Recommended

CGD NOTE

Reconciling SME Production in China with Coronavirus Control

Since the coronavirus outbreak began in January, Chinese business activity has been severely slowed, affecting China’s position in the global industrial supply chain. The Enterprise Survey for Innovation and Entrepreneurship in China (ESIEC) launched a survey on the “condition of micro, small and medium-sized enterprises (SMEs) amidst the coronavirus outbreak.” Our surveyors then conducted follow-up interviews with a representative sample of private entrepreneurs from a database maintained over the past three years, asking about the resumption of production as well the different challenges enterprises face. Our findings include:

-

80 percent of surveyed firms had not resumed operations at the time of the survey, February 10, 2020, and 40 percent could not determine a timeframe for resumption;

-

20 percent of surveyed firms will be unable to last beyond a month on a cash flow basis, and 64 percent beyond three months, presenting a dire picture for SME bankruptcies under an extended epidemic scenario;

-

Barriers to business operations vary along the supply chain, with upstream firms mainly affected by labor shortages, while downstream firms face more serious challenges related to supply chains and consumer demand; and

-

Policies aimed at work resumption should consider the characteristics of each industry and avoid a one-size-fits-all approach.

This note is one of two that explore the impact of the coronavirus on SME production in China, drawing on ESIEC survey data and interviews. The second note considers whether SMEs can resume production without compromising epidemic control measures.

Survey Results

Based on our survey data, we found that the impacts experienced by upstream and downstream firms were not identical under coronavirus conditions, reflecting their different positions in the industrial supply chain. While enterprises downstream in the industrial chain directly provide goods to consumers, upstream enterprises provide intermediate goods required by those downstream actors. In general, upstream enterprises enjoy the advantage of economies of scale. They can also rely on the capital structure to form large enterprises. In contrast, downstream enterprises consist mostly of labor-intensive, micro, small, and medium-sized firms.

Upstream entrepreneurs hold different points of view regarding the impacts of the novel coronavirus outbreak. In short, they believe that the impacts of the outbreak will be relatively small in the long run. The biggest issue for them currently is labor shortages. In contrast, entrepreneurs in downstream industries face declining consumer demand as well as shortages of raw materials caused by disruptions in the supply chain. And as with upstream enterprises, they also are experiencing shortages in the supply of labor.

BOX 1. The ESIEC and Survey Methodology

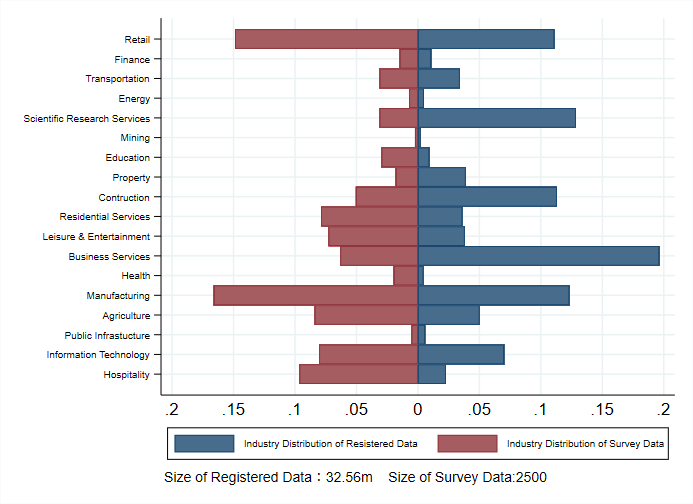

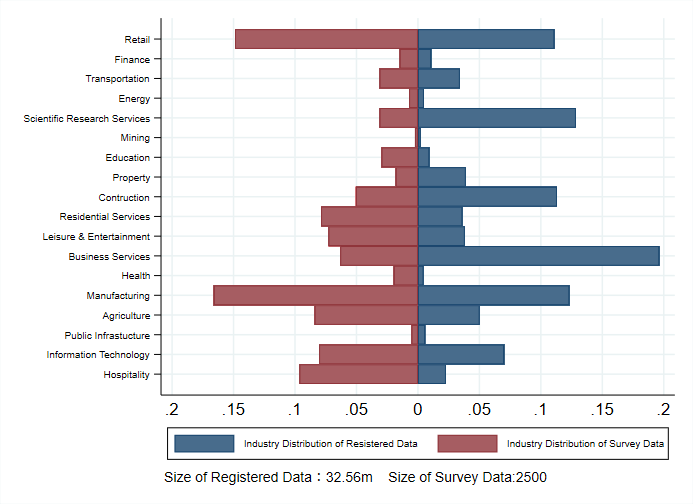

ESIEC is a field survey of Chinese private enterprises conducted by the Center for Enterprise Research of Peking University over three consecutive years (2017, 2018, and 2019). Based on a random sampling of enterprises with business registration, the survey previously interviewed nearly 10,000 new private enterprises in seven provinces from 2010 to 2017, collecting information such as start-up history and business operations. Following the coronavirus outbreak, the ESIEC Project Alliance (formed by Peking University, Central University of Finance and Economics, Harbin Institute of Technology – Shenzhen Campus, Guangdong University of Foreign Studies, and Shanghai University of International Business and Economics) conducted a special survey on the survival of small, medium, and micro enterprises under coronavirus conditions. A total of 2,668 samples were collected (including 2,459 samples with industrial information). As shown in Figure 1, the industry distribution of the collected samples is about the same as that of the total data. At the industry level, these samples are to reasonably representative of small, medium, and micro enterprises in China.

Figure 1. Industry Distribution of Survey and Total Data

Note: Authors' calculations based on survey and business registration data.

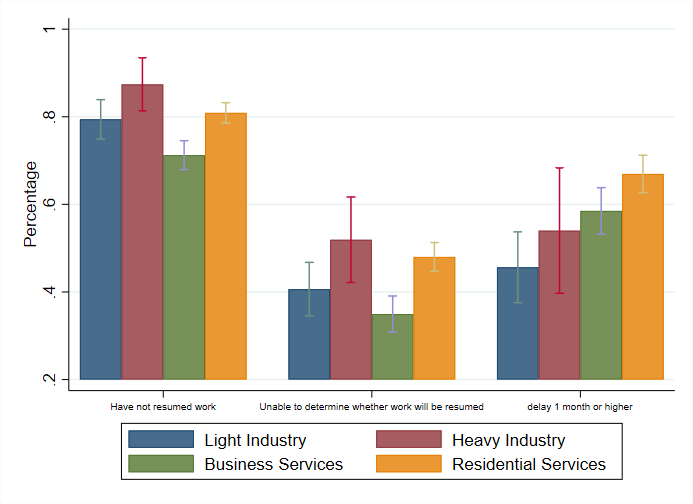

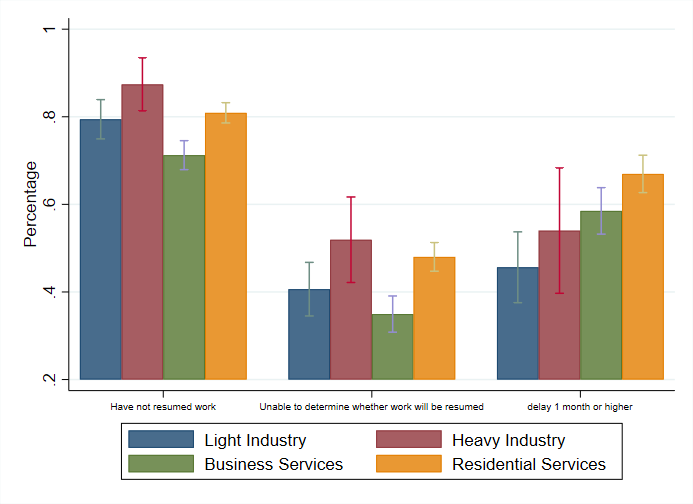

As shown in Figure 2, as of February 10, 2020, an average of 80 percent of enterprises still had not resumed operations, while the level of work resumption in business services was slightly higher at 30 percent. A possible reason for this difference is the fact that the operations of the business services sector can be conducted online, and industries such as IT, logistics, and scientific research have become the foundation of social operations following the outbreak. Meanwhile, the heavy industry and residential services sectors are the most pessimistic about work resumption. Among those that have yet to resume work, 40 percent currently cannot determine the timeframe for eventual resumption. Among those that can determine this timeframe, over 50 percent of entrepreneurs feel that they will not resume work within two weeks (that is, late February 2020). Overall, the work resumption outlook is grim.

