Women own more than half of all micro, small, and medium enterprises in Indonesia. But of the estimated 22–33 million businesswomen in the country, most operate informal unregistered microenterprises, with significantly fewer assets and profits than men’s.

The stark gender inequalities in entrepreneurial ventures are evident in our baseline analysis of women and men entrepreneurs in East Java.[1] That analysis showed that business assets and outcomes are skewed 2 to 1 in favor of the men. Only 32% of the observed gap in earnings is explained by differences in characteristics (age, marital status, education, cognitive ability, risk taking, and business and household assets) that give men entrepreneurs a headstart over women.[2] So, to unlock these women’s economic potential, policies must go beyond equalizing characteristics between men and women to addressing social customs and gender discrimination in service provision that tilt business environments in favor of men.

Ongoing study of supply- and demand-side interventions

An ongoing randomized controlled trial (RCT) to study the effectiveness of supply- and demand-side interventions on the constraints to women entrepreneurs’ access to mobile savings offers early indications of efforts to empower women and equalize business environments in East Java (see box).[3]

The mobile savings RCT design. A random sample of 4,828 business owners (59% women and 41% men) was selected for the study in 401 villages in East Java in which mobile savings products were available. Half of the 2,800 women were randomly selected and offered an average three-hour group session for training in financial literacy, including information on using mobile phones for banking, signing up for a mobile savings account, and engaging in profitable business practices.

At three subsequent group mentoring visits, the businesswomen could ask questions and practice what they had learned in the financial literacy training, to test whether the training and the mentoring affect women’s uptake of mobile savings products (therefore addressing demand-side constraints). The other half of the women and all of the men did not receive the training but could sign up for the mobile product (control).

The supply-side intervention tested whether financially incentivizing village bank agents increases uptake of mobile savings products. It recruited 400 male and female branchless bank agents (at least one per village, 47% of them women) to receive two levels of monetary incentives for signing up clients. Half were randomly assigned to receive a low incentive payment (Rp. 2,000, about $0.15), and the other half a high incentive payment (Rp. 10,000, about $0.77). All agents received training, including on the importance of targeting the financially underserved, especially women.

Testing supply and demand

Village-based branchless bank agents randomly received low or high financial incentives to promote mobile savings products to new customers. Half of the businesswomen randomly received group training and mentoring to increase uptake of the mobile savings products. All bank agents received training on the product and information on the importance of targeting the underserved, especially women.

2,800 women entrepreneurs (+2,000 men entrepreneurs)

- 1,200 women (mobile savings)

- 1,600 women (mobile savings + group financial literacy training and mentoring)

400 branchless bank agents (men + women)

- 200 agents (low incentives + training)

- 200 agents (high incentives + training)

Short-term results—one year after baseline survey

The results reported here summarize findings from a survey in early 2018 to roughly half the total sample, about a year after the baseline survey. The data are for 2,319 entrepreneurs: 1,344 women and 975 men from 200 villages. Data were also gathered from bank administrative records on 189 agents from the same villages and on total mobile financial transactions by village.

Logistical problems with agent recruitment and training, which had to be phased over several months, and connectivity problems with the mobile platform (both now resolved) delayed full implementation of the supply-side treatment and slowed the businesswomen’s training and mentoring. These problems, and the resulting delay, were the reason for restricting the short-term measure to half the sample and for focusing the analysis of the survey results solely on the businesswomen. More than three-fourths (77%) of these businesswomen responded to the survey a month or less after they received the last group mentoring.[4]

The short-term results suggest that the financial literacy training plus mentoring was effective and that it led to increased businesswomen’s savings and e-savings, as well as to both “empowerment” and more general welfare effects, particularly in villages where branchless bank agents were receiving higher incentives.[5] Here are the results in more detail:

-

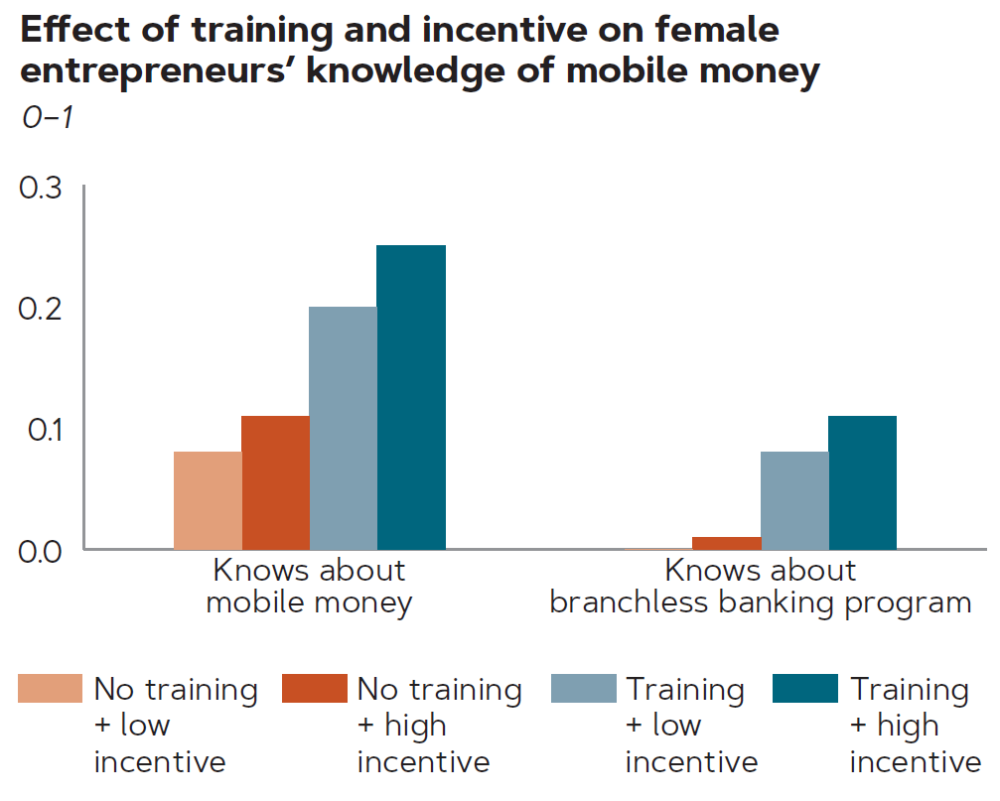

The training increased women’s knowledge of mobile money generally and mobile savings in particular. The training had a highly significant effect in increasing women’s knowledge of mobile money and mobile savings (see figure). These direct outcomes were positively (but not significantly) affected by the level of incentives given to bank agents.

-

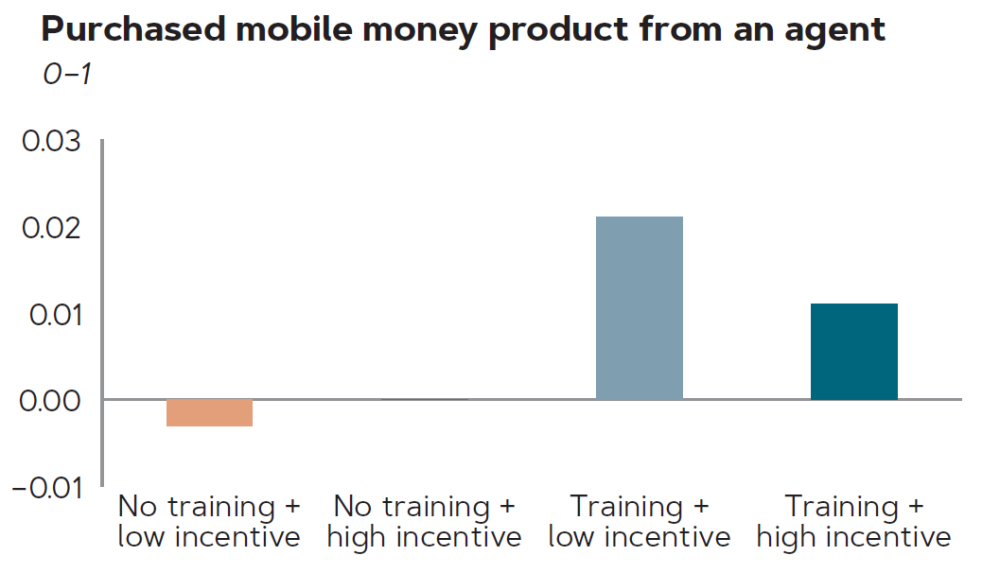

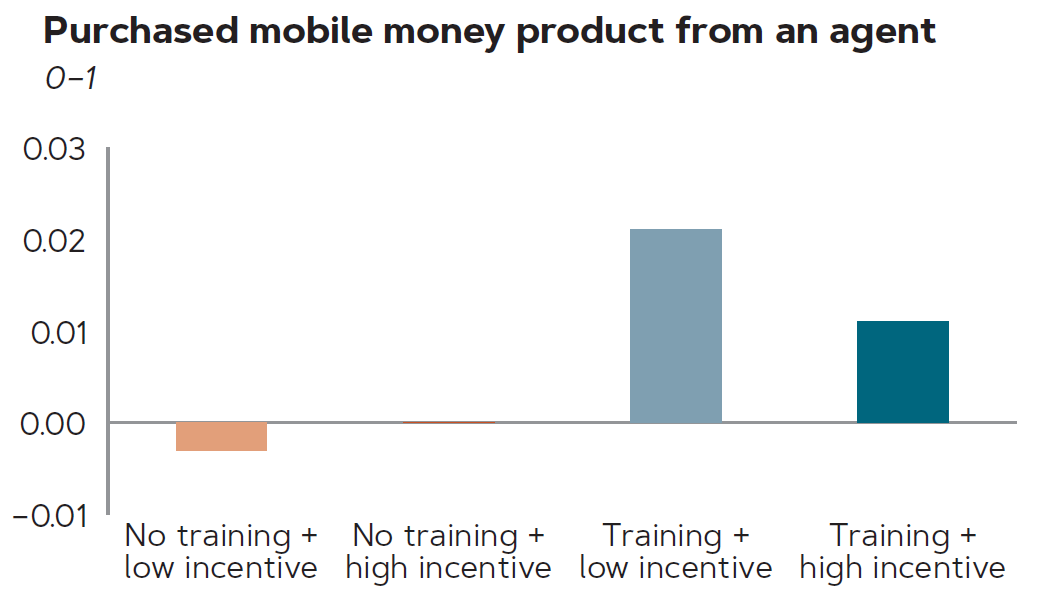

The training—and additional knowledge—also increased businesswomen’s likelihood of opening a mobile saving account. This effect is significant but small (owing to delays in recruiting agents and providing a fully operational mobile platform). Bank agents’ incentive levels had no significant effect on this outcome (see figure).

-

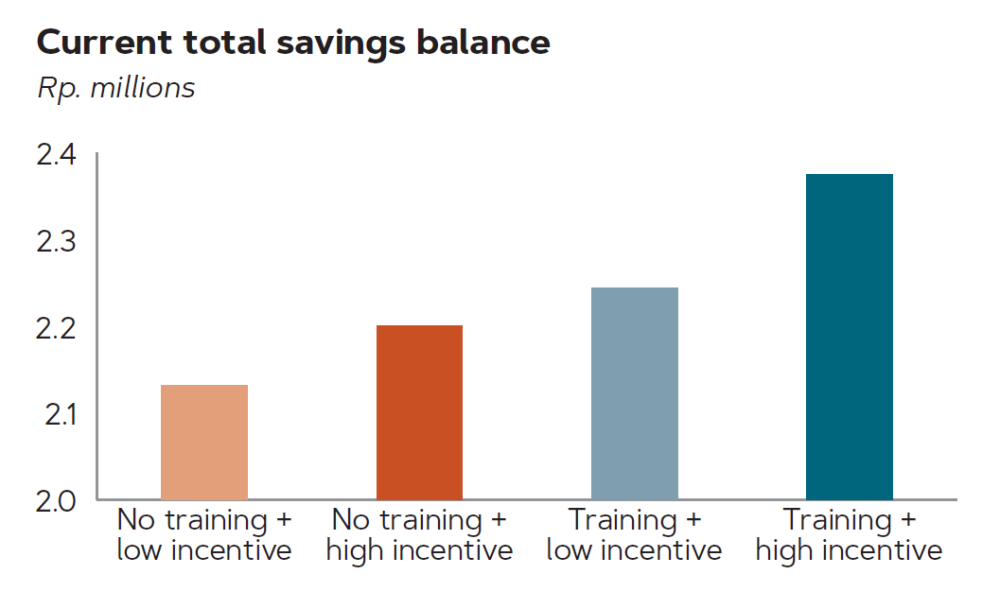

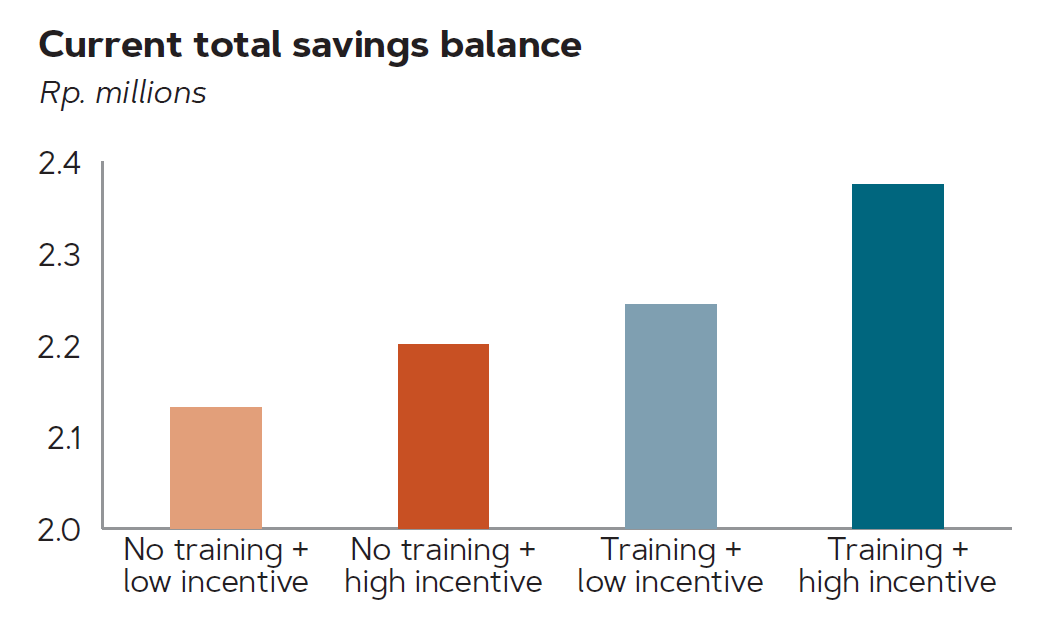

Women who were trained and exposed to more highly paid agents significantly increased both their total savings and their e-savings balances. Women who received training and were in villages served by bank agents with high incentives significantly increased their current total savings balances by 24% (see figure) in different forms of savings, including a small but significant increase in e-savings (1.4%) and e-savings current balance (4%). Women who were in villages served by high-incentive agents but were not trained and women in the training group but in villages served by an agent paid low incentives also increased current savings balances by 7% and 11%, respectively, but these increases did not reach statistical significance.

-

There were, however, no significant effects on reported business outcomes (business assets, revenue, profits, numbers of paid and unpaid workers, establishment of a second business). The lack of significant effects of the training and the agent incentives on business outcomes could be related to the supply-side treatments not being fully operational during the entire reporting period. So, it is difficult to make inferences about the interventions’ possible lack of economic impacts.

-

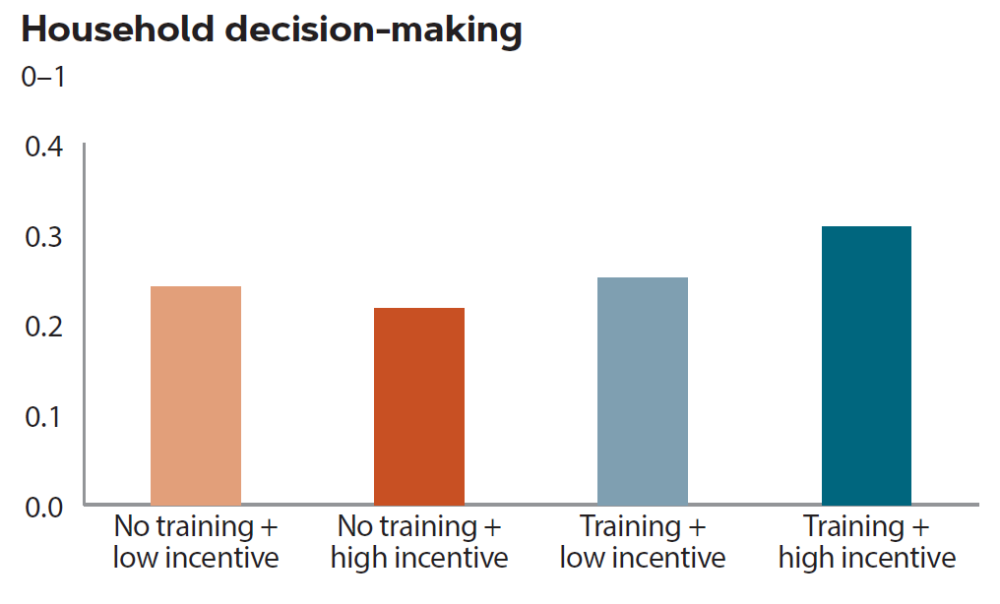

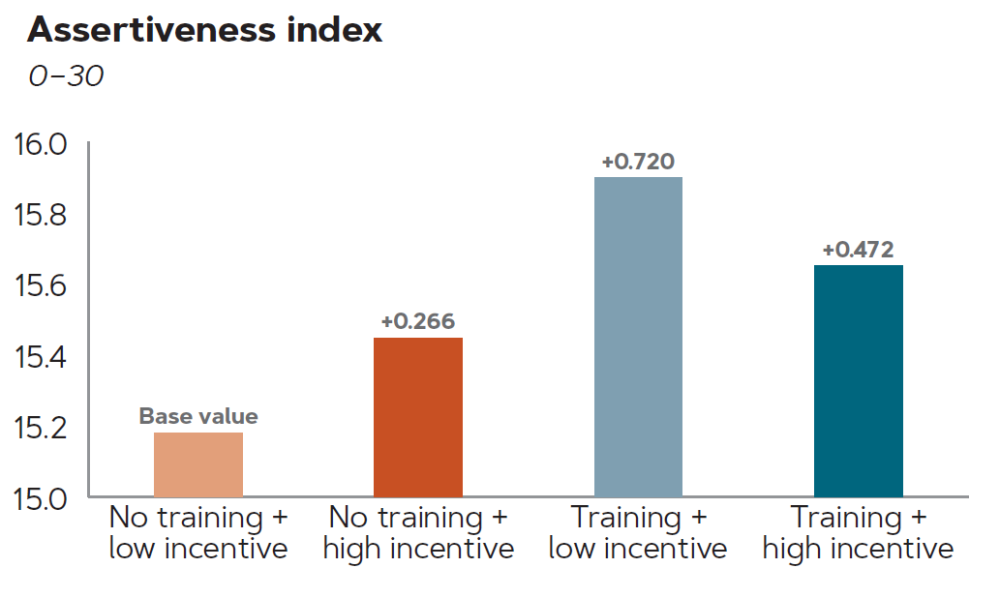

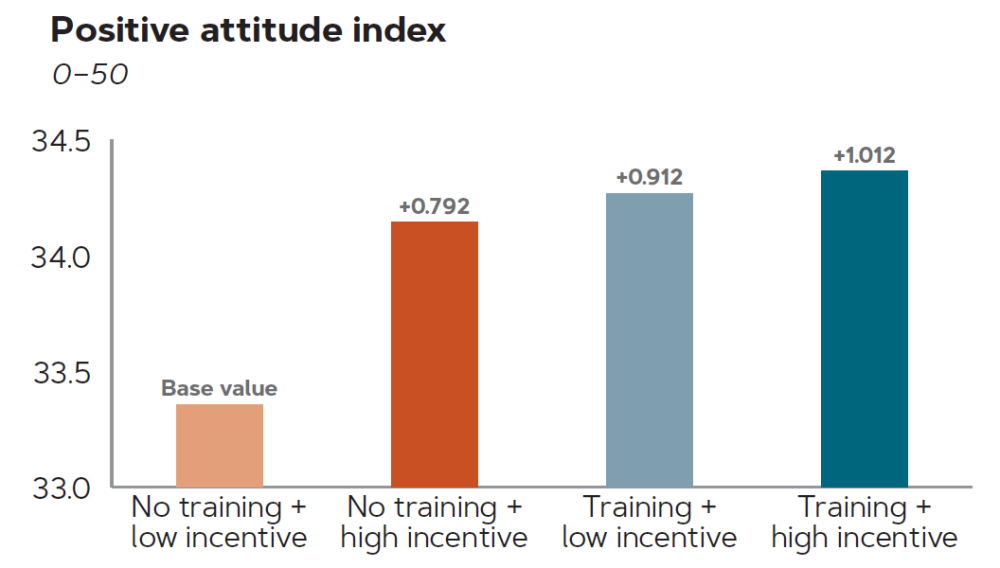

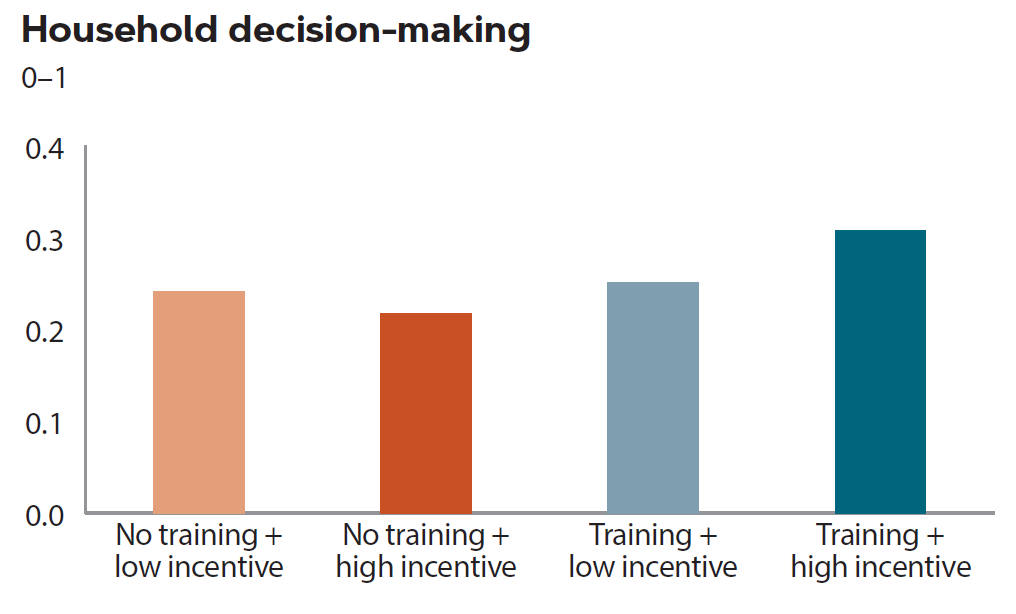

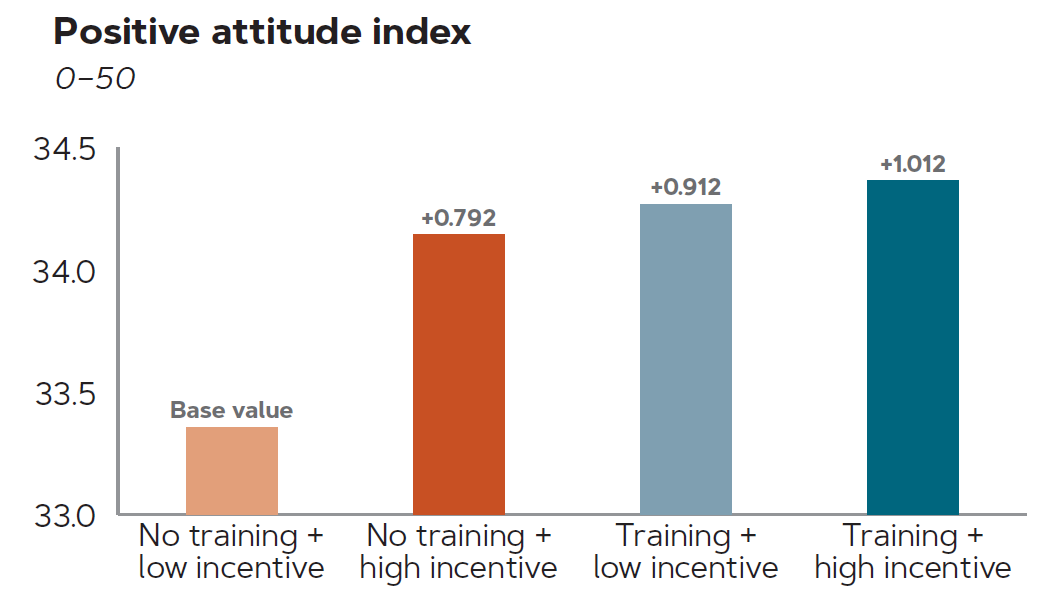

The training and mentoring combined with the presence of agents with high incentives increased the likelihood of women reporting that they were the sole decision-makers on several household decisions. In the presence of agents with high incentives, training and mentoring had a significant positive effect on one dimension of female empowerment, an index based on responses on who makes key household decisions. In addition, the training and high incentives both individually and in combination had a significant positive effect on women’s self-confidence, as measured by indexes of women’s assertiveness and positive attitudes (see figures).

These empowerment effects are mediated by increases in savings. An increase in private savings likely encouraged women’s economic self-reliance and self-confidence. Self-confidence was likely also bolstered by increased financial literacy and knowledge about mobile savings and perhaps also by the social validation from training and mentoring with peers. Self-confidence was also possibly reinforced by being served by a better paid agent.

-

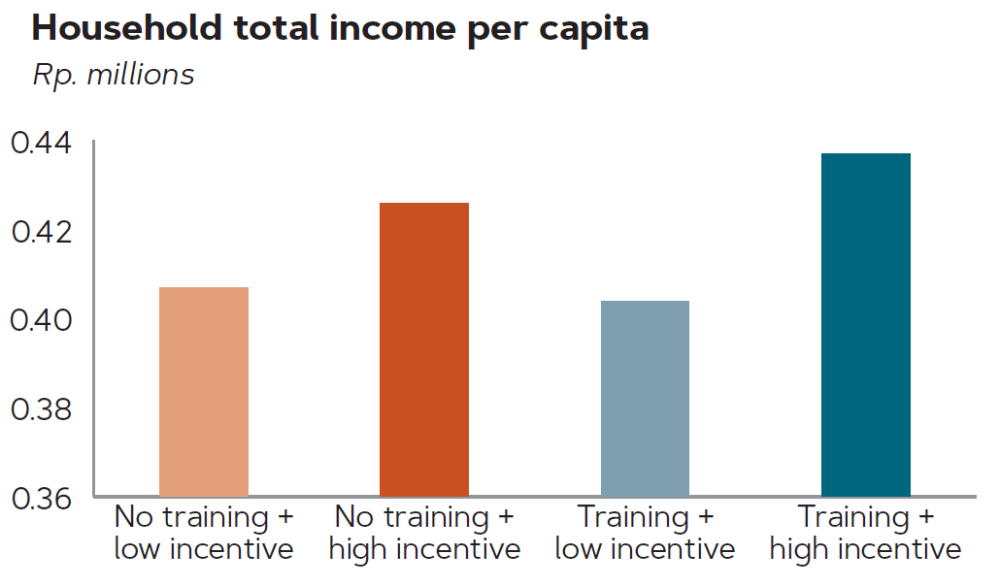

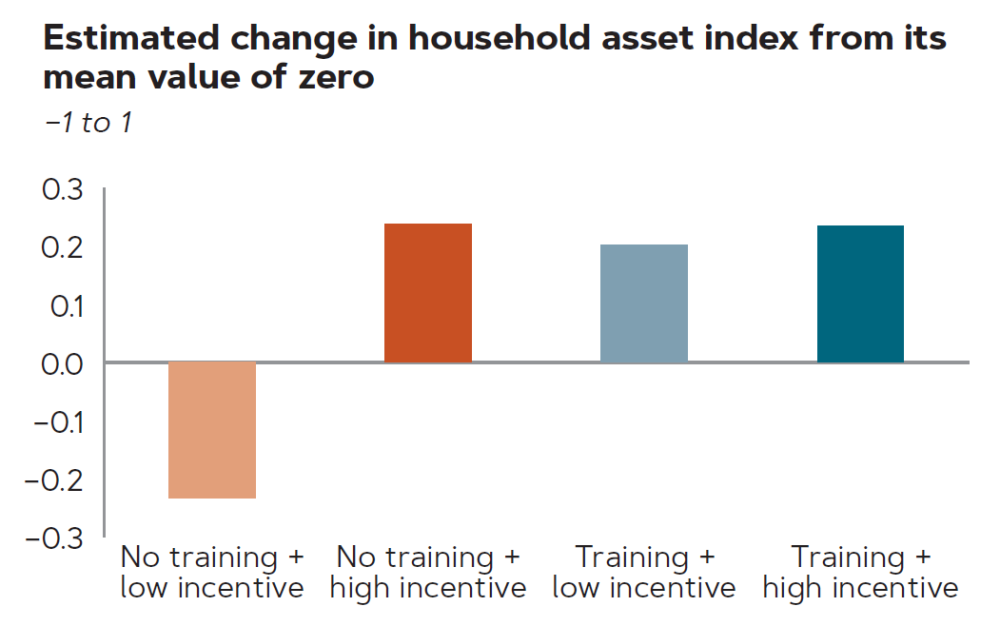

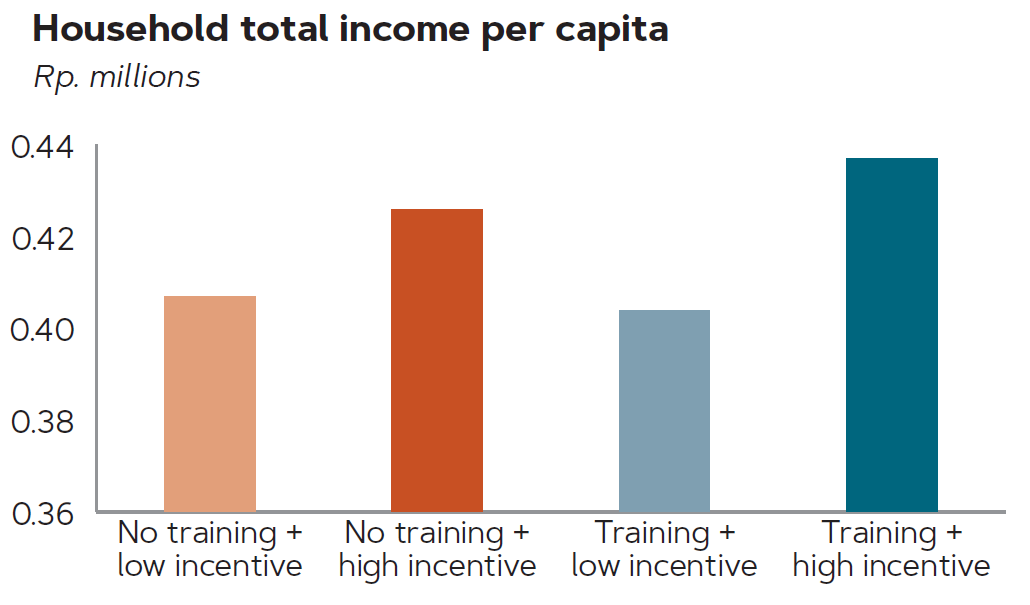

The training and high incentives had positive economic welfare effects on the businesswomen. In addition, the training and the high agent incentives had significant positive effects on household total income per capita and on a household asset index constructed from a list of 20 consumer durables owned by the household (see figures). Women receiving training and in villages with better paid agents reported a significant 3% increase in total household income per capita. The asset index, which is a more reliable measure of household income in rural settings, picked up significant positive reinforcing effects of both training and higher agent incentives. Women who received training reported a 20% increase in consumer durables and those in villages with better paid agents reported a 24% increase in consumer durables. These women likely invested at least part of their increased savings in durable household assets rather than in their businesses. A question yet to be answered is whether their increased savings will eventually also be invested in the business.

Summarizing, the overall results show a consistent picture. The financial literacy training and mentoring increased businesswomen’s knowledge of financial products and their saving behavior and, when combined with the presence in villages of more highly incentivized financial service providers, increased both their overall and e-savings balances and had both empowerment and household welfare-enhancing effects. These results show that relaxing both demand- and supply-side constraints increases savings and e-savings and that they encourage women’s economic independence and self-confidence. Their self-confidence may also have been boosted by the increased knowledge (and perhaps by their increased social validation) resulting from the group training and mentoring as well as by the presence of better paid financial service providers.

Empowerment effects—lasting or short-lived?

Are these empowerment effects from increased savings and mobile savings resulting from the combination of financial literacy training and the presence in the village of a more highly motivated financial service provider lasting or short-lived?

There is evidence for both in the experimental literature. An evaluation of a series of multifaceted graduation programs for the very poor found only a short-lived effect on women’s empowerment that vanished a year after the programs ended.[6] But other studies that combined business training with affirming or self-confidence–enhancing psychological messages—or the supportive presence of a friend—empowered women over a longer time and resulted in positive economic outcomes.[7] In a more intensive case of this psychological boosting, cognitive behavioral therapy (16 sessions) had a similar empowerment effect on the decision-making over household expenditures of perinatally depressed mothers in rural Pakistan—which was observed 7 years after the psychological intervention ended.[8]

Stay tuned

The East Java project has since implemented additional measures to address the logistical and operational problems encountered during the project’s initial year, and a follow-up assessment is planned for the end of this year. This follow-up should give a better indication of whether these observed empowerment effects were just short-term or are more lasting and whether higher incentives to financial service providers help to equalize business environments for women and men in East Java. Similarly, this follow-up measure should clarify possible business effects as well as household welfare-enhancing effects of mobile savings.

Details of the survey and treatment

The midline survey data were collected during a one-month period in February 2018 in 200 of the 401 study villages in East Java (the 200 villages were not randomly selected intentionally; they are the villages in which the agent and business owner training had been completed by the time of the survey). In each village, 7 women and 5 men entrepreneurs were randomly selected for the study and responded to a baseline questionnaire in two phases (107 villages from November 2016 to February 2017 and 294 villages from July to November 2017). Of the respondents, 1,344 women entrepreneurs and 975 men entrepreneurs were re-interviewed, as well as 189 bank agents (one agent per village). All the entrepreneurs were business owners between 18 and 55 years old, resided in the village, and owned a mobile phone.

Half the women were randomly selected to receive an average three-hour group sessions for financial literacy training, including information on using mobile phones for banking, on signing up for a mobile savings account, and on engaging in profitable business practices, plus three group mentoring sessions following the training for asking questions and practicing what they learned (90% of the women completed the training and the mentoring). The other half received no training but could open mobile savings accounts. Half the bank agents were randomly assigned to receive high incentives when signing in a new client and half to receive low incentives. All agents were informed of the importance of reaching the financially underserved, including women. The control group for the statistical analyses is the businesswomen not receiving training and residing in a village with low agent incentives.

