The COVID-19 pandemic has left a large dent in the government budgets of low-income countries (LIDCs). During 2020, they had no choice but to increase public spending to fight the pandemic at a time when shrinking economic activity depressed their revenues. Consequently, public debt rose by 5 percentage points on average in this group of countries in 2020, to 46 percent of GDP. This happened despite the delivery of more than $5 billion in relief to over 40 LIDCs under the Group of Twenty (G20) Debt Service Suspension Initiative launched in May 2020. A $650 billion increase in IMF reserve assets—Special Drawing Rights (SDRs)—could be distributed to member countries in August 2021 with about $23 billion going to sub-Saharan African countries. Discussions are currently underway to devise a mechanism allowing advanced economies to on-lend part of their SDRs, to expand concessional resources available to LIDCs. The recently concluded Group of Seven (G7) meeting set a goal of $100 billion SDR contributions from advanced economies to support the poorest and most vulnerable countries in dealing with the consequences of the pandemic.

In this blog post, we argue that while these efforts to expand the flow of concessional resources to LIDCs are laudable, they are unlikely to be sufficient and, going forward, some form of debt relief will be necessary to secure fiscal sustainability down the road for these countries. Our argument is based on a detailed analysis of the experience with fiscal tightening in LIDCs during 1979-2019 using a more comprehensive database than previously employed (the full set of results will be made available in a forthcoming paper). Absent debt relief, LIDCs are likely to suffer from uneven growth and a worsening of income inequality. Already, more than half of the LIDCs (36 of 59) are either in or at high risk of debt distress. The average interest payments as a share of GDP of LIDCs have risen to almost 1.6 percent in 2019/20, similar to the level prevailing prior to the launch of the Heavily Indebted Poor Countries (HIPC) Initiative in 1996. The rising share of interest payments in more recent years reflects the changing composition of debt, with a growing proportion of non-concessional borrowing.

Fiscal tightening going forward

LIDCs are expected to tighten their fiscal position in the coming years to help contain further increases in debt. This emerges from the analysis presented in the IMF’s April 2021 Fiscal Monitor, which projects a median improvement in the primary fiscal balance (the budget balance net of interest payments) of 2.5 percentage points of GDP between 2020 and 2025 for 40 LIDCs. Fiscal tightening is expected to take place in over 90 percent of these LIDCs.

What can we learn from past episodes of fiscal tightening?

Several lessons emerge:

First, fiscal tightening in LIDCs is uncommon. Over the past 40 years, LIDCs undertook fiscal tightening just around 20 percent of the time, that is, on average once in five years. Even for countries that needed fiscal tightening to stabilize their public debt ratios—that is, where the primary balance needed to be reduced to put the debt-to-GDP ratio on a declining path—fiscal tightening happened just around 14 percent of the time.

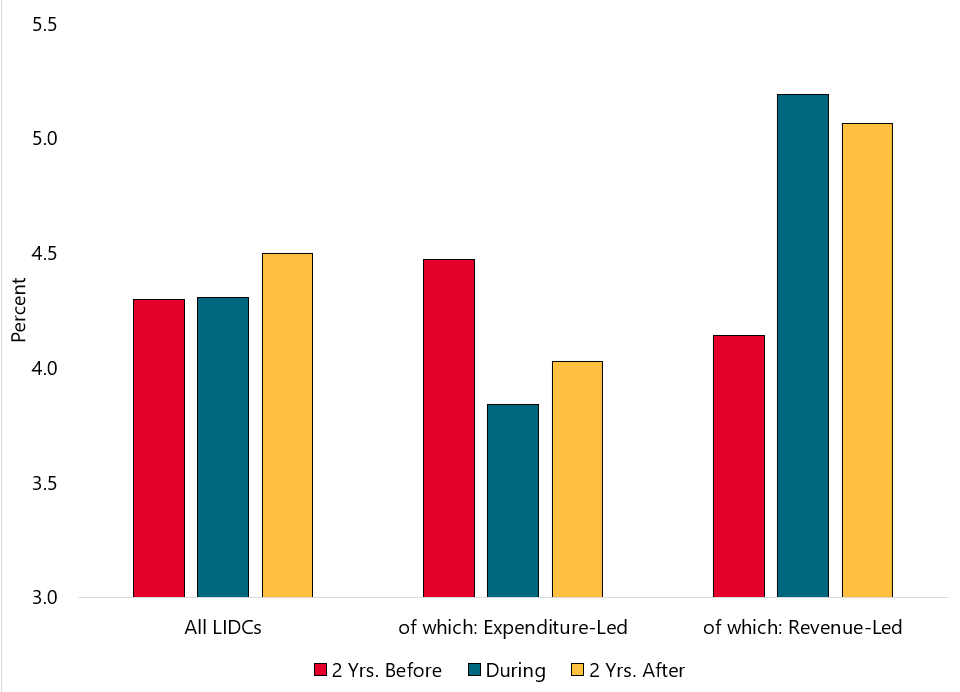

Second, fiscal tightening in LIDCs tends to be short-lived and is often partially reversed. Around 70 percent of the fiscal tightening episodes lasted just 2 years. The median annual improvement in the primary balance was 1.7 percent of GDP (Figure 1). However, periods of fiscal tightening were often partially reversed: in the two years following the fiscal tightening, median primary balances worsened by about 0.8 percent of GDP per year. This contrasts with fiscal tightening experiences in advanced economies, where such slippages are much smaller at 0.2 percentage points. This pattern of giving back some of the gains achieved during the tightening episodes casts doubt on fiscal projections for LIDCs that assume a steady and continuous decline in governments´ budget deficits. This pattern of fiscal tightening in LIDCs is similar to the one found in emerging market economies, except that a larger proportion of gains from fiscal tightening are retained after two years in the former.

