Recommended

Introduction

The global impact of the COVID-19 pandemic on economic output and public finances in 2020 and beyond is projected to be massive. Fiscal policy can have a crucial role in mitigating the pandemic’s overall economic impact and promoting a quick recovery. It can help save lives and shield the most-affected segments of population.

Both advanced and developing countries have responded to the pandemic by implementing several fiscal measures. As of early April, their fiscal costs ranged between 1 percent and 34 percent of GDP— larger fiscal packages have been announced by advanced economies, such as Germany and Italy. These packages include revenue and expenditure measures as well as liquidity support to businesses (such as loans or loan guarantees). The International Monetary Fund (IMF) has estimated that the global cost of fiscal measures (including increased allocations for health) implemented so far is $8 trillion, or 9 percent of global GDP. The fiscal cost is rising as countries implement additional measures, including, for example, India, Japan and the US.

Policymakers in low-income countries have implemented a range of fiscal measures to provide income support to the households and sectors most affected by the COVID-19 pandemic, made possible by expansionary fiscal policy and international support. The announced measures have included reductions in standard VAT rate, personal and corporate income tax, and turnover tax (Kenya); support to hotels, restaurants, and transport, including suspension of VAT paid by these sectors (Senegal); and waiver of import duty on medical equipment (Bangladesh, Nigeria, and Zambia). Bangladesh has announced sizeable financial support to all large, medium, small and micro enterprises, costing 3.5 percent of GDP. In Senegal, additional spending and tax concessions granted so far are expected to raise the fiscal deficit by 2.4 percent of GDP in 2020. Nigeria and Zambia have been hit by falling commodity prices, drastically weakening their revenue position.

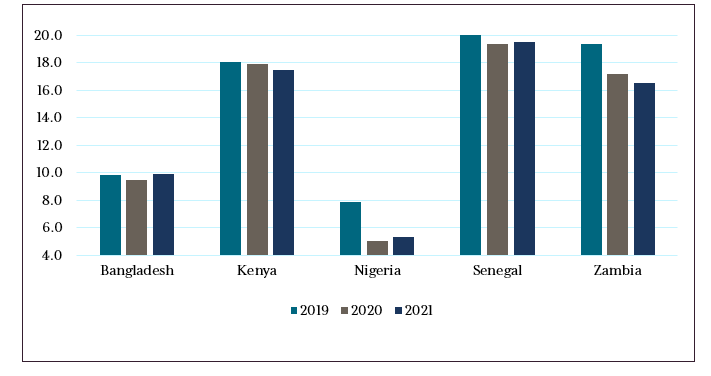

Together with lower projected output growth, the above measures would reduce revenues in relation to GDP in 2020 and possibly beyond (Figure 1), with important implications for public spending (Figure 2). These projections were prepared by the IMF at the end of March/early April, as the crisis was unfolding. The revised IMF projections expected in June are likely to show a further fall in outputs and worsening fiscal positions of these countries. A word of caution: expressing revenues and expenditures in relation to GDP understates the seriousness of the fall in the ratio when GDP is contracting. As a result, the fall in revenue/expenditure per head could be significant.

Figure 1. Revenue (% of GDP) in five countries, 2019-2021

Data source: Fiscal Monitor (April 2020)

Figure 2. Expenditure (% of GDP) in five countries, 2019-2021

Data source: Fiscal Monitor (April 2020)

The Center for Global Development has been studying revenue mobilization in four countries in sub-Saharan Africa (Kenya, Nigeria, Senegal, and Zambia) and one in Asia (Bangladesh). Conducted by scholars based in the region, the studies analyzed tax and spending policies in the five countries over the past 20 years to unearth the political and structural impediments to raising domestic revenues and spending efficiently. These studies concluded that the real constraint to raising more revenues and improving spending quality has been political in nature.

However, COVID-19 has reshaped the political and economic landscape of these countries in different ways.

First, as noted above, many taxes have been lowered to provide support to businesses and households. This is likely to make future tax reforms even more challenging politically, given vested interests. For example, there could be opposition to raising the standard VAT rate from 14 percent back to 16 percent in Kenya, given the strong resistance the government faced when it imposed VAT on petroleum products in 2018.

Second, the crisis is likely to alter the economic structure of these countries in a major way, at least in the foreseeable future. Countries that rely on tourism will witness a large-scale contraction of the sector in the short term. Because of falling commodity prices, natural-resource dependent countries will face a large revenue decline. On top of this, remittance flows are expected to drop.

Third, despite debt relief granted by official creditors to many low-income countries, their debt-to-GDP ratio is likely to rise from already high levels because of falling output and expansionary fiscal policies. For example, the average debt-to-GDP ratio stood at 57 percent in 2019 in sub-Saharan Africa. Finally, the outlook for aid flows is likely to change. Prior to COVID-19, the average debt-to-GDP ratio for advanced countries exceeded 100 percent; it was projected to surpass 115 percent in early April, and additional fiscal measures implemented since then in these countries will further add to debt.

This piece argues that an important implication of the changing landscape is that low-income country policymakers would have to reconsider their revenue-raising strategy in favor of an approach that embraces a comprehensive reform package, including policies that have encountered political opposition in the past. The package must also include reversal of tax measures introduced in response to COVID-19 that are poorly targeted (such as the VAT rate cut and reductions in the top personal tax rate in Kenya). This strategy would garner popular support because it would be perceived as fair, with every citizen contributing to the country’s urgent needs. To induce taxpayers to take their obligations seriously and to ensure that taxpayers are getting their money’s worth, governments would have to spend their limited resources better. While this policy prescription is applicable to all low-income countries, we draw on the five case studies to amplify the argument.

A comprehensive reform package would receive support from the international community. Already, donors are pressuring developing countries to collect more taxes domestically to help achieve the Sustainable Development Goals (SDGs), reflected in the seven action areas in Addis Agenda for financing for development adopted in 2015. This is because the financing required to achieve the SDGs is large. Additional spending—public and private—required to achieve SDGs by 2030 in five areas (education, health, roads, electricity, water, and sanitation) was estimated by the IMF before the crisis to average 15 percent of GDP for low-income countries. Underlying these projections is the belief that if average tax-to-GDP ratios in low-income countries were to increase by at least 5 percent of GDP by 2030, the remaining resources could be found from other sources.

Key revenue and expenditure characteristics

Before turning to a discussion of key political and other impediments to raising revenues in the five studied countries, a brief description of their key revenue and spending characteristics is in order. (Appendix tables 1 through 3 present the evolution of the revenue and expenditure structure of the five countries between 2000 and 2017.)

Senegal has increased its tax-to-GDP ratio the most since 2000; by contrast, Nigeria and Zambia have witnessed a decline in the ratio. In Nigeria, this was accompanied by a major drop in resource revenues. Contrary to general belief, receipts from income taxes as a share of GDP have increased in all countries between 2000 and 2017. On the other hand, receipts from the VAT—the tax with most revenue potential—have increased marginally or stagnated. Little, if any, revenue is collected from property taxes in these countries.

Spending varies across these countries, with Kenya spending the most in relation to GDP and Bangladesh, the least; this is largely a reflection of these countries’ revenue-raising capacities. In two countries—Kenya and Senegal—capital spending has increased manifold in the 17-year period under study. Because of the rising debt-to-GDP ratio, interest expense as a share of tax revenues has increased, constituting 36 percent of tax receipts in Nigeria and 20 percent in Bangladesh and Kenya in 2017. Between 2000 and 2017, only two countries were able to increase spending on social benefits, though the quality of that spending remains questionable. This has important implications for responding to COVID-19: if a country lacks well-developed social programs, it is difficult for the government to transfer income to its population rapidly when a crisis—such as COVID-19—strikes. All countries spend substantially more on education than on health, with spending on the latter ranging between 0.4 percent and 1.9 percent of GDP. Going forward, these countries would need to allocate more to health and improve their public financial management systems to ensure that the budgeted amounts are actually spent. In virtually all countries, interest outlays are larger than those on health.

Political and other impediments to higher revenues

Despite the fact that countries’ underlying economic positions have changed as a result of the COVID-19 crisis, the five country studies provide valuable insights on the way forward. The country study authors identified a series of impediments to revenue mobilization. In the ensuing discussion, they are grouped into six categories.

