With the Biden administration now in the lame duck period, there is little opportunity to build on its current legacy, making this an opportune time to review President Biden’s track record while it’s still fresh. Some of my colleagues and I are preparing a series of blogs that will assess the Biden administration’s global development agenda over the past 3 ½ years and consider how a second Trump administration might affect its impact, especially in global health and climate.

This series will assess the Biden administration's impact based on the administration’s own account of its accomplishments as laid out in the U.S. Strategy on Global Development released by the White House in September 2024. Practically speaking, the strategy is a retrospective intended to cement the outgoing administration’s legacy, which the document itself acknowledges: “This strategy reflects the Biden-Harris administration’s commitment and work over the past four years to accelerate development progress around the world.” (italics mine). It is worth noting at the outset that because President Biden took office amid COVID-19, his ability to secure a legacy was constrained.

The administration’s strategy document is organized around five pillars:

- Reduce Poverty through Inclusive and Sustainable Economic Growth and Quality Infrastructure Development

- Invest in Health, Food Security, and Human Capital

- Decarbonize the Economy and Increase Climate Resilience

- Promote Democracy, Human Rights, and Governance and Address Fragility and Conflict

- Respond to Humanitarian Needs

The “strategy” lays out principles, policies and goals around each pillar and highlights major initiatives and accomplishments to demonstrate success. We will evaluate each in turn. But first, here are five high-level takeaways:

First, the success of some Biden-era initiatives depends on whether the next administration supports their continuity (a perennial challenge), and it’s likely that sharp reversals in policies, especially related to renewable energy and reproductive health, will be immediate.

Second, the Biden administration relied on multilateral financial institutions like the World Bank and other multilateral platforms like the G7/G20 for many of its big initiatives. Even if repudiated by Trump administration officials, these Biden-era reforms are more likely to endure because they have already taken institutional root (e.g., the change in multilateral development bank (MDB) mandates to include climate and other global challenges).

Third, a notable departure from previous administrations was the decision to prioritize a new industrial policy agenda to help build resilient and sustainable supply chains, including through friendshoring, in response to COVID-19, Russian aggression, and China’s domestic economic policies (i.e., its subsidization of the energy sector). The Biden policy agenda focused on renewable energy, and the Trump administration has affirmed that it will be much more fossil-fuel friendly. However, as part of an “America First” policy, the Trump administration may pursue its own efforts at friendshoring or supply chain diversification.

Fourth, multiple development policy initiatives were designed to thwart China, even though the country itself is often unnamed (e.g., the Nairobi-Washington Vision, discussed below). The Trump administration will have its own anti-China agenda but will likely employ blunter instruments (e.g., tariffs) as major policy tools, rather than working to build coalitions with likeminded countries to combat China’s influence.

Fifth, opposition to parts of the administration’s development agenda by some lawmakers has resulted in several unfulfilled financial promises, especially those directly related to climate. A key question is the extent to which the Trump administration will seek to fulfill other outstanding MDB pledges, including the forthcoming US pledge to support IDA. (IDA is the arm of the World Bank that finances low-income countries and is in the final stages of negotiating its 21st replenishment).

Read on for today’s first blog in this series of five:

U.S. Strategy on Global Development Pillar 1: Reduce Poverty through Inclusive and Sustainable Economic Growth and Quality Infrastructure Development

For this pillar, the administration emphasizes its commitment to reducing poverty and supporting sustainable, inclusive growth through the promotion of strong macro policies, capacity building, private sector-led investment, and job creation—all hallmarks of previous US administrations. But in stark contrast to previous administrations, President Biden included building resilient and secure supply chains as a major priority.

The Biden administration highlights three key initiatives as embodying the objectives of this pillar: 1) The Nairobi-Washington Vision; 2) the multilateral development bank reform agenda; and 3) the Partnership for Global Infrastructure and Investment. Here’s a look at each:

Nairobi-Washington Vision

The Nairobi-Washington Vision, endorsed by Presidents Biden and William Ruto of Kenya this May, lays out elements of a shared view on development finance, including debt relief. Unsustainable debt service burdens in many low- and middle-income countries have proved to be an especially intractable challenge, and the Vision was one avenue to try to apply pressure on China, by far the largest bilateral creditor in Africa.

In essence, the two leaders proposed that “high ambition” countries receive enhanced levels of financial support from international financial institutions, including the World Bank and the IMF, and bilateral creditors. “High ambition” countries are not named but characterized as those with robust domestic reform agendas committed to meeting global challenge goals, like climate and pandemic preparedness (including Kenya, presumably). While the vision is a bilateral document, it depends entirely on actions by multilaterals and other countries to come to fruition.

