Read Maya's letter "African countries cannot tax non-existent revenue" in the Financial Times (paywall).

Matti Kohonen of Christian Aid holds out the enticing prospect that African countries could collect an additional 1.5 percent of gross domestic product in tax if only big multinationals would stop dodging. The problem is that this estimate is (still) based on wishful thinking. Multinational corporations should pay tax, but the scale of potential revenues depend on underlying levels of investment and profitability in a country.

Let’s take a look at where the 1.5 percent estimate comes from. It is not an “IMF estimate” based on data from Africa, but a very rough global estimate from a working paper by Ernesto Crivelli, Ruud A. de Mooij, and Mick Keen. As the disclaimer on the front page reads “This Working Paper should not be reported as representing the views of the IMF…Working Papers describe research in progress by the author(s) and are published to elicit comments and to further debate.” Within the paper itself the authors call the estimate “highly speculative.”

Their calculation is based on two sets of numbers: the statutory corporate tax rates of 173 countries and the corporate tax base of 121 countries (the corporate tax base is found by dividing total corporate tax revenues by the statutory rate). They run a regression to try to work out how the corporate tax base reacts to changes in a country’s own tax rate, and the tax rates of other countries, both considering other real investment destinations (weighted by GDP) and other countries that attract paper profits as “tax havens.”

The basic logic of the calculation is that if a country’s corporate tax rate falls, its corporate tax base tends to rise. This reflects a combination of economic effects: greater real investment, more incorporation—and policy effects. Countries often combine changes of the tax rate with changes to the way that tax base is calculated. They “lower the rate and broaden the base.” So if a country’s base does not rise as much as might be expected following a tax rate cut, can this be explained by the tax rates of other countries—and in particular of tax havens—and thus be attributed to multinational profit shifting?

Perhaps, but it is also likely to be influenced by factors such as the certainty with which investors view the country’s tax system, and other barriers to investment which prevent them responding to tax rate changes. On the revenue side the amount of tax collected is influenced by domestic tax holidays and the ability to evade taxes domestically.

How big is 1.5 percent of GDP in context? It’s pretty large in relation to current corporate tax revenues. Low-income countries tend to collect an average of 2 percent of GDP as corporate income tax, and middle- and high-income countries collect around 3 percent. This includes both taxes on subsidiaries of multinationals and locally-owned companies. A 1.5 percent of GDP revenue gain therefore suggests that average income tax bills across the corporate sector would increase by over 50 percent.

