Recommended

Blog Post

Where Is the UK’s Global Fund Commitment?

UK Chancellor, Kwasi Kwarteng, is preparing a “medium-term fiscal plan,” expected to be published at the end of this month. That plan may offer some clarity on the UK’s aid budget, which has been frozen since July to accommodate the unprecedented costs of Ukrainian refugee arrivals.

We have argued that extraordinary events call for extraordinary measures, and that—just as additional funding has been found for military support for Ukraine—so too should new money be found for hosting Ukrainian refugees in the UK. If this doesn’t happen, and it is instead taken from the existing UK aid budget, then a third round of deep cuts to aid programmes is on its way, arguably putting the nail in the coffin of this Government’s reputation as a reliable development partner with allies (including the US) and partners alike.

But might there be a solution that enables the Chancellor to respond to immediate pressures, avoids further cuts to the UK’s aid programmes, and actually improves the UK’s medium-term fiscal position?

We think so.

We propose that the Chancellor combines the aid budget over four years, bringing forward spend of 0.1 percent of GDP across 2022 and 2023, by reducing spend by the same amount over 2024 and 2025. Overall aid spend would be unchanged but smoothed, with inefficient cuts avoided, and borrowing lower in the key years of the medium-term fiscal plan.

Here we set out the problem, its impact, and a plan for the Chancellor:

Yo-yoing aid spend: not good for anyone

The UK is struggling to fund from its aid budget a spike in the cost of accommodating refugees, with additional arrivals this year from Afghanistan and Ukraine. These costs could more than triple to over £3bn this year: up to a quarter of the UK’s £12bn aid budget, which has already been cut twice in the last two years. (It’s perhaps important to note these refugee “costs” ignore the significantly tax revenues from the 40 per cent of refugees already working). Based on current and expected refugee arrivals in 2022, we estimate refugee costs of some £3bn this year and £2.6bn in 2023. But these costs are temporary and should fall back to pre-2022 levels from 2024.