The joint statement also advocates that creditor countries provide relief to the “high ambition” countries through debt suspensions, restructurings, or new budget support. While it does not say so explicitly, this is obviously directed at China, which bears outsized responsibility for the debt crises plaguing many lower-income countries—including Kenya.

Doubling down on the (implicit) anti-China sentiment, the statement affirms that “free riding from individual creditors who get paid back from multilateral support should come to an end,” (i.e., it is not okay that MDB financing is enabling debt-ridden countries to pay China back at the expense of urgent development priorities). It also states that “transparent, sustainable, and resilient financing” should “replace opaque and unsustainable lending,” and that “non-disclosure agreements that keep citizens and their creditors in the dark about the terms of sovereign lending should no longer be used.”

The crux of this vision was first articulated in a speech by Treasury Under Secretary for International Affairs Jay Shambaugh in April 2024 during which he focused attention on high debt levels and record net outflows from low- and middle-income countries. A key remedy, he reasoned, should be enforcement of norms around official debt flows, including through IMF policy and comparability of treatment in restructurings. He argued that this would help incentivize official creditors “to participate responsibly with restructurings, reschedulings, or new liquid finance to borrowing countries.” While the bulk of the speech was aimed at China, the country itself never gets a single mention.

During a recent press conference, Treasury Secretary Janet Yellen called for implementing the Nairobi-Washington Vision “so that countries with strong policy frameworks facing liquidity stress receive the financing support they need to realize their sustainable development ambitions.” But at this stage there is no plan of action or follow-up mechanism underpinning the Vision.

A positive spin on this document is that it represents an unprecedented alignment between a Global South country and the United States on how international financial institutions should engage with client countries. A more cynical interpretation is that it is meant as a shot across China’s bow. Either way, while the logic may not be inconsistent with Trump administration objectives, there is little reason to think the new administration would work to operationalize the vision.

Reform of the Multilateral Development Banks

After taking office amid COVID-19 and increasingly urgent alarms about the risks of climate change, Secretary Yellen started making the case for MDB reform, underscoring that these institutions, while vital, were no longer fit for purpose. Her priority was to support the evolution of the MDBs’ missions, incentives, financing capacity and operational structures, with a special focus on the World Bank. MDB reform was also the major US “deliverable” at the 2023 G20, with President Biden committing to ask Congress for new funding to enable the World Bank to scale up lending for “global challenges” (e.g., climate). This is noteworthy because MDBs had never before been a major US priority at the G20.

The World Bank’s Evolution Roadmap (which colleagues and I have written about here and here) is well aligned with the Yellen vision. (For an assessment of broader reform efforts across the MDB system, see our MDB reform tracker.) Without re-hashing the roadmap in detail, suffice it to say that it focused heavily on the formalization of mandates for global challenges—like climate change—at the MDBs, especially the World Bank, which manifested as the Bank’s new “Livable Planet Agenda, ” approved in 2023.

The US also led efforts to push for the more efficient use of MDB resources after the publication of a G20-commissioned report on capital adequacy. The Capital Adequacy Framework (CAF) report provided five recommendations that together had the potential to dramatically boost lending volumes without putting MDB AAA credit ratings at risk. Pressure from shareholders, with a leading US role, prompted a range of actions around these recommendations, unlocking billions of dollars in development finance across the MDBs. G20 finance ministers affirmed the large scale of potential additional MDB lending if CAF reforms are fully implemented, which they estimated in their July communique at $357 billion over ten years. These reforms are centered around more efficient use of existing MDB capital and do not require additional US funding for MDBs. As such, they should be appeal to the Trump administration but could be undermined by a general inclination to turn away from multilateral institutions.

Yellen also emphasized the US role in bolstering lending at the regional banks, including capital increases for the European Bank for Reconstruction and Development and Inter-American Development Bank Invest, and a callable capital increase for the African Development Bank. (A callable capital increase requires authorization but no appropriations because funding is only made available in the unprecedented event that the institution could not repay its debt obligations.)

During a speech at the Brookings Institution, National Security Advisor Jake Sullivan ran a victory lap, heralding the US role in making the MDBs “bigger and more effective,” and unlocking “hundreds of billions of dollars in new lending capacity, at no cost to the United States.”

As discussed here, a disappointing outcome was the administration’s failure to obtain funding for several pledges for MDB financing to support “global challenges,” (e.g., climate). But even if approved, this funding would have had a comparatively small impact relative to the magnitude of resources made available through internal MDB reforms.

