Recommended

The stakes are high for the African Development Fund (AfDF) as it kicks off its replenishment fundraising exercise this spring. Countries in sub-Saharan Africa (SSA) are still grappling with the health and economic fallout of the COVID-19 crisis, with over 30 million of their citizens pushed into poverty since the onset of pandemic. According to the IMF, an extra $425 billion in SSA government spending will be needed over 2021-2025 to make up for the lost ground in the fight against poverty. African countries are also strongly impacted by the war in Ukraine, including through higher food and energy prices. Ninety percent of East Africa’s wheat imports, for example, come from Russia and Ukraine. Debt dynamics in the region are increasingly precarious, with nearly half of sub-Saharan African countries in or at a high risk of debt distress. We anticipate increased volatility in capital flows to the region as global monetary conditions tighten. And accelerating climate change disproportionately threatens sub-Saharan Africa, a region that produces less than 3 percent of global emissions but is home to a third of the world’s droughts.

Proposal

Against this backdrop, the mission of AfDF—Africa’s only dedicated grant and concessional financing fund—remains profoundly relevant. But on the heels of last year’s landmark $93 billion IDA replenishment—and with the international community preoccupied with responding to Ukraine—AfDF must make a compelling case to donors for a large replenishment. Doing so will require the AfDF to articulate a plan to focus its resources on a core set of defining challenges and to offer a clear vision on how it can help fill critical finance gaps. We see the upcoming AfDF as having two broad purposes. First, it should combine its legacy of a strong focus on infrastructure and food security with a rapidly expanding role in climate adaptation and resilience through intersectional investments. Second, it should use its resources more catalytically to mobilize more private finance and expand fiscal space in the countries it serves.

To fulfill these twin objectives, we propose a replenishment of $10 billion, allocated over four areas:

-

Resilient, green, and inclusive infrastructure ($5 billion). Using the performance-based allocation (PBA) system, these resources would finance growth-promoting public and public-private infrastructure that is aligned with the African Development Bank’s (AfDB) climate change mitigation and adaptation objectives, that builds resilience to climate- and health-related shocks, that strengthens food security and agricultural supply chains, and that is specifically designed to reach and empower excluded populations, including women.

-

Regional integration ($2 billion). Resources would build on AfDF’s already strong track record in growth-enhancing cross-border projects through its regional window, using a top-up approach that incentivizes regional projects by adding to resources committed under the PBA system. Priorities would be infrastructure that creates efficient regional power and transport networks, helps implement the African Continental Free Trade Area (AfCFTA), and supports the region’s rich natural capital, including forests, arable land, biodiversity, and water sources.

-

Climate change adaptation and natural capital ($2 billion). Grants and concessional finance would focus on underfinanced areas of adaptation critical for highly vulnerable countries and for the poorest populations. The window would deploy a top-up approach to PBA resources to incentivize more adaptation and natural capital investments. A key priority would be projects in the agriculture sector to facilitate adaptation, especially by smallholder farmers, to new climate-driven realities through new production techniques, new products, and climate-resilient distribution systems. A second priority would be helping poor populations develop sustainable livelihoods from forests, fisheries and aquaculture, and tourism. And a third priority would be support for preservation of natural capital through environmental services payments to local populations. This window could be augmented and its impact scaled by an additional $1 billion co-financing vehicle pooling contributions from private foundations and philanthropic investors with shared objectives. The window and the co-financing vehicle would therefore generate a total of $3 billion in funds for these purposes.

-

Sustainable debt enhancement ($1 billion). Finance would be used to scale up the use of green and social policy-based guarantees (PBGs) to help countries reprofile their commercial debt, maintain or expand access to capital markets, capture greeniums (lower capital costs than for non-green borrowing), attract new investors, or incentivize private sector participation in debt restructurings. In addition to PBGs, resources would support capacity building in green and social debt management, green and social bond origination, building investor networks, and relevant policy and institutional reforms.

To track progress in these priorities, the AfDF should also strengthen its results measurement system in four critical ways:

- Build a more user-friendly, transparent online results and impact reporting system.

- Mainstream gender and climate in ex ante impact scoring and ex post results reporting.

- Deploy outcome payments more frequently in appropriate projects, shifting the focus in relevant operations from paying for inputs to paying for independently verified outputs and outcomes.

- Track and report mobilization of private finance for relevant projects and at the portfolio level.

