The most recent World Bank data on financial inclusion shows that by 2014, only 54 percent of the adult population in Latin America had an account at a financial institution. This compares to an average of 62 percent of adults worldwide and 70.5 percent for those countries with a similar level of income per capita (the region’s peers). In developed economies, 94 percent of adults have an account at a financial institution.

Many factors could be cited for the low ratios of financial inclusion in Latin America, but in a recent paper published at BBVA Research, that also came as a CGD working paper, we focus on the potential role of financial regulation. We assessed and compared the quality of the policies and regulations that impinge on financial inclusion in eight Latin American countries (Argentina, Brazil, Chile, Colombia, Mexico, Paraguay, Peru, and Uruguay). Peru and Mexico came out on top, with what appear to be the best regulatory frameworks for promoting financial inclusion. But even in these top performers, there is room for improvement.

Identifying regulatory influences on financial inclusion

In our recent study, we identified three dimensions of regulatory practices and policies that can influence financial inclusion:

Enablers: regulatory practices that determine the overall quality of the financial environment where providers of financial services operate

Promoters: regulations that deal with specific types of market frictions and describe the rules of the game for the provision of specific financial products and services for low-income populations

Preventers: regulations that, often unintentionally, create obstacles for expanding the supply and demand for financial products and services

In total, we identified 11 regulatory practices across these three dimensions. The assessment of these policies relies on the construction of three indices of regulatory quality (one for each dimension), and 11 sub-indices (for the 11 regulatory practices that form these dimensions). Additionally, we constructed a non-regulatory sub-index for assessing governments’ efforts to promote financial literacy.

Enablers

Promoters

Preventers

Competition Policies

Supervisory Quality

Simplified Accounts

Electronic Money

Correspondents

Microcredit

Credit Reporting Systems

Simplified Know-Your-Customer (KYC) requirements

Transaction Taxes

Interest Rate Ceilings

Directed Lending

To form each of the sub-indices, we assessed a number of variables selected on the basis of internationally accepted standards and a vast review of the existing literature. For each variable, we assigned scores in a range from 0 to 2 (where 2 represents the highest level of quality for the variable). For obvious reasons, it is not possible to go into the specifics of each variable and each sub-index here (the detailed explanation can be found in the study). However, there are two novelties about the construction of the sub-indices that are worth highlighting.

First, in constructing the sub-indices, we recognize that there may be interactions between variables that affect their whole impact on inclusion. Let’s take, for example, the sub-indices of simplified accounts or electronic money. Should regulatory constraints on fees and commissions charged by financial institutions to their customers for owing or using these products be assessed as detrimental or favorable for financial inclusion? The answer, as reflected in our index, is “it depends.” Setting no restrictions on fees and commissions to open and manage simplified or e-money accounts is desirable if the quality of competition policies for the financial sector is satisfactory. In other words, the recommendation to let financial institutions determine fees freely depends on the ability to prevent the emergence of monopoly powers through robust competition policies. In terms of our index, this means that to assess the quality of some Promoter components (simplified accounts and electronic money) we need to recognize their interaction with an Enabler component (competition policies).

A second interesting feature is that the index incorporates an interaction between some of the regulatory practices and other forms of government intervention that can increase the potential of those regulations. Continuing with the example of simplified accounts and electronic money, in the study we considered that the regulation governing the provision of these products is of a better quality if the government promotes their usage by individuals and small companies through additional efforts (such as depositing government transfers to low-income populations in these accounts) than if it stays aside. Finally, the amplifying effect of policies to enhance financial literacy on regulatory practices classified as Promoters is another example of the interactions between regulations and governmental interventions.

Which countries have the best regulatory framework for financial inclusion in Latin America?