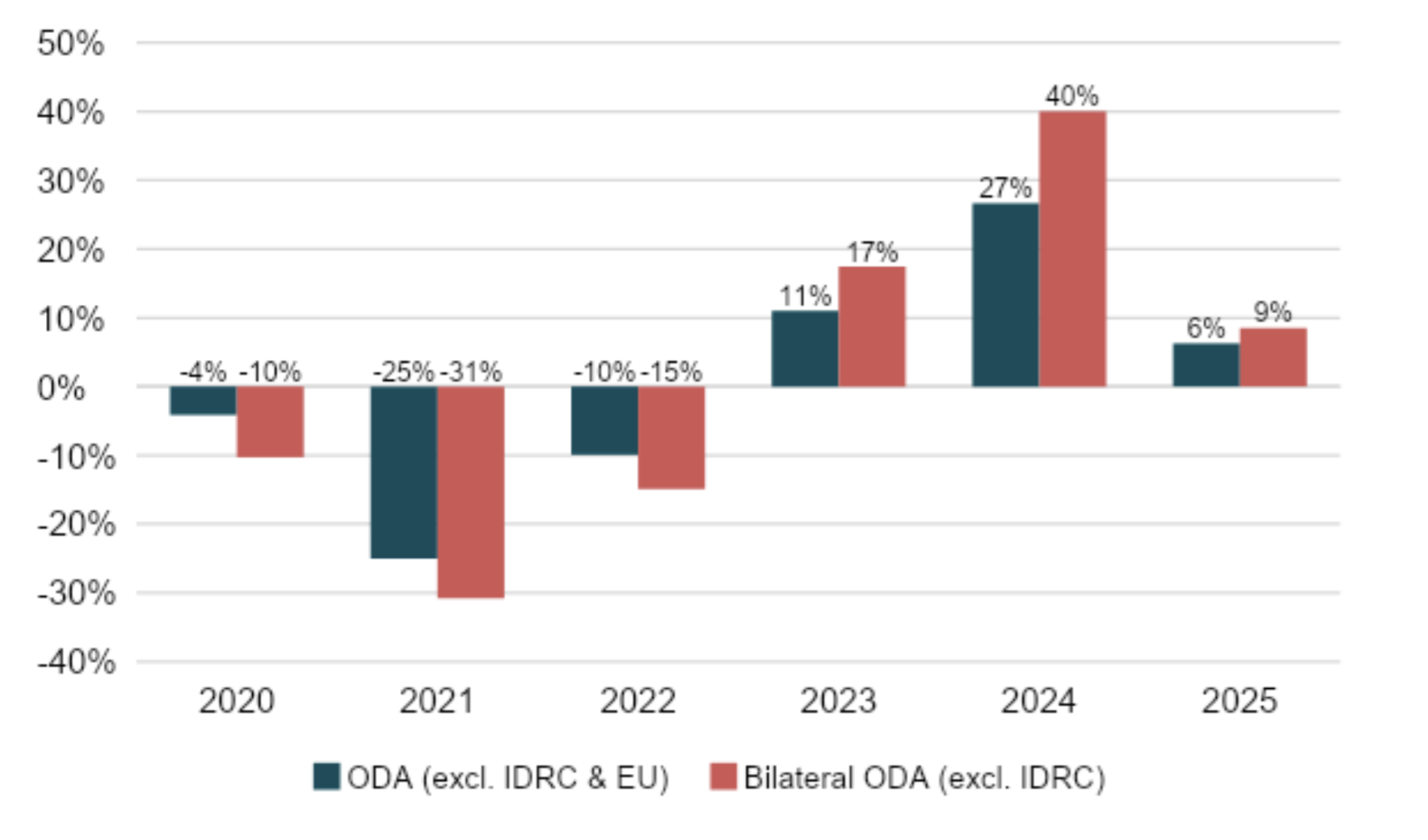

The effect of this large one-off cost is to create cuts in aid this year; but large increases in 2024 (see figure 1). Assuming refugee spend falls back to pre-2022 levels after next year, and the aid budget remains at 0.5 percent of Gross National Income (GNI), then aid spending not allocated to refugee hosting or EU contributions will fall by £0.9bn this year, followed by a £3.4bn rise to 2024. If these cuts are in the bilateral budget (multilateral budgets tend to be committed), it implies a 15 percent cut this year; followed by a cumulative 64 percent increase over the following two years.

Figure 1. Annual Percentage Change in Allocable ODA Budgets

Source: Authors’ analysis of OBR projections; Statistics In International Devt (to 2021)

Notes:

(a) “Allocable” Official Development Assistance (ODA) excludes fixed spending commitments of EU contributions and expenditure on in-donor refugee costs.

(b) Assumes: non-EU multilateral spend remains at 2021 levels (in line with Government target of no more than 25% of total ODA by 2025); in-donor refugee spend returns to its 2021 level from 2024 onwards; and ODA is fixed at 0.5% GNI in line with the OBR’s August GDP projections.

The planned return to spending 0.7 percent of GNI on ODA is now a long way off—potentially 2027—due to the weakened economic outlook and massive cost of the energy price cap.

Volatility damages efficiency and relationships

These abrupt falls in the bilateral aid budget not including refugee costs—a cumulative 47 percent decline over the past 3 years—followed by a steep rebound are a recipe for inefficiency and value for money risks. The National Audit Office have repeatedly criticised sharp changes in aid expenditure where there is limited time for planning. Projects that can be cut are often not the weakest, and officials, ambassadors and Ministers expend significant effort in administration to stop or (re)start, programmes.

A volatile aid budget is also unwelcome in partner countries themselves trying to deal with economic shocks from COVID, high prices, a strong dollar and the war in Ukraine. The third set of cuts in three years will mark the UK out as an unreliable partner and couldn’t be further from the first commitment in the development strategy to build “in-depth, long-term partnerships”.

…And frozen spend is now undermining the UK’s reputation

Chancellor Kwarteng will meet other finance ministers in Washington this week at the annual shareholder meetings of the IMF and World Bank. They, and particularly the US, will be aware that controversially, the UK failed to make any pledge at the President Biden-hosted Global Fund replenishment; and the head of USAID called out countries like the UK who are cutting aid and re-writing rules on what counts.

Not only could these decisions cost lives, they are also deeply damaging for the UK’s reputation, coming fast on the heels of development strategy published just this summer, authored by the now-Prime Minister, which promised “honest and reliable investments.”

Medium-term fiscal space

Some pressures on the aid budget are likely to ease in 2024 and 2025. Of course, it’s impossible to predict humanitarian needs so far out, and there may be additional spending to support Ukraine directly, but we do know that the UK’s substantial ODA payments to the EU, agreed as part of the withdrawal agreement, will fall. EU payments were £1.3bn in 2021—over 11 percent of the total aid budget—and are expected to fall to around £0.3bn in 2025.

