Recommended

Blog Post

2025: A Crucial Year for Scaling Up Health Taxes

Blog Post

Why We Need to Hike Taxes on Alcohol, Tobacco, and Sugar

This note assesses how large tobacco, alcohol, and sugar-sweetened beverage (SSB) companies navigated the COVID-19 pandemic in terms of sales and profits, in order to provide evidence for raising health taxes on these products. As governments faced budget shortfalls, some considered or implemented increases in tobacco, alcohol, and SSB taxes to generate additional revenue (Lane 2021). Not surprisingly, producers pushed back, arguing that increased taxes would raise costs for consumers in an era of rising inflation, encourage illicit product consumption, and cut employment.

Chaloupka et al. (2021) found that tobacco companies did not experience a significant negative impact from the pandemic, with their financial performance indicators reaching or surpassing pre-pandemic levels in most cases. Therefore, there was no reason to hold back on tobacco taxes to reduce tobacco use and the resulting burden of tobacco-related diseases on strained health care systems during the pandemic. We update this work for tobacco and expand it to alcohol and SSB producers up to 2023, using Euromonitor data for 99 countries and financial reports for large tobacco, alcohol, and SSB firms listed in the United States

Key findings

-

The generally harmful impact of the pandemic on company profits did not apply to tobacco companies and was temporary for alcohol and SSB companies. Therefore, arguments for holding back on health taxes never applied in the tobacco sector and only applied temporarily for the alcoholic and SSB sectors.

-

For four large multinational tobacco companies, we confirm that sales revenues held up during the pandemic (US$106 billion in 2020 compared to US$104 billion in 2019), gross profit margins increased, and gross profits and net profits (adjusted for special factors) were maintained. We ascribe this result to tobacco companies’ strong control of pricing and relatively firm demand for tobacco products during the pandemic (i.e., inelastic demand).

-

For six large alcohol companies and seven large SSB companies, sales revenue and profit margins fell, as did gross and net profits during the pandemic in 2020, as demand declines from the hospitality sector were not fully offset by higher retail sales. These producers faced larger overall demand declines than tobacco producers. However, this decline was temporary with a more or less complete recovery during 2021 for SSB and alcohol producers (five large alcohol producers’ sales rose to US$122 billion compared to US$ 120 billion pre-pandemic and seven large SSB producers’ sales rose to US$208 billion compared to US$ 186 billion pre-pandemic). In general, alcohol and SSBs are more price sensitive than cigarettes. Alcohol and SSB companies have weaker pricing power than tobacco companies, and they sought to offset demand declines by reducing prices and profit margins.

Methods and sources

We use Euromonitor data for sales value and volume of cigarettes, alcohol, and SSBs. This covers 99 countries excluding small states and some low-income countries and can be viewed as a proxy for global sales trends in each product category. We use standardized brokerage reports (mainly from Standard & Poor’s) for the financial results of the largest tobacco, alcohol, and beverage companies that are traded in the United States, which covers companies that are listed on US stock exchanges including foreign companies shares that are traded via American Depositary Receipts (ADRs).[1]

Recent consumption and sales value trends

There are divergent consumption trends for tobacco, alcohol, and SSBs pre- and post-pandemic.[2] Total alcohol and SSB sales volumes were increasing moderately pre-pandemic.[3] However, cigarette sales volume exhibited a significant decline of 10 percent in the period 2014-19 with volumes only rising significantly in the Middle East and North Africa region. The sales decline is attributable, at least in part, to tobacco taxes and other tobacco control measures articulated in the WHO Framework Convention on Tobacco Control (Paraje et al. 2024).

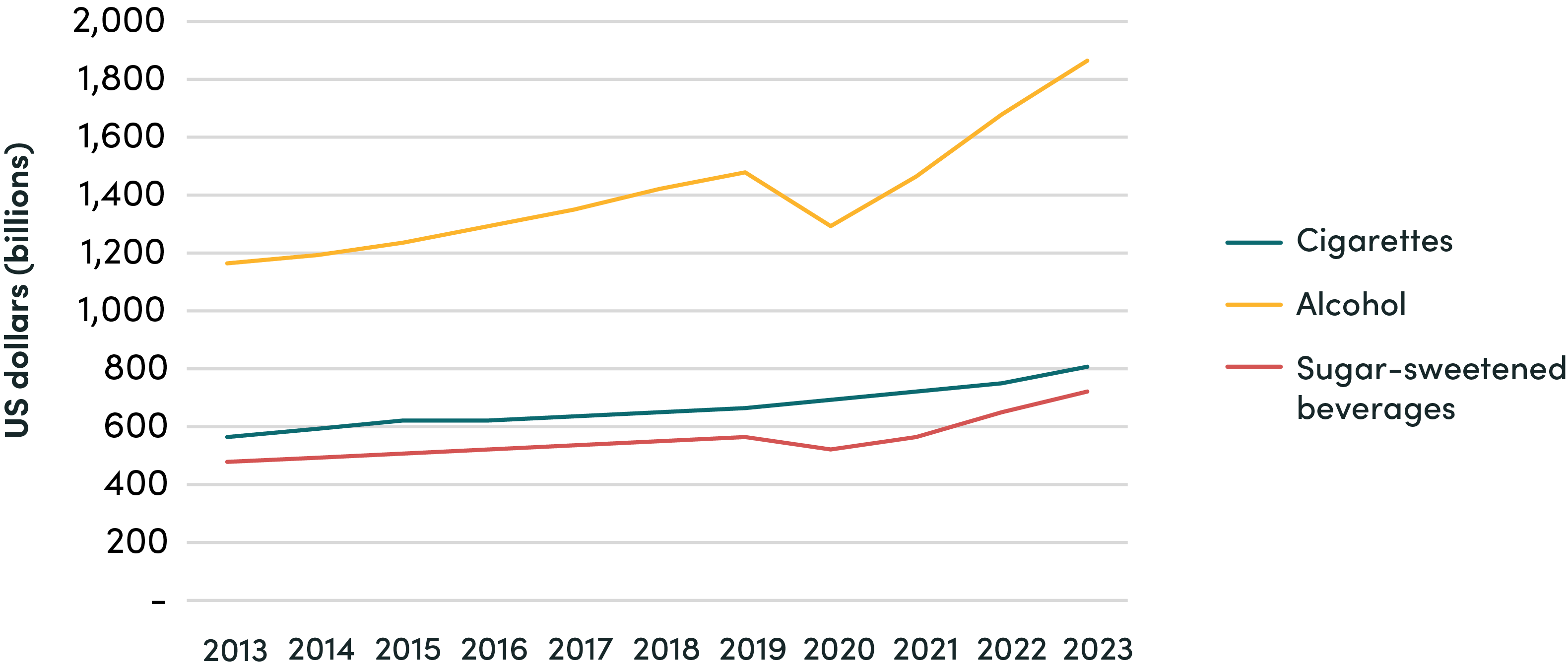

Restrictions related to the COVID-19 pandemic affected many health behaviors, including food and drink consumption (Kalbus et al. 2023). In the first full pandemic year, 2020, reported sales volumes for 99 countries surveyed by Euromonitor dropped for all three product categories. Sales volume of cigarettes dropped by 2 percent, alcohol by 7 percent, and SSBs by 6 percent according to Euromonitor data (Figure 1). By comparison, global real GDP dropped by nearly 3 percent (IMF World Economic Outlook Database) and personal consumption typically fell faster than GDP with personal savings rising (see here for US personal consumption data).

Figure 1. Global sales volumes cigarettes, alcoholic and sugar-sweetened beverages, 2013-23

Academic research broadly confirms these consumption trends. A systematic review of tobacco consumption studies during the pandemic found that the pattern of tobacco use decreased during the pandemic, i.e., most smokers decreased the number of cigarettes and e-cigarettes consumed from baseline (before the COVID-19 pandemic) to follow-up (during the COVID-19 pandemic) as a global health crisis provided a useful opportunity to quit or reduce smoking (Almeda and Gómez-Gómez 2022). For alcohol, the consumption picture is more complex: a systematic review of alcohol consumption studies indicated declines in 3 studies, increases in 7 studies and a mixed effect in 14 studies (Roberts et al. 2021). Another subtext is that alcohol “off sales” increased while sales in bars and restaurants fell. There is less systematic research on the effects of the pandemic on sugary beverage consumption: one study suggests that SSB consumption among youth in Korea fell (Park et al. 2023).

The larger volume declines for alcohol and SSBs than for cigarettes most likely reflect a proportionately greater impact from restrictions on social gatherings. A significant proportion of alcohol and SSB sales are consumed in social settings whereas cigarettes are primarily purchased for own consumption and not so closely linked to social settings. As restrictions were lifted on social gatherings in 2021 and 2022 sales volumes rebounded for alcohol and SSBs. Conversely, because cigarette consumption is not so closely linked to social gatherings, cigarette volumes remained essentially flat post-pandemic in 2021 and 2022. Nonetheless, cigarette sales volume did not resume their downward trend exhibited before the pandemic, although the reason for this outcome is unclear.

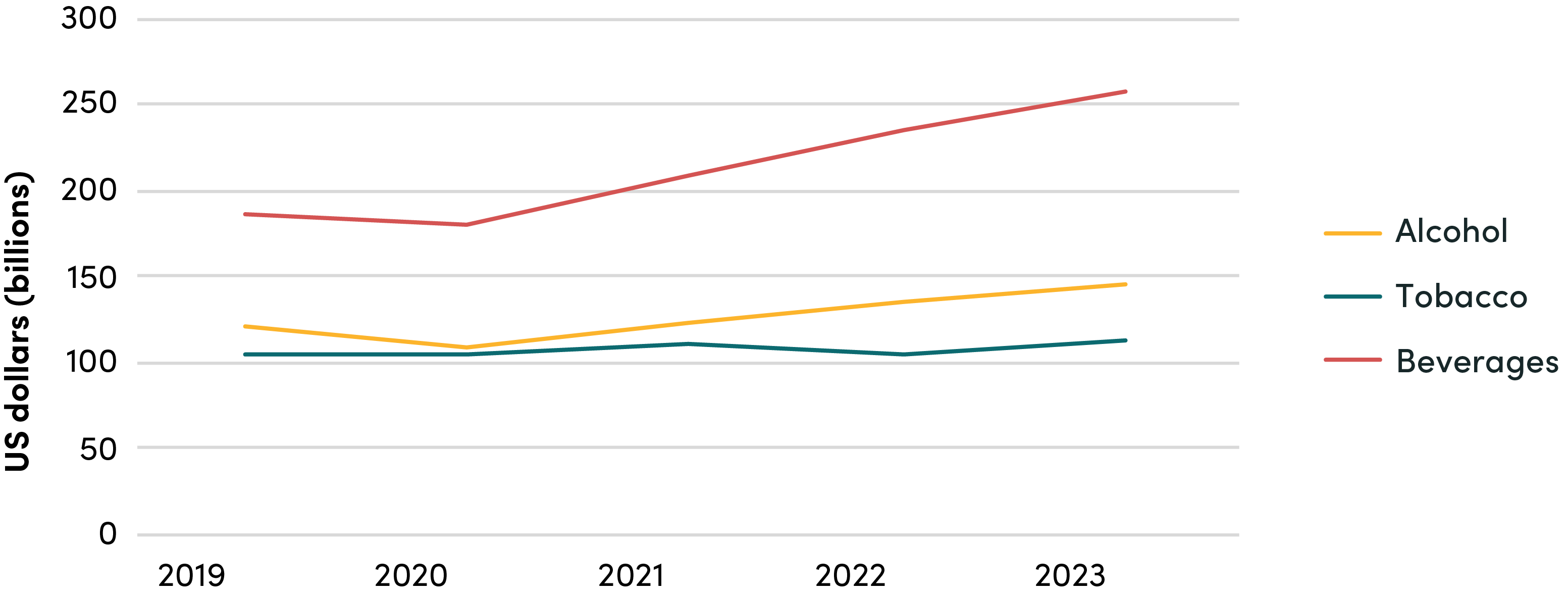

Retails sales values at the onset of the pandemic in 2020 increased for cigarettes but decreased for alcohol and SSBs, confirming the previous analysis for cigarettes (Chaloupka et al. 2021) (Figure 2). According to Euromonitor data, cigarette retail sales value increased by 3 percent in 2020 (suggesting a price increase of about 5 percent given a volume decline of 2 percent) so that essentially the cigarette sales value trends were unaffected by the pandemic (cigarette sales value increased by 2.8 percent in 2018 and 2.6 percent in 2019). However, alcohol sales value fell 12 percent and SSB sales value fell 9 percent in 2020. For alcohol and SSBs it appears that both prices and volumes decreased in 2020. Another factor that affects pricing policy is the sensitivity of demand to price. Cigarette sales are less sensitive to prices than alcohol and SSBs, so there is less incentive to cut prices to maintain sales volumes for cigarettes than for beverages.[4] Sales values for SSBs returned to 2019 levels in 2021 while sales values for alcohol also recovered to 2019 levels in 2021 indicating that the pandemic impacts were significant but temporary. Due to higher inflation, the sales value trend increased more rapidly post-pandemic than pre-pandemic for all three products.

Figure 2. Global sales value cigarettes, alcoholic and sugar-sweetened beverages, US$ billions current prices, 2013-23

Financial reports of tobacco, alcohol and SSB firms

An analysis of company financial reporting sheds light on the divergent trends for cigarettes and alcoholic and non-alcoholic beverages sales and profits during and after the pandemic. We focus on the 10 largest tobacco and beverage companies by market capitalization (obtained from https://companiesmarketcap.com) and then search for their standardized income statements by S&P for companies that are traded in US markets either because they are listed in the US or traded via American Depositary Receipts (ADRs). Of the top ten companies worldwide by market capitalization in each sector, four tobacco companies are traded in the US (including the top three: Philip Morris, Altria, and BAT), six of the top ten alcohol companies (including three of the top five: Inbev, Diageo and Heineken), and seven of the top ten beverage companies (including the top three: Pepsico, Coca Cola and Starbucks).[5]

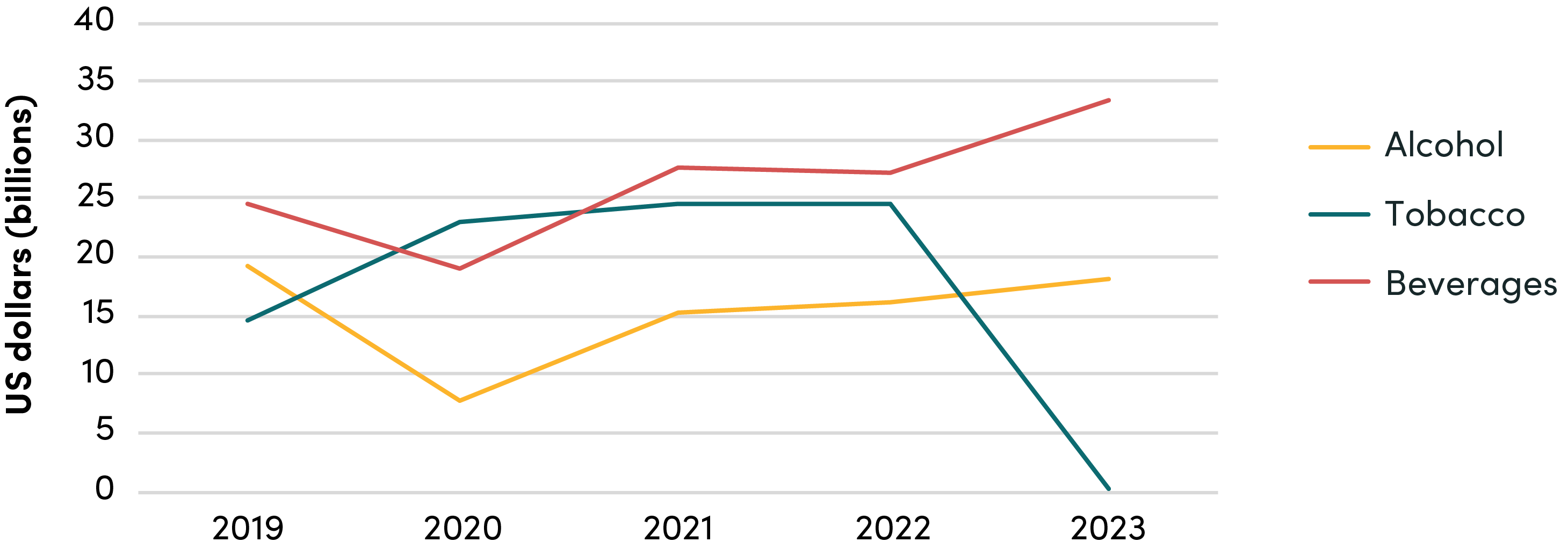

The aggregated income statements are consistent with Euromonitor data on revenues showing that alcohol and beverage revenues dipped in the first year of the pandemic while tobacco company revenues increased(Figure 3). They also show that alcohol and beverage revenues recovered after the first year of the pandemic while tobacco revenues appear flatter than in the Euromonitor data, perhaps reflecting that there were stronger increases in sales in companies traded outside the US, e.g., in India and China, that are not captured in US-traded companies results.

Figure 3. Big tobacco, big alcohol and big beverage company sales revenues, 2019-23