Figure 2. Work Resumption Situation, by Sector

Note: Authors' calculations based on survey data. Vertical lines in the bar chart represent 95 percent confidence intervals. If vertical lines in a bar chart do not match one another, this means that the average values of the two groups differ at the 95 percent significance level.

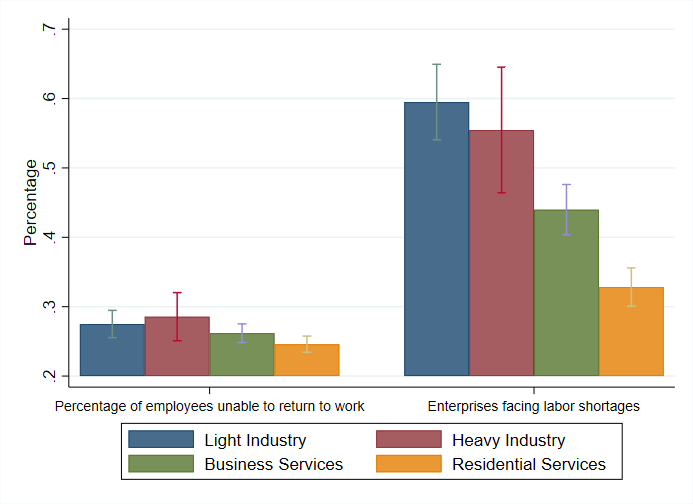

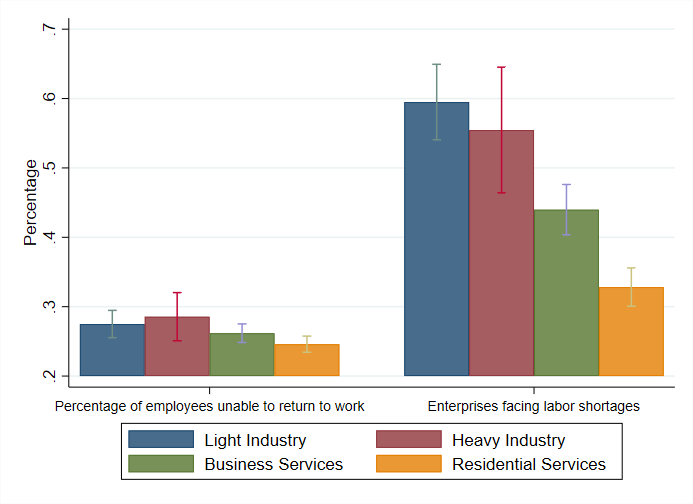

An important reason that enterprises cannot resume work is that employees are unable to return to work in a timely manner, a major impact. As shown in Figure 3, the percentage of employees unable to return to work in heavy industry enterprises is the highest, at nearly 30 percent. At the same time, among entrepreneurs in both light and heavy industries, concern over temporary labor shortages is at its highest, at 60 percent and 55 percent, respectively. Light industry is often labor-intensive and relies heavily on its workforce. It also has a high proportion of foreign workers. For these industries, the most severe issue is the current labor shortage. Although the residential services sector has been directly hit by the coronavirus outbreak, only 30 percent of entrepreneurs in this sector saw this shortage as an issue primarily because they are usually small or self-employed and feature a high proportion of local employees.

Figure 3. Labor Situation, by Sector

Note: Authors' calculations based on survey data. Vertical lines in the bar chart represent 95 percent confidence intervals. If vertical lines in a bar chart do not match one another, this means that the average values of the two groups differ at the 95 percent significance level.

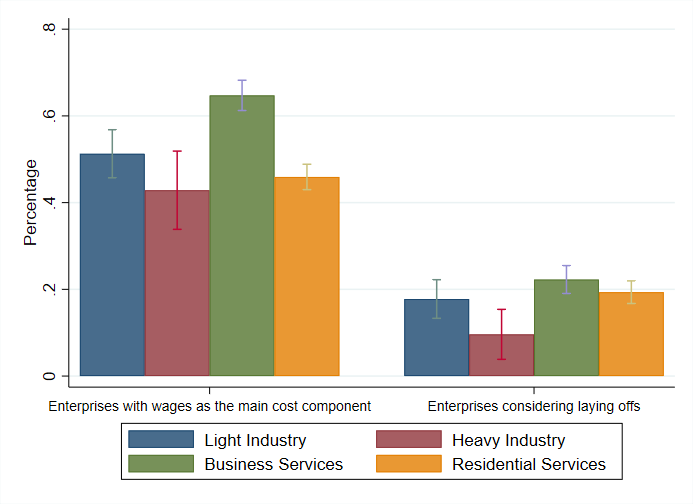

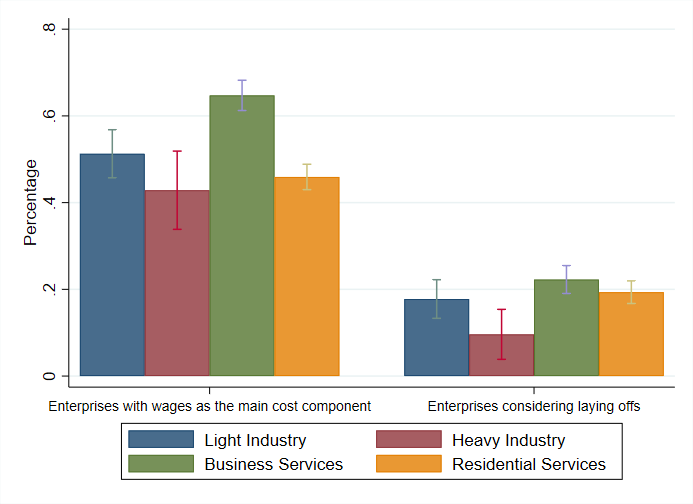

Under conditions of economic stagnation, enterprises’ inability to resume work poses a major challenge and places significant stress on their cash flow. As enterprises remain responsible for fixed costs such as wages, rents, and taxes, they have no choice but to declare bankruptcy once their cash flow is depleted. In the coronavirus context, 20 percent of enterprises will be unable to last beyond a month with their current cash flow, while 64 percent will be unable to last beyond three months. In terms of cost pressures, the most critical issue facing the business services and light industry sectors is wage costs. As shown in Figure 4, as wages in the business services sector are comparatively high, over 60 percent of enterprises in that sector believe that current wages are the biggest cost pressure. Meanwhile, over 20 percent of business services enterprises are considering laying off workers, with the light industry sector in second place. As most of these enterprises depend heavily on their labor force, wages are an important component of their costs. In contrast, wage pressure in the heavy industry and residential services sectors are more modest, at less than 50 percent each. The percentage of these enterprises considering laying off personnel is also relatively small.

Figure 4. Cost Pressures, by Sector

Note: Authors' calculations based on survey data. Vertical lines in the bar chart represent 95 percent confidence intervals. If vertical lines in a bar chart do not match one another, this means that the average values of the two groups differ at the 95 percent significance level.

