The International Monetary Fund (IMF) and CGD kicked off the week of Spring Meetings with an event focused on financial inclusion. In her opening remarks, IMF Managing Director Christine Lagarde noted that financial inclusion is not just a priority for this year’s meetings but for the post-2015 development agenda as a whole. Here we explore both the benefits of financial inclusion and some concrete steps for achieving it, specifically looking at ways of overcoming a persistent gender gap that leaves women with less access to financial services than men.

The micro-level case for promoting financial inclusion is clear. Access to financial services allows individuals to save, invest, and insure their assets, which decreases their vulnerability to shocks, increases their incomes, and improves their lives. There is also a macro-level case for financial inclusion; bringing more people into formal financial systems can increase GDP growth and country-level stability.

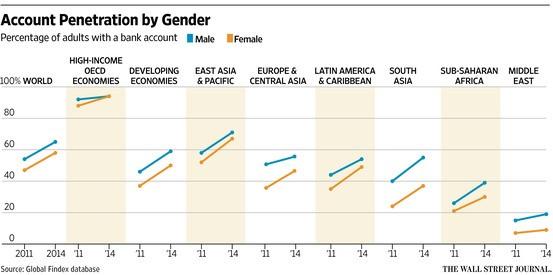

But while the number of formal bank accounts has increased significantly over the past few years, the gender gap in who has access to these accounts has not budged. Comparing Findex data from 2011 and 2014, we see that the 9 percentage point gap between men and women’s access to bank accounts in developing economies has not shrunk. And among the poor, this gender gap is larger still. In the Middle East, women are half as likely as men to have an account, and South Asia has the largest gender gap in absolute terms, at 18 percentage points.

If we don’t view financial inclusion through a gender lens, these gaps are likely to persist into the future. Meaningful financial inclusion will require doing something more and something different to bring women into the financial system. Fortunately, robust new knowledge hints at what can be done: as we mentioned in our last blog – in seeking financial services or any other type of service provision – men and women have different preferences and are subject to different constraints that shape their interactions with banks and the products they offer. So far, a lot more attention has been paid to particular constraints women face in accessing financial services, including mobility constraints, low financial literacy, and lack of collateral, than to what women actually want out of financial products.

What Do Women Want?

Women show a distinct preference for savings, perhaps because they tend to be more risk averse than men and may prefer to keep savings in case of emergencies and use their own savings, rather than borrowed capital, when making business investments. Secure savings accounts may also provide a good vehicle for women to hide or protect their money and resist asks from spouses or relatives.

A unique longitudinal data set from commercial and state banks in Chile backs this preference, showing that a majority of Chilean savings accounts are in the hands of women. From 2002 to 2014, the percentage of savings accounts held by women increased from 50 to 58 percent of all individual accounts (while women are still a minority of those seeking credit). Outside of Chile, recent evidence from field experiments in countries including Kenya and the Philippines shows that providing women with savings helps them to have greater control over their money and grow their business incomes.

What Can Be Done to Close the Gender Gap?

Given what we increasingly know about women’s preferences, what should banks do to reach the goal of full financial inclusion?

Design with A Nudge: Banks (and other financial service providers) need to customize products to meet women’s needs and include design nudges to help them save. Secure, confidential savings, especially commitment savings, provide women with greater legal and psychological control over funds, shield women from family pressures to share cash with others, and help overcome a tendency to spend now instead of saving for later. These constraints related to internal and external pressures are either specific to women or greater for women than men, so providing women with access to secure and private savings accounts and building in commitments (as well as reminders) to save can help overcome gender-specific hurdles. Mobile technology in particular is an asset, as it provides privacy and overcomes the mobility restrictions that many women face.

Add A Twist: Financial service providers need to examine gender biases in the supply of financial services, and un-bias the delivery of these products. In addition to “Know Your Customer” requirements, the industry should have “Know Your Bank” standards as well, so that we can better understand whether players in the formal financial sector operate in gender-equal ways.

Are banks open during hours and in locations that women can access? Do banks advertise products with a potential female as well as male clientele in mind? Do banks have female banks managers and bank agents, or are they male-dominated workplaces? Do bank agents make equal efforts to serve women clients as they do men? Importantly, do banks believe that increasing the female clientele makes business sense? A stronger “Know Your Organization” framework will provide us with the answers to these types of questions, allowing banks to examine and change their internal gender biases.

Monitor Progress: As we’ve emphasized in previous blogs, monitoring progress on financial inclusion will require sex-disaggregated data on the supply as well as the demand side for financial services. A new partnership – one including Data2X, the Global Banking Alliance for Women, the Inter-American Development Bank (IDB), the World Bank, the International Finance Corporation (IFC), and the IMF – is working to increase the collection of sex-disaggregated data by both financial regulatory bodies and commercial banks.

(Rigorously) Experiment: As system-level biases are being examined, now is the time to test innovative ways to increase women’s access to and ability to use financial services, and specifically the savings products that meet their needs. Along those lines, CGD is currently evaluating mobile savings pilot projects in Indonesia and Tanzania.

CGD, in collaboration with J-PAL and affiliated researchers from the Kellogg School, the London School of Economics, and the University Pompeu Fabra (Indonesia) and the World Bank’s Africa Gender Innovation Lab (Tanzania), is running randomized controlled trials (RCTs) designed to measure the impact of supply and demand side interventions on women’s ability to access and use mobile savings platforms. In Indonesia, we’re looking at Bank Mandiri’s new branchless banking initiative, which seeks to provide access to financial services through mobile phones. Working with Bank Mandiri and Mercy Corps Indonesia, we’re testing the impact of monetary incentives and training (delivered to branchless bank agents) on these agents’ likelihood of targeting female clients, and whether women in the rural provinces of East Java are more likely to adopt and use mobile savings products as a result.

In Tanzania, we’re examining telecommunications company Vodacom’s savings platform M-Pawa and whether various levels of technical and financial literacy training delivered by TechnoServe to women business owners will increase their take-up and use of the M-Pawa product. Stay tuned for whether these particular interventions effectively contribute to closing the financial gender gap.

CGD’s work to evaluate mobile savings programs for women in Indonesia and Tanzania is supported by the ExxonMobil Foundation.

Disclaimer

CGD blog posts reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions.