Recommended

Over the past 18 months, the IMF’s newly established Resilience and Sustainability Facility (RSF) has swiftly moved from initial set-up to providing financing to countries. The facility, which is the operational arm of the Resilience and Sustainability Trust (RST), is designed to support the climate transition and pandemic preparedness. Since its inception in late 2022, the IMF Board has approved 17 programs, with the 18th involving Côte d’Ivoire currently at the staff-level-agreement stage. Previous CGD analyses (see here, here, and here) have critiqued the initial programs for their lack of ambition in reform measures. In response, in November 2023, the IMF issued new guidance on RSF programs.

What impact did that updated IMF guidance have? While there’s evident progress in the robustness of reform measures, we find that they still fall short compared to those in programs supported by the Poverty Reduction and Growth Trust, the IMF’s other major trust fund. Additionally, the countries that have taken up RSF programs are not the ones the most urgently in need of climate finance, raising questions on what would enhance RSF’s appeal to countries most in need. Moreover, the fungibility in budget allocation poses significant challenges in monitoring whether incremental spending on climate transition is indeed occurring.

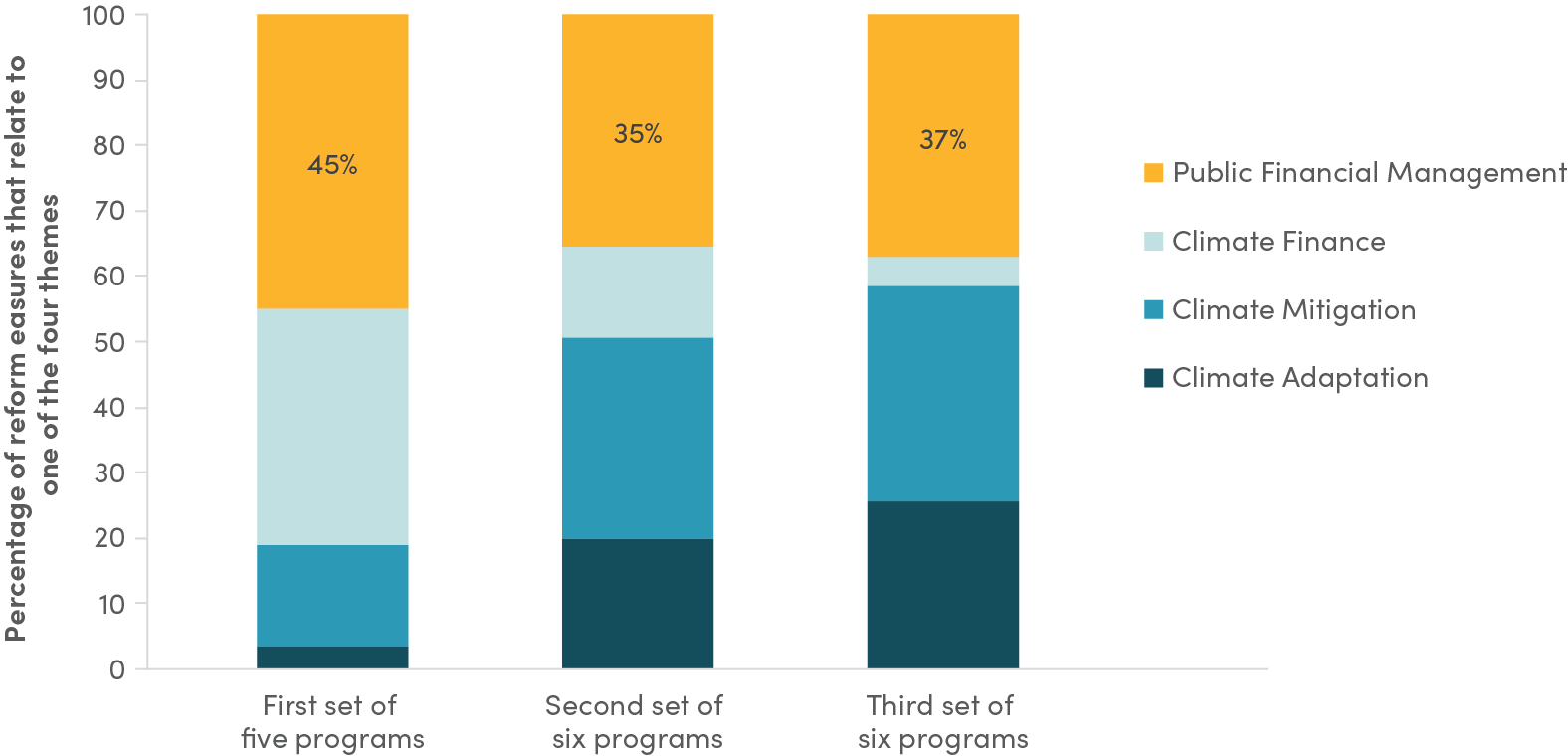

Below, we categorize the 17 Board-approved RSF programs into three groups: the first five that were approved by February 2023, the following six approved prior to October 2023, and the remaining six approved thereafter. This segmentation aims to capture the impact of the new November 2023 guidance on the latter group.

We find that there is a noticeable shift towards prioritizing climate adaptation measures in recent programs. While the median number of measures in RSF programs remains stable at 12, there has been a notable increase in the proportion of measures specifically targeting climate adaptation, with a decline in those focusing on climate finance (see Figure 1). Additionally, reform measures using Public Financial Management principles, broadly defined, continue to hold precedence, underscoring the pivotal role of efficient public spending in facilitating successful climate transition initiatives.

Figure 1. Theme of reform measures

We also find signs that the depth of RSF program measures is increasing, with greater ambition in the latest programs compared to their predecessors.

The IMF categorizes reforms into high-, medium-, or low-depth measures. High-depth reforms encompass permanent institutional changes, such as legislative amendments (e.g., parliamentary approval of new value-added tax laws), or reforms with enduring impacts (e.g., civil service restructuring). Medium-depth reforms entail significant changes but are typically one-time actions (e.g., budget approvals or temporary adjustments to tariff/tax rates). Lastly, low-depth reforms may not bring about immediate change but serve as incremental steps towards larger reforms.

The IMF’s new guidance emphasizes that low-depth reforms “should not stand alone” except in exceptional cases, and when included, they should be part of a broader package of more substantial reforms.

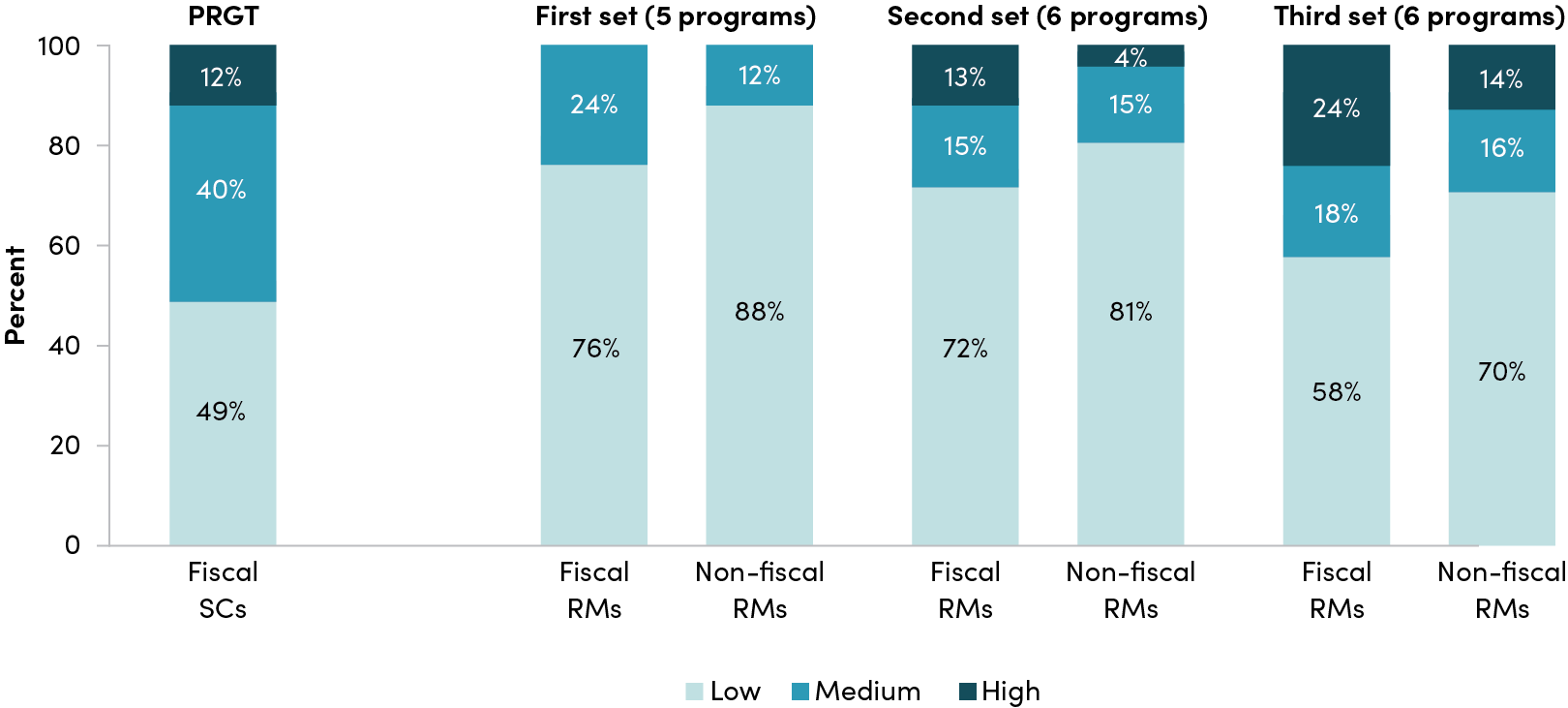

While the recent guidance has yielded more ambitious programs, there is still room to improve, especially given the scale of the climate challenge. Figure 2 below classifies reform measures into fiscal and non-fiscal categories across three groups of RSF programs and compares them with fiscal structural measures included in PRGT programs from 2008 to 2019. There is a discernible increase in the depth of reform measures from the first to the third set of programs. High-depth measures now constitute nearly one fourth of all fiscal reform measures in recent programs, more than in PRGT programs. However, they still fall short of achieving the levels of high- and medium-depth measures seen in PRGT programs.

Figure 2. Depth of reform measure is improving

Sources: SCs = structural conditions. RMs = reform measures. Fiscal SC, PRGT Gupta (2021) based on 131 programs implemented during 2008 and 2019; various RSF documents.

A notable development is the increased utilization of diagnostics to identify high-depth measures in more recent programs. A significant proportion of these measures, approximately two-thirds, has been identified through IMF/World Bank diagnostics and technical assistance provided to RSF countries. Specifically, they are drawn from the World Bank Country Climate and Development Report, the IMF Climate – Public Investment Management Assessment and the IMF Climate Policy Diagnostic. Additionally, almost 20 percent of these measures have been identified through pre-existing technical assistance or projects.

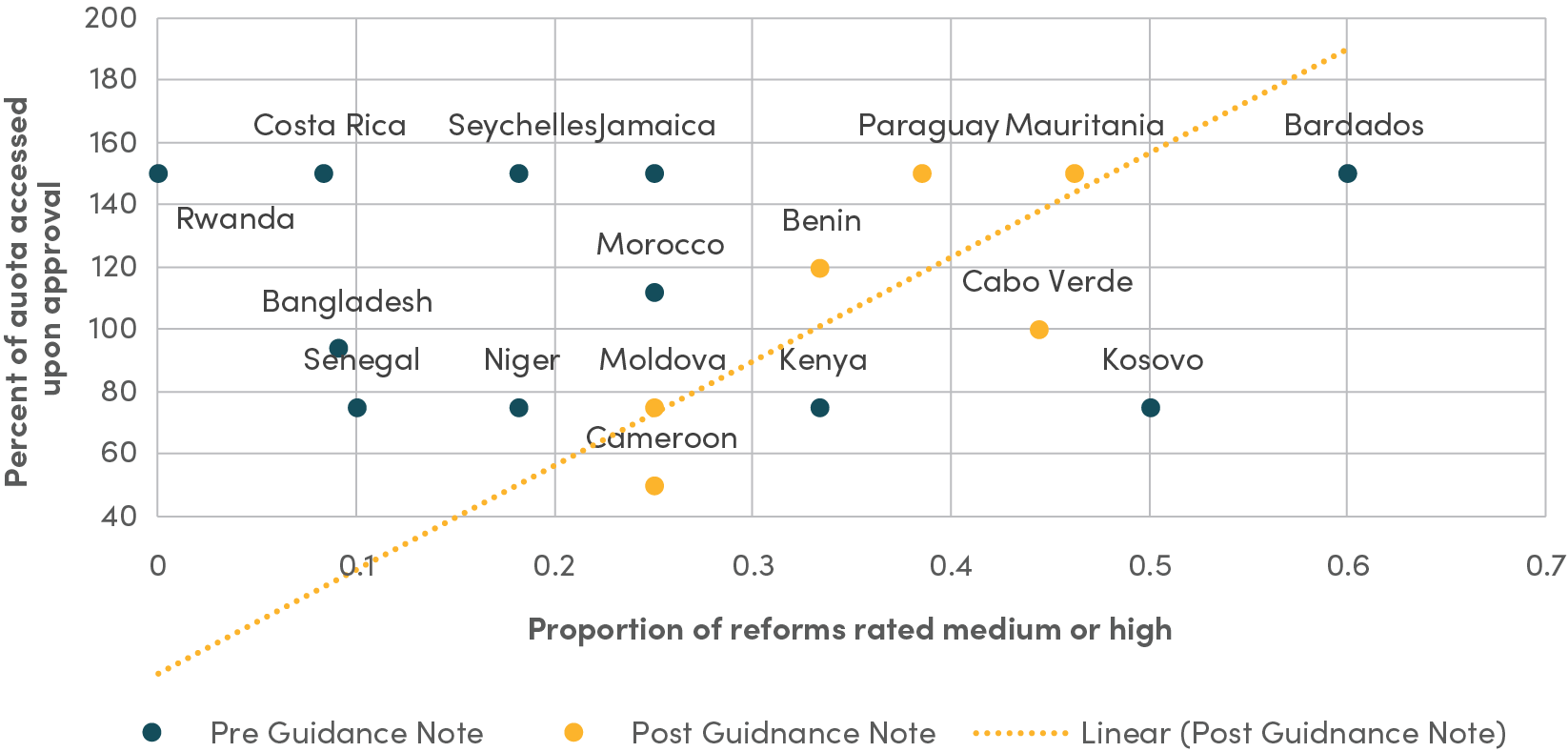

More ambitious programs are now receiving increased financing through the RSF. When the facility was established, it was anticipated that the challenge of reforms would be proportional to the amount of financing provided. This notion was reiterated in the November 2023 guidance note.

Figure 3 illustrates that since the guidance note, there is a stronger correlation between the amount of RSF financing provided (measured as a percentage of the quota accessed upon approval) and the complexity of the reform program (measured as the percentage of reforms rated as medium or high difficulty), as depicted by the trend line. For programs committed to prior to the guidance note, there appears to be little correlation between the financing provided and the difficulty of the reform program.

Figure 3. Amount of financing vs. reform difficulty

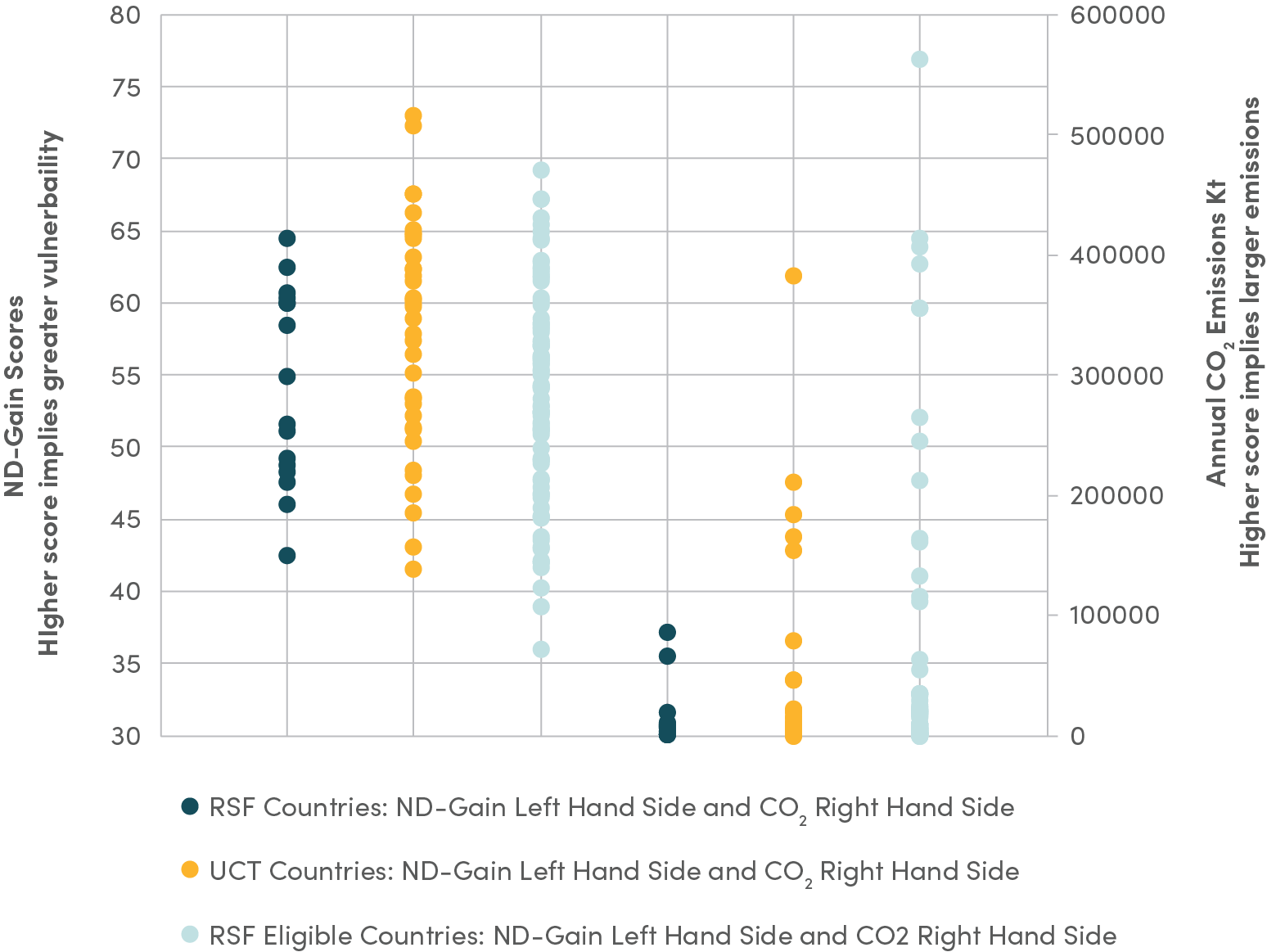

However, the RSF has yet to gain traction among the countries most vulnerable to climate change and/or those with relatively higher CO2 emissions. Among the 143 countries eligible for the RSF, there is significant diversity across measures of climate change vulnerability and CO2 emissions.

In Figure 4 below, we chart three groups: countries with an RSF program, those with IMF’s Upper Credit Tranche (UCT) conditionality program— a requirement for assessing the RSF—but without an RSF program, and countries that would otherwise be eligible for RSF but lack a UCT program. These comparisons are made across two climate-related indicators: the ND-Gain Index that evaluates vulnerability to climate change and CO2 emissions per country. Higher ratings on these indicators indicate worse climate change outcomes.

The figure indicates that the RSF is attractive to some countries vulnerable to climate change and/or some significant emitters. On the vulnerability index, the current RSF recipients are spread out in terms of their level of vulnerability, while for CO2 emissions, RSF recipients cluster towards the lower end of the distributions compared to the two groups that lack RSF programs. If the RSF were appealing to highly vulnerable countries and/or major emitters, we would expect RSF recipients to be clustered towards the top of the indicator distributions. While all countries need climate finance, why the most climate-vulnerable countries and the biggest emitters, including those with an existing UCT program, have not yet taken up the RSF is an important question for the IMF to answer.

Figure 4. Is the RSF attractive to the most vulnerable countries and/or largest emitters?

Note: Higher ND-Gain scores imply a lower level of vulnerability. The data used here has been inverted by subtracting each country’s score from 100 to facilitate the readability of the graph. Source: ND-Gain, and CO2 from WDI 2020; CO2 Emissions (Kt) latest available). Note there is no data available for Kosovo, and the CO2 data for China, India, and Russia has been dropped to aid the readability of the graph.