Tax concessions. In all countries, favorable tax treatment accorded to certain consumers and producers has eroded the tax base. Tax concessions have taken several forms, such as exemptions from payment of import duties or taxes (such as the VAT) on domestic production, which has affected taxpayer morale. Tax concessions have their origins in part in industrial policy, but have morphed into protection for the politically connected. In Senegal, tax expenditures were estimated at 7.8 percent of GDP in 2014, accounting for 40 percent of tax revenues. The bulk of concessions have benefitted private enterprises, mostly multinationals operating in the mining sector. The identity of beneficiaries of tax concessions is not known, although the case study the author suggests that they have been granted to cronies. A similar picture emerges in Nigeria, where the government has enacted tax exemptions and tax holidays for enterprises to benefit the influential and politically connected, which has lowered the productivity of corporate taxes. From time to time, the federal government announces duty waivers and concessions on imports in the annual budget. In Kenya, companies often shut down their operations when tax concessions expire and open a new company with a different name in another jurisdiction to avail themselves of tax benefits. There is no public record of tax expenditures and their merits are not discussed at the time of the budget. Several goods are exempt from the VAT, which has affected its revenue performance.

The buoyancy of a tax system depends on how well it is able to capture the growing incomes in an economy’s expanding sectors over time. However, Bangladesh has exempted much of the income emanating from the fast-growing ready-made garment sector, and from companies producing power and engaged in emerging industries such as electronics and located in certain areas including export processing zones. The ready-made garment sector is the most dynamic segment of the economy, and its exports make up more than 12 percent of the GDP. Notwithstanding its growing importance, the sector hardly contributes to taxes. It enjoys a special corporate tax rate of 12 percent, in contrast with 35 percent for other non-listed companies. Even this lower tax rate is not paid by most firms in the sector, prompting the government to levy a minimum tax of 0.3 percent of its gross turnover.

In Zambia, the coverage of corporate taxes is limited to a subset of companies. The mining companies enjoy exemption from the VAT. In general, Zambia has generous tax incentives for companies, including duty-free importation of equipment and machinery. Companies investing more than US$10 million are able to negotiate special tax deals with the government. Most benefits accrue to large foreign companies, and as in other countries in the region, the government does not compile data on revenue foregone and beneficiaries of tax exemptions. The situation is compounded by poorly negotiated double-taxation agreements with 22 countries, which allow local multinationals to transfer profits to low tax jurisdictions.

Political fragmentation and policy uncertainty. Political fragmentation has led to frequent changes to tax policies, creating uncertainty for the private sector and undermining efforts to mobilize domestic resources. The most vivid case is that of Zambia, which changed its mining tax regime seven times during 2000 to 2019. Ostensibly, this arose out of the belief that the mining sector was not contributing enough to the country’s development, turning it into a key issue during elections. The tensions between the mining sector and the government have been accentuated by the opaqueness of the government’s dealing with the sector (including foreign operators) and the latter’s ability to secure favorable deals from the government. The varying tax burden has impaired the credibility of tax policies and fueled distrust between the government and key players in the economy. The unpredictability of tax policies continued in the 2018 budget which proposed abolishing the VAT introduced in 1995 and replacing it with a sales tax. This decision was reversed in the 2019 budget speech, even after introducing a bill six months earlier to adopt the sales tax.

A similar unpredictability has existed in Kenya with tax policy changes in every budget, reflecting political divisions. The turnover tax introduced in 2006 was replaced by a presumptive tax in 2019. The latter turned out to be ineffective due to noncompliance and lack of cooperation from county governments, leading to use of both turnover and presumptive taxes for medium and small enterprises. Bangladesh has faced uncertainty with the implementation of the 2012 VAT law, which has been repeatedly postponed since parliament approved it. Political and electoral considerations lie behind these postponements. Opposition to raising the VAT rate in Nigeria has kept the overall revenue level low.

Weak revenue administration. Weaknesses in administrative systems have hurt revenue mobilization efforts. In Kenya, the revenue authority lacks the capacity to conduct frequent audits to deter taxpayer noncompliance. Tax administration in Bangladesh is virtually unchanged from that inherited from the British colonial administration, and almost completely manual and paper based. The different cadres of tax officials work in silos as information across different wings is not shared or coordinated. Efforts to merge different cadres into one homogenous group have time after time been thwarted by officials. Tax administration is based on geographical administrative units rather than on functional lines as recommended by the experts. There is virtually no monitoring of withholding of wage incomes by administration. In Nigeria, customs collection is hampered by rampant smuggling of goods from neighboring countries, in particular Benin. Nigeria’s VAT yield is low in part because there is no threshold for registered taxpayers, leading to a large number of inactive taxpayers in the system. Political interference in senior appointments has further limited the effectiveness of tax administration. The lack of tax identification numbers continues to hamper tax collections in many countries. E-filings is limited; in Nigeria it has ranged between 2 and 3 percent of corporate and VAT filers.

Weak revenue administration is partly reflected in relatively low C-efficiency of the VAT in sample countries—that is, the extent to which actual tax collections are close to the potential. In Kenya, this ratio has fallen from 0.32 in 2010 to 0.29 in 2017, while in Nigeria and Senegal it has risen to 0.20 and 0.45, respectively during this period—and remains below 0.5 found in emerging economies. If there are no exemptions, a single rate, and full compliance, C-efficiency would be 1. In advanced economies, average C-efficiency has been flat over the last 20 years, at about 0.6 percent.

The inability of governments to tax the large informal sector means that the sector contributes relatively little to total tax collections. This is illustrated in Senegal, where despite accounting for more than half of GDP, it provides merely 3 percent of total tax. This has meant that the burden of rising tax-to-GDP ratio has fallen largely on the formal sector.

Poor public services and their impact on taxpayers. In all countries studied, the population is unclear about the benefits of paying taxes as services provided by the government are either of poor quality or nonexistent. Taxpayers see large and powerful players in the economy—be they individuals or corporations—not paying their share of taxes. They also continue to witness large-scale misappropriation of public funds by the rich and powerful, creating the perception that the government cannot be trusted with taxes. In Nigeria, police and security agencies regularly harass and intimidate tax payers.

Reluctance to adjust excise taxes. Excise revenues have either fallen in relation to GDP or remained stagnant. In Kenya, the government has faced pushback from vested interests whenever it places a proposal to raise taxes on cigarettes and alcohol on the table. Bangladesh has unusually low yield from excises, mainly because tobacco products with very high supplementary duty of about 400 percent pay only the VAT. In some countries, there is scope for raising petroleum taxes either through higher excise duties and/or through the imposition of the standard VAT. This will allow governments to charge for externalities that arise with consumption of petroleum products.

Opposition to property taxation. Property taxes in these countries continue to be opposed by groups with political influence (Bangladesh, Kenya, and Senegal). This is despite the fact that property prices have risen sharply in recent years and countries require resources to finance growing urbanization. Since the property tax is borne by the relatively wealthy, it is viewed as progressive. Even when property taxation exists in some form, property values are outdated and tax rates very low (Bangladesh) and exemptions for different classes of property owners are not uncommon (Kenya). Among other reasons behind inadequate revenue from property taxes are weaknesses in the cadastre system and inability of governments to value properties in thin markets. In Nigeria, the problem is compounded by dispersal of legislative authority to levy property taxes across the three levels of the government, federal, state and local.

Expenditure inefficiencies

Enhancing spending efficiency can free up as many resources as through increased mobilization of domestic revenues. Here we identify key inefficiencies in expenditure programs.

Government wage bill. In most countries, the government wage bill consumes a large portion of the revenue receipts, thereby crowding out higher priority outlays. Senegal’s wage bill accounts for 40 percent of domestic revenues, which is higher than that of countries with comparable GDP per capita. Zambia’s share of the wage bill in total outlays stands at 33 percent and remains one of the highest, relative to its peers in sub-Saharan Africa—it is even higher at 46 percent in relation to tax revenues. In Kenya, political considerations have been behind establishment of new government positions, particularly after the elections.

Spending inefficiencies. Although Senegal has one of the highest levels of education expenditures in the region, the average number of years of education is much lower than its comparators. This is in part due to the fact that the government apportions a large share of resources to wages at the expense of investment and pedagogical activities. In Zambia, the auditor general’s reports have frequently referred to irregular or overpayments, undelivered materials, and wasteful expenditures in government departments. In Nigeria, the quality of government spending has suffered from persistent delays in budget approval, erratic releases, weak procurement practices, and the influence of electoral cycles. Kenya loses about 1 percent of its GDP to corruption. Bangladesh suffers from poor quality of project implementation owing to inadequate supervision and corruption.

Most countries are undertaking large investment projects to reduce infrastructure gaps. In two countries (Kenya and Senegal), public investment increases as a share of GDP have been particularly sharp during the period under study. An IMF assessment found that Senegal’s public investment efficiency is lower than that in emerging markets. In Bangladesh, it is be believed that the mega projects are overpriced, contracted without open bidding, and awarded to unsolicited bidders.

Poor targeting. Countries are allocating resources to programs designed to enhance the well-being of disadvantaged segments of the population. Unfortunately, only a relatively small proportion of these expenditures are actually reaching the poorest. This is the case for agricultural subsidies and social assistance in Senegal. In Bangladesh, 40 percent of allocations for social safety net programs are misdirected, due to poor targeting and corruption in the selection of beneficiaries.

