Recommended

Blog Post

The World Bank’s Self-Inflicted Crisis

The private sector should be engaged with the World Bank Group. Firms care a lot about government policies, and the bank has influence on those policies through both research and advice as well as policy lending across its client countries. Firms want access to finance, and the bank’s private sector arm committed $71.7 billion to investments in fiscal year 2025. Again, firms want access to business, and the World Bank’s procurement team currently supports projects with a total commitment of over $300 billion. Meanwhile, the Bank Group needs private sector engagement, as the largest source of jobs and growth worldwide, as investment clients and as service providers.

But this necessary and important relationship needs guardrails: the Bank Group’s ultimate clients are its member countries, and private interests of individual firms can be very different from the public interest of those ultimate clients. It is imperative that the Bank Group act in the public interest, and it is important to the Bank Group’s credibility and effectiveness that it is seen to be doing so.

That is why the Bank Group has rules and guidance governing potential conflicts of interest facing staff and the institution in cases where private interests and public interests might diverge. But this guidance is being tested by a closer relationship between firms and World Bank leadership, as well as reforms to bring the Bank Group’s private and public sector arms closer together.

The Private Sector Investment Lab and the World Bank Group

The World Bank’s Private Sector Investment Lab brings CEOs of global companies into the bank to offer advice on reforms to the institution. The bank suggests that: “Since the Lab's launch in 2023, private sector leaders have provided the World Bank Group with valuable feedback that has helped us better align our strategies and undertake several new initiatives to increase the speed and scale of private capital flows for development.”

As with any firms operating in World Bank client countries, the firms that Lab members run will be interested in the advice the Bank Group offers and the policy conditionality that sometimes comes alongside World Bank lending. To take examples, Bayer AG might be particularly interested in what the World Bank has to say about the regulation of genetically modified organisms (GMOs) or glyphosate. Tata is surely and reasonably interested in what the World Bank suggests about policy and regulation around public-private power projects.

Again, the firms that Lab members run are frequently involved in IFC-backed projects as financiers and sponsors: Tata’s relationship with the World Bank Group in particular is long (and more than a little complex), and there have been 24 Tata-IFC projects so far. But it’s not just Tata; Macquarie is or has been an investor or sponsor in 19 different IFC-backed projects, while HSBC, Temasek, Standard Chartered, Standard Bank, AXA, and Dangote all appear as well, multiple times. And Tata Power and Tata Projects are suppliers on World Bank financed contracts worth $341 million since 2020, for example, while Bayer has supplied $47 million in contract value over that time.

Lab members have also advocated changes to the Bank Group that would allow their companies to invest more in World Bank client countries—indeed, this is a central idea behind the creation of the Private Sector Investment Lab. BlackRock has long called for multilaterals including the World Bank to “de-risk” investments in developing countries so that firms like BlackRock can profitably finance them. And thanks to the Private Sector Investment Lab, the IFC has started down that path, issuing a collateralized loan sold to institutional investors. (This was attractive to investors. It is less clear if it is sustainable for the IFC, which will have to pay most of the investors an interest rate about four times what it pays to borrow on its own behalf, on top of arrangement and insurance fees.)

A second example: the Private Sector Investment Lab suggested IFC do more local currency financing, and Standard Bank is now partnering with IFC to hedge currency exposure linked to local currency lending, including in a number of IDA countries where IFC local currency hedging is often subsidized by the World Bank’s IDA itself.

A conflict of interest within the World Bank Group?

There is nothing untoward about the fact that Lab members represent firms with financial interests in the World Bank Group’s investments and policy positions; indeed that might make their advice more pertinent. And Lab members are not board members, management, or employees of the World Bank or IFC. It is not the offering of (even self-interested) advice from outside that creates the risk of a potential or perceived conflict of interest in the Bank Group. The concern here is whether World Bank staff and management favor, or are perceived to favor, the interests of Lab members and the companies they run over the interests of the Bank Group and the countries it works for.

A recent example involving a Lab member is a report on Nigeria’s economy published by the World Bank on April 7. One of the recommendations: open petrol imports to bring prices down. “Allowing qualified marketers to resume imports would restore competition, reduce pricing distortions, and better align domestic prices with global benchmarks. Greater market contestability would also strengthen supply security by reducing reliance on a single refinery.” The Dangote refinery referred to by the report is preparing for an initial public offering that might raise $5 billion, and is owned by Lab member Aliko Dangote.

On April 9, the report was taken down by the World Bank on the grounds that opening to petrol imports “may run counter to efforts that countries around the world are undertaking to ensure their energy and national security.” Then on April 15, Aliko Dangote gave a keynote address at the bank, introduced by the World Bank’s president as “an old friend of mine” making "very large-scale investments that have expanded domestic refining capacity and reduced the reliance on imports.” Subsequently, a new version of the report was issued without the language on opening to fuel imports.

I don’t know if the report’s initial advice was good advice in the context of Nigeria at this moment (even though “increase competition to reduce prices” is hardly a radical departure from World Bank policy positions of the past). And the report’s withdrawal may be an innocent coincidence of unfortunate timing. But for those who might want to question the quality or impartiality of the World Bank’s policy advice, even an unfortunate coincidence can provide potential ammunition if conflict of interest rules aren’t rigorously and transparently applied.

