.0

0.0

22.1

0.0

0.0

56.6

3.3

40.0

Chad

81.6

0.0

0.0

45.9

0.0

0.0

47.4

10.5

50.0

Congo, Dem. Rep.

78.4

0.0

0.0

32.0

0.0

0.0

64.9

12.4

53.8

Congo, Rep.

74.4

0.0

0.0

57.0

0.0

0.0

45.5

0.0

0.0

Côte d'Ivoire

50.1

0.0

0.0

44.7

0.0

0.0

66.2

100.0

100.0

Guinea

84.2

0.0

0.0

52.2

0.0

0.0

61.4

0.0

0.0

Guinea-Bissau

75.7

0.0

0.0

27.1

0.0

0.0

75.7

100.0

100.0

Liberia

60.8

9.5

20.0

40.3

0.0

0.0

37.7

30.7

40.0

Sudan

41.0

0.0

0.0

22.0

0.0

0.0

45.0

0.0

0.0

Togo

53.8

9.7

20.0

32.3

0.0

0.0

50.8

3.8

20.0

Correlation

–0.25

–0.25

0.61

0.64

Source: International Finance Corporation and authors’ calculations.

Ultimately, however, the IFC is less likely, on average, to support investment deals in environments with more binding constraints, apart from access

to finance. The data illustrate IFC’s recent concerted efforts to target access to finance constraints in several African fragile states, including

Côte d’Ivoire and Guinea-Bissau. Recent IFC investments in these two countries are wholly concentrated in finance-related sectors.[19] While firm concerns could

signify strong market demand opportunities for IFC, the high respondent rates likely also signify regulatory distortions and other market risks that