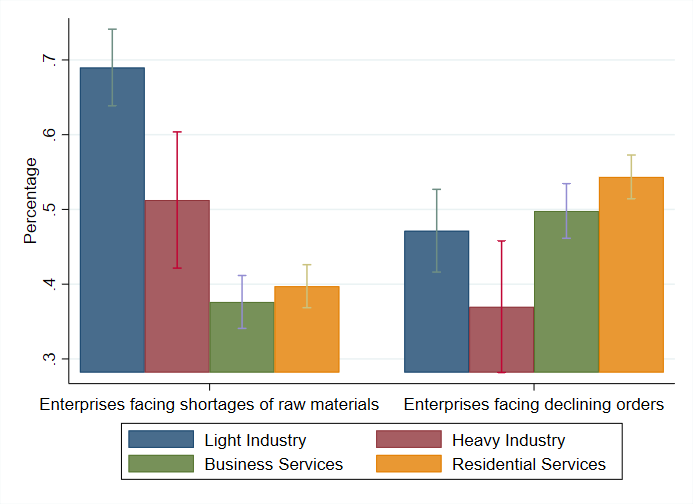

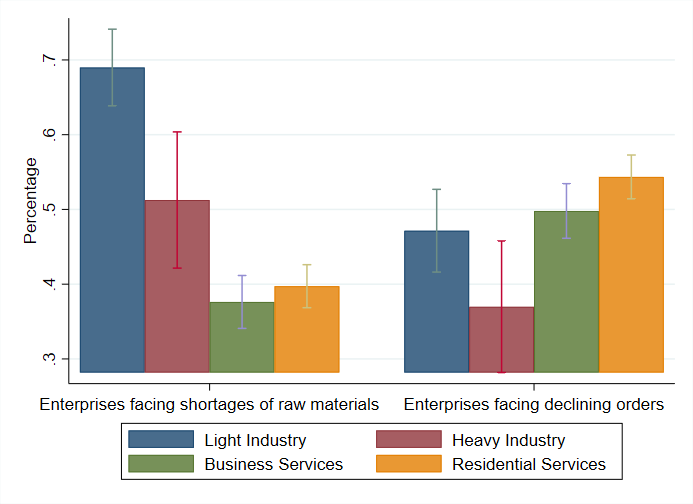

For enterprises engaged in economic activities that rely on both upstream raw materials and downstream demand, economic stagnation will be transmitted down the industrial chain. At the upstream end, the light industry sector currently faces the most severe issue of shortages of raw materials, with nearly 70 percent of enterprises in that sector pointing to that problem. In contrast, in the services sector, less than 40 percent of entrepreneurs face similar shortages. As shown in Figure 5, on the demand side, the light industry, business services, and residential services sectors have been directly hit by the outbreak, resulting in weak consumer demand, with over 50 percent of entrepreneurs citing declining orders. At the other end of the industrial chain, the heavy industry sector has been hit less hard because raw materials often originate from state-owned enterprises with large resources, and demand comes from orders from the light industry sector, which is currently operating in an urgent production resumption mode.

Figure 5. Upstream and Downstream Pressures in the Industrial Chain, by Sector

Note: Authors' calculations based on survey data. Vertical lines in the bar chart represent 95 percent confidence intervals. If vertical lines in a bar chart do not match one another, this means that the average values of the two groups differ at the 95 percent significance level.

