Recommended

POLICY PAPER

Do Climate Targets Affect Lending at the World Bank?

The World Bank has targets for the proportion of its lending that can be labeled climate finance. It demands every project appraisal must discuss how the investment fits with national and international goals around mitigation and adaptation. And it uses a “shadow price” of carbon to inform project selection and design choices. How much does all of this make a difference to what the World Bank actually finances? In a new policy paper, I try to answer that question looking at both finance trends and the project appraisal documents (PADs) presented to the World Bank’s Board. The answer: it seems likely the climate focus has had some impact, and likely the impact isn’t very big.

The first reason to believe that the impact of climate finance targets has been limited involves country allocation. Previous CGD work has suggested that World Bank climate finance is poorly allocated across countries in terms of adaption needs or importance in the mitigation fight. That will be in large part because country allocation mechanisms for IDA haven’t substantially changed in response to climate needs, and IBRD lending remains largely determined by client demand.

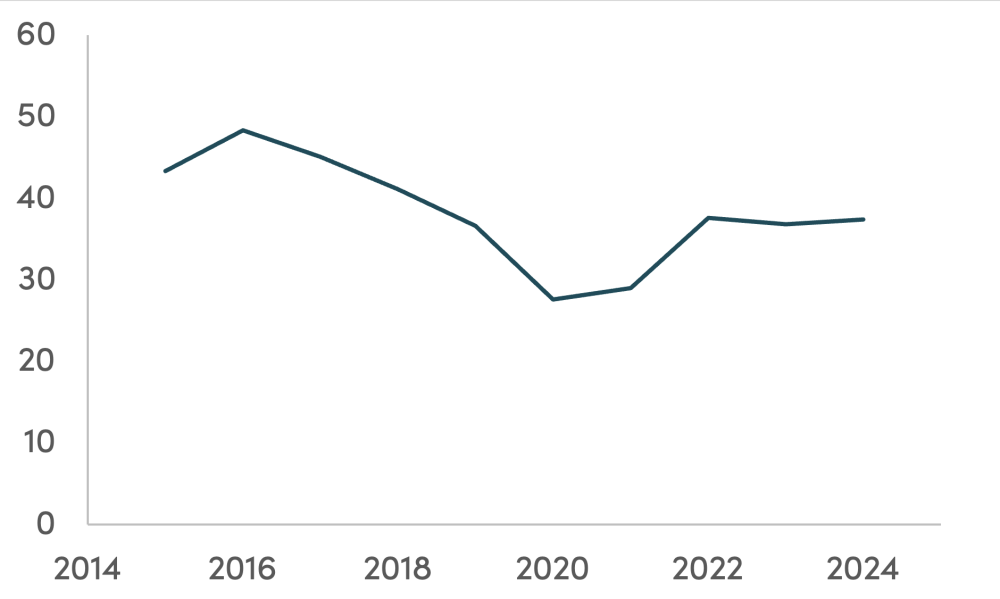

A second reason to doubt significant change involves looking at sectoral lending trends. A focus on climate concerns would suggest more financing for the “climate” sectors, infrastructure (and in particular electricity) and agriculture. But the last ten years of data don’t show a marked change in the lending pattern (see Figure 1).

Figure 1. Percentage of World Bank lending to climate sectors FY15–24

At the project level, looking at 347 World Bank project appraisal documents from 2024, there is some evidence that, on occasion, the Bank has financed electricity production technologies that are chosen on the grounds of lowest cost only including a shadow price of carbon, and perhaps one or two projects that appear to have little rationale beyond their climate impact.

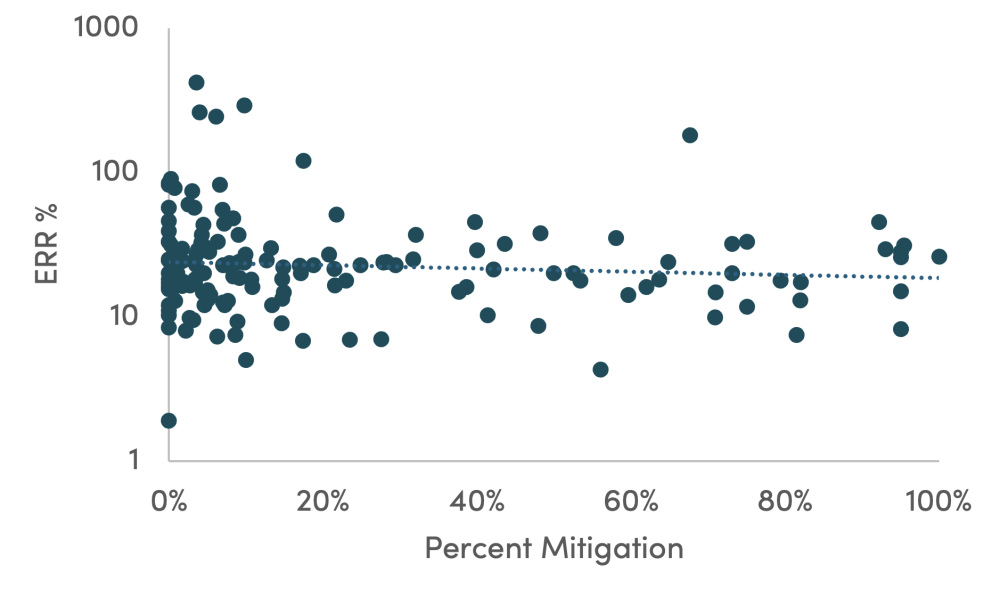

But a third reason for doubting significant impact of climate targets is that there is little evidence overall that the Bank is choosing climate projects over non-climate projects with higher local development impact. Projects where most of the cost is labeled as climate finance do not see lower predicted local economic rates of return (ERRs) than projects with low or no climate finance shares. That is something you might expect if the World Bank was trading development effectiveness for mitigation impact more broadly (see Figure 2).

At the same time, there is no link between the proportion of project finance marked as mitigation and the share of total ERRs (including impact on emissions) driven by emissions impact. That is a finding matching previous CGD work, which has suggested it is difficult to tell why much of the World Bank’s climate finance is labeled as such, and that estimated cost effectiveness in terms of climate outcomes varies by orders of magnitude across projects.

Figure 2. Percentage of project finance labeled mitigation and local economic rate of return

The bottom line: there are reasons to think climate finance targets and the shadow price of carbon have been part of at least a marginal change in the World Bank project mix but strong reasons to think they haven’t been part of a revolutionary change. Beyond that, it isn’t possible from the outside (or indeed very plausibly from the inside at the aggregate level) to know how different the portfolio looks because of the focus on climate, nor what is the impact of that on the average local economic return to World Bank investments, nor the impact on emissions. And reported climate finance numbers only appear to help at the very margin in any of those regards.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: Adobe Stock