Equipped with a renewed purpose, a discriminating focus, and an improved ability to measure its own impact, the AfDF can help shareholders keep African development issues high on the international agenda and efficiently deliver more resources essential for confronting the continent’s growing challenges. This would represent a near 30 percent increase over the last replenishment, which, as we argue below, is warranted both by the needs of the region and by institutional performance of AfDF.

This proposal is also profoundly relevant to African governments’ priorities and remains true to the demand-driven nature of the AfDF. According to a survey from ODI, infrastructure, energy, and agriculture, including food security, are top government priorities for multilateral development bank (MDB) investments in their countries.

What is AfDF and why does it matter?

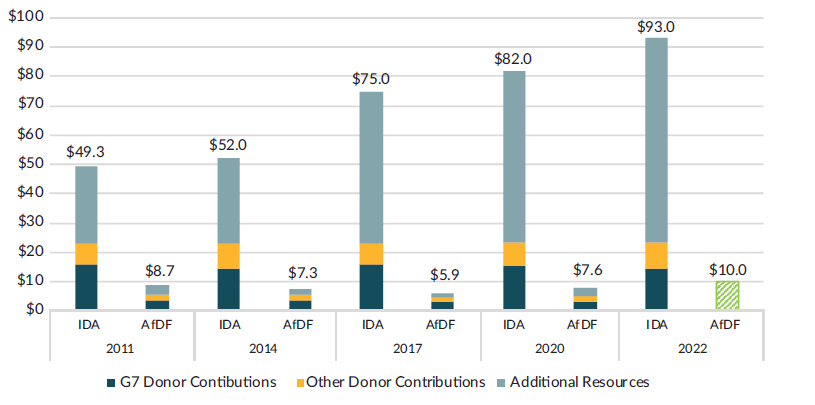

The AfDF is the African Development Bank’s (AfDB’s) concessional lending window for the world’s poorest countries. Like IDA, AfDF needs to be “replenished” by donors every three years because it provides grants and low-interest loans. But unlike IDA, which has seen exponential growth over the last decade, AfDF has remained broadly flat. In 2010, IDA was just over five times the size of AfDF. Today the IDA is more than 10 times as big.

Figure 1. IDA vs. ADF replenishment breakdown, 2010-2022 (USD billions)

Source: ADF, IDA, CGD staff calculations. https://ida.worldbank.org/en/replenishments/ida20-replenishment; https://adf.afdb.org/

Note: ADF replenishment figures do not include technical gaps listed in ADF replenishment reports.

Defining AfDF vis-à-vis IDA

The growing overlap between AfDF and IDA in terms of countries, structure, and sectors, and the divergence in their funding trajectories is striking. Approximately 70 percent of IDA’s financing goes to sub-Saharan Africa and just over half of its countries are in the region. [1] The two funds are also structurally similar. They allocate most of their resources through a performance-based allocation (PBA) mechanism and also have similar set-asides—special windows—that provide top-ups and incentives to finance specific projects. They both have a regional window that gives countries additional funding for cross-border projects (IDA also introduced a refugee sub-window in 2017), a private sector window, and different top-up mechanisms for fragile states. Finally, while their sectoral investments do show some divergence, the much bigger IDA out-finances AfDF across every single sector.

AfDF has in essence become a “mini” IDA, which makes it harder for donors to justify big jumps in contributions to AfDF. This is especially true because IDA can stretch its donor funding by virtue of its large reflows and ability to leverage its equity through market borrowing. Today, donor funding represents less than one-fifth of the total IDA replenishment compared to the AfDF, where donor contributions make up closer to 70 percent of the replenishment. For a donor, the bigger and more financially efficient IDA becomes, the more appealing a vehicle it is since it stretches grant contributions further.

AfDF should not resign itself to this state of affairs. Donors and management should instead use this replenishment to begin to carve out a separate lane for the AfDF and differentiate its offer—ideally in the context of a broader look at the MDB concessional system as a whole—to develop a more efficient division of labor between the institutions. This will require strong discipline on the part of shareholders who tend to push institutions in many different directions during replenishment negotiations. The key for the AfDF will be to focus on a few key areas of comparative advantage where it can meaningfully move the needle and leave the rest to IDA.

The case for a bigger AfDF

The case for a bigger AfDF replenishment must rest not only on the enormous need but also on the comparative advantage and track record of both the AfDF and the African Development Bank (AfDB) as a whole. The uphill battle the AfDB confronts in this replenishment negotiation in part stems from insufficient stakeholder knowledge of its strong performance in areas like public-private infrastructure finance, regional integration, performance-based allocation of resources, and recipient country ownership.

Need

Financing needs are only expanding in the wake of the pandemic and accelerating climate change. The continent labors under a triple burden: shortages of both public and private infrastructure finance, high carbon transition costs, and high climate change adaptation costs. McKinsey estimates that closing infrastructure finance gaps in Africa requires a doubling of annual investment to reach $150 billion by 2025. The IMF projects that SSA countries will need to spend about 20 percent of GDP on infrastructure by the end of the decade. Doings so in a sustainable way will raise costs. McKinsey’s analysis indicates that the cost of the net zero transition in SSA will be higher as a share of GDP than in Europe and the United States.

Countries in or near sovereign debt distress are numerous in Africa. The IMF now puts 20 African countries in this category. Public debt in SSA increased to almost 58 percent in 2020, the highest level in almost 20 years and a jump of 6 percentage points in one year. In 2020, interest payments reached 20 percent of tax revenue for the region. Market borrowing for many countries is either not available, unwise given their current debt service burden, or expensive and likely to get more so as global interest rates rise on the back of surging inflation. There are only two paths out of these tight public spending constraints (short of debt restructuring, which will be necessary in some cases): domestic resource mobilization (DRM) and concessional finance. Certainly, better DRM performance is needed, but the evidence suggests that realism is essential regarding the likely speed of progress, even in politically stable countries, and the limits on the effectiveness of external drivers of better DRM.

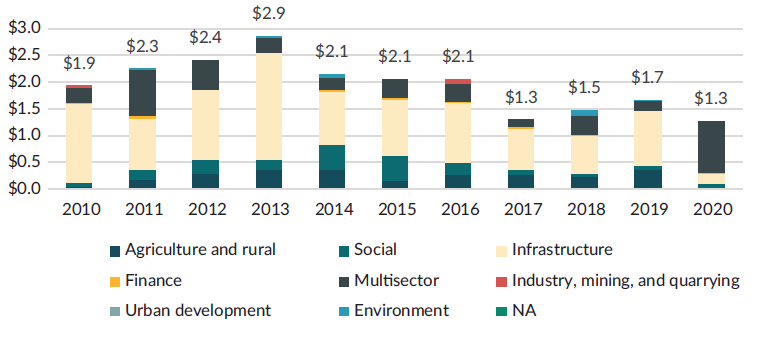

At a time when more concessional finance is clearly needed, we have seen a drop in AfDF funding during the pandemic, driven by its own financial constraints. In striking contrast to IDA, AfDF commitments fell 24 percent to $1.3 billion in 2020. Squeezed by intense budgetary pressures for social spending, the share of infrastructure in AfDF commitments dropped sharply to 12 percent in 2020, from an average of 57 percent during 2010-2019.[2]

Figure 2. AfDF sector breakdown, 2010-2020 (USD billions)

Source: AfDB annual reports, CGD staff calculations.

Private finance for SSA infrastructure has not come to the rescue, as some had hoped in the “billions to trillions” enthusiasm of 2015. Recent CGD research covering public-private infrastructure transactions in SSA from 2007-2020 found overall finance volumes stuck at around $10 billion for the whole region.[3] No upward trends were evident in the private finance component, in local private finance for infrastructure, and in finance from international institutional investors. The same was true of publicly funded institutions—bilateral and multilateral development finance institutions—charged with catalyzing private investment; their finance volumes also remained broadly flat. An expanded effort by AfDF, in concert with other parts of the AfDB, to use concessional resources to make more projects investible by the private sector is critical for changing this picture.

Performance

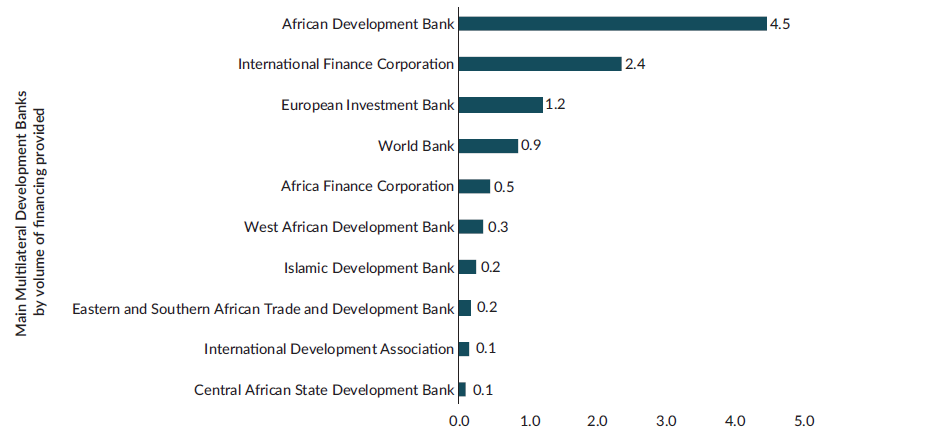

For the AfDB as a whole, its track record in public-private infrastructure compares well to that of its peer institutions. Infrastructure has been a core priority under both the Kaberuka and Adesina presidencies. Less well known is its role in public-private infrastructure transactions. The CGD study mentioned earlier ranked multilateral development banks by the cumulative contribution to public-private infrastructure transactions in SSA for 2007-2020.

Figure 3. Cumulative public-private infrastructure finance from multilateral development banks, 2007-2020

Source: IJ Global, CGD staff calculations.

The AfDB outspent other MDBs on public-private infrastructure in SSA by a wide margin. Many would have expected the much larger World Bank Group—IDA, IBRD, IFC—to rank higher. But the data show that the AfDB’s consistent focus on infrastructure has allowed it to punch above its weight.

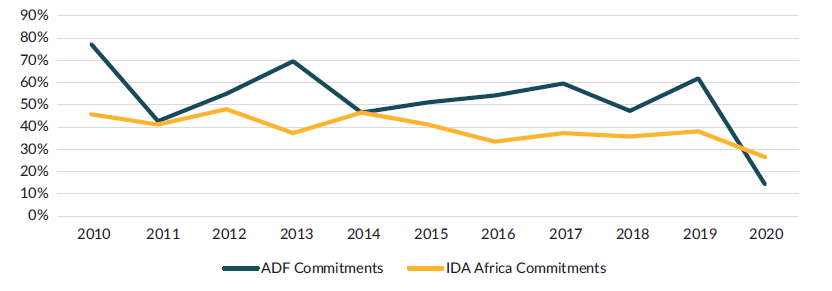

For AfDF specifically, if we compare the share of infrastructure in its commitments to that of IDA, we see that it has maintained a higher share, except for 2020, when infrastructure was crowded out by budget spending for current social needs.

Figure 4. Share of commitments going to infrastructure, AfDF vs. IDA, 2010-2020

Source: AfDB annual reports, CGD staff calculations.

While it is tempting to press AfDF to grow its share of commitments in the social sector, IDA has been dominant in this area (which counted for 33 percent, or nearly $26 billion of IDA commitments across 2018-2020) and we see merit in concentrating donor support for social finance in IDA and capitalizing on AfDF’s comparative advantage.

Moreover, as pointed out in research from ODI, AfDF is a leader in regional projects, critical for building more competitive economies in Africa.[4] For 2017-2019, an average of 18 percent of AfDF projects were regional projects, as compared to 0.5 percent for IDA. MDB models generally heavily favor country-specific programs and projects. The AfDF’s record in bringing countries together around regional infrastructure is highly significant in this context and especially important in meeting the challenge of boosting finance for global public goods.

Beyond infrastructure, the AfDF performs well according to the criteria identified in CGD’s QuODA rankings of aid effectiveness, ranking second among 49 bilateral and multilateral institutions. Notably, its strengths are prioritization and country ownership (over 80 percent of its borrowers report alignment with their own objectives) and its focus on the poorest countries.

This finding was corroborated in the latest Multilateral Organization Performance Assessment Network (MOPAN) report of the AfDB, which scored the institution’s organization architecture and financial framework “highly satisfactory” and highlighted the AfDF’s performance-based allocation (PBA) framework in particular. The AfDF also scores well on QuODA’s predictability and reliability metric, with the bulk of its official development assistance (ODA) received by partners in a timely manner. Performance in this regard makes the institution easier to work with, and allows governments to manage their resources better, use ODA for longer-term initiatives, and keep their citizens better informed about the progress of development projects.

And the AfDB has clearly demonstrated its leadership in climate finance. The share of climate finance in its operations in 2020 was 33 percent, the highest of any of the major MDBs, including the World Bank.