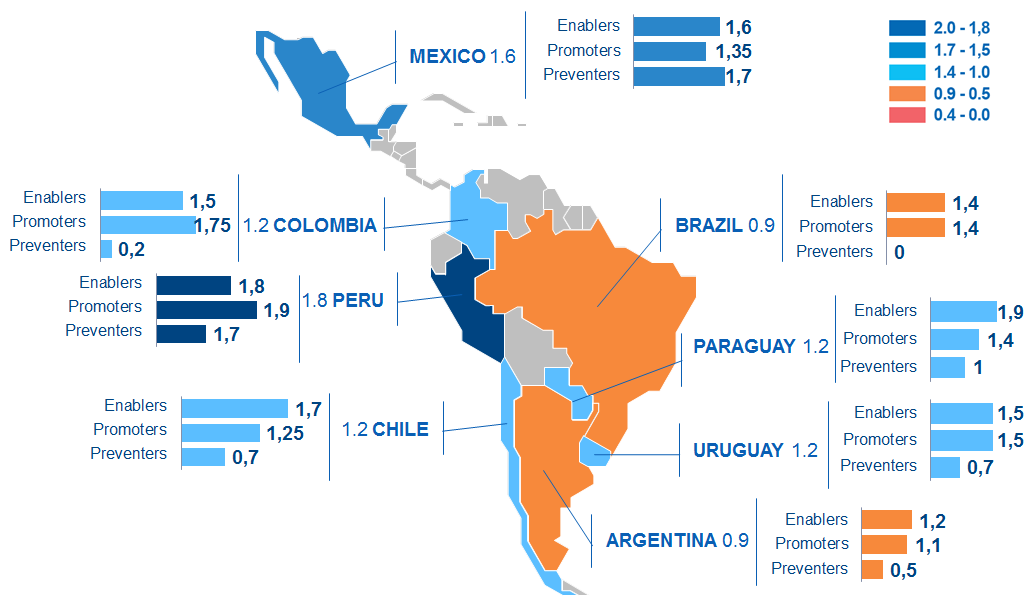

The map below summarizes the results of our index of regulatory practices for financial inclusion in eight Latin American countries. The numbers represent the values of the overall index and of each of the three sub-indices (each ranging from 0 to 2, as mentioned above).

As shown, all the countries have strengths and weaknesses in their regulatory frameworks. Peru appears to have the best regulatory framework, followed closely by Mexico. Obviously, some areas of Peruvian regulation could be enhanced, but in broad terms, the regulatory framework is robust and conducive to financial inclusion. Mexico, on the other hand, has more room to improve the quality of its regulatory framework, especially the regulations classified as Promoters. Still, the country might soon solve some of the deficiencies we identified in our study (for instance, the absence of a dedicated regulatory framework for electronic money). In fact, Mexico’s Congress is currently discussing a draft law that seeks to leverage the possibilities of financial technology (or Fintech) to advance financial inclusion.

At the opposite end of the spectrum, Argentina and Brazil have the lowest scores. Both present very low scores along the Preventers dimension as there are various elements in their regulatory framework (from financial transaction taxes to directed lending by the state) that might run counter to financial inclusion objectives. Thus, in these countries major changes to the regulatory framework are needed to achieve sustainable progress in financial inclusion.

The rest of the countries obtain modest results that also tend to be explained by very low scores in the Preventers index but more solid results in the Enablers and Promoters indices. The case of Colombia stands out in this last group: although the country is strong in the Promoters index, the existence of a financial transaction tax, the imposition of ceilings on interest rates, and directed lending practices generate multiple distortions and explain why Colombia’s overall score lags behind Peru and Mexico.

Does regulatory quality alone explain the financial inclusion gap?

The answer to this question is “no.” As discussed in the CGD report on Financial Regulations for Improving Financial Inclusion, regulation is important for two main reasons: first, because the right regulatory framework is key to enable the private sector to adapt innovations in digital finance and encourage their use by low-income populations, and second, because policies to increase financial inclusion must be compatible with the traditional objectives of financial regulators. Thus, they should not undermine the stability and integrity of the financial system, while ensuring effective consumer protection.

It should not be a surprise, though, that regulation is not the only factor that determines a country’s success in advancing inclusion. Many other factors matter, including socioeconomic constraints, the macroeconomic environment, institutional quality, and specific characteristics of the financial system. In other words, having an enabling regulatory framework is a necessary but not sufficient condition for sustainable progress in financial inclusion. This is the conclusion of an econometric study in Rojas-Suarez (2016) that shows that in Latin America, institutional factors matter most in explaining the financial inclusion gap.

That said, an appropriate regulatory framework is essential for financial inclusion. Thus, by signaling areas of strength and weakness in the regulatory practices of individual countries, the index of regulatory practices for financial inclusion is meant to support the efforts of policymakers in the region with a mandate to improve financial inclusion. Therefore, beyond the specific country scores, what is truly useful from this index is the opportunity it provides in motivating discussion among market participants, policymakers, and interested researchers, as it already has at the Latin American and Caribbean Economic Association meeting in Buenos Aires last November. Hopefully, these types of conversations will serve to guide regulatory reforms.

Liliana Rojas-Suarez is a senior fellow at the Center for Global Development.

Lucía Pacheco is an economist at BBVA Research.