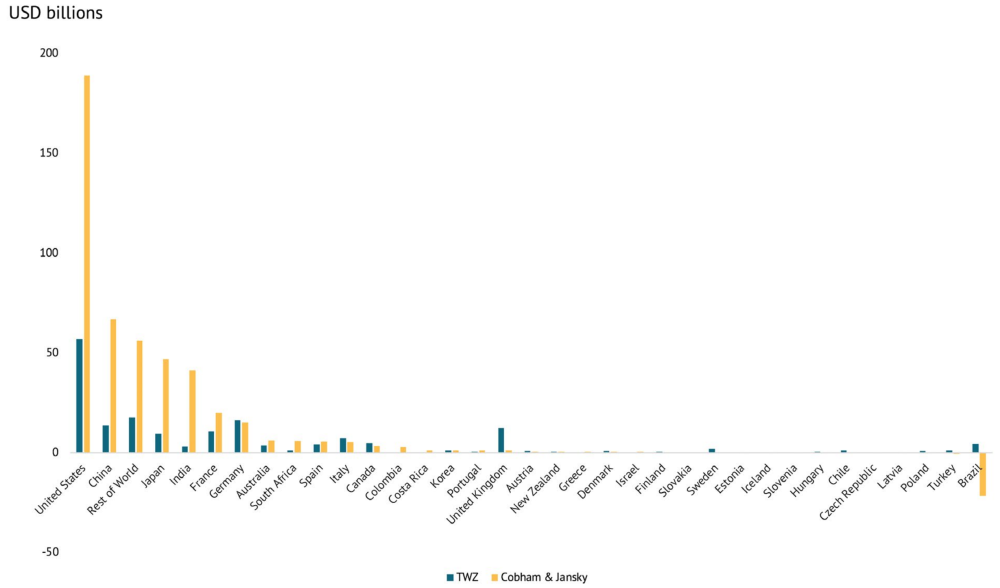

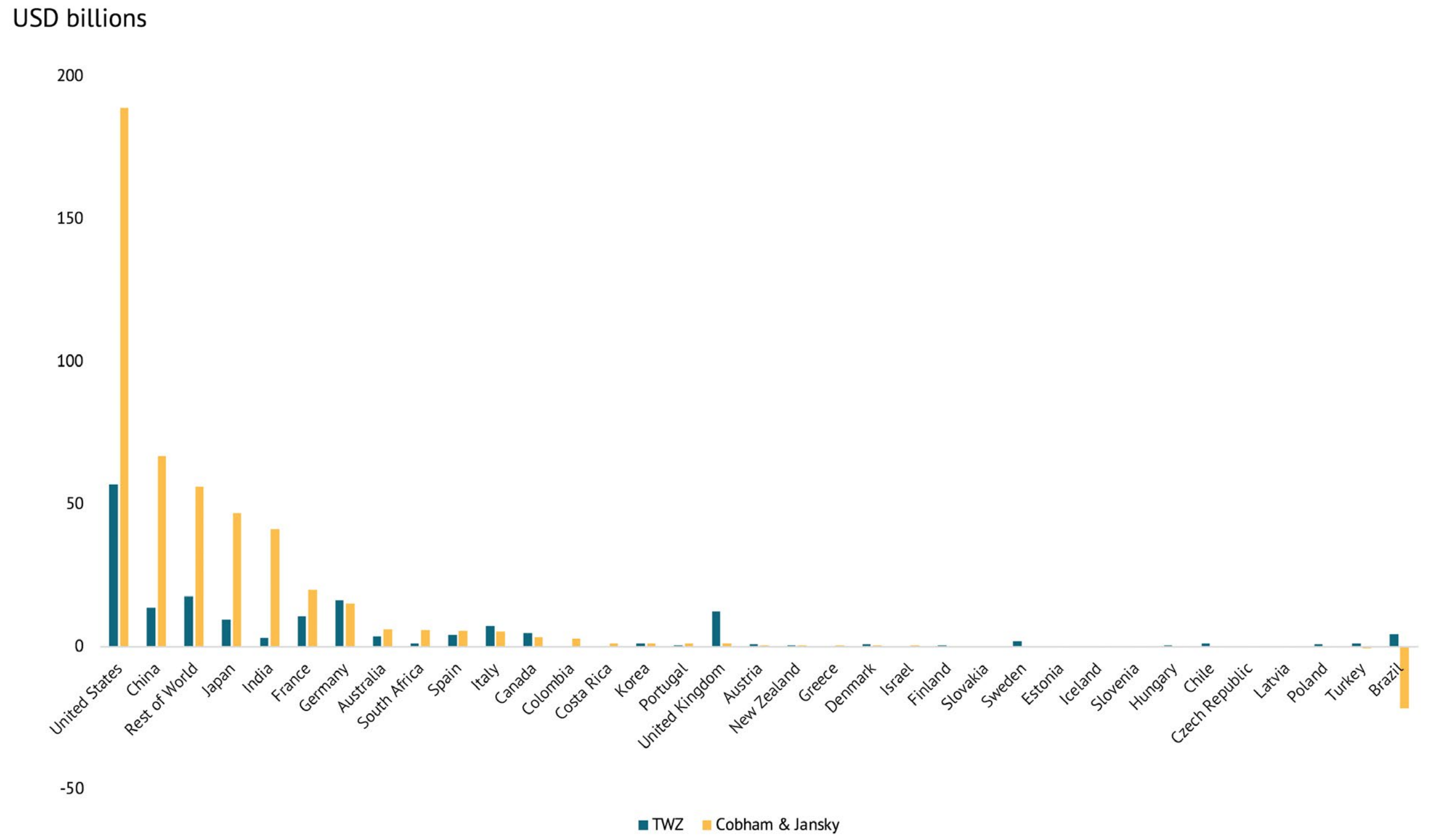

Furthermore, it is very large compared to the scale of foreign direct investment, and profits by foreign multinationals. Thomas Tørsløv, Ludvig Wier, and Gabriel Zucman last year estimated that the total net profits of multinational companies outside of their headquarters country average around 2 percent of GDP globally. In Brazil, China, and Colombia it is around 1.5 percent of GDP; in India it’s 0.5 percent. Based on these numbers, Tørsløv, Wier, and Zucman estimate revenue losses from corporate profit shifting which are a fraction of the scale of Crivelli, De Mooij, and Keen’s estimates. The graph below compares the estimates (drawing on country level estimates developed by Alex Cobham and Petr Jansky using the same methodology as the IMF working paper).

Two very different estimates in country-level revenue losses

The absolute value of revenue losses for low-income countries from multinational corporate profit shifting is likely to be much smaller than popular perception. For example, Tørsløv, Wier and Zucman’s calculations for India put the gross surplus of all foreign firms at around $15 per capita, suggesting tax revenues at stake are a couple of dollars per person per year.

Mick Keen highlights that the experience of efforts to enhance domestic resource mobilisation suggests we should be distrustful of fads. “The fundamental strengthening of revenue collection will be largely a matter of persistent and unspectacular effort.” Promoting spectacular hopes for gains from international action on multinational corporations risks undermines the persistent and unspectacular effort of policymakers and tax authorities (and of international action to assist them), as well as undermining the morale of citizens to pay tax.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

{kind=link}