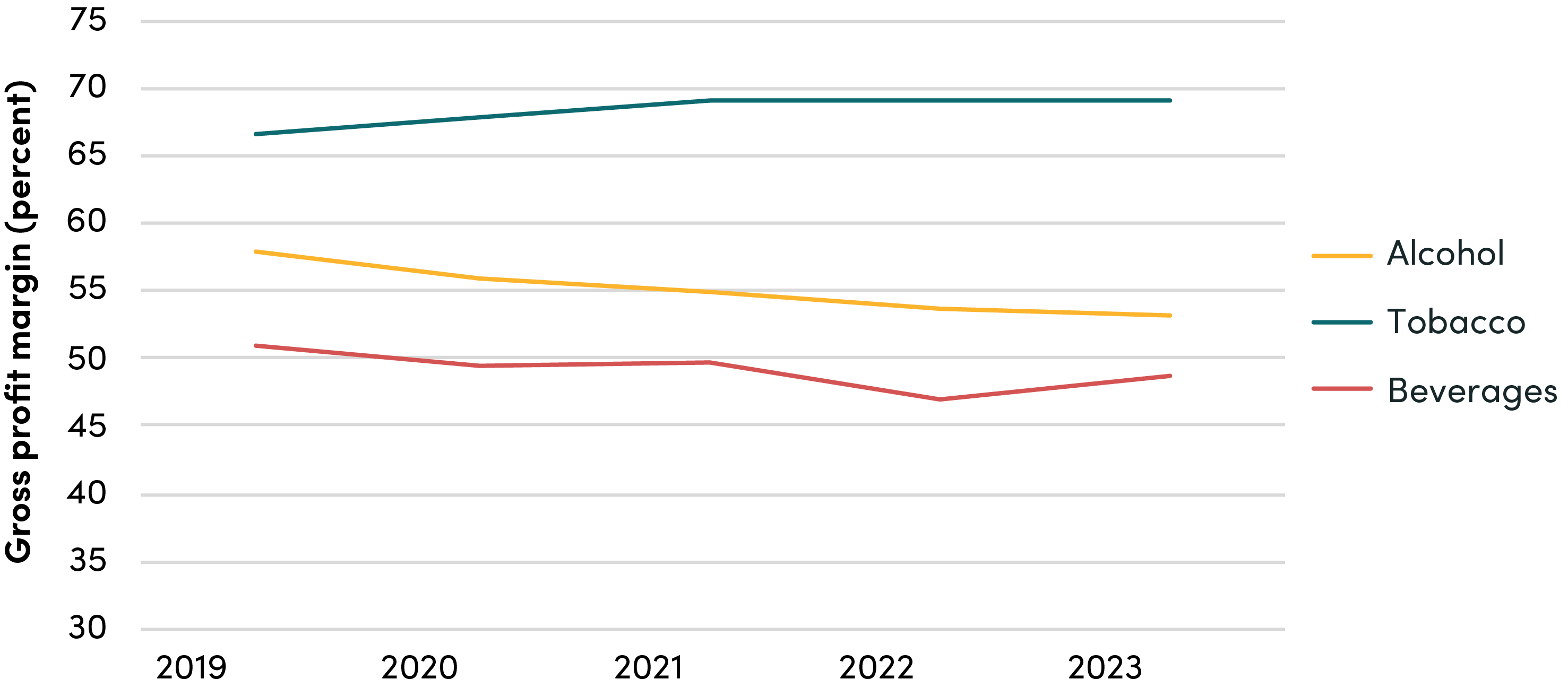

A second divergence observed between tobacco and beverage companies’ financial results is the behavior of gross margins (Figure 4). Gross margins (gross profit/ revenues) represent revenues less the cost of production before administrative and marketing expenses, depreciation, interest, and other charges (gross profit margins are typically in the 50 to 60 percent range). Tobacco companies were able to increase gross margins during the pandemic and maintain these higher margins post-pandemic. By contrast, alcohol and beverages gross margins fell during and after the pandemic, suggesting weaker pricing power. One likely explanation for this is that beverage companies faced a larger demand drop than cigarettes and tried to compensate by cutting prices, a strategy that would not work as well for cigarettes as demand is less sensitive to price.[6]

Figure 4. Big tobacco, big alcohol and big beverage gross profit margins, 2019-23

Note: Tobacco excludes BAT and Imperial Brands that do not report gross profits on a comparable basis.

Source: S&P Income Statements.

A final financial comparison is the performance of net income, which is gross profits less selling, general and administrative expenses, interest, depreciation, and special items (Figure 5). For alcohol and beverage companies, net income mirrors the behavior of gross income with a drop in the first year of the pandemic and a subsequent recovery, although faster in the case of beverage than alcohol producers. For tobacco companies, it appears that net income peaked during the pandemic years 2020-22. However, this performance is in part explainable by special factors that bring down net income in 2019 and 2023. In 2019, Altria wrote down the value of investments in JUUL (e-cigarette maker) by US$ 8.6 billion due to regulatory uncertainty. 2019 net income excluding this adjustment would have been very similar to net income in 2020, indicating that apart from special factors the pandemic did not affect tobacco profits. Similarly in 2023, a special downward adjustment of US$31.5 billion was made to the net income of British American Tobacco on account of the impairment of its 2017 acquisition of Reynolds, the then-second largest US tobacco company. As noted in a Reuters report of Dec 6, this write-down of goodwill on the balance sheet acknowledged that “its traditional market has no long-term future.”[7]

Adjusting net income for this accounting adjustment would have resulted in net incomes of the top 4 tobacco companies of 2023 of $31 billion compared to adjusted net income of US$ 23 billion in 2019 and in 2020.