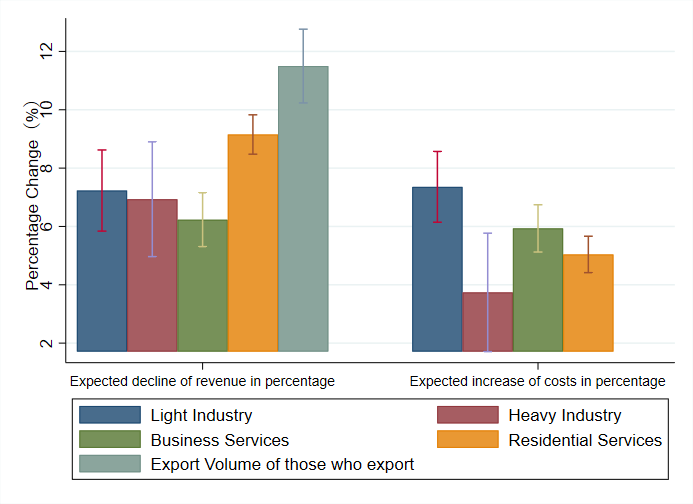

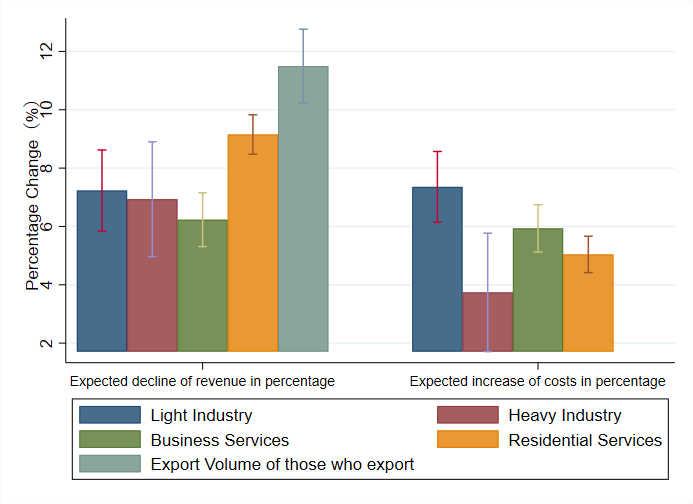

Are the repercussions of the outbreak for business operations short- or long-term? We surveyed a large number of entrepreneurs on their predictions for total revenues and costs for all of 2020 relative to 2019. As shown in Figure 6, residential services entrepreneurs believe that the heaviest impact will be on operating income, with an average predicted decline of over 8 percent, while the business services sector holds a somewhat more optimistic view for the longer term, with a predicted decline of no more than 6 percent. As regards raw materials, the light industry sector expresses concerns over rising costs and believes that the estimated cost of raw materials will soar by about 7 percent. Finally, it is worth noting that entrepreneurs involved in exports cite a more significant concern, predicting that the impact of the outbreak on their activities may surpass 10 percent.

Figure 6. Prediction of Medium- to Long-Term Impacts of Outbreak, by Sector

Note: Authors' calculations based on survey data. Vertical lines in the bar chart represent 95 percent confidence intervals. If vertical lines in a bar chart do not match one another, this means that the average values of the two groups differ at the 95 percent significance level.

Based on the data analysis presented above, we can deduce that the light industry sector faces the biggest challenges. Not only does it face disruptions in the industrial chain, but it has also been hit hard by shortages of raw materials as well as by soaring prices. In addition, it has had to deal with labor shortages. On the consumer demand side, orders have also been decreasing. In particular, for light industry enterprises involved in exports, the decline in orders arising from the epidemic surpasses 10 percent. Meanwhile, the main issue facing the heavy industry sector is the labor shortage. If the epidemic does not spread widely and employees are able to resume work following the outbreak, the impact on the heavy industry sector will be comparatively small. For their part, business services often have modern ways of operating their businesses, including the important role played by Internet Plus[1] in the context of coronavirus, which has raised demand for business services. If the cash flow of business services enterprises can be ascertained and wage costs such as social security contributions can be reduced, recovery could be relatively fast. Finally, the residential services sector will be directly affected by weak consumer demand as a majority of problems will originate as part of declining demand. As the residential services sector consists mostly of sole proprietors and small enterprises, the issue of labor shortage is not apparent. However, the issue of rents creates the main cost pressure.