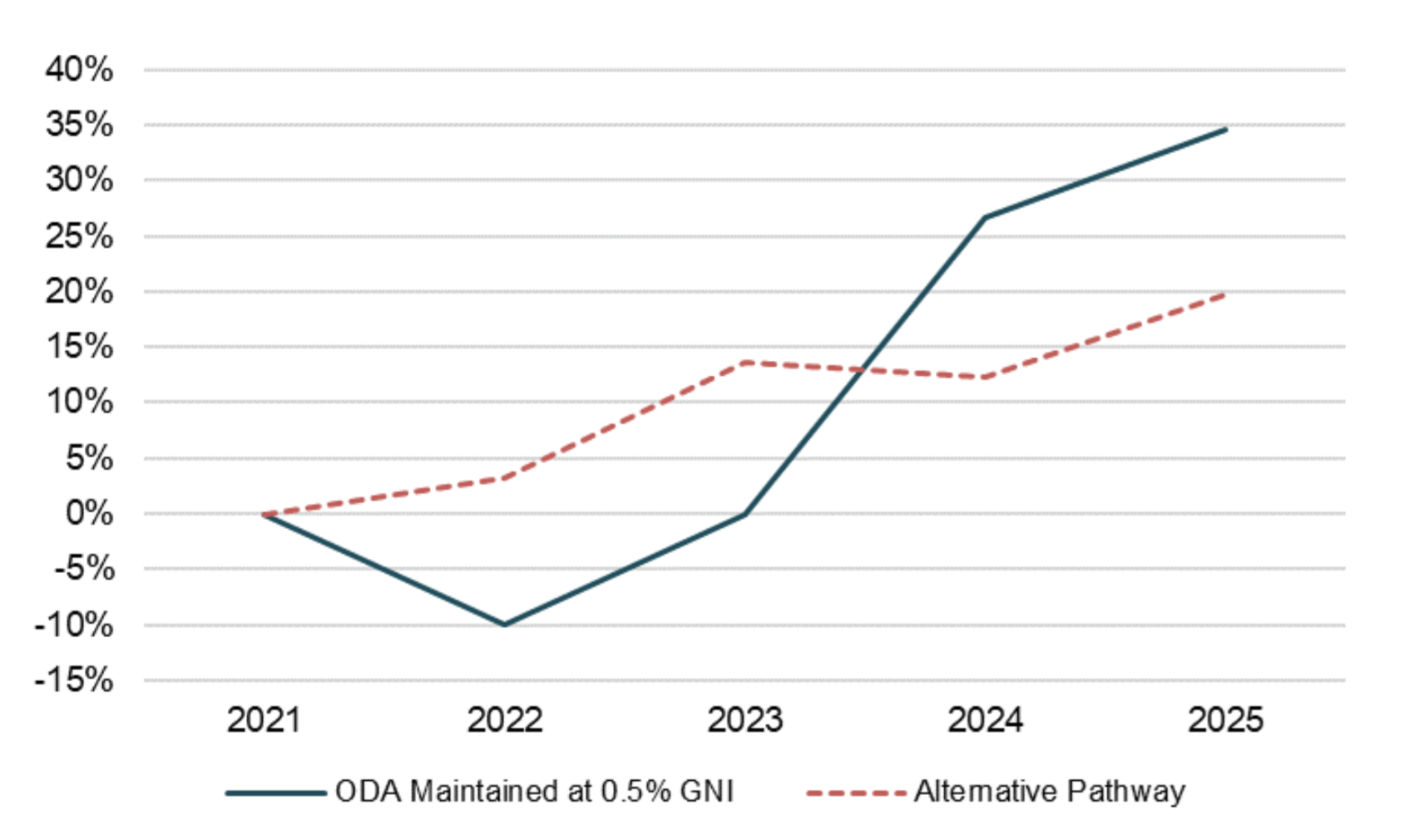

If the aid budget rose to 0.55 percent in 2022 and 2023 and fell to 0.45 percent in 2024 and 2025 then, after EU payments and assuming refugee costs fall back to under £1bn as in 2019, the remaining budget would more gradually rise over the next four years (with a slight fall in 2024). This “alternative pathway” (see fig 2) is much smoother than the status quo of maintaining the ODA budget at 0.5% GNI, which implies a third round of cuts this year, a recovery next year, and then a steep increase in 2024.

Figure 2. Percentage Change from 2021 in the Nominal Value of the UK’s Allocable ODA Budget

Source: Authors’ analysis of OBR projections; Statistics In International Devt (to 2021)

Notes:

(a) “Allocable” ODA—see fig 1

(b) The “Alternative Pathway” refers to allocating 0.55% of GNI to the total ODA budget in 2022 & 2023, and 0.45% of GNI in 2024 & 2025.

A more flexible ceiling and strengthened fiscal outlook

Spending from the energy price cap will be huge in 2022 and 2023, and markets will be looking to see a stronger fiscal position beyond that period. In the above alternative scenario, spending in 2024 and 2025 would be respectively around £1.3bn and £1.4bn lower. The cut to the lower 0.5 per cent of GNI aid budget is already saving £5bn per year, and these further amounts are small but helpful relative to the UK’s potential current spending deficit of £30bn in 2025-26.

The Chancellor has a rare opportunity to improve efficiency and value in aid spend, strengthen the UK’s international reputation, and improve the fiscal outlook. He should respond to the extraordinary circumstances of the Ukraine war. If he is unwilling to increase the budget, he should bring it forward.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.