Figure 1. Median annual change in budget balance around a fiscal tightening, by income classification

Source: Authors’ calculations using the HP filter and data from the April 2021 IMF World Economic Outlook (WEO) Database. Note: “Budget Balance” refers to the cyclically adjusted primary balance (CAPB). “Fiscal Tightening” is defined as a minimum annual improvement in the CAPB-to-GDP ratio of 0.5 percentage points (pp) over two consecutive years as defined by Alesina and Perotti, “Fiscal adjustments in OECD countries: composition and macroeconomic effects”. IMF Staff Papers, 44(2), 210-248 (1997).

Third, economic growth falls (rises) when fiscal tightening relies largely on cuts in public spending (revenue increases) (Figure 2). In expenditure-led tightening, expenditure cuts (rather than revenue increases) account for the majority of the fiscal tightening. Revenue increases allow countries to maintain or even raise spending that can help boost growth over the longer term, which may also help explain their better growth performance in the two years following the fiscal tightening. Revenue increases allow median spending to expand by 1.5 percent of GDP during the fiscal tightening, which is sustained even after the tightening phase elapses.

Figure 2. Median annual real GDP growth around a fiscal tightening in LIDCS, by tightening type

Source: Authors’ calculations using the HP filter and data from the April 2021 IMF World Economic Outlook (WEO) Database. Note: Median real GDP growth rates are calculated for a sample of 116 fiscal tightening episodes in LIDCs (of which 67 are classified as expenditure-led and 49 as revenue-led) during the period 1979-2019. A fiscal tightening episode is defined as expenditure-led if the cumulative change in the primary expenditure-to-GDP ratio divided by the cumulative adjustment (defined as the sum of all annual changes in the CAPB-to-GDP ratio) is larger than (or equal to) 0.5 (with the episode being defined as “revenue-led” otherwise). See Figure 1 for further elaboration.

Fourth, revenue-led fiscal tightening is associated with much lower public debt (by about three times) relative to expenditure-led tightening (Figure 3). While fiscal tightening does lower public debt, LIDCs adopt this policy infrequently (see point 1 above) and do not persist with it over a long period. What is more, a smaller proportion (42 percent) of fiscal tightening episodes in LIDCs is driven by increased mobilization of domestic revenues. In any case, it would seem inappropriate at this stage to embark on fiscal tightening when the IMF has estimated that scarring from the COVID-19 pandemic has raised average spending by 2.5 percent of GDP in LIDCs, over and above the amounts needed to meet the Sustainable Development Goals by 2030.

Figure 3. Median annual change in gross debt in LIDCS around a fiscal tightening, by tightening type

Source: Authors’ calculations using the HP filter and data from the April 2021 IMF World Economic Outlook (WEO) Database. See Figures 1 and 2 for further elaboration.

Finally, income inequality worsens after both expenditure- and revenue-led fiscal tightening (Figure 4). This result is consistent with previous research on fiscal tightening and inequality in developing countries. In expenditure-led tightening, there is a temporary reduction in inequality during the tightening period, but this is more than reversed in the post-tightening period. Further research is needed to isolate the ways (and causal channels) through which fiscal tightening affects inequality.

Figure 4. LIDCs: Median annual Gini coefficient in LIDCs around a fiscal tightening, by tightening type

Source: Authors’ calculations using the HP filter and data from the April 2021 IMF World Economic Outlook (WEO) Database and the Standardized World Income Inequality Database (SWIID). Note: “Gini Coefficient” refers to the “net” (post-tax/transfer) Gini coefficient. See Figures 1 and 2 for further elaboration.

The above results have important implications for fiscal policy design in LIDCs and the need for additional external flows. First, with expenditure needs rising in the aftermath of the COVID-19 pandemic, LIDCs are likely to find it difficult to embark on fiscal tightening to reduce their debt-to-GDP ratios. This implies that debt forgiveness may need to be part of the package to help LIDCs get debt back to its pre-COVID-19 pandemic levels. Second, countries are rarely able to stick with fiscal tightening for a very long time. Thus, some allowance for slippages should be incorporated into fiscal projections. Third, the design of fiscal tightening seems to matter for performance. Revenue-led tightening is associated with larger debt reductions compared to tightening based on expenditure cuts. And, finally, fiscal tightening tends to be associated with higher inequality, underscoring the potential need for safety nets to compensate vulnerable groups.

Benedict Clements is a Professor at the Universidad de las Américas en Ecuador.

João Tovar Jalles is an Assistant Professor at the University of Lisbon.

Victor Mylonas is a graduate student at the University of Chicago.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}