Towards a targeted policy package

The COVID-19 crisis provides an opening to low-income countries to chart a new policy course. There is scope for raising revenues and improving spending efficiency in the five countries examined. To a varying degree, this conclusion is applicable to all low-income countries. We believe that COVID-19 has reshaped the political and economic landscape. While COVID-19 presents major fiscal challenges for low-income countries as they seek to restore their tax bases affected by crisis-induced policy responses and changing structure of their economies, at the same time it presents opportunities to implement reforms previously opposed by vested interests.

In arriving at a policy package more readily acceptable to the population, governments should consider initiating a consultation process with various stakeholders in the country. This would help moderate the political opposition to reforms. In Kenya, the introduction of 16 percent VAT on petroleum products was initially rolled back following public boycott and civil strife in 2018, but subsequently approved by Parliament when the president negotiated with the main opposition leader and suggested a reduction of the tax to 8 percent.

Drawing on the foregoing discussion, governments should consider:

- Eliminating temporary tax cuts given under COVID-19 to help support incomes and demand. These tax cuts should not become permanent as they would reduce the effectiveness of the tax system to raise revenues over time (e.g., Kenya’s VAT rate cut, given also that other countries in the East African Community have a rate that is 4 percentage points higher at 18 percent).

- Announcing scrutiny of all tax concessions and instituting enhanced budget transparency. Since comprehensive estimates of tax expenditures are not readily obtainable for all countries, a beginning could be made with existing partial estimates. Governments must list all tax concessions and discuss them in the parliament in the context of the annual budget. In a similar vein, information on beneficiaries of tax concessions, including their regional distribution, should be published. These steps would not only increase revenues over time but also signal to the population that all taxpayers are equal. Furthermore, there should be enhanced transparency regarding the selection and implementation of public sector projects. Special attention should be paid to strengthening public investment management processes. To date, over 50 countries have obtained assistance from the IMF in response to COVID-19 and this number is expected to rise to over 80 in the coming weeks. One key condition for IMF assistance is that countries commit to a high level of transparency of spending (e.g., undertake to publish procurement contracts as well as greater auditing). Countries should leverage this requirement to embrace a more comprehensive approach noted earlier.

- Enhancing VAT productivity. The VAT exemptions and other concessions granted to appease different groups should be eliminated, including on petroleum products. Given the importance of food in the budget of a poor household, it would be appropriate to retain exemptions for a few food items. Improved compliance with the VAT law can potentially generate more revenue than other taxes, suggesting the critical importance of addressing weaknesses in its administration on a priority basis. The regressivity of the VAT would need to be addressed by progressive spending programs made possible by higher revenues.

- Adjusting excise taxes on tobacco (including rationalization of duties across cigarettes and bidis), alcohol and petroleum. This would not only generate additional revenues but also provide health benefits. Taxation of petroleum should reflect the cost of externalities associated with its consumption, including the impact on climate. As part of its COVID response, Nigeria has decided to do away with budgetary subsidies by adopting an automatic pricing formula. Excise increases should be coordinated with neighboring countries to avoid smuggling across borders and erosion of the tax base. To make this happen, requisite strengthening of administrative systems would also be needed.

- Committing to adopting a stable tax policy framework to facilitate private sector growth.

- Strengthening/implementing property taxes. Digitalization of land and property records and use of satellite technologies can help countries to secure the information required to implement the tax. The development of property taxes will take time, but it is important to start as soon as possible.

- Compensating government workers at levels that are competitive with the private sector. At the same time, the number of workers—particularly at lower-levels—should not be disproportionately high. Certain institutional changes, such as regular comparisons of government wages with the private sector would help in restraining growth in government wages over the short to medium term. Budgeting of the wage bill and workforce management should be centralized in the ministry of finance or another central agency.

- Conducting expenditure reviews of existing programs; governments can do this either on their own or with the assistance of international organizations. The results from such reviews should guide expenditure allocation decisions. Experience with COVID-19 has once again demonstrated the value of a properly functioning social safety nets to onboard, target, and pay population groups most affected by income losses. Digital technologies are helping in this regard.

We are grateful to Benedict Clements, Alan Gelb, and Mark Plant for very insightful comments on earlier versions of this piece.

For the appendix and supporting data, please see the full pdf.

Rights & Permissions

You may use and disseminate CGD’s publications under these conditions.