And yet while all Bank Group employees are meant to follow a code of ethics in their work that includes reference to conflicts of interest and the staff manual lays down general obligations, there is no specific published conflict-of-interest language, disclosure requirement, or recusal policy for Bank Group staff and management regarding working with the Private Sector Investment Lab and its members.

A broader challenge

This speaks to a larger issue connected to the World Bank’s ongoing reorganization, which includes the merger of numerous IFC and World Bank departments. The interests of those investing in private projects are not always the same as the public interest. The IFC invests in private projects. The World Bank is meant to advise and invest in the public interest. There is an ongoing risk of conflict there.

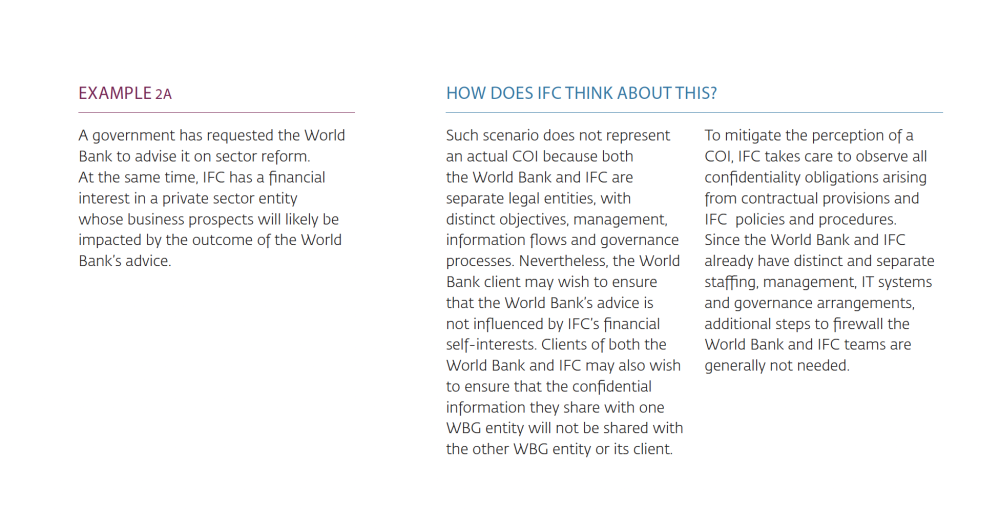

The IFC’s traditional advice on conflict of interest between providing policy advice directly related to investment returns alongside private sector investment support in the same country-sector can be summarized as: don’t do it. The handbook provides an example: “IFC has a loan investment in an Independent Power Producer (IPP). Later the government asks IFC to advise on the tariff it should pay under the Power Purchase Agreement (PPA) with the IPP.” The guidance it offers: “this is a circumstance in which IFC would decline the government’s request to advise.” The IFC’s general counsel has traditionally been more relaxed about conflicts of interest involving the World Bank because it and the IFC “are separate legal entities, with distinct objectives, management, information flows and governance processes.” But, of course, that is precisely what is going away.

An illustration of the problems that might result involves the Tata Power hydropower project in Bhutan agreed this year, which shares with many other IFC energy investments the fact that it was not competitively bid despite World Bank guidance around best practice for public-private power projects. Sadly, it also involves the World Bank not following its own best practice guidance as well, because the bank is also involved in design and financing. Tata’s investment will benefit from a $150 million grant and a $150 million credit from IDA, $215 million in IBRD loans, and $300 million from the IFC.

Figure 1. Managing IFC and World Bank Conflicts of Interest (2018)

Source: IFC: Facilitating Multiple Roles IFC Conflicts of Interest Management Process

The risks of “One World Bank Group”

The private sector is the engine of growth and job creation worldwide. The World Bank should listen to private sector representatives about their needs and concerns in order to better serve its client countries—most of which are themselves very keen for the institution to focus on growth and jobs.

But the Bank Group is a public sector institution meant to be engaged in promoting the public good. A web of rules and mechanisms to seek widespread input and avoid any potential or perceived conflicts of interest is part of that. While the evidence suggests the Bank Group has long struggled to be fully impartial—toward the countries it ranks, regarding the companies it invests in, and the companies paid to deliver projects—that web of rules and mechanisms appears at risk of further fraying.

There should be public clarity regarding conflict-of-interest guidelines affecting staff and management working with the Private Sector Investment Lab, as well as greater transparency in its operation. The Lab should open up to a wider group of actors—both on the grounds of diluting any sense of undue influence from a particular sector but also to gain valuable perspectives. Primarily talking to firms that already have significant engagement with the IFC, for example, is unlikely to address the concerns of the investors who haven’t engaged with the IFC—which appears to include potential investors in low-income countries, where the IFC is largely and increasingly absent.

More broadly, perhaps the bank might stand up a Regulation and Competition Lab to seek input from officials charged with ensuring private investment occurs on a level playing field, alongside civil society organizations dedicated to transparency.

And before mergers between IFC and World Bank units go any further there should be a discussion involving the Board and shareholders of what units must stay separate or be returned to separation to avoid conflicts of interest and, for any units still to be merged, how conflicts of interest will be resolved. Both the World Bank Group’s credibility and effectiveness are at issue.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: World Bank Photo Collection/ Flickr