This week over 170 policymakers, government officials, and members of academia, civil society, and international organisations will gather in Berlin to discuss the future of the Addis Tax Initiative (ATI). The overarching goal of the ATI is to improve domestic revenue mobilisation (DRM) in order to finance the Sustainable Development Goals (SDGs). More than 55 countries, regional and international organisations have joined the ATI, which commits donors to collectively double their assistance to DRM, developing countries to step up their tax collection efforts, and all members to ensure “policy coherence for development.” However, noticeably absent from the ATI’s progress monitoring is the issue of equity. Indeed, analysis by Oxfam finds that only 7 percent of DRM support reported by ATI donors in 2017 contained clear goals related to equity or fairness in revenue systems.

The importance of equity

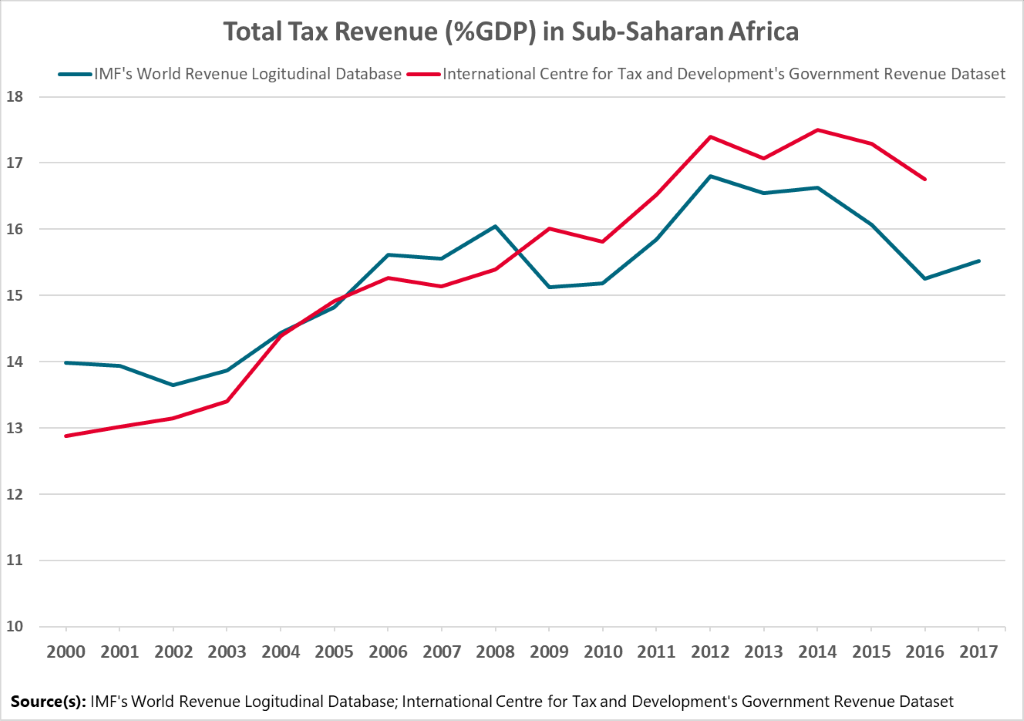

If the primary goal of DRM projects and reforms is simply to collect more revenue, this can have negative consequences for development efforts. For example, revenue targets (like collecting 15 percent of GDP in tax) can create perverse incentives to collect wherever it is most feasible – which can harm those without political power such as the poor or women the most. Tax and transfer systems in low and middle-income countries are, in general, far less effective than those in OECD countries at reducing poverty and inequality. In fact, research by the CEQ Institute shows that in 16 out of the 29 countries analysed, taxes and direct transfers to the poor actually increased income poverty. Of course, part of that pattern reflects the inadequacy of social spending, but it equally reflects the need for a greater focus on the equity implications of tax reforms.

Priority areas for increasing equity in DRM

Given that in low and middle-income countries, taxes on consumption currently make up over 60 percent of revenues, there is a great deal of room for making tax systems more equitable at the national level. We suggest four priority areas for reform:

-

Strengthening taxation of income and wealth: OECD countries collect about 10 percent of GDP in personal income taxes, while non-OECD countries collect only slightly more than 2 percent of GDP on average. There is much developing countries can do to better tax professional incomes, increase the progressivity of income tax schedules, and tax inheritance and capital gains. When it comes to wealth, it remains largely undertaxed, despite a surge in ultra-high net worth individuals (especially in developing countries). An increasing amount of that wealth is being concentrated in real estate, yet property tax collection is similarly low. Non-OECD countries on average collect merely 0.5 percent of GDP from property taxes (compared to 2-3 percent in OECD countries). If low and middle-income countries as a group could reach 1.5 percent, this would be equivalent to an additional $28.9 billion in government coffers annually: more than total combined aid disbursed by Canada, France, Netherlands, Norway and Sweden in 2017.

-

Rationalising the use of tax incentives: Tax incentives to attract investment can play a legitimate role in economic policy. Unfortunately, studies suggest that tax incentives in developing countries frequently continue to be characterized by excessive discretion, poor monitoring, and little transparency. The result is reduced revenue and little new investment – in effect, a handout to corporations and wealthy interests. More transparent and accountable governance of tax incentives is needed.

-

Reducing the burden of consumption taxes and informal and nuisance taxes on the poor: While many assume that the poor do not pay much tax in low-income countries, they actually bear a heavy fiscal burden due to a wide array of consumption and informal taxes, small subnational taxes and levies, and formal and informal user fees to access essential services. In low and middle-income countries, consumption taxes make a significant proportion of the poor poorer than they were before taxes and transfers. Unless the poor can be sufficiently compensated with transfers, exemptions for basic foodstuffs and other essential goods may thus be necessary. Studies from Sierra Leone and the DRC suggest that total formal and informal burdens of direct taxes, levies, and user fees make up as much as 10-20 percent of the incomes of poor households. Limiting these burdens should be given significantly greater priority.

-

Enhancing the participation of accountability stakeholders: Civil society organizations, academic institutions, women’s rights groups, and journalists have a critical role to play in monitoring and pressing for increased fairness in tax systems, voicing the concerns of the vulnerable, and advocating for the translation of tax revenues into public benefits. Nevertheless, in 2017, only 7 percent of DRM aid (reported to ATI) supported these actors.

Parallel action is also needed at the global level to make the ATI’s third commitment to “policy coherence” a reality:

-

Reforming the international tax system. While the BEPS Action Plan was a useful first step in trying to combat aggressive tax avoidance, it is not enough. Low-income countries continue to be disadvantaged by restrictive tax treaties and often still have little voice in global decisions that impact their taxing rights. All countries should be given the opportunity to raise their voice in the BEPS 2.0 negotiations, even if they are not members of the OECD Inclusive Framework – a situation that pertains to half of ATI partner countries. Meanwhile, existing international rules continue to be difficult to implement in lower-income countries, which are substantially more dependent on corporate tax revenues than OECD countries. A continued push for developing country taxing rights and priorities, including simplified approaches to enforcement, is needed.

-

Increasing cooperation on tackling offshore tax avoidance and evasion by wealthy individuals. It is estimated that Africans hold $500 billion in financial wealth alone offshore, which results in governments losing around $15 billion per year in unpaid taxes. Progress must be made to include developing countries effectively in automatic exchange of information processes and ensure effective collaboration in cases of tax evasion, while strengthening rules on beneficial ownership.

-

Continuing external support. In low-income countries, even the most substantial improvements in DRM will not generate enough revenue to finance adequate social protection and human development floors. External support such as aid will therefore remain critically important in pursuing equity at the global level.

Prioritizing equity in the ATI agenda

The theme of this week’s conference is “Towards a Roadmap for the ATI post-2020.”

In drawing that roadmap, we are calling on ATI members to focus more explicitly on equity and inclusion. Along with the priorities outlined above, we propose that members of the ATI:

-

Adopt specific indicators on revenue composition in monitoring progress on Commitment 2, in order to prioritize not only collecting more revenue, but from more progressive sources, like direct taxes on income and property, rather than indirect taxes on consumption.

-

Regularly assess, under Commitment 3, tax spillovers and the distributional impact of tax policy reforms. ATI donor countries should conduct tax spillover analyses to ensure that their own corporate tax rules and practices, and tax treaties, are not undermining their DRM support. ATI partner countries should conduct distributional impact assessments in order to ensure the drive for more revenue does not come at the expense of achieving the SDGs, particularly on inequality and poverty.

-

Make a collective commitment to increase tax transparency. All government ATI members should commit to transparency on data about tax collection, tax policy decisions, administrative practices, and the amount of revenue raised from each type of source. In addition, all ATI members should commit to encouraging and facilitating the engagement of accountability stakeholders, and to support the effective representation of developing countries in international policymaking forums.