Recommended

Substantial investments are needed in sub-Saharan Africa (SSA) to achieve the Sustainable Development Goals (SDGs) and address the climate crisis. A report prepared for the G20 last year underscored that two thirds of the required resources must be mobilized domestically, with the remainder sourced externally. Despite progress in boosting domestic tax collections since 1990, SSA countries—like other low- and middle-income countries—have witnessed stagnation in their tax-to-GDP ratios over 2012–2020. This stagnation poses a significant challenge to financing the SDGs and achieving climate outcomes, especially in a context where significant increases in concessional external financing also look unlikely, growth on the continent remains tepid, and rising interest repayments on sovereign debt now equal more than a third of tax revenues in many countries.

We argue that prospects to boost domestic revenue in SSA countries are grim, and future tax reform in SSA will need to be undertaken carefully, given the recent social unrest. There are reasons to be optimistic with recent growth in tax-to-GDP ratios in middle-income countries (MICs), but revenue performance in low-income countries (LICs) and fragile and conflict-affected situations (FSCs) continues to languish. This reflects the scarring of these economies by the COVID-19 pandemic, compounded by the relatively poor performance of value-added tax (VAT) as well as income and capital gains taxes.

Stagnating revenues during 2012–2020

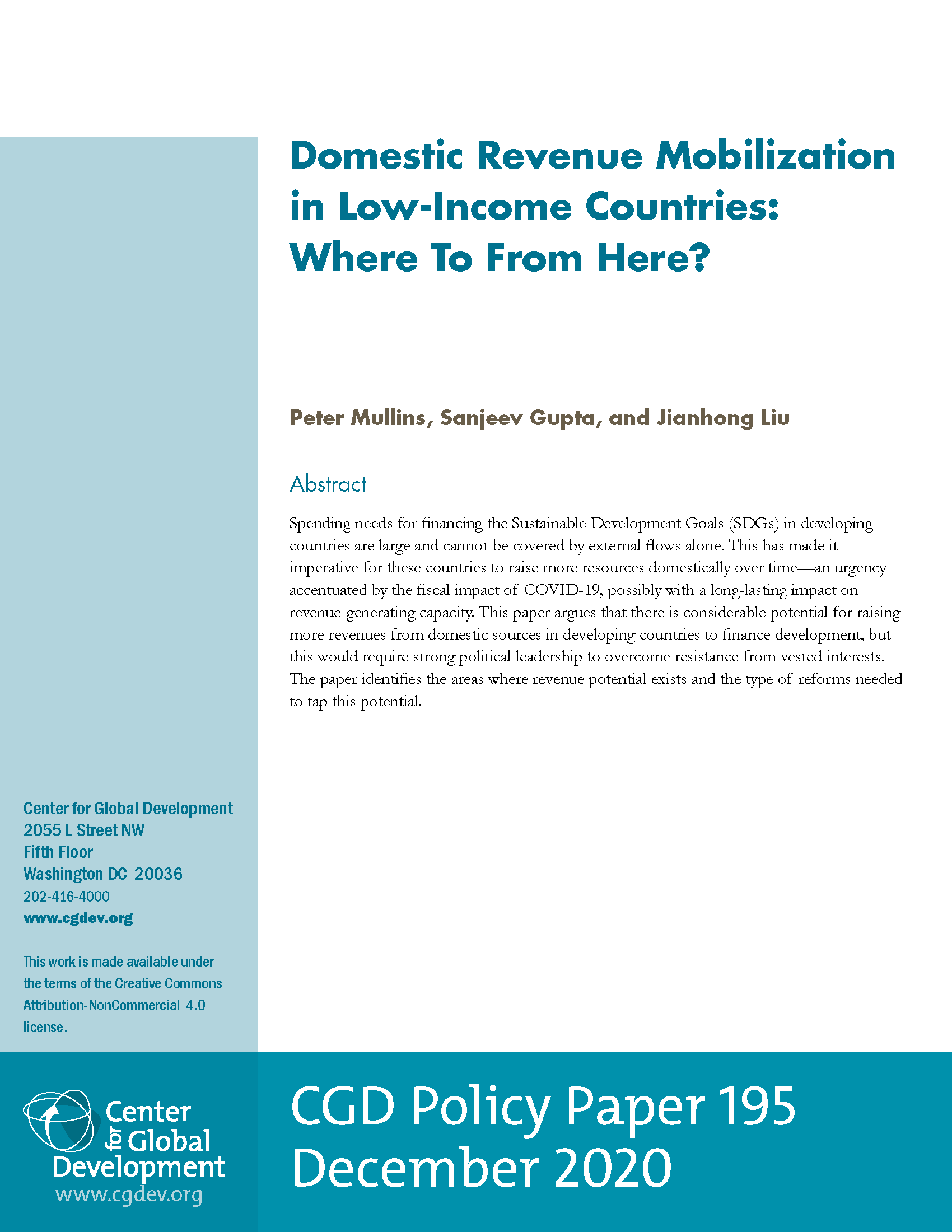

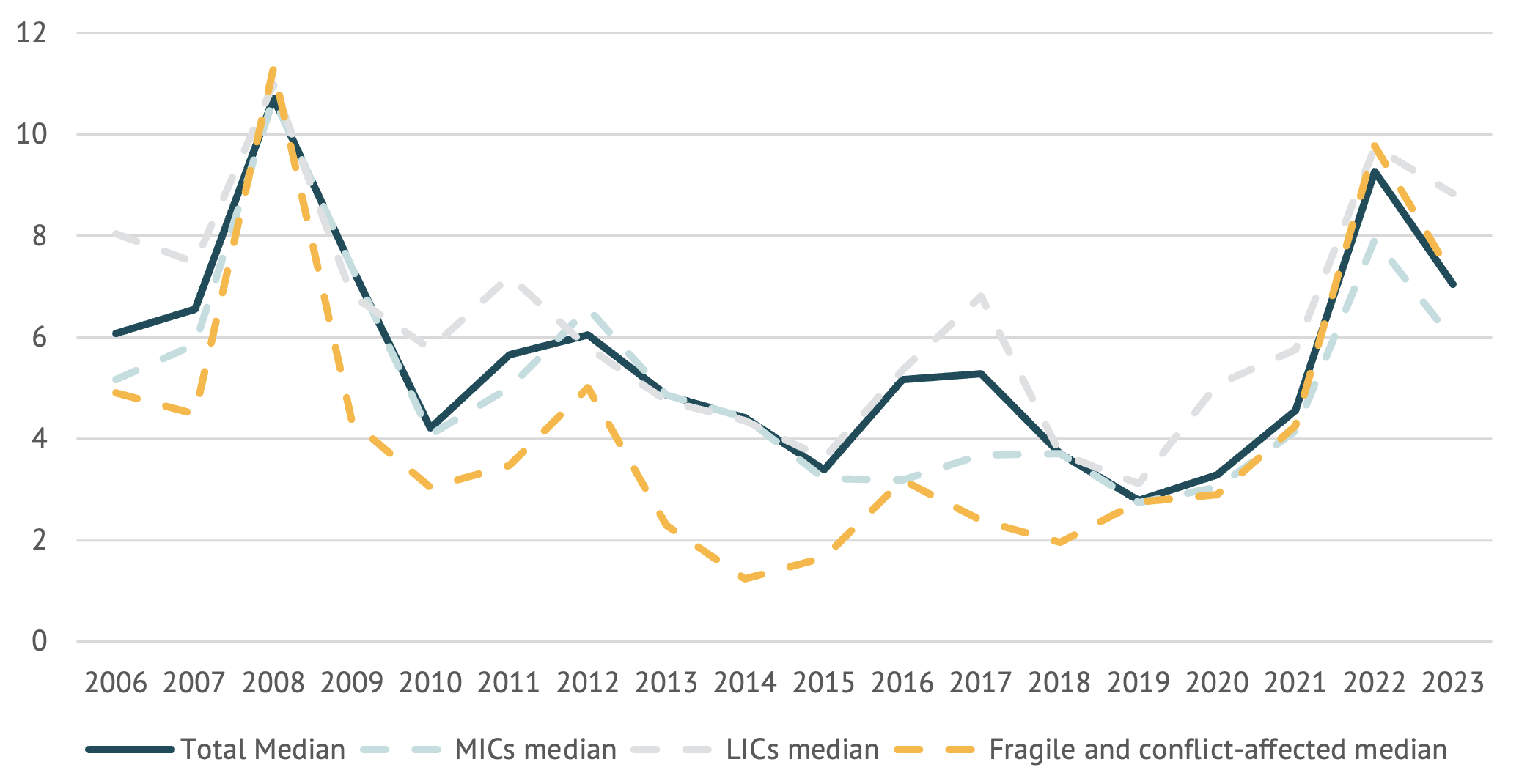

Figure 1 below shows that the median tax-to-GDP ratio in SSA remained virtually unchanged at around 13 percent of GDP during 2012–2020. That ratio is low, below an average of 18 percent in other emerging and developing economies.

The good news is that there is an upward trend starting in 2021, driven largely by sub-Saharan African MICs, where the median tax-to-GDP ratio rose from 17.0 percent in 2021 to 18.6 percent in 2023. The challenge will be to sustain these improvements (Figure 2).

In contrast, LICs and FCS have shown little change in the tax-to-GDP ratio since 2012. For the former, the tax-to-GDP ratio has hovered around 12.0 percent, while for the latter it has stood at about 11.7 percent (Figure 3). This level of revenue effort cannot support the achievement of the SDGs and facilitate the climate transition as envisaged in last year’s G20 report.

Figure 1. SSA median tax-to-GDP ratio

Source: IMF World Economic Outlook (WEO) April 2024: General Government taxes, percent of fiscal year GDP. The classification of countries into middle-income, low-income, and fragile and conflict-affected situations is based on the IMF’s Regional Economic Outlook. Note: Chad, Eritrea, Gabon, Somalia, and South Sudan are not included due to a lack of data.

Drivers of revenue performance of SSA’s middle-income countries

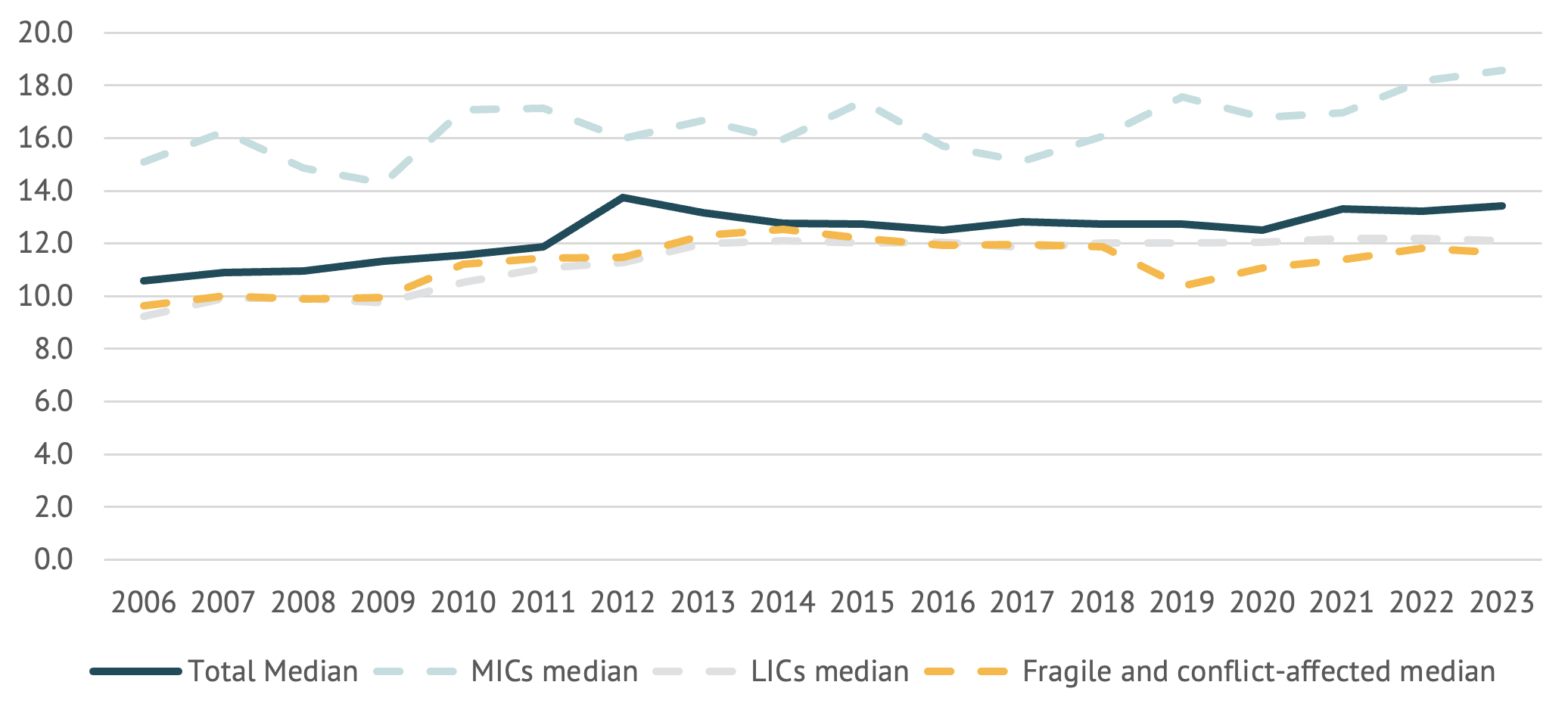

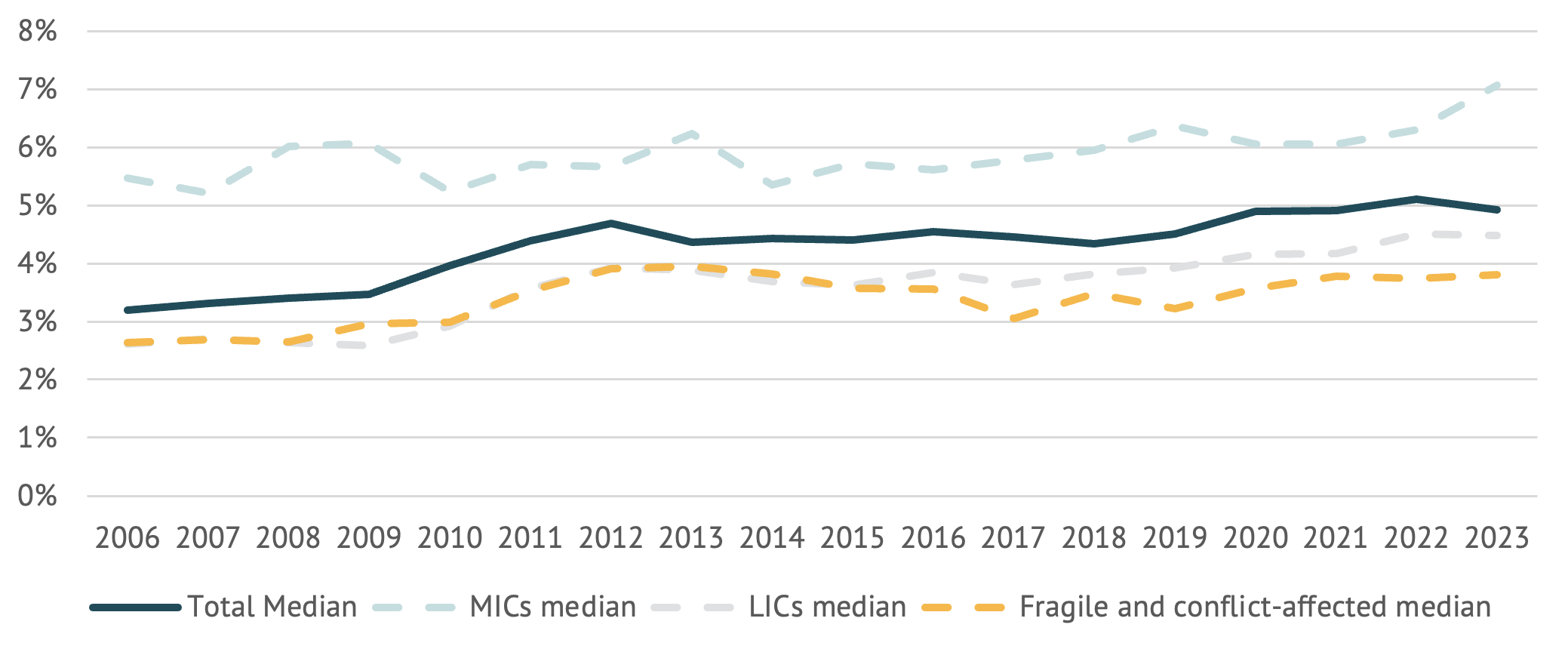

Figures 2 and 3 below suggest that the recent increase in tax collections in sub-Saharan African MICs is attributable to increased collections specifically from taxes on income and capital gains (equivalent to around two thirds of the increase in tax-to-GDP) and taxes on goods and services or value-added tax, or VAT (equivalent to approximately another third). These are important reform areas for SSA. In an earlier study, we noted that mobilizing additional domestic revenues will require limiting tax expenditures ( tax credits, deductions, exemptions, and preferential tax rates) which are mostly granted in two areas in SSA—corporate income taxes and VAT, together costing between 2 percent and 6 percent of GDP. That study also stressed the need to strengthen progressive taxation in SSA by adjusting personal income taxes. Top personal income tax rates tend to be lower in SSA countries than in advanced economies, and apply at a much higher income level as a multiple of GDP per capita. Reducing tax expenditures in VAT is a key reform area for SSA countries: these expenditures lower tax collections in MICs in SSA by 3.2 percent of GDP as compared to 2.1 percent of GDP in LICs. Streamlining excises by limiting them to a few goods that have significant negative externalities and implementing environmental taxation would also be desirable. The drawback is that these recommendations would raise the effective tax rate by expanding the tax base or raising tax rates, which in the current environment is likely to be difficult.

Figure 2. Median taxes on income profits and capital gains as a percent of GDP

Source: IMF WEO April 2024: General Government taxes on income, profits and capital gains, and GDP current prices. The classification of countries into middle-income, low-income and fragile and conflict-affected situations is based on IMF’s Regional Economic Outlook. Note: Chad, Eritrea, Gabon, Somalia, and South Sudan are not included due to a lack of data.

Figure 3. Median taxes on goods and services as a percent of GDP

Source: IMF WEO April 2024: General Government taxes on goods and services, and GDP current prices. The classification of countries into middle-income, low-income, and fragile and conflict-affected situations is based on the IMF’s Regional Economic Outlook. Note: Chad, Eritrea, Gabon, Somalia, and South Sudan are not included due to a lack of data.