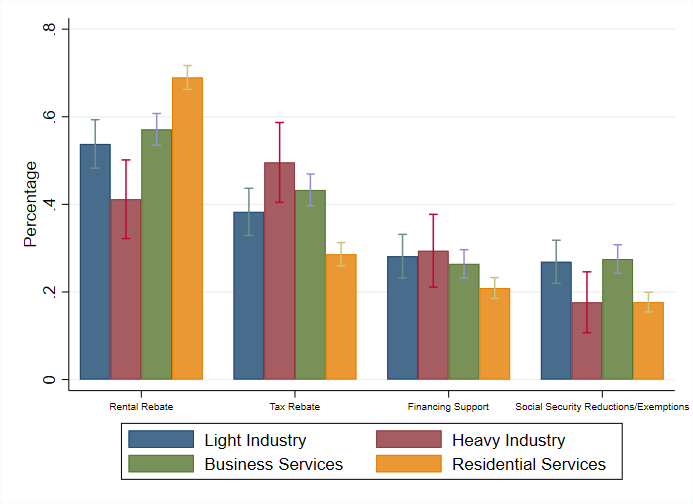

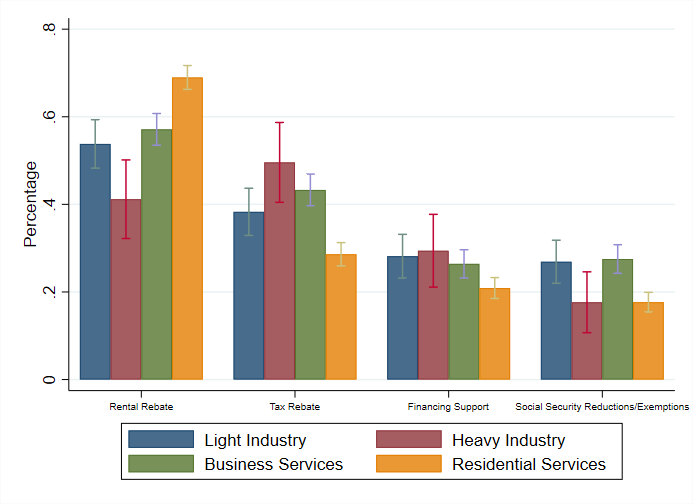

When we asked entrepreneurs to list the two supportive policies they think are most needed, it became apparent that the policies required by entrepreneurs differ in importance across sectors, and directly relate to the specific problems each faces. As shown in Figure 7, over 70 percent of enterprises in the residential services sector would require rental relief, while only 40 percent of entrepreneurs in the heavy industry sector believe that rent reductions would be effective. In fact, over 40 percent of heavy industry enterprises would prefer tax rebates instead. For these enterprises, a reduction in value-added tax (VAT) would be a more effective relief measure. For their part, enterprises in the light industry and business services sectors face increased wage pressure. Consequently, 30 percent of these entrepreneurs wish for a rebate in social security contributions to ease the cash flow pressure arising from wage costs. In comparison with asset-light sectors such as residential services, financing support is more important for heavy industry enterprises.

Figure 7. Support Policies Entrepreneurs Consider Most Effective, by Sector

Sector-specific recommendations

Given limited public resources, we recommend that the Chinese government assist enterprises in resuming work and production as soon as possible. Supportive policies should be tailored to the unique characteristics of each sector. For example:

-

The light industry sector is most in need of support, in particular those enterprises involved in exports. By introducing support for the full industrial chain, and rebates in social security contributions, the government can help enterprises to quickly resume operations.

-

To assist the heavy industry sector, the government should roll out region-specific epidemic control measures. Many medium- and large-sized heavy enterprises have their own dormitories. They should take responsibility for organizing production while keeping workers safe within their perimeters.

-

In the business services sector, as the long-term impact of the outbreak will likely be relatively small, the government should continue to provide medium- to long-term loans to avoid disrupting cash flows.

-

Although the residential services sector has been hit by the direct impact of weak demand, the need for government support should be relatively limited. Rent relief is identified by the residential services sector as the most important supportive policy.

Despite more than a dozen supportive policies unveiled by various ministries and commissions to help enterprises overcome the epidemic, most private entrepreneurs lack a clear understanding of these policies and have no idea how to make proper use of them. Supportive policies should take into account differences across sectors to be more relevant to their specific needs; they should also be more transparent if they are to deliver subsidies directly to the private entrepreneurs they aim to help overcome the crisis.

Rouchen Dai is at the Central University of Finance and Economics.

Junpeng Hu is at the National School of Development, Peking University.

Xiaobo Zhang is at the National School of Development, Peking University; IFPRI; and the Center for Global Development.

The Enterprise Survey for Innovation and Entrepreneurship in China (ESIEC) is a key project of the Institute of Social Science Surveys of Peking University. It is conducted by the Center for Enterprise Research of Peking University.

[1] Editor's note: This China-specific concept corresponds to the UN's Asia-Pacific Information Superhighway.

Topics

CITATION

Dai, Rouchen, Junpeng Hu, and Xiaobo Zhang. 2020. The Impact of Coronavirus on China’s SMEs: Findings from the Enterprise Survey for Innovation and Entrepreneurship in China. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}