Según los datos más recientes de inclusión financiera del Banco Mundial, en 2014 sólo el 54 por ciento de la población adulta de América Latina tenía una cuenta en una institución financiera. A nivel mundial la cifra asciende al 62 por ciento de los adultos, mientras que en los países con un nivel similar de ingreso per cápita (los pares de la región) alcanza el 70.5 por ciento. En las economías desarrolladas, el 94 por ciento de los adultos tiene una cuenta en una institución financiera.

Pueden citarse muchos factores para explicar los bajos ratios de inclusión financiera en América Latina, pero en el estudio recientemente publicado por BBVA Research y como documento de trabajo de CGD, nos centramos en el papel potencial de la regulación financiera. En este estudio valoramos y comparamos la calidad de las prácticas regulatorias que influyen en la inclusión financiera en una muestra de ocho países latinoamericanos (Argentina, Brasil, Chile, Colombia, México, Paraguay, Perú y Uruguay). Perú y México se situaron a la cabeza del ranking, con lo que parecen ser los mejores marcos regulatorios para promover la inclusión financiera. Aun así, incluso en estos países hay margen de mejora.

Identificando la influencia de la regulación en la inclusión financiera

En nuestro reciente estudio identificamos tres dimensiones de prácticas regulatorias y políticas que pueden afectar a la inclusión financiera:

Facilitadores: prácticas regulatorias que determinan la calidad global del entorno financiero en el que operan los proveedores de servicios financieros

Promotores: regulaciones que tratan de dar soluciones a fallas de mercado y regulan la prestación de productos y servicios financieros específicos para segmentos de la población de bajos ingresos

Obstaculizadores: regulaciones que, aunque involuntariamente, crean obstáculos para ampliar la oferta y la demanda de productos y servicios financieros

En total identificamos 11 prácticas regulatorias que se distribuyen entre estas tres categorías. Con el fin evaluar la calidad de estas tres dimensiones de la regulación financiera, construimos un índice para cada una de ellas y subíndices para las 11 prácticas/políticas regulatorias que componen los índices. Además, también construimos un subíndice para evaluar los esfuerzos de los gobiernos a la hora de promover la Educación Financiera.

Facilitadores

Promotores

Obstaculizadores

Políticas de competencia

Calidad de supervisión

Cuentas simplificadas

Dinero electrónico

Corresponsales

Microcrédito

Sistemas de información crediticia

Requisitos simplificados de “conoce a tu cliente" (KYC)

Impuestos a las transacciones financieras

Topes a las tasas de interés

Créditos dirigidos

Para formar cada uno de los sub-índices valoramos un conjunto de variables cuya selección se basó tanto en estándares internacionalmente aceptados, como en una amplia revisión de la literatura. Para cada variable, se definió una puntuación que oscila del 0 al 2 (donde 2 es el grado más alto de calidad que puede tomar la variable). Por razones evidentes, no podemos entrar en el detalle de cada variable y cada subíndice (la explicación detallada se encuentra en el estudio). Sin embargo, cabe señalar dos aspectos novedosos en la construcción de los sub-índices.

Primero, en la construcción de los sub-índices se reconoce que pueden darse interacciones entre las variables que afectan a su impacto final sobre la inclusión financiera. Tomemos como ejemplo los sub-índices de cuentas simplificadas y dinero electrónico. ¿Deben valorarse las restricciones regulatorias a las comisiones y tarifas que las instituciones financieras pueden cobrar a sus clientes por usar estos productos como favorables o perjudiciales para la inclusión financiera? La respuesta, como se refleja en nuestro índice es “depende”. No imponer restricciones a las tasas y comisiones por la apertura y manejo de estos productos es deseable siempre y cuando haya normativa de competencia adecuada en el sector financiero. En otras palabras, la recomendación de dejar que las instituciones financieras determinen libremente las comisiones depende de la habilidad de las autoridades de competencia de evitar que surjan poderes monopólicos mediante políticas de competencia robustas. En términos de nuestro índice, esto significa que para valorar la calidad de algunos componentes del índice Promotores (cuentas simplificadas y dinero electrónico) debemos incorporar la interacción con un componente del índice Facilitadores (políticas de competencia).