Prospects for reforming SSA tax systems going forward

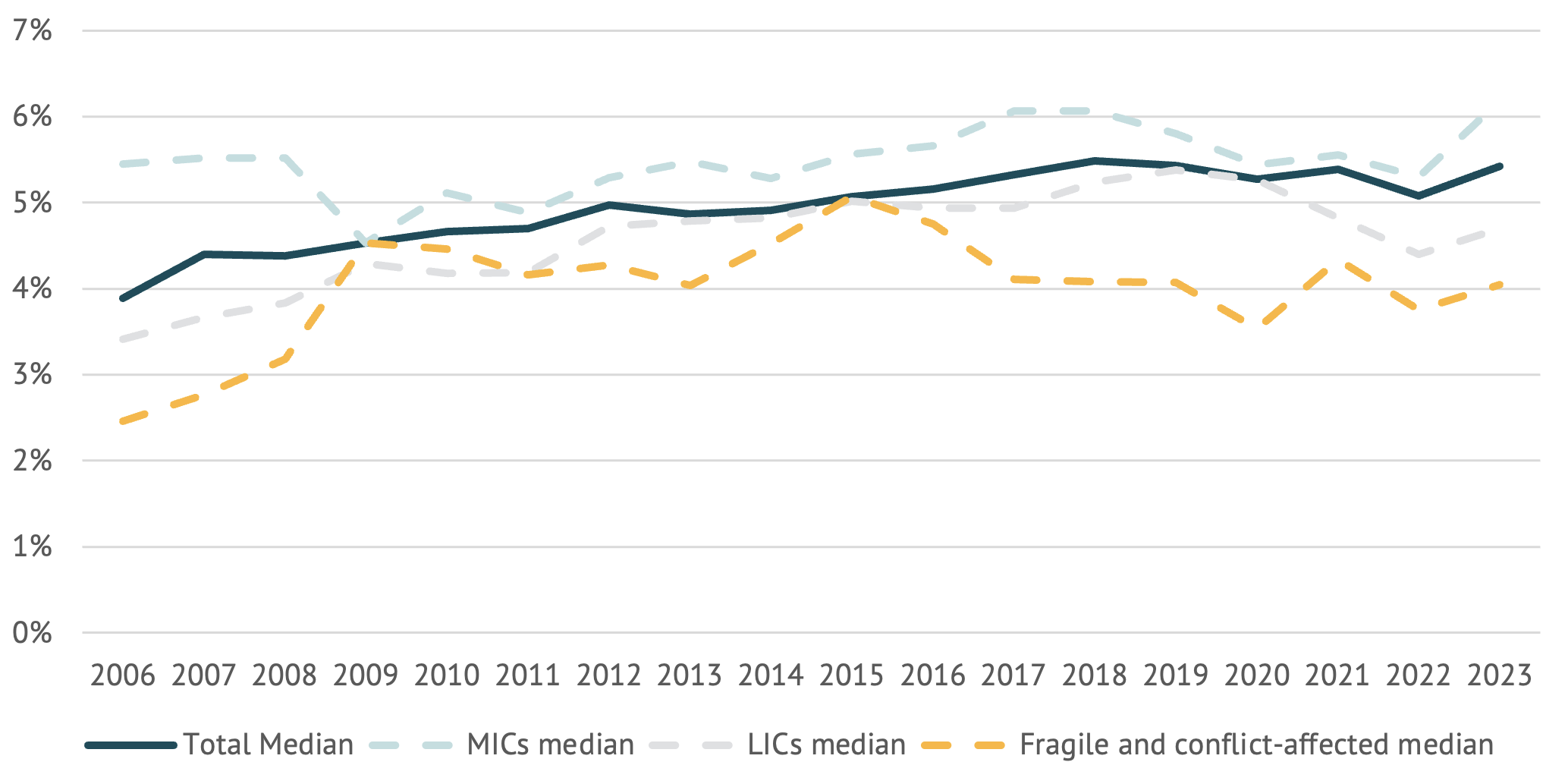

The prospects of adjusting tax effective rates in SSA to raise more revenue domestically in the immediate future have become increasingly unlikely in part due to the recent social unrest in response to proposed higher taxes in Kenya in May and to a reduction of subsidies in Nigeria in August and in part due to elevated inflation (Figure 4). Under this milieu, the leadership of SSA countries are likely to be reluctant to embark on tax reforms. Kenya and Nigeria, both middle-income countries have experienced some increases in their tax-to-GDP ratios since 2021. However, these levels remain below their potential for revenue generation. Both countries face growing fiscal and debt pressures, and increasing tax revenue is one way to help alleviate these challenges. While some of the proposed tax changes were aimed at those who were relatively more well off, and at improving environmental outcomes, it is exacerbating cost of living pressures and instigating social unrest.

Figure 4. SSA Median consumer prices, percentage change

Source: IMF WEO April 2024: Inflation, average consumer prices, percent change. The classification of countries into middle-income, low-income and fragile and conflict-affected situations is based on the IMF’s Regional Economic Outlook. Note: Chad, Eritrea, Gabon, Somalia, and South Sudan are not included due to a lack of data.

Going forward, these prospects could improve if leadership of SSA countries engaged with citizens, businesses, and civil society on future tax and subsidy policies. This should include discussions on the use of part of the additional revenues to finance targeted safety nets for lower- and middle-income households to ensure that the overall changes in the tax and transfer system are progressive, and to ensure these changes happen in an orderly and sequenced manner. Otherwise, prospects for raising additional domestic resources for the SDGs and the climate transition will remain bleak.

We wish to thank Benedict Clements for helpful comments.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.