Partnership for Global Infrastructure and Investment

Launched in 2022 the Partnership for Global Infrastructure and Investment (PGI) was President Biden’s flagship G7 initiative to finance infrastructure in low- and middle-income countries. PGI aims to mobilize $600 billion by 2027 in “quality” infrastructure investments in emerging economies in an effort to counter China’s Belt and Road Initiative, especially in Africa. The emphasis on quality is meant to signal that unlike China, PGI projects would focus on sustainability and affordability. Its flagship project is the Lobito Economic Corridor, which stretches from the port of Lobito on Angola’s Atlantic coast to Zambia through the Democratic Republic of Congo.

The US committed to mobilize $200 of the $600 billion, and during the 2024 G7 Summit, hosted by Italy in May, President Biden reported that they had reached more than $60 billion, the vast majority from other actors including MDBs, large institutional investors, philanthropies and private companies. US funding is limited and largely in the form of guarantees and export credits.

It is difficult to assess the PGI because there are no formal reporting or accountability mechanisms that enable stakeholders to verify funding claims. But the truth is that many—if not most—of the projects credited to this initiative would likely have moved forward anyway, such as the $450 million agreement between the Millennium Challenge Corporation (MCC) and Zambia, or highly aspirational like the expansion of a Pacific-based infrastructure investment coalition to other regions.

That said, the PGI is arguably a good platform for making complex, transformational projects like the Lobito Corridor possible.

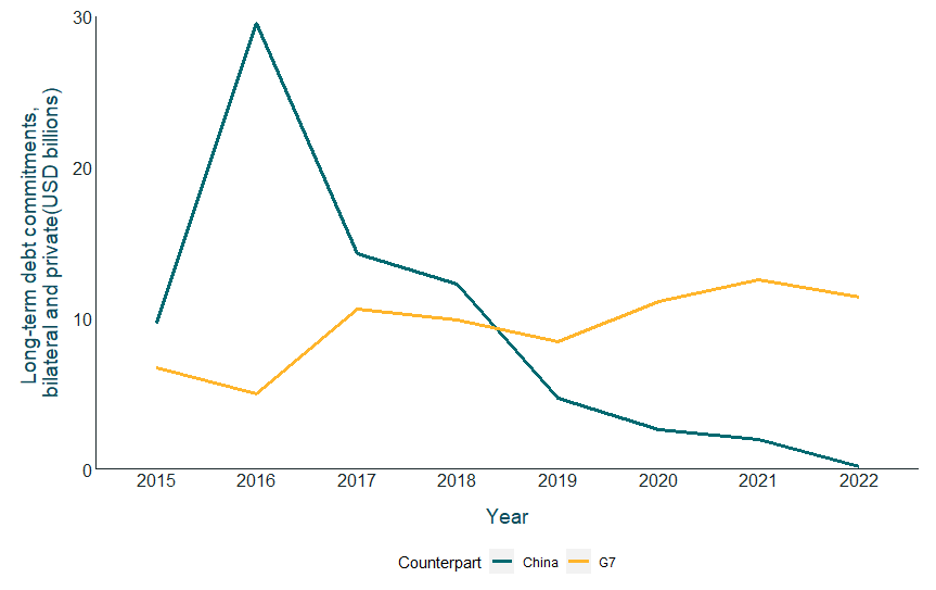

It turns out China did not need competition from the West to change its role in Africa. The specter of widespread debt defaults was incentive enough. According to Boston University, China’s funding to Africa peaked in 2016 at nearly $29 billion, but fell rapidly after that to a low of $1 billion in 2022. G7 investments have increased modestly over the same period, but this cannot necessarily be attributed to the PGI.

Legacy Assessment: Pillar 1

Under this pillar, the US deserves credit for getting the MDBs to expand their mandates to include global challenges like climates and pandemics, and for its advocacy around the balance sheet-stretching exercises, freeing up billions of dollars that will be instrumental in helping achieve a range of development goals. An open question is whether the Trump administration will aim to curtail MDB financing for climate mitigation and adaptation. Because MDBs are consensus-based organizations and other shareholders are strongly in favor of a climate-heavy agenda, it will be hard to reverse course so this legacy should endure.

President Biden’s China-focused initiatives under this pillar have been less successful so there’s no real legacy to protect. For example, the US had no clear way of gaining traction on its joint initiative with Kenya to induce China to be more cooperative in fixing the debt crisis and it’s simply not clear whether PGI is additive or largely an amalgamation of projects already in the G7 pipelines. However, because China grossly underestimated the financial consequences of making large, politically motivated investments of dubious economic merit, it may behave more like traditional donors in the future even without substantial external pressure.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.