Un segundo aspecto novedoso es que se han incorporado interacciones entre algunas de las normativas con otras intervenciones del Estado que mejoran el potencial de inclusión financiera de las mismas. Siguiendo con los ejemplos de cuentas simplificadas y dinero electrónico, en la construcción de sus respectivos sub-índices se considera que la normativa que regula la oferta de estos productos es de mejor calidad si el gobierno promueve el uso de las cuentas por parte de individuos y pequeñas empresas a través de esfuerzos adicionales (como el pago de transferencias por parte del gobierno a la población de menores ingresos a través de estos productos) que si se queda al margen. Por último, el efecto magnificador de las políticas de educación financiera sobre la eficacia de las políticas regulatorias clasificadas como Promotores es otro ejemplo de la interacción entre normativas y otras intervenciones del Estado.

¿Qué países tienen el mejor marco regulatorio para la inclusión financiera en América Latina?

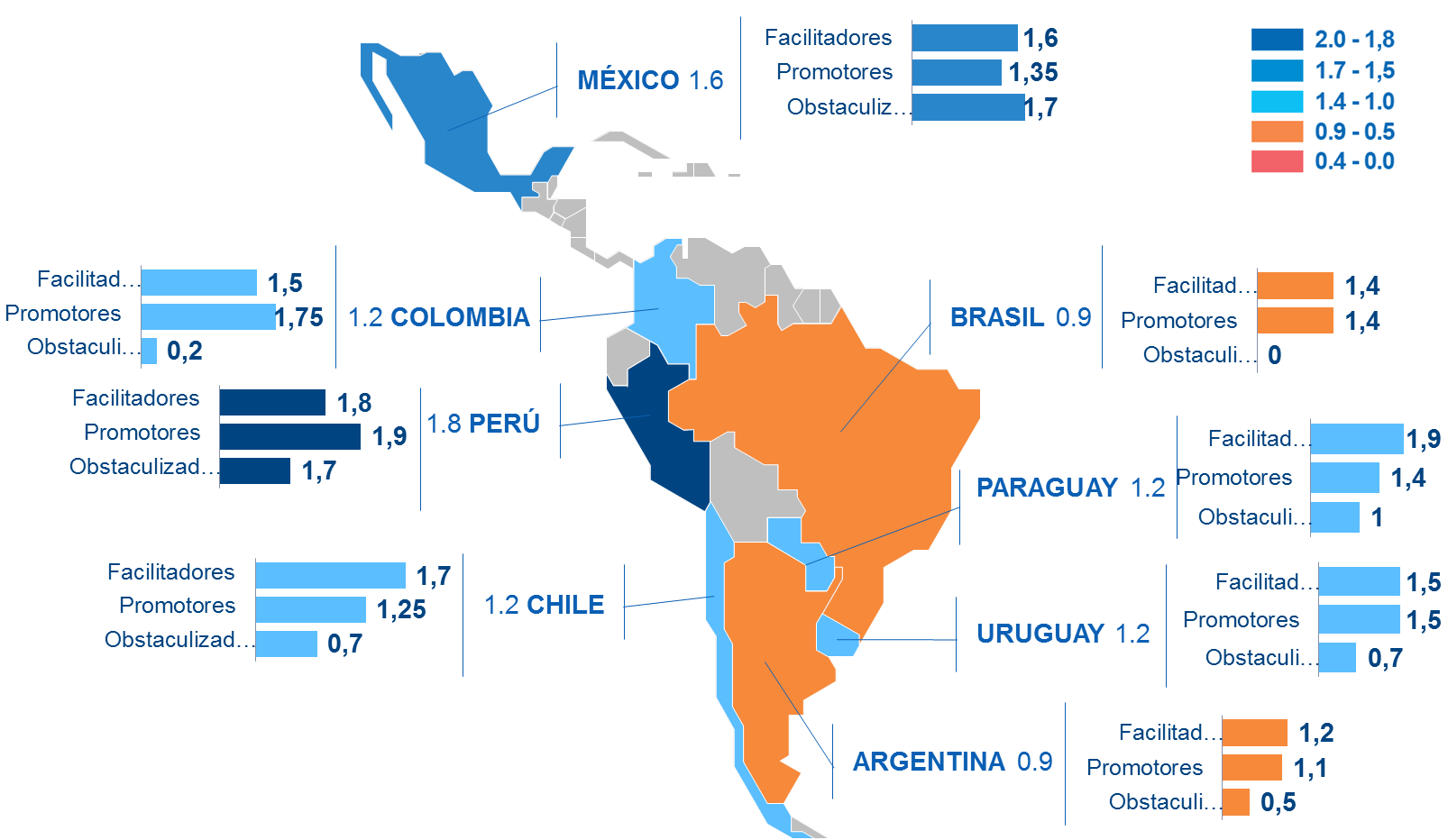

El siguiente mapa resume los resultados de nuestro índice de prácticas regulatorias para la inclusión financiera en los ocho países latinoamericanos seleccionados. Los números representan los valores del índice general y de los índices para cada una de las tres dimensiones (cada uno de ellos en un rango de 0 a 2, como se mencionó anteriormente)