The role of AfDF in expanding public-private infrastructure finance

The AfDF can combine its concessional tools with those of other parts of the AfDB for greater development and mobilization impact in AfDF-eligible countries. It can:

-

add concessional finance to fiscal space for infrastructure, either for fully public projects or for public-private projects;

-

support project development, planning and project selection capacity, project management capabilities, and policy and institutional reforms that increase project productivity and make more projects bankable;

-

help finance the subsidies frequently needed in public-private infrastructure transactions to crowd in private participation or increase development impact, such as results payments for extending affordable infrastructure access to poorer populations; and

-

expand on the Private Sector Credit Enhancement Facility (PSF) model to take risk off the AfDB balance sheet, including through first-loss and other kinds of instruments to share risk, including currency risk, to enable more AfDB lending to private entities in AfDF-eligible countries. Donors could offer additional, complementary guarantees that enhance AfDB’s capacity to take on risk.

The potential for crowding in more commercial private finance in SSA is realistic and significant. The IMF estimates that the private sector could provide additional financing of 3 percent of GDP for infrastructure in SSA by 2030, representing about $50 billion per year.

IMF analysts point out that 95 percent of infrastructure finance in SSA currently comes from the public sector, more than in most other regions. It would be efficient to use part of that public finance to mobilize more private participation. In East Asia, for example, 90 percent of infrastructure projects with private participation receives government support, compared to 50 percent in SSA.

As part of the replenishment package, donors and management could establish a target for mobilization of private finance in public-private infrastructure transactions. Our proposal is that the target be set at $1.5 of private finance mobilized for every AfDF dollar committed to AfDB private transactions.

While this may seem like a relatively modest target, it is in line with results we have seen so far in other institutions. As a reasonable comparator, we can look at the track record of the IDA Private Sector Window (PSW), which was established in 2018 for the same purpose: to use concessional resources to take on part of the risk of IFC’s transactions in IDA-eligible countries. (In this case, it would be AfDB’s private finance transactions.)

The World Bank’s Independent Evaluation Group (IEG) recently assessed the performance of the IDA PSW, including whether it expanded IFC’s operations in IDA-eligible countries and how much private finance was mobilized by those operations. Through 2020, the IEG reported that the volume of private finance mobilized totaled $1.4 per dollar of IDA PSW concessional finance.

These are early results, as IFC’s push into poorer countries through investments in upstream pipeline development was at an early stage during the evaluation period. AfDF can use the PSW experience to move rapidly up the learning curve. And AfDF donors, who are also IDA donors, can push for more collaboration between IDA/IFC and AfDF to capture cost efficiencies through jointly developing and sharing pipeline.

Major institutional changes will be needed to help AfDF achieve its catalytic potential. As noted in the AfDB private sector strategy document, reforms are needed to improve synergies between sovereign and private operations, strengthen internal coordination on private sector development activities, allocate headroom in ways that are not biased against private sector operations, and increase risk appetite for private operations in transition countries.[5] The replenishment negotiations are the best time to embed these changes firmly in AfDB operations as a condition of generous donor replenishment pledges.

The AfDF can also take advantage of relevant experience in designing platforms that facilitate public-private infrastructure development suited to poor countries. The IFC’s Scaling Solar platform, for example, deploys a one-stop shop, standardized bidding process for solar generation investments that introduces some welcome elements of competition in access to finance and subsidies.

AfDF also has a clear opportunity for greater mobilization through partnerships with the bilateral and multilateral DFIs that are interested in increasing their activity in poor countries and in meeting ambitious zero emissions targets but struggle to expand project pipelines in Africa. The US Development Finance Corporation is one. The DFC aims to achieve a net zero emissions portfolio by 2040 and has a congressional mandate to focus operations in low-income and lower-middle-income countries. But the DFC has staff constraints generally, minimal on-the-ground presence in Africa, and very little concessional/project development finance. The AfDF’s strengths therefore complement the DFC’s ability to bring large scale finance to the commercial side of public-private transactions.

Climate adaptation and food security: intertwined challenges

Climate change mitigation often dominates the conversation, but for sub-Saharan Africa, climate change adaptation is equally salient. The AfDB’s own work suggests that the continent needs $7-$15 billion a year in adaptation finance. The institution has already committed to allocate over 40 percent of its projects to climate finance, evenly split between climate mitigation and adaptation.

Adaptation issues are also closely linked to food security—a key challenge facing the continent that has been exacerbated by global supply chain disruptions and the invasion of Ukraine. The SSA region has long been among the most vulnerable to climate-change-related food insecurity. The disruption of the Ukrainian harvest and sanctions of Russian exports have caused already rising prices to skyrocket, which will worsen food insecurity, even for SSA countries that do not directly import from those countries. As a result of these factors and others, the portion of Africa’s population that is malnourished is expected to grow, from 282 million today to 350 million by 2050.

These risks make the economic case for adaptation in the region especially strong. It is also a form of prevention finance: $15 billion a year in adaptation finance could save an estimated $200 billion down the line. Put another way, adaptation is among the most cost-efficient investments the AfDF can make. And given the prevalence of smallholder farming, adaptation programs have strong co-benefits, simultaneously reducing the risk of food insecurity and safeguarding livelihoods, both of which are already areas of special emphasis for the AfDB group. As experts have pointed out, climate adaptation and development are not in tension with one another but are mutually enforcing and should be pursued concurrently.

The measures that fall under adaptation are diverse and overlapping. Investing in emerging crop technologies, disaster warning systems, and insurance products can help farmers to adapt their production to a changing climate. Water security is a key part of the adaptation agenda, with irrigation only covering 7 percent of the region’s cultivated areas. Investments in cold storage and grain storage can reduce the 36 percent of African agricultural yields currently lost to spoilage. On more traditional infrastructure projects, spending an additional 3 percent in upfront costs on resiliency measures can provide returns of up to four times the initial investment by avoiding additional rebuilding and maintenance costs.

Conserving natural capital and biodiversity can be accomplished in ways that protect and create income generation opportunities for vulnerable local populations. For example, preserving mangroves, wetlands, floodplains, and river basins can strengthen biodiversity, improve water conservation management, build sustainable food production, fishing, and tourism livelihoods, and protect urban and agricultural areas from flooding. AfDF’s concessional resources are essential for supporting payments to local populations for environmental services to preserve natural capital, as well as for sharing the risk of AfDB private investments in local firms, farms, and fisheries. The Congo Basin, home to the world’s second largest rainforest and enormous peat reserves that trap carbon, is a prime example of a place where multiple adaptation, conservation, and poverty reduction efforts intersect and should be an explicit priority for the AfDF.

Adding philanthropic co-financing to the climate adaptation and natural capital window

The goal of scale and mobilization can be advanced further by creating a co-financing vehicle for philanthropic funders that share an interest in climate-focused investments in Africa to invest alongside governments in the climate adaptation window. This would be an opportunity to engage private funders that don’t fit into the standard categories of grant-makers or commercial investors.

Foundations and philanthropic investors are increasingly focused on combining their social and poverty reduction objectives with their climate objectives, but they lack an independent capacity to build robust green and resilient project pipelines in Africa. They would benefit from joint activities with a partner with strong relations with local governments and the ability to support policy and institutional reforms that are often essential for viable green public-private infrastructure investment. The co-financing vehicle would also facilitate coordination among philanthropic investors and help them achieve greater scale and synergies through collective action and finance.

The private philanthropic funds in the co-financing vehicle would be additional to the funds provided by donor governments to the adaptation window. Clear parameters would have to be agreed on the scope and nature of relevant projects to ensure that public and private donors’ objectives are aligned. The private funds would augment finance available for AfDF projects, make larger investments possible, and increase adaptation benefits.

The co-financing vehicle could have a longer time horizon than the three-year replenishment cycle. A notional fundraising target for the co-financing vehicle could be $1 billion, so that every donor dollar in the $2 billion AfDF adaptation window could potentially be matched by $0.50 of private philanthropic funds. Depending on private funder preferences, a financial goal could be established for their funding that is different from that of public donors; the goal could, for example, target below-market returns or simple preservation of their capital.

Governance of the co-financing vehicle would be separate from the AfDF governance of the climate adaptation window. The co-financing vehicle would have independent decision-making authority over its own resources. Projects would be proposed by the climate adaptation window, and decisions about funding from the co-financing vehicle would be made by its own governance structure. This would avoid an upfront obligation to invest in every climate adaptation window project or in some part of the window’s portfolio: such a passive investing role may not be acceptable to private funders. A model might be the new ILX Fund, under which a Dutch pension fund will decide on a transaction-by-transaction basis whether to co-finance SDG projects proposed by a number of MDBs.

Guarantees: more catalytic than sovereign lending

Policy-based guarantees (PBGs) offer the AfDF the opportunity to simultaneously expand the amount of financing available to its clients, improve financial terms, and increase the leverage of its own balance sheet. By substituting an MDB’s risk rating for the sovereign rating on a portion of a sovereign loan or bond issuance, PBGs can achieve lower interest rates and longer maturities than would be achievable if sovereigns were to borrow on a standalone basis.

Forthcoming CGD research on PBGs finds that since 2008, each dollar of PBGs has mobilized on average approximately $1.8 in commercial financing, expanding the amount of fiscal space available to sovereigns and its sources of external financing. [6] MDB guarantees are particularly catalytic because they are partial and only generally cover 40-80 percent of the loan. For example, $50 million of “insurance” to a creditor for a $90 loan is enough to improve the rate and maturity of the loan to the point that the transaction is appealing to both the creditor and the sovereign. As a result, $1 of guarantee has mobilized $1.8 of private sector financing. But the financial tradeoff is even more appealing in the concessional windows, where only a quarter of every dollar of guarantees currently counts against a country’s regular resource envelope. AfDF could go a step further and book guarantees on a 1:5 basis. Under this scenario PBGs could potentially generate nine times the amount of financing of a traditional loan while consuming the same amount of a country’s PBA.[7]

This instrument could be particularly valuable for sovereigns seeking to reprofile or rollover existing commercial debt on cheaper terms. It could also be used in the context of restructurings to entice private sector participation. The AfDB Group has experience with the instrument—it successfully employed a PBG in the Seychelles to entice private creditors’ participation in restructuring negotiations, and the AfDF itself issued a guarantee as part of a financing package to Madagascar in 2016. Recent research from S&P found evidence of a greenium on green bonds of between 1 and 10 bps globally, as well as more frequent trading and lower bid/ask spreads, with the effect particularly strong for dollar-denominated debt. As more investors enter this space, analysts expect that greenium to increase.

PBG policy conditionality

The policy conditionality included in PBGs should advance a pro-climate or social set of policy measures. While historically the bulk of MDB PBGs have featured traditional macroeconomic conditionality, the AfDF could condition its PBGs on implementing policies that support climate adaptation, emissions mitigation, natural capital conservation, or gains in equity/inclusion, ensuring green or social benefits from the debt issuance. Examples of such conditionality can be found in a recently approved Inter-American Development Bank PBG, which includes ex ante policy reforms such as promoting better management of marine resources, upgrading building codes to reduce climate risk in coastal and offshore areas, and improving the business climate for micro, small, and medium enterprises operating in the blue economy. Even prior PBGs that were not branded as environmental, social, and governance (ESG) related have included ESG conditions—for example, nearly half of the policy reforms specified in the latest IBRD PBG to Ukraine were environmental or social-related, such as shifting health care financing from curative to preventative care and implementing an agricultural land governance monitoring system. Specifying far-reaching policy conditions like these upfront goes beyond the impact of any one green or social project by directly integrating adaptation, social protection, and other AfDF-aligned priorities into government programs.

Conclusion

In these “dangerous times,” Africa and its international partners must be able to deploy all the tools in their arsenal to confront mounting risks. One of the most critical tools at Africa’s disposal is concessional finance from a regional bank with a track record in some of the most important areas for the region. The task for AfDF donors and regional recipients is to use this replenishment to empower the fund to target critical finance gaps—both public and private—that impede progress on climate vulnerability, food security, and poverty reduction and inclusion. But size is critical as well as a focused mandate. The AfDF cannot play a meaningful role if donors neglect it in favor of IDA. Nor can IDA be all things to all poor countries. This replenishment is an opportunity for donors to restore and strengthen AfDF’s role and relevance. It would be hard to imagine a time and circumstances when there would be a more compelling case to do so.

[1]As of CY2021.

[2][2] AfDB annual reports.

[3]Includes only projects that reached financial closure;

[4] Regional defined as multi-country;

[5] AfDB, not yet publicly available.

[6] CGD staff calculations, not yet publicly available.

[7] The 1:5 PBA ratio multiplied by the average 1.8 mobilization level.

Topics

CITATION

Lee, Nancy, Clemence Landers, and Rakan Aboneaaj. 2022. Replenishing Africa’s Development Fund: A Time for Ambition. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.