Recommended

Ride-hailing is one of the platform success stories in many African countries. US leader Uber was the first into most markets, but Estonian challenger Taxify now claims to be larger, with 2.4 million active riders compared to Uber’s 1.3 million. Both companies—as well as a number of smaller competitors—have expanded their offerings, pushing farther downmarket and incorporating motorbike and tuk tuk modes of transportation as well as an increasing range of private car options.

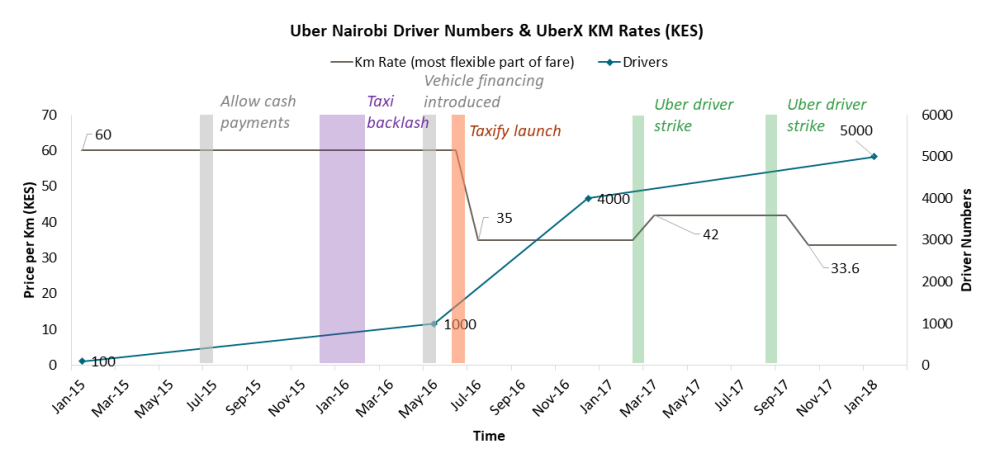

What has the growth of ride-hailing platforms meant for employment in Africa? Taxify claims to have “hundreds of thousands” of drivers across the continent, but exact numbers are hard to come by. The latest media coverage in Nairobi suggests that there are about 5,000 drivers on the Uber platform there. Spikes in the issuing of public service vehicle licenses (required for both taxis and platform-registered vehicles) and registrations of eligible cars suggest that there are likely some overall net gains in transport livelihoods, gains made possible by the fact that platforms dramatically lowered prices and expanded the private transport market.

The number of drivers may be rising, but is their income falling?

Yet, a succession of strikes and protests by quickly mobilized driver associations in Kenya, Nigeria, South Africa, Ghana, and Uganda force us to think about whether these new jobs are good jobs, and whether competition among some of the biggest players is delivering efficiencies or creating a new race to the bottom in driver wages.

Although the platforms are loss-making they are well capitalized, and as long as new drivers are available to join the platforms, there seems to be no floor to the price that platforms are willing to set in the quest for greater market share. As of August 2018, minimum passenger fares for UberX were US$1.75 in Nairobi, US$1.81 in Johannesburg, and US$1.11 in Lagos. The competition among platform players extends beyond pricing: Taxify tries to attract drivers by taking a lower commission on driver revenues (10-20 percent for Taxify versus 25 percent on Uber), and both subsidize passenger-facing promotions for free and discounted rides.

There are a few things about African markets that make these experiences so distinct from the West. First, the opportunity landscape for formal work is limited. As pointed out in an earlier post in this series, only 17 percent of workers in Kenya are in the formal economy. Unemployment in South Africa is at 26.7 percent.

Second, in these markets, vehicles—cars more than motorbikes—are rarely idle assets to be put to work part-time to make supplemental income. Drivers either make a substantial investment to purchase their own vehicle or they lease one from a so-called partner who is a vehicle owner and keeps a share of driver earnings, which are typically pooled across multiple platforms. This investment is based on wage expectations that can at any moment be dramatically altered by the unilateral decision of a platform company. Rather than merely facilitating many transactions between buyers and sellers, large platforms are price setters, creating “perfect” markets by fiat.

But, because of vehicle investments and limited opportunity landscapes, exit frictions are significant. When drivers are lured to a platform at one price and instantaneously face a different set of prices, they feel stuck and angry, even if wages themselves appear to be multiples above local minimums.

This appears to be what we have been witnessing in Kenya as Uber and Taxify have slashed fares, battling over market dominance and attempting to force one another out of the market. Growing rider numbers and relatively high fares lured many new drivers to Uber in Kenya, which slashed prices just as Taxify entered the market. Uber defended the move, claiming that it doubled ridership and increased drivers’ trips per day by 70 percent. Still, the first strike of Uber drivers took place in March 2017, successfully achieving a short-lived price increase. The need for work, however, continued to attract new drivers even after two driver strikes in 2017. In July 2018, Uber and Taxify appeared to yield to pressure from a week-long strike led by driver associations and—with nudging from the Ministry of Transportation—signed a non-binding agreement to set a floor on rates as recommended by the Kenya Automobile Association. However, neither platform implemented the new floor, leading to a new strike in September 2018.

Figure 1. Uber driver numbers and price-per-kilometer changes in Kenya

Note: We stop in February 2018, when Uber diversified offerings (Uber Chap Chap, UberX, Uber Select), making it impossible to track driver numbers and price changes from press releases and media reports alone. We focus only on the variable kilometer price here, though there are also varying base fares and driver volume incentives. The kilometer rate appears to be the most volatile and contested by drivers in Kenya.

Sources: Uber press releases (1, 2, 3) and media reports (1, 2, 3, 4).

Is app-based driving good work?

So, is app-based driving good work? Without objective data on driver earnings, hourly wages, and satisfaction, it is impossible to know for sure. However, somewhat stable driver numbers seem to suggest that—even if not a good livelihood—it may indeed be better than available alternatives.

The cost of the car may create barriers to entry that might keep incomes at livable levels. Customers enjoy the convenience and low prices, and platform investors seem willing to underwrite the fight for market share. It is possible that platforms could make these jobs more attractive by adding driver benefits, like facilitating access to Kenya’s National Health Insurance Fund for basic health insurance.

But, what drivers seem to most want are higher profits and some protection from the shocks of platforms’ overnight price cuts. On this core issue, driver collective action appears to have achieved little by way of changing platform decisions or government incentives to intervene. Lured to platforms by the mirage of good work, drivers in Africa are now confronting the reality of precarious revenues. Rather than good work, they have ended up with work that is merely good enough.

This blog post is part of a series from CGD's Study Group on Technology, Comparative Advantage, and Development Prospects that is exploring issues of jobs and paths of economic development in the context of technological change. You can find the group’s latest research at cgdev.org/future-of-work.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

More Reading

SPEECH

The Future of Global Development and Implications for Aid

Blog Post

Using Space to Spark Global Prosperity