Recommended

The Spring Meetings of the International Monetary Fund and the World Bank were dominated by discussions of the economic impact of the Iran war and concerns about declining global cooperation. With representatives from across the globe flooding Washington, it was clear the war’s impacts varied sharply by location. For example, natural gas prices are up 46 percent on the main Asian market, up by 38 percent in Europe, and down by 19 percent in the US (as of April 26, 2026). These price disparities are muted by rationing, which is increasingly common in Asia (e.g., Sri Lanka). Given what we learned about the cost of school closures/online classes during the COVID pandemic, it is disturbing to see countries like Lao PDR, Pakistan, Peru, and Sri Lanka turn to this again. Fiscal burdens vary enormously depending on whether—and how much—countries subsidize or cut taxes for fossil fuels (my colleