Recommended

“Trade not aid” is a slogan that appeals to certain instincts on both the left and right. The idea being that rich countries can do more for economic development in poor countries by granting them market access than by sending charity. But will market access really stimulate economic growth in lagging regions?

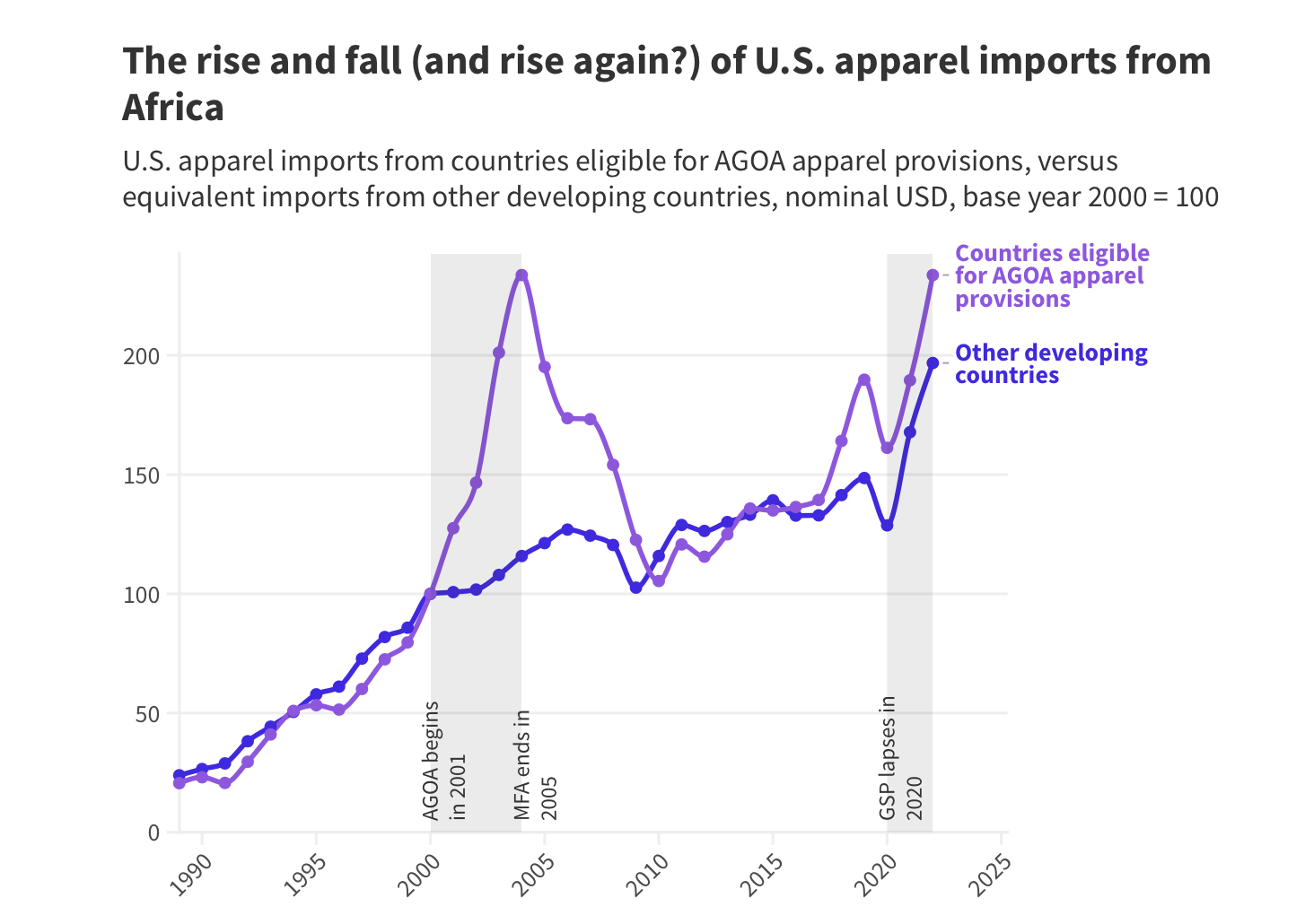

In 2001, the bipartisan Africa Growth and Opportunity Act, or AGOA, granted duty-free access to thousands of products from African countries, everything from crude oil to t-shirts. But the results have been mixed. An initial US-Africa trade boom was extremely short-lived.

AGOA is up for renewal in 2025. In a new CGD working paper, we argue that a simple extension of AGOA is unlikely to do much for Africa’s structural transformation. Instead, we put forward some ideas to give AGOA considerably more punch, including

- restoring the competitive advantage African countries enjoyed in AGOA’s early days (but which has since eroded) through negative tariffs and

- redirecting US investment subsidies in Africa from extraction of primary products toward industrialization and job creation.

The goal of these proposals is not just to boost US-Africa trade, but specifically to promote Africa’s structural transformation through export-led manufacturing at a critical time when China is rapidly vacating this space.

Why the AGOA boom went bust (Hint: the first China shock)

Once AGOA took effect in 2001, the impact was fast and furious. Garment exports—the classic example of a labor-intensive manufacturing sector—were the big story, accounting for nearly 80 percent of the tariffs waived under the program. Within five years of AGOA’s passage, African garment exports to the US had grown by 150 percent, with new factories opening up in Kenya, Lesotho, and Mauritius.

But by 2010, those exports were almost back at their 2000 level.

The crucial context to understand this rise and fall is that, circa 2001 when AGOA was launched, global textile trade was still governed by the arcane Multi Fiber Agreement (or, technically, by its successor, the Agreement on Textiles and Clothing). These treaties imposed quotas or caps on garment exports from specific developing countries to rich countries. The practical effect was to prevent China from dominating the market. Meanwhile, AGOA offered African countries a way around the barriers. Thus from 2001 to 2005 Africa had not only a tariff advantage over other competitors, that advantage was much bigger than it looked on paper due to the quota system.

In 2005 those global textile treaties expired, Chinese competition flooded the market, and Africa’s manufacturing boom ended.

Idea #1: Re-establish Africa’s tariff advantage over competitors

During the early-aughts “AGOA boom”, African apparel exports enjoyed a double advantage over global competitors, including China. They not only faced zero tariffs, they bypassed quotas. Studies in the 1990s typically estimated those quotas were equivalent to an additional tariff on the order of anywhere from 10 to 100 percent on garments from various Asian countries. So Africa’s advantage was huge—and most of it disappeared in 2005. Looking ahead, as China loses competitiveness in low-skill manufacturing, countries such as Vietnam have benefitted as they are part of the Chinese supply chain. Competing against them will require a compensatory boost.

To re-establish that tariff advantage—or, more likely, to level the playing field against ferociously competitive Asia—we propose a simple but fairly radical tweak to AGOA starting in 2025: negative tariffs.

Since AGOA tariffs are already at zero, the only way to open up a price incentive for production in Africa at this stage without totally tearing up the World Trade Organization (WTO) rules would be to cross into negative rates. While unconventional, we find that such tariffs—think of them as targeted manufacturing subsidies for extremely lagging regions—would be both effective and cheap.

On the cost side, AGOA currently costs the US about $250 million per year in foregone tariffs. (That’s probably an overestimate for reasons we discuss in the paper.) Compare that to total US foreign assistance for Africa, which was about $18 billion in 2022 (including all economic, humanitarian, and military aid). That means AGOA costs the equivalent of about 2 percent of US aid to Africa, and that “cost” is really just taxes the US waives on American importers.

Strengthening AGOA to include negative tariffs would present costs of a similar order of magnitude. We estimate a 10 percentage point negative tariff on apparel products would “cost” about $291 million in foregone revenue, while a 20 percentage point negative tariff would be more expensive, at about $880 million.

The benefits would potentially be large. We estimate that a 10 percent negative tariff would create about $1.5 billion in new trade, and a 20 percent tariff nearly $3 billion.

Table 1. Implied impact of a negative tariff on African apparel imports to U.S.

| 10% negative tariff | 20% negative tariff | |||

|---|---|---|---|---|

| Benchmark estimate from Table 2, columns [2] and [3] | High end estimate (top of 95% confidence interval) | Benchmark estimate from Table 2, columns [2] and [3] | High end estimate (top of 95% confidence interval) | |

|

Total increase in African exports to U.S. ($) |

$1.48 billion in new trade |

$2.94 billion in new trade |

$2.97 billion in new trade |

$5.88 billion in new trade |

|

Percentage increase over 2022 |

104 percent increase |

percent increase |

208 percent increase |

411 percent increase |

|

Marginal cost to U.S. Treasury in foregone revenue/rebates |

$291 million |

million |

$880 million |

$1.46 billion |

Attentive readers will note that we already lamented that the AGOA apparel boom collapsed after 2005, so why do we think doubling down is a good idea? Empirical analysis in our paper shows that while AGOA’s impact has attenuated, it remains statistically significant and non-trivial in magnitude. Furthermore, it is exclusively concentrated in products where Africa’s tariff advantage is big. Where other countries pay high tariffs, AGOA boosts African exports; where they don’t, it doesn’t. This demonstrates the importance of restoring Africa’s tariff advantage to its early 2000s levels.

Idea #2: Redirect US investment subsidies in Africa from extractives to manufacturing

If capital markets function perfectly, then if America provides tariff incentives to expand manufacturing in Africa, new private investment in African garment factories should follow.

In the real world, policy action on the investment side may be necessary. India, for example, has allocated about $1.3 billion by way of production subsidies for its textile and clothing sector. Since Africa might potentially have more and more serious binding constraints, a greater allocation might be warranted.

Many African economies are, however, fiscally strapped with high debt burdens and other pressing needs, which render infeasible the provision of similar subsidies. The US could take the lead in addressing this challenge. It could set aside, say, $2.5 billion (implying about a 15 percent increase in US foreign aid to the region) as venture capital to build manufacturing supply chains in Africa. The binding constraints which industrial policy would try to overcome would be several: political risk, business risk, small market size, etc. Africa needs to attract large companies that can create and sustain competitiveness in manufacturing.

The US International Development Finance Corporation (DFC) has been established precisely to address these problems.

To date, DFC has performed well at delivering finance to lower-middle income countries, but struggled to find projects outside of banking and insurance in the more labor-intensive sectors of the “real” economy. In fiscal year 2023, the agency committed over $2 billion for projects in Africa, and around $1.3 billion for projects in the manufacturing sector, but just $50 million for manufacturing in Africa. Since fiscal year 2020, it has committed just $200m for African manufacturing compared to $2.2 billion for mining, oil, and gas extraction in the region. In a sense, America’s marquee effort to finance private sector activity in the developing world is tilting against African industrialization—financing industrialization elsewhere, while focusing on mining and public administration in Africa.

Strengthened AGOA trade preferences could serve as a pull mechanism to create bankable projects for DFC to lend to and invest in, reorienting its work away from financial services towards job creation and industrialization.

AGOA 2.0 would benefit from two of Washington’s current intellectual fads: friend-shoring and industrial policy

Exporting light manufactured goods like t-shirts, shoes, and toys has been the first rung on a ladder of rapid economic growth and development for most of the newly industrializing countries in the twentieth century.

There is an ongoing debate among economists about whether that ladder exists anymore, or whether automation and a shift in demand in favor of services over manufacturing requires a new model. For Africa, with only a toe-hold in global manufacturing, the answer seems clear: global demand is not a meaningful constraint.

Geopolitically, it’s a good time for the US to make an ambitious push on African industrialization.

After dominating global apparel exports in the 2000s and 2010s, China’s market share is now in decline, falling from a peak of 38 percent of American apparel imports in 2010 to 24 percent in 2022, as the country graduates to more capital- and skill-intensive industries.

As multinational companies pursue “China + 1” strategies to diversify their investments outside of mainland China, the US is attempting to redirect its own import purchases to geopolitical allies through “friend shoring.” A window of opportunity has opened for other entrants into the light-manufacturing export sector.

Simply renewing AGOA “as is” won’t be enough to enable African economies to compete. But stronger policy tools exist; evidence suggests they’re affordable and could significantly boost the continent’s industrial output.

Trade not (just) aid, and investment in manufacturing in Africa, not just extracting raw materials from Africa, should be the new mantra for policymakers as they contemplate possibilities for AGOA 2.0.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.