Figure 5. Big tobacco, big alcohol and big beverage net income, 2019-23

Source: S&P Income Statements.

Sales volume data indicates that the COVID-19 pandemic did reduce the volume of consumption of cigarettes, alcoholic drinks, and SSBs in 2020, although tobacco was previously on a declining trend, whereas beverages were on a slight upward trend. These volume declines were temporary for alcohol and SSBs but were sustained for cigarette consumption at least through 2023.

For tobacco companies, sales revenues held up during the pandemic as any volume decrease was offset by price increases, gross profit margins increased, and gross profits and net profits were maintained during the pandemic (after adjusting for special factors). We ascribe this result to tobacco companies’ strong control of pricing relatively firm demand for tobacco products during the pandemic, i.e. inelastic demand.

For alcohol and SSBs, sales revenue and profit margins fell, as did gross and net profits during the pandemic in 2020, as demand declines from the hospitality sector were not fully offset by higher retail sales and they faced larger overall demand declines than tobacco producers. However, this decline was temporary with a more or less complete recovery during 2021 for SSB producers and by 2022 for alcohol producers. In general, alcohol and SSB markets have less sticky demand than cigarettes, and so alcohol and SSB companies have weaker pricing power than tobacco companies, and they sought to offset demand declines by reducing prices and profit margins.

Our results show that the impact of the pandemic on company profits did not apply to tobacco companies and was temporary for alcohol and SSB companies. Therefore, arguments for holding back on health taxes never applied in the tobacco sector and, at best, only applied temporarily for the alcoholic and sugar-sweetened beverage sectors.

With thanks for comments from Pete Baker and Katherine Klemperer, Center for Global Development, Jeff Drope, Johns Hopkins University, and an anonymous referee.

[1] American depositary receipts (ADRs) are negotiable certificates issued by a U.S. depositary bank representing a specified number of shares—usually one share—of a foreign company's stock. The ADR trades on U.S. stock markets as any domestic shares would (https://www.investopedia.com/terms/a/adr.asp).

[2] Euromonitor reports data from 99 countries and territories collected from national sources and producers.

[3] Alcohol volume in liters comprises of the sum of beer, cider/perry, ready to drink, wine and spirits, i.e., gross volume not net alcohol by volume. Disaggregated data on types of alcohol was not available. SSBs volume in liters comprises of the sum of carbonates, concentrates, juice, ready to drink tea and coffee, energy drinks, sports drinks and Asian specialty drinks.

[4] Cigarette price elasticity estimated to be between -0.2 and -0.6 (IARC 2011), alcohol price elasticity -0.5 (Nelson 2013), SSB price elasticity -1.3 (Cabrera Escobar et al. 2013).

[5] The companies’ financial reports used are for tobacco: Philip Morris, Altria, British American Tobacco, and Imperial Brands. Data was also available for Japan Tobacco except for 2023 and was therefore not included; For alcohol the companies used were: Inbev, Ambev, Diageo, Heineken, Forman, and Constellation Brands. For beverages: Pepsico, Coca Cola, Starbucks, Monster Beverage, Keurig Dr Pepper, Fomento Economico Mexicano and Coca Cola Europacific Partners. The details of the financial reports are shown in Annex 1 in the PDF version of this paper.

[6] Another possible explanation is that alcohol and beverage markets are more competitive than cigarette markets. However, sales data for the largest companies in each of these sectors suggests that they are each dominated by a few large companies. The top three companies share of sales from top ten companies is 53 percent for alcohol companies, 58 percent for tobacco companies, and 63 percent for SSB companies.

[7] “Goodwill” is added to a company balance sheet when it acquires another company for more than its market value.

Topics

CITATION

Lane, Chris. 2024. Navigating the Pandemic: Health Taxes and the Financial Performance of Large Tobacco, Alcohol, and Beverage Companies. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.