Como se observa, todos los países tienen puntos fuertes y débiles en sus marcos regulatorios. Perú figura como el país con el mejor marco regulatorio, seguido de cerca por México. Evidentemente, algunas áreas de la regulación en Perú podrían mejorarse, pero en términos generales, el marco regulatorio es sólido y favorable a la inclusión financiera. México, por otro lado, presenta más margen de mejora en la calidad de su marco regulatorio, especialmente en las regulaciones calificadas como Promotoras. Aun así, es posible que parte de estas deficiencias se resuelvan pronto (por ejemplo, la ausencia de un marco regulatorio dedicado al dinero electrónico). De hecho, el Congreso de México está actualmente debatiendo un proyecto de ley que persigue aprovechar las oportunidades de la tecnología financiera (o fintech) para avanzar en inclusión financiera.

En el extremo opuesto encontramos a Argentina y Brasil, que obtienen las puntuaciones más bajas. Ambos presentan puntuaciones muy bajas en la dimensión de los Obstaculizadores, ya que hay varios elementos en su marco regulatorio (desde impuestos a las transacciones financieras a políticas de crédito dirigido por parte del gobierno) que pueden actuar en contra de los objetivos de inclusión financiera. Por tanto, en estos países son necesarios cambios profundos en sus marcos regulatorios para alcanzar un progreso sostenido en inclusión financiera.

El resto de países obtienen resultados más modestos que también tienden a ser explicados por puntuaciones muy bajas en el índice Obstaculizadores, con resultados más sólidos en los Facilitadores y Promotores. El caso de Colombia es especialmente llamativo: aunque el país es fuerte en el índice Promotores, la existencia de impuestos a las transacciones financieras, la imposición de topes a las tasas de interés y las prácticas de crédito dirigido generan múltiples distorsiones que explican porqué la puntuación final de Colombia se encuentra por detrás de las de Perú y México.

¿Es suficiente la calidad regulatoria para explicar la brecha de inclusión financiera?

La respuesta a esta pregunta es “no”. Como se recoge en el informe de CGD sobre Regulaciones financieras para mejorar la inclusión financiera, la regulación es importante por dos razones principales: primero, porque contar con el marco regulatorio adecuado es esencial para permitir que el sector privado adopte innovaciones financieras digitales y promueva su uso por la población de bajos ingresos, y segundo, porque las políticas destinadas a avanzar en inclusión financiera deben ser compatibles con los objetivos tradicionales de los reguladores financieros. Por tanto, no deben amenazar la estabilidad y la integridad del sistema financieros, al tiempo que aseguran una protección al consumidor efectiva.

Sin embargo, no es sorprendente que la regulación no es el único factor que determina el éxito de un país en su avance en inclusión financiera. Muchos otros factores son también relevantes, incluyendo factores socioeconómicos, el entorno macroeconómico, la calidad de las instituciones y algunas características del sector privado. En otras palabras, tener un marco regulatorio facilitador es una condición necesaria pero no suficiente para alcanzar un progreso sostenido en inclusión financiera. Esta es la conclusión de un estudio econométrico en Rojas-Suarez (2016) que muestra que en América Latina, los factores institucionales son los más importantes para explicar la brecha de inclusión financiera.

Habiendo dicho esto, un marco regulatorio apropiado es esencial para la inclusión financiera. Por ello, al señalar las áreas de fortaleza y debilidad en los marcos regulatorios de los países, el índice de prácticas regulatorias para la inclusión financiera pretende apoyar los esfuerzos de los reguladores de la región con el mandato de promover la inclusión financiera. Por tanto, más allá de las puntuaciones individuales de los países, lo que es verdaderamente útil de este índice es la oportunidad de motivar la discusión entre participantes del mercado, reguladores e investigadores interesados, como ya sucedió en la reunión de la Asociación de Economía de América Latina y el Caribe en Buenos Aires el pasado mes de noviembre. Con suerte, este tipo de debates servirán para guiar las reformas regulatorias.

Liliana Rojas-Suarez es una Investigadora principal del Center for Global Development.

Lucía Pacheco es una economista del BBVA Research.

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.