Despite the incorporation of numerous high- and medium-depth reform measures into programs, there persists uncertainty regarding whether countries are truly augmenting their investment in climate adaptation and resilience. One method to assess this is by monitoring climate-related investments in relation to total investment spending over time, considering the fungibility of RSF financing. Unfortunately, the IMF’s guidance note overlooked this concern.

Finally, none of the 17 RSF programs approved by the IMF Executive Board thus far have included financing for pandemic preparedness, despite the facility's intended mandate to do so. It appears that the borrowing countries did not perceive the necessity for such funding.

In summary, the November guidance on RSF seems to have addressed some of the shortcomings observed in the initial RSF programs. However, as we highlighted, other deficiencies remain unresolved and require attention from the IMF’s Executive Board during the upcoming RSF review.

We recommend:

- The Board should continue to encourage and enforce that programs have a larger share of medium- and high-depth measures and provide funding proportionally.

- The Board should also consider facilitating access to the facility for eligible countries with relatively high emissions, allowing them to access up to 25 percent of their IMF quota without requiring a concurrent IMF program with UCT conditionality, as advocated by our colleague John Hicklin in his forthcoming CGD paper.

- Finally, the Board should consider mechanisms for monitoring climate-related investment expenditure as a proportion of total investment spending facilitated by RSF financing.

Topics

CITATION

Dimond, Victoria, and Sanjeev Gupta. 2024. Assessing the Impact of New IMF Guidance on Resilience and Sustainability Facility Programs. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.