The survey contained 225 questions and took about 60 to 75 minutes to fill out. Interviewers used tablets for registering responses. About half (52%) of the women were surveyed less than one month after they received the last group mentoring, 25% one month after this last mentoring, and the remaining 23% two or more months after this last mentoring. Sample attrition rates between the baseline survey and this survey were low (3.9% of business owners dropped out), and there was no evidence of selective attrition. Linear regression was used for continuous or dichotomous dependent variables, Poisson regressions for count-dependent variables (0,1,2,3…), and an ordered logit regression for dependent variables with ordered qualitative responses. All monetary values, including the household asset index were winsorized and transformed to inverse hyperbolic sine values. The covariates include the baseline value of the dependent variable (or a close substitute) as well as baseline values of the following entrepreneurs’ characteristics: age, schooling level completed, number of children, cognitive ability, willingness to take risk, marital status, head of household, household size, and household asset index. The estimated standard errors are adjusted for clustering at the village level. (More details on the analysis and the results are in Knowles 2018b.)

Acknowledgements

We would like to acknowledge the pivotal role of our partners, the ExxonMobil Foundation and Women’s World Banking in the creation of “She Counts.” We are grateful for the intellectual support of Principal Investigators Erika de Serrano, Northwestern University, and Gianmarco Léon, Pompeu Fabra University. We especially wish to thank our colleagues Andrea Adhi, Nurzanty Khadijah, Chaerudin Kodir, Lina Marliani, Alexander Michael, Irwan Setyawan, and Poppy Widyasari of the Abdul Latif Jameel Poverty Action Lab Southeast Asia, for their care in coordinating the fieldwork; Mercy Corps Indonesia, especially Britt Rosenberg and Glory Sunarto, for their skill in implementing a challenging pilot program, and SurveyMETER, for their excellence in conducting the survey. Thanks also to Hillary Johnson and Elizaveta Perova, of the World Bank East Asia and the Pacific Gender Innovation Lab, for their support of this project. Many thanks also to Bruce Ross Larson, Meta de Coquereaumont, Elaine Wilson, and Debra Naylor, of Communications Development Incorporated, for their editorial and design work on the report, and to Kelsey Richardson and her colleagues at APCO Worldwide for their communications and outreach expertise. Lastly, our deep gratitude goes to the Indonesian entrepreneurs who participated in the survey.

The Center for Global Development is grateful for funding from the ExxonMobil Foundation in support of this work.

This publication was revised in August 2018.

[1] Buvinic, M., J. C. Knowles, and F. Witoelar. 2018. “Unequal Ventures: Results from a Baseline Study of Gender and Entrepreneurship in East Java, Indonesia.” CGD Notes. Washington, DC: Center for Global Development. /publication/unequal-ventures.

[2] Knowles, J. C. 2018a. “Mobile Financial Services for Women in Indonesia: A Baseline Survey Analysis.” Background Paper. Washington, DC: Center for Global Development. /sites/default/files/analysis-impact-evaluation-baseline-survey.pdf.

[3] This ongoing research project is coordinated by the Center for Global Development in collaboration with Mercy Corps Indonesia, academic researchers from the Kellogg School of Business and Pompeu Fabra University, J-PAL Indonesia, SurveyMETER Indonesia, the World Bank East Asia and Pacific Gender Innovation Lab, and an Indonesian bank. Connect with us at http://www.shecounts.com or /she-counts to receive updates on the evidence base.

[4] Results from the incentive treatment are weak—as would be expected given the operational problems (43% of the bank agents included in this short-term measure had worked in their jobs for fewer than six months)—and are therefore only suggestive of trends.

[5] Knowles, J. C. 2018b. “Midline Effects of a Randomized Controlled Trial to Increase Access to the Utilization of Financial Services by Women Entrepreneurs in Rural Indonesia.” Background Paper. Washington, DC: Center for Global Development. /sites/default/files/impact-evaluation-midline-survey.pdf. (forthcoming).

[6] Banerjee, A., E. Duflo, N. Goldberg, D. Karlan, R. Osei, W. Parienté, J. Shapiro, B. Thuysbaert, and C. Udry. 2015. “A Multifaceted Program Causes Lasting Progress for the Very Poor: Evidence from Six Countries.” Science 348 (6236): 1260799.

[7] Campos, F., M. Frese, M. Goldstein, L. Iacovone, H. C. Johnson, D. McKenzie, and M. Mensmann. 2017. “Teaching Personal Initiative Beats Traditional Training in Boosting Small Business in West Africa.” Science 357 (6357): 1287–1290. Croke, K., M. P. Goldstein, and A. Holla. 2017. “Can Job Training Decrease Women’s Self-Defeating Biases? Experimental Evidence from Nigeria.” Policy Research Working Paper 8141. Washington, DC: World Bank. Field, E., S. Jayachandran, R. Pande, and N. Rigol. 2015. “Friendship at Work: Can Peer Effects Catalyze Female Entrepreneurship?” NBER Working Paper 21093. Cambridge, MA : National Bureau of Economic Research.

[8] Baranov, V., S. Bhalotra, J. Maselko, S. Sikander, and A. Rahman. 2017. The Long-term Impact of Treating Maternal Depression: Evidence from a Randomized Controlled Trial in Pakistan. Working Paper. https://editorialexpress.com/cgi-bin/conference/download.cgi?db_name=RESConf2016&paper_id=1186.

Topics

CITATION

Buvinic, Mayra, Tanvi Jaluka, and Firman Witoelar. 2018. Unequal Ventures Update: Empowering Women Entrepreneurs in East Java, Indonesia. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.