As we start out 2019, a growing consensus has been forming among experts and market participants: the increased volatility in international capital markets and rising trade tensions of 2018 will not abate in 2019, and in fact may have adverse spillover effects on economic growth and stability of emerging markets and developing economies (EMDEs). How will this challenging international environment shape prospects for Latin America? As a panelist at a recent CGD event on the state of the global economy and development prospects for EMDEs, I dealt with this issue by answering three questions:

Which are the most important external factors affecting Latin America?

How resilient is the region to external shocks?

And finally, what can policymakers do?

Below, I lay out detailed responses to each of these, including a set of recommendations that policymakers can take on right now.

1. Which external factors might affect Latin America’s economic growth and stability most in 2019?

The short answer: policy-uncertainties in the US

In recent years, developments in China and the United States have been key external factors affecting economic and financial variables in Latin America. Although trade and financial developments interact with each other, China’s effect has mostly been through the trade channel while the US’ effect has largely been through the financial channel.

For example, due to the large number of commodity exporters in the region, China’s slowdown, associated with the decrease in commodity prices, has affected the pace of the growth in the region since 2014. Likewise, financial developments in the United States—e.g., the collapse of Lehman Brothers in 2008, which marked the beginning of the global financial crisis; Ben Bernanke’s suggestion in May 2013 that the Fed might begin reducing its rate of liquidity expansion (the so-called Taper Tantrum); and the sharp volatility of the US stock markets in 2018—increased investors’ risk aversion and reduced their appetite for EMDEs assets, including those from Latin America. On these three occasions, the region was not spared from the reduction in net capital inflows that ensued.

In 2019, there is consensus about a further slowdown in China’s economic growth. However, I believe this slowdown has already been internalized in commodity prices and, based on past experiences, the Chinese’s policymakers’ response has also been highly anticipated.

In contrast, policy uncertainty in the US remains high and there are no signs of improvements in the foreseeable future. Thus, in my view, developments in the United States will be the most influential external factor impinging on Latin America’s economic growth and financial stability.

Specifically, three key sources of uncertainty are:

the behavior of Fed rates;

dollar appreciation; and

the Trump-led protectionist war and nationalistic stance.

These lie at the core of the current volatility in international financial markets and may continue decreasing investors’ demand for EMDEs’ assets, of which Latin America is an important supplier.

Figures on the recent behavior of external debt in Latin America provide some initial illustration on potential problems that the region might face if continuation of US policy uncertainties were to result in further increase in investors’ risk aversion and, therefore, further declines in net capital inflows:

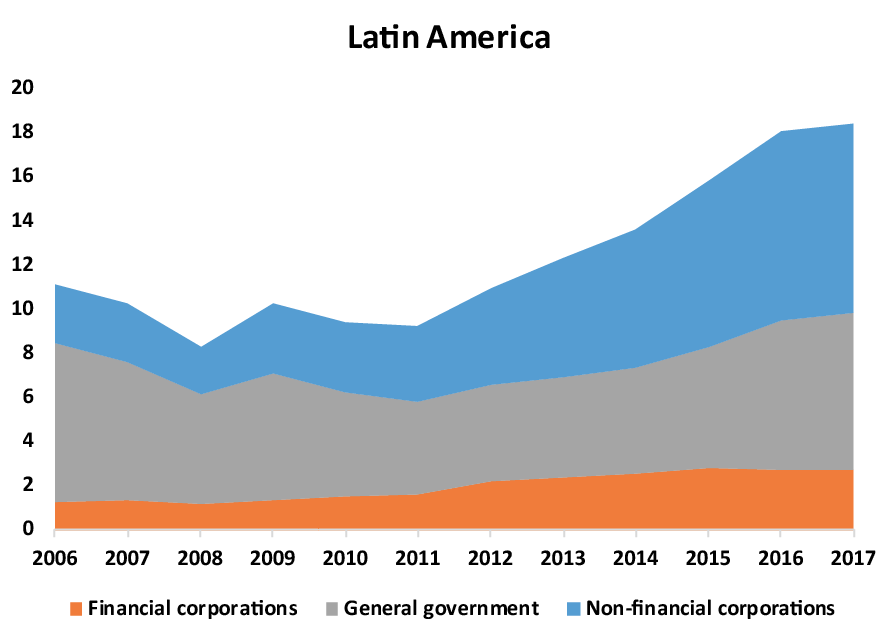

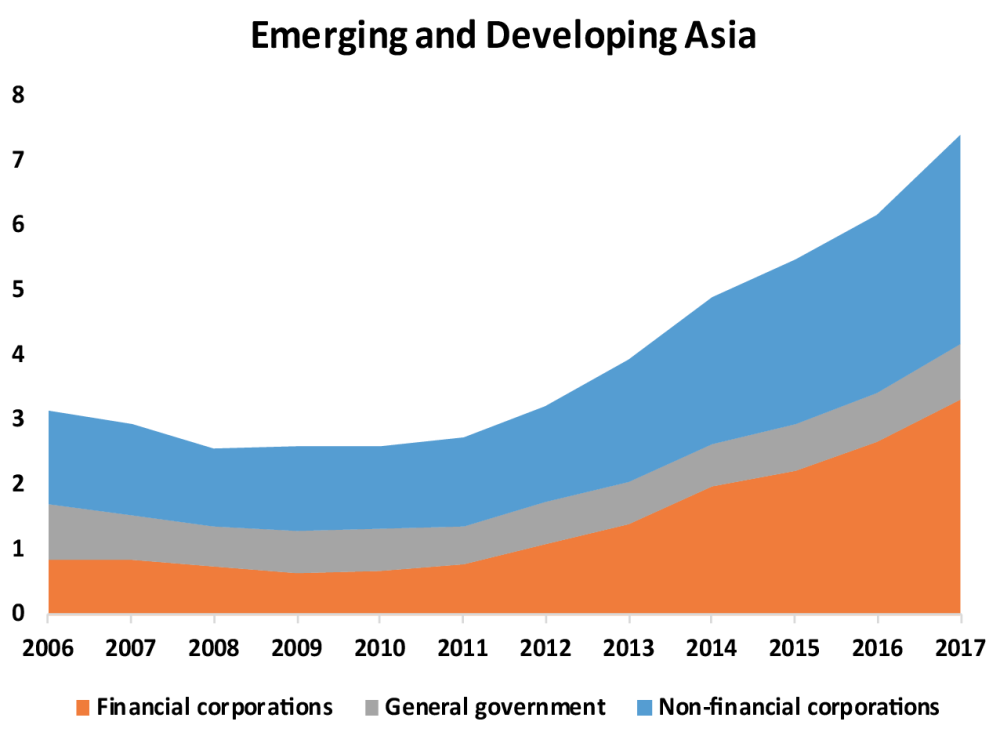

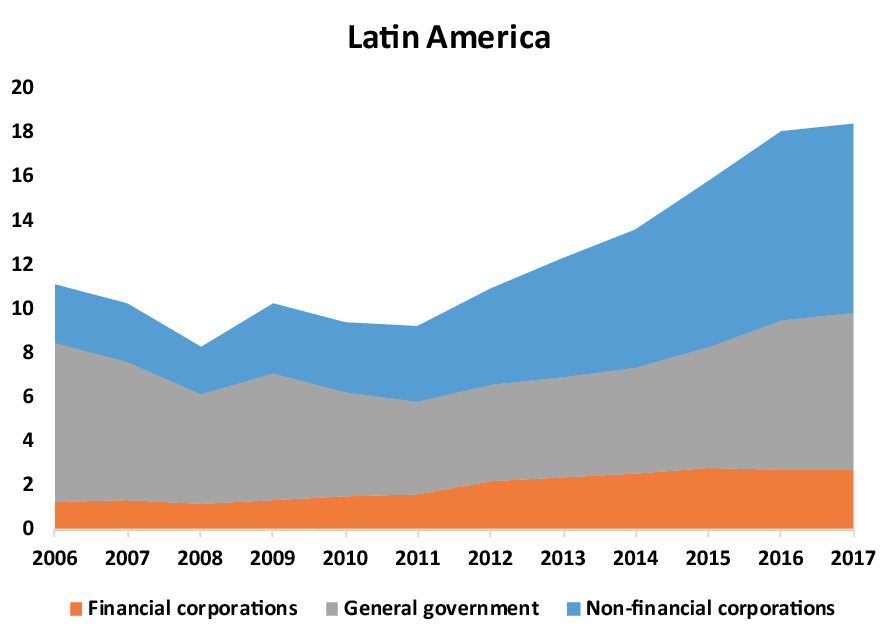

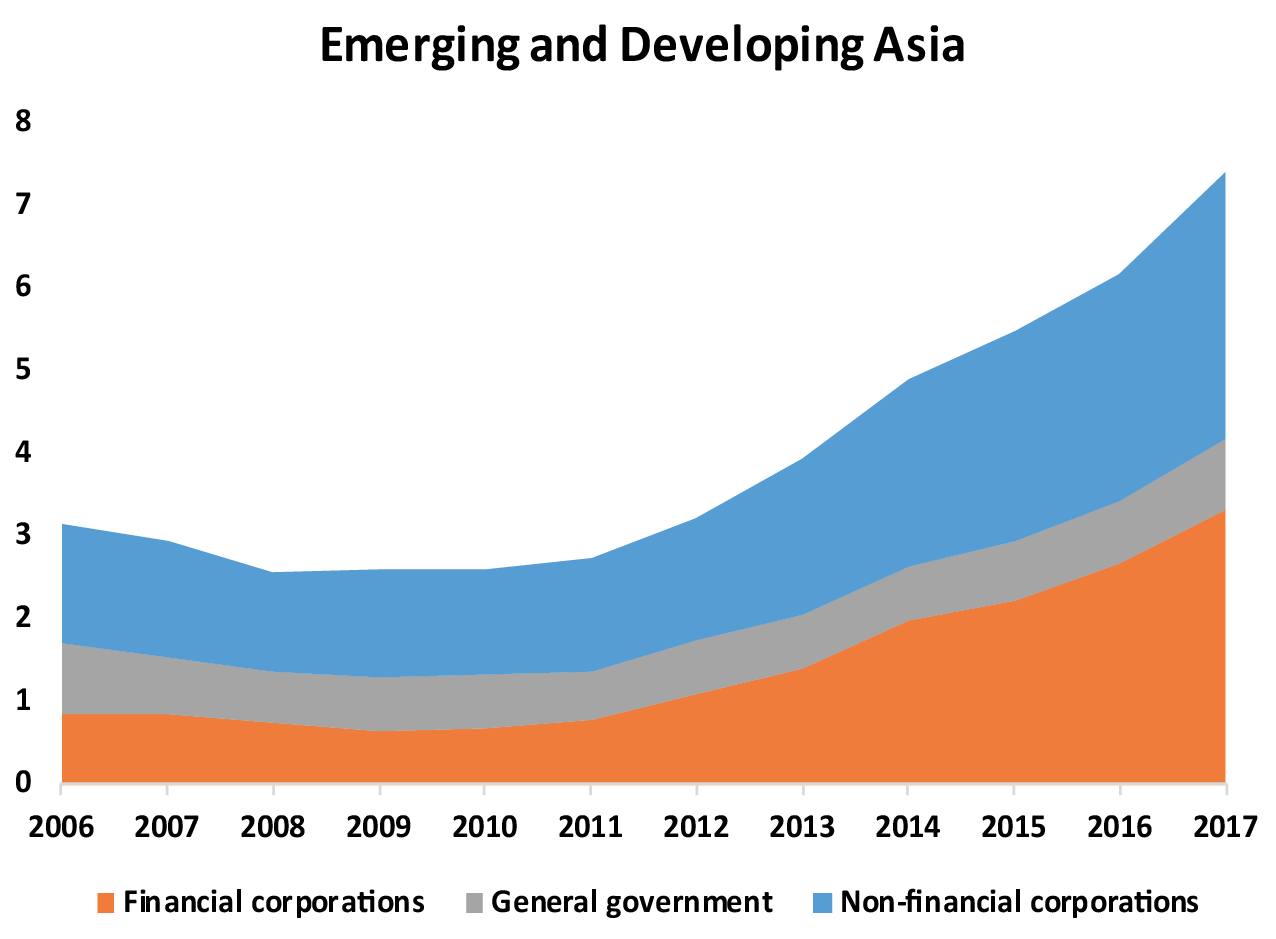

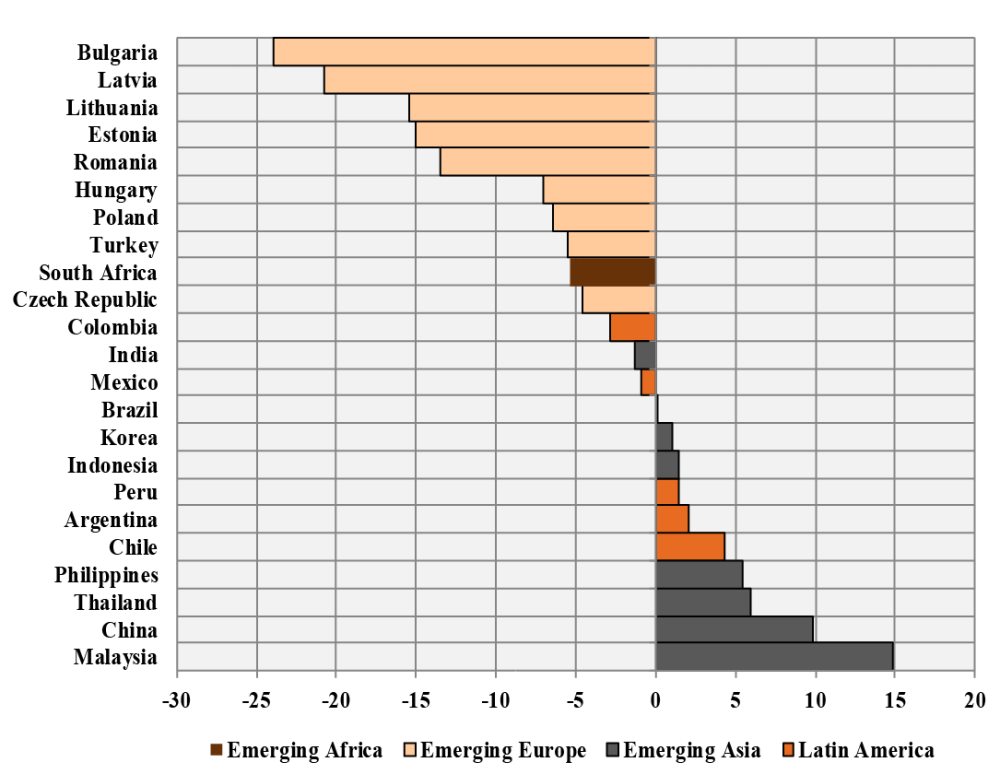

While issuance of external debt securities (bonds) increased substantially in all EMDE regions since 2010, and the latest discussion has centered on the issuance of debt securities by non-financial corporations, in Latin America, government debt issuance also accelerated significantly, at much rapid pace than other regions like Asia (see Figure 1 below). In most countries in Latin America, the ratio of total external debt securities to GDP has more than doubled since 2010 (and this, without including other sources of external debt, such as international loans). Of course, countries differ significantly. For example, in Argentina government debt accounts for the lion’s share of external debt securities; whereas, in Chile it’s mostly a private sector issue.

Figure 1. Stock of External Debt Securities / GDP (%)

Source: BIS

Among the six largest Latin American countries, excluding Mexico and Peru, total external debt service (amortization and interest payments) as percentage of GDP has also increased significantly, currently reaching about 16 to 18 percent in some countries. As a reference, by 2017 this ratio was about 20 percent in Turkey.

This brings me to my second question:

2. How resilient is Latin America to further deterioration in the international environment?

Consistent with the main sources of uncertainty in the US outlined above, the countries that would probably be most affected are those that have:

the largest external financing needs;

the largest share of unhedged debt denominated in US dollars; and

weak domestic motors of growth and sources of finance which make it harder to face higher international interest rates.

Again, data serves to provide some insights, conveying that Latin American governments allowed economic fundamentals to worsen in a period of high global liquidity and capital inflows:

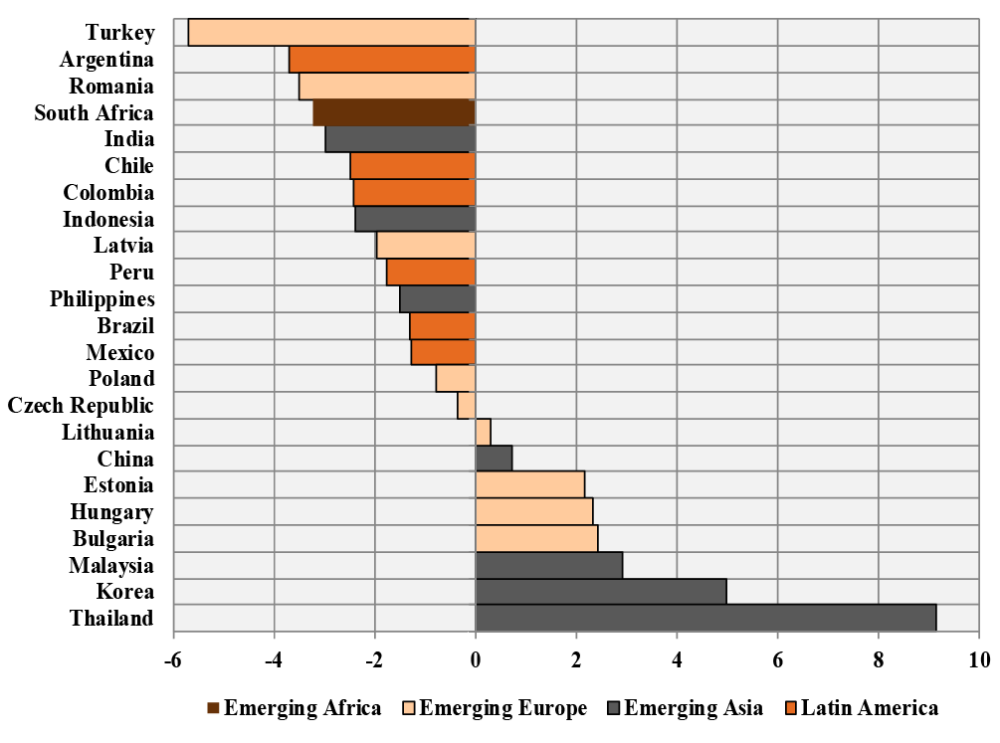

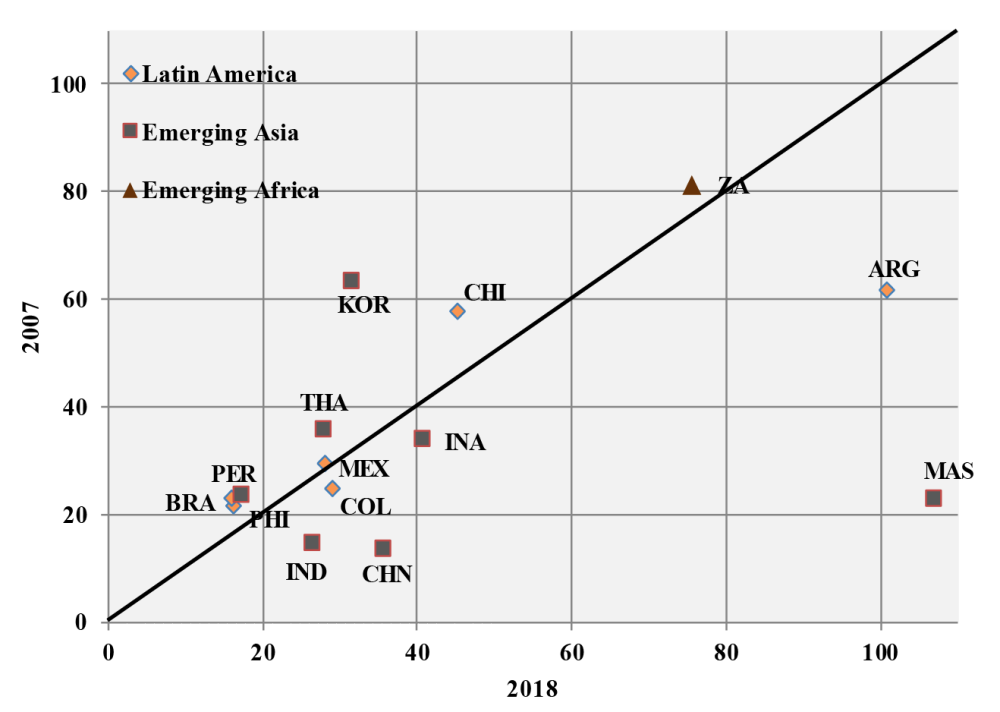

Among emerging markets, Latin America stands out as relatively vulnerable in terms of external financing needs, given the current account deficit persistence in a number of countries. Figure 2 below compares a sample of emerging markets’ pre-global crisis current account balances, where most Latin American countries were experiencing surpluses, to the latest available observations where all Latin American countries were running deficits.

Figure 2. Current Account Balance / GDP (in percentages)

2007

2018

Source: IMF-WEO

If we were to rank Emerging Market countries by their current account positions, Turkey and Argentina display the worst ratios of current account balance to GDP (although, of course, Argentina counts right now with the IMF support).

In some countries, the mirror image of large external financing needs has been large fiscal deficits. Argentina is the clearest case in point. But the truth of the matter is that most Latin American countries, including those without large external financing needs, are currently lacking fiscal space to undertake countercyclical fiscal policies in case of shocks. Brazil is a good example.

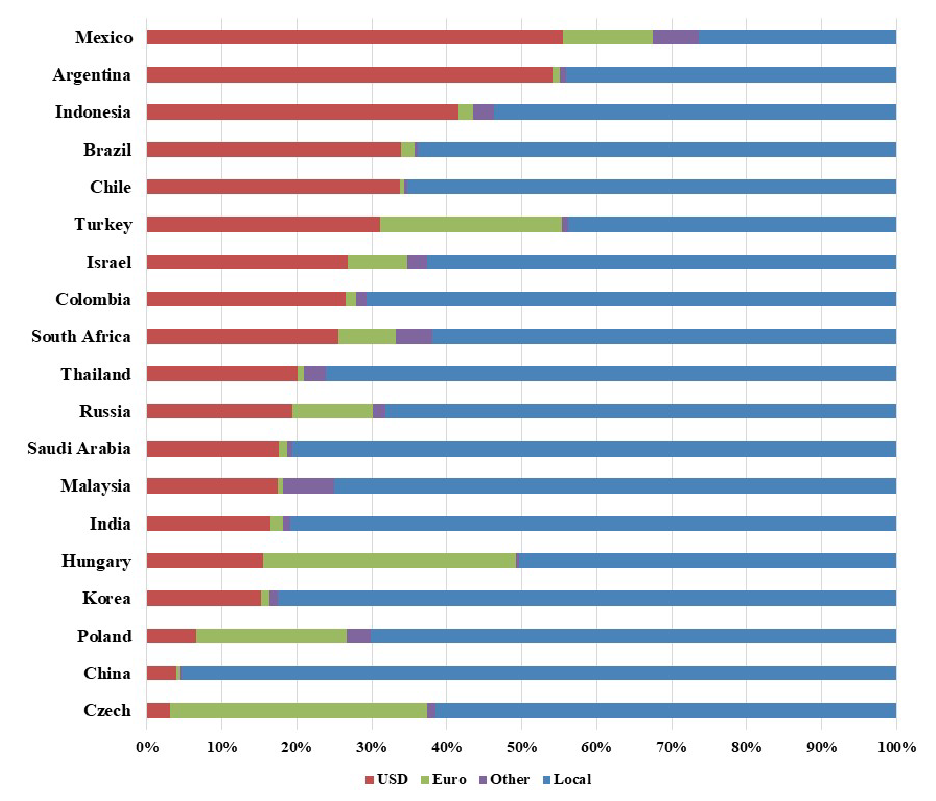

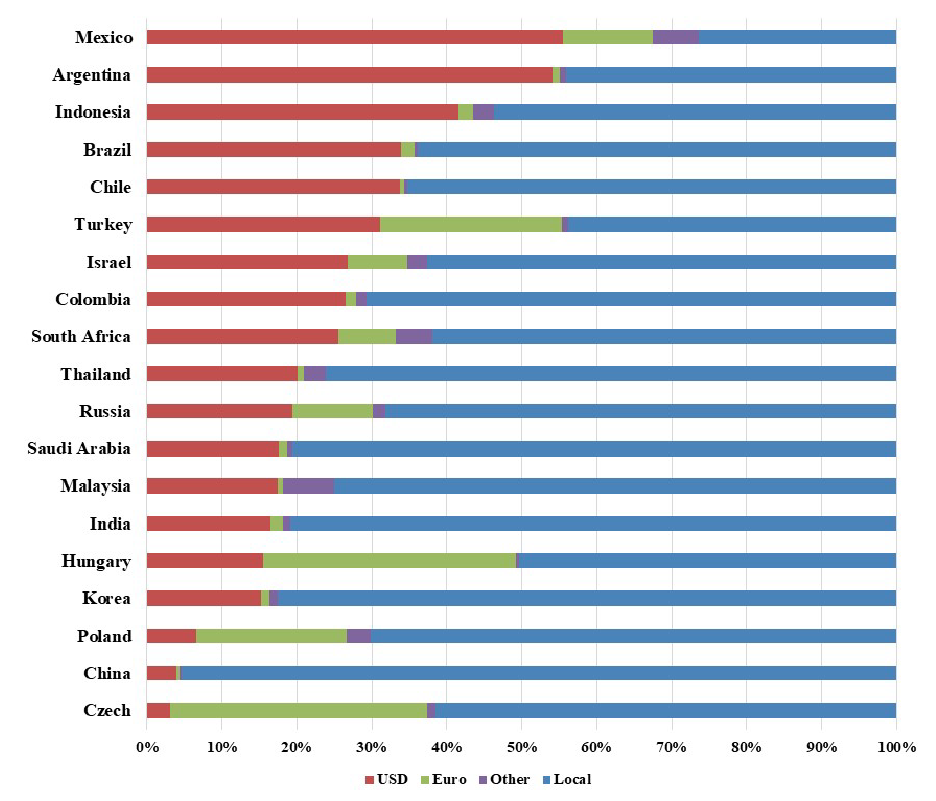

Regarding the share of debt denominated in US dollars, available data show that Latin American corporations display the largest ratios, led by Mexico, Argentina, and Brazil (see Figure 3 below). A note of caution, however, is that we don’t know what proportion of this debt is hedged against exchange rate fluctuations. But experience also shows that the value of the hedges decreases significantly during periods of stress.

On growth dynamics, except for Chile, most countries in Latin America lack internal and sustainable motors of growth. The June 2018 issue of the World Bank Global Economic Prospects reveals two very discouraging facts: the first is that per capita potential growth in Latin America is below the average for developing countries as a whole. The second is that potential growth is expected to decline further in the region due to sustained weakness in productivity as well as slower labor force growth and capital accumulation.

Now, it would not be fair to talk about resilience by focusing only on vulnerabilities. Moving to a discussion on strengths, it’s important to note four important sources:

Although fiscal space is quite limited, central bank policies in most countries in Latin America have been adequate, keeping inflation within their announced targets (again Argentina is an exception along with the more obvious case of Venezuela) and there is sufficient space for counter-cyclical monetary policies.

Despite the abundance of stresses, no systemic domestic banking crisis has emerged. Not even during the recent Brazilian and Argentinean recessions. This is a great accomplishment as lack of banking problems gives more degrees of freedom to the implementation of counter-cyclical monetary policies.

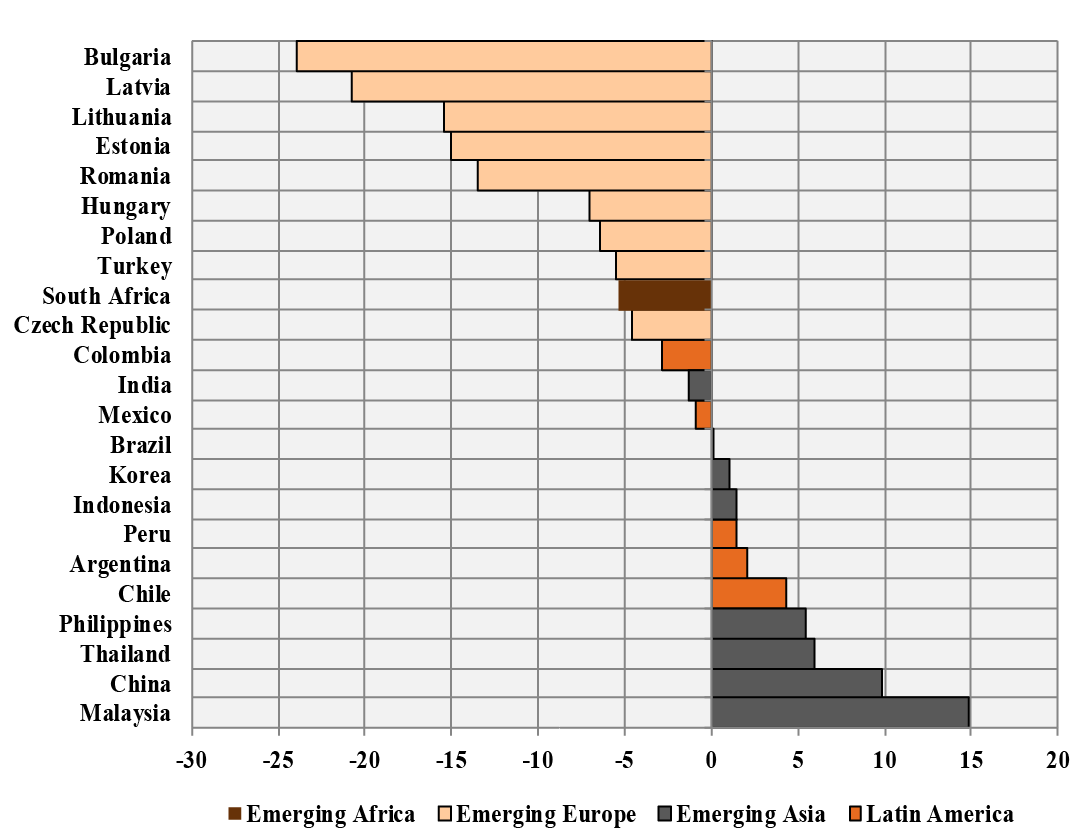

Low ratios of short-term external debt to international reserves is an additional source of strength (see Figure 4 below). Indeed, I strongly believe that this is the central variable to watch to make forecasts about Latin American countries’ abilities to meet further deteriorations in the international environment. Argentina lost huge amount of international reserves during the previous administration and is now paying the price.

Figure 4. Short-term External Debt/ Gross International Reserves (%)

Source: Own elaboration based The World Bank-IMG Quarterly External Statistics

Exchange rate flexibility has also played an important role as a shock absorber to external shocks. However, these benefits have been supported in the last years by the abundance of global liquidity. As global liquidity declines and risk aversion increases, countries facing a combination of high refinancing needs and important currency mismatches might find that sharp depreciation of their currencies become a problem for maintaining financial stability.

It is the capacity to contain vulnerabilities and improve strengths discussed above that will determine each country’s resilience to face the external challenges of 2019.

3. What can policymakers in the region do?

The challenge for policymakers is clear: how to manage the bumpy and protracted transition from abundant global liquidity—where fundamentals could afford to take the back seat because finding external of finance was an easy task—to a world where strong fundamentals become (once again) the name of the game.

Each country has its own list of pending long-term structural reforms that requires significant attention, including fiscal and labor reforms. Here, however, I will advance three recommendations centered on what policymakers should be doing right now.

“Be practical.”

While recognizing that structural reforms need to be in place, the truth is that recent surveys by Latinobarometro show that the public confidence on institutions and powers of the state (especially Congress and the judiciary) has been on a consistent downward trend in the last decade. Passing reforms in this environment is particularly difficult, especially when the external pressures are for less growth. In this situation, my view is to protect the independence of those institutions that could prove highly effective if international conditions worsen further. Very specifically, I’m talking about the central banks. As in advanced economies, central banks are the ones that can quickly put in place policies (monetary and macro-prudential) that can minimize the costs of a shock.

“Build up buffers.”

This recommendation, also acknowledged by the 2019 Global Economic Prospects, relates to the first recommendation because several of these buffers can be put in place without political confrontation. In addition to continue efforts to maintain high stocks of international reserves, an active debt management strategy needs to be given high priority, including acquiring information about the degree of unhedged currency exposures of the private sector. Moreover, it is important to establish access to available credit lines from multilateral organizations. One example is access to the Flexible Line of Credit of the IMF. At the moment, only two countries in the region—Mexico and Colombia—have access to this line, although there are others that qualify. Also, it is advisable to explore the establishment of currency swaps arrangements between central banks in the region and between these and the Fed.

“Learn from recent good and bad experiences in other emerging markets.”

One example, discussed by the Latin America Committee on Macroeconomic and financial Issues (CLAAF), is the lessons that the recent experience in Argentina provide for Brazil: In dealing with the fiscal problems inherited from the previous administration, Macri’s government in Argentina undertook an extremely gradual fiscal adjustment. This over-gradualism implied the continuous accumulation of debt, whose service became unsustainable. Right now, the new administration in Brazil is also facing the need for a very large fiscal adjustment—indeed much larger than Argentina (5 to 6 percent of GDP)—to stabilize domestic public debt. Not doing so puts Brazil at risk to join the list of EMDE countries facing severe debt sustainability problems which involves high interest rates and a constraint on economic growth. Under the current external environment, Brazil has even less space for excessive gradualism than Argentina.

Without doubt, we’ll have plenty of news coming from Latin America in 2019. Let’s hope for a positive balance.

Al comenzar el 2019, se ha estado formando un consenso cada vez mayor entre los expertos y los participantes en el mercado: la mayor volatilidad en los mercados internacionales de capital y las crecientes tensiones comerciales del 2018 no disminuirán en el 2019, y de hecho pueden tener spillovers negativos sobre el crecimiento económico y la estabilidad en economías emergentes y en desarrollo (EMDE). ¿Cómo moldeará este desafiante entorno internacional las perspectivas para América Latina? Como panelista en un evento reciente de CGD sobre el estado de la economía mundial y las perspectivas de desarrollo para los EMDE, resolví este problema respondiendo a tres preguntas:

¿Cuáles son los factores externos más importantes que afectan a América Latina?

¿Qué tan resistente es la región a los choques externos?

Y, finalmente, ¿qué pueden hacer los policymakers?

A continuación, presento respuestas detalladas para cada uno, incluyendo recomendaciones que policymakers pueden tomar.

1. ¿Cuáles son los factores externos más importantes que afectan el crecimiento y estabilidad en el 2019 a América Latina?

La respuesta breve: las incertidumbres políticas en los Estados Unidos.

En los últimos años, el desarrollo de países como China y Estados Unidos han sido factores externos clave que afectan las variables económicas y financieras en América Latina. Si bien los desarrollos comerciales y financieros interactúan entre sí, el efecto de China se ha producido principalmente a través del canal de comercio, mientras que el efecto de los Estados Unidos ha sido mayormente a través del canal financiero.

Por ejemplo, debido a la gran cantidad de exportadores de productos básicos en la región, la desaceleración de China, asociada con la disminución de los precios de los commodities, ha afectado el ritmo del crecimiento en la región desde 2014. Del mismo modo, la evolución financiera en los Estados Unidos - por ejemplo, el colapso de Lehman Brothers en 2008, que marcó el inicio de la crisis financiera mundial; la sugerencia de Ben Bernanke en mayo del 2013 de que la FED podría comenzar a reducir su tasa de expansión de liquidez (el llamado Taper Tantrum); y la fuerte volatilidad de los mercados de valores estadounidenses en 2018 - aumentó la aversión al riesgo de los inversores y redujo su apetito por los activos de las EMDEs, incluidos los de América Latina. En estas tres ocasiones, la región no se salvó de la reducción de las entradas netas de capital que se produjo.

En el 2019, hay consenso sobre una nueva desaceleración en el crecimiento económico de China. Sin embargo, creo que esta desaceleración ya se ha internalizado en los precios de los commodities y, en base a experiencias pasadas, la respuesta de los policymakers de China también ha sido altamente anticipada.

En contraste, la incertidumbre política en Estados Unidos sigue siendo alta y no hay signos de mejoras en el futuro previsible. Por lo tanto, en mi opinión, el desarrollo en los Estados Unidos será el factor externo más influyente que afecte el crecimiento económico y la estabilidad financiera de América Latina.

Específicamente, las tres fuentes clave de incertidumbre son:

el comportamiento de las tasas de la FED;

la apreciación del dólar; y

la guerra proteccionista liderada por Trump y su postura nacionalista.

Estos son el foco de la volatilidad actual en los mercados financieros internacionales, y pueden continuar disminuyendo la demanda de los inversionistas por los activos de las EMDEs, de los cuales América Latina es un proveedor importante.

Las cifras sobre el comportamiento reciente de la deuda externa en América Latina proporcionan una ilustración inicial de los problemas potenciales que la región podría enfrentar si las incertidumbres en las políticas de los Estados Unidos resultasen en un mayor aumento de la aversión al riesgo de los inversionistas y, por lo tanto, mayores caídas en las entradas de capital:

Si bien la emisión de títulos de deuda externa (bonos) aumentó sustancialmente en todas las regiones de las EMDEs desde el 2010, y la última discusión se centró en la emisión de títulos de deuda por parte de corporaciones no financieras, en América Latina, la emisión de deuda pública también se aceleró de manera muy rápida, al mismo ritmo de otras regiones como Asia (ver la Figura 1 a continuación). En la mayoría de los países de América Latina, la proporción del total de títulos de deuda externa con respecto al PIB se ha más que duplicado desde el 2010 (y esto, sin incluir otras fuentes de deuda externa, como los préstamos internacionales). Por supuesto, los países difieren significativamente. Por ejemplo, en Argentina, la deuda del gobierno representa la mayor parte de los valores de deuda externa; mientras que en Chile se trata principalmente de un problema del sector privado.

Entre los seis países más grandes de América Latina, excluyendo México y Perú, el servicio de la deuda externa total (amortización y pago de intereses) como porcentaje del PIB también ha aumentado significativamente, alcanzando el 16 y el 18 por ciento. Como referencia, para 2017 esta proporción era de alrededor del 20 por ciento en Turquía.

Esto me lleva a mi segunda pregunta:

2. ¿Qué tan resistente es América Latina a un mayor deterioro en el entorno internacional?

De acuerdo con las principales fuentes de incertidumbre en los Estados Unidos descritas anteriormente, los países que probablemente se verían más afectados son aquellos que tienen:

las mayores necesidades de financiamiento externo;

la mayor parte de la deuda no cubierta denominada en dólares estadounidenses; y

motores domésticos débiles de crecimiento y fuentes de financiamiento que hacen más difícil enfrentar tasas de interés internacionales más altas.

Nuevamente, los datos sirven para proporcionar algunas ideas, ya que los gobiernos de América Latina permitieron que los fundamentos empeoren en un período de alta liquidez global y flujos de capital:

Entre los mercados emergentes, América Latina se destaca como relativamente vulnerable en términos de necesidades de financiamiento externo, dada la persistencia del déficit en cuenta corriente en varios países. La Figura 2 a continuación compara una muestra de los saldos de la cuenta corriente pre-crisis global de los mercados emergentes, donde la mayoría de los países de América Latina estaban experimentando superávit, con las últimas observaciones disponibles, donde todos los países de América Latina tenían déficit.

Si tuviéramos que clasificar a los países de Mercados Emergentes por sus posiciones de cuenta corriente, Turquía y Argentina muestran los peores índices de saldo de cuenta corriente con respecto al PIB (aunque, por supuesto, Argentina cuenta ahora con el apoyo del FMI).

En algunos países, la imagen reflejada de las grandes necesidades de financiamiento externo ha sido un gran déficit fiscal. Argentina es el caso más claro en este punto. La verdad del asunto, sin embargo, es que la mayoría de los países latinoamericanos, incluidos aquellos sin grandes necesidades de financiamiento externo, carecen actualmente de espacio fiscal para emprender políticas fiscales anticíclicas en caso de crisis. Brasil es un buen ejemplo.

Con respecto a la proporción de la deuda denominada en dólares estadounidenses, los datos disponibles muestran que las corporaciones latinoamericanas muestran los índices más altos, liderados por México, Argentina y Brasil (Figura 3 a continuación). Sin embargo, algo a tomar en cuenta es que no sabemos qué proporción de esta deuda está cubierta contra las fluctuaciones del tipo de cambio. Pero la experiencia también muestra que el valor de las coberturas disminuye significativamente durante los períodos de estrés.

En cuanto a la dinámica de crecimiento, a excepción de Chile, la mayoría de los países de América Latina carecen de motores de crecimiento internos y sostenibles. La edición de junio de 2018 de las Perspectivas Económicas Mundiales del Banco Mundial revela dos hechos muy desalentadores: el primero es que el crecimiento potencial per cápita en América Latina está por debajo del promedio de los países en desarrollo en general. La segunda es que se espera que el crecimiento potencial disminuya aún más en la región debido a la debilidad sostenida en la productividad, así como al menor crecimiento de la fuerza laboral y la acumulación de capital.

Ahora, no sería justo hablar de resiliencia al centrarse solo en las vulnerabilidades. Pasando a discutir sobre las fortalezas, es importante tener en cuenta cuatro fuentes importantes:

Si bien el espacio fiscal es bastante limitado, las políticas de los bancos centrales en la mayoría de los países de América Latina han sido adecuadas, manteniendo la inflación dentro de sus rangos anunciados (de nuevo, Argentina es una excepción junto con el caso más obvio de Venezuela) y hay suficiente espacio para políticas monetarias anticíclicas.

A pesar de la abundancia de estreses, no ha surgido ninguna crisis doméstica bancaria sistémica. Ni siquiera durante las últimas recesiones brasileñas y argentinas. Este es un gran logro, ya que la falta de problemas bancarios otorga más grados de libertad a la implementación de políticas monetarias anticíclicas.

Los bajos índices de deuda externa a corto plazo con respecto a las reservas internacionales son una fuente adicional de fortaleza (ver la Figura 4 a continuación). De hecho, creo firmemente que esta es la variable central que se debe observar para hacer pronósticos sobre la capacidad de los países de América Latina para enfrentar mayores deterioros en el entorno internacional. Argentina perdió una gran cantidad de reservas internacionales durante la administración anterior y ahora está pagando el precio.

La flexibilidad del tipo de cambio también ha jugado un papel importante como amortiguador de choques externos. Sin embargo, estos beneficios han sido apoyados en los últimos años por la abundancia de liquidez global. A medida que la liquidez global disminuye y la aversión al riesgo aumenta, los países que enfrentan una combinación de altas necesidades de refinanciamiento e importantes desajustes cambiarios pueden encontrar que la fuerte depreciación de sus monedas se convierta en un problema para mantener la estabilidad financiera.

Es la capacidad para contener las vulnerabilidades y mejorar las fortalezas discutidas anteriormente lo que determinará la capacidad de resistencia de cada país para enfrentar los desafíos externos del 2019.

3. ¿Qué pueden hacer los policymakers en la región?

El desafío para los responsables de la formulación de políticas es claro: cómo manejar la transición irregular y prolongada de la abundante liquidez global, dónde los fundamentales podrían permitirse estar en un estado de subordinación, porque era una tarea fácil encontrar recursos externos a un mundo en el que los fundamentales se vuelven (una vez más) el nombre del juego.

Cada país tiene su propia lista de reformas estructurales pendientes a largo plazo que requieren una atención significativa, incluidas reformas fiscales y laborales. Aquí, sin embargo, adelantaré tres recomendaciones centradas en lo que deberían hacer los policymakers en este momento.

"Ser práctico."

Si bien reconocemos que las reformas estructurales deben implementarse, lo cierto es que las encuestas recientes realizadas por Latinobarometro muestran que la confianza pública en las instituciones y los poderes del estado (especialmente el Congreso y el Poder Judicial) ha estado en una tendencia constante a la baja en la última década. La aprobación de las reformas en este entorno es particularmente difícil, especialmente cuando las presiones externas son para un menor crecimiento. En esta situación, mi opinión es proteger la independencia de aquellas instituciones que podrían resultar altamente efectivas si las condiciones internacionales empeoran. Muy específicamente, estoy hablando de los bancos centrales. Al igual que en las economías avanzadas, los bancos centrales son los que pueden implementar rápidamente políticas (monetarias y macro prudenciales) que pueden minimizar los costos de un shock.

"Acumula reservas".

Esta recomendación, también reconocida por las Perspectivas Económicas Mundiales del 2019, se relaciona con la primera porque varios de estos amortiguadores pueden implementarse sin confrontación política. Además de continuar los esfuerzos para mantener un alto nivel de reservas internacionales, se debe dar una alta prioridad a una estrategia de gestión activa de la deuda, incluida la adquisición de información sobre el grado de exposición a las divisas no cubiertas del sector privado. Además, es importante establecer el acceso a las líneas de crédito disponibles de las organizaciones multilaterales. Un ejemplo es el acceso a la Línea de Crédito Flexible del FMI. Por el momento, solo dos países de la región, México y Colombia tienen acceso a esta línea, aunque hay otros que califican. Además, es aconsejable explorar el establecimiento de acuerdos de canje de divisas entre los bancos centrales de la región y entre éstos y la Reserva Federal.

"Aprenda de las experiencias recientes buenas y malas en otros mercados emergentes".

Un ejemplo, discutido por el Comité de Asuntos Macroeconómicos y Financieros de América Latina (CLAAF), son las lecciones que la experiencia reciente en Argentina brinda a Brasil: al enfrentar los problemas fiscales heredados de la administración anterior, el gobierno de Macri en Argentina emprendió un ajuste fiscal gradual. Este exceso de gradualidad implicó la continua acumulación de deuda, cuyo servicio se hizo insostenible. En este momento, la nueva administración en Brasil también enfrenta la necesidad de un ajuste fiscal muy grande, de hecho, mucho más grande que Argentina (5 a 6 por ciento del PIB), para estabilizar la deuda pública interna. No hacerlo pone a Brasil en riesgo de unirse a la lista de países de EMDE que enfrentan graves problemas de sostenibilidad de la deuda, lo que implica altas tasas de interés y una restricción en el crecimiento económico. Bajo el entorno externo actual, Brasil tiene aún menos espacio para el gradualismo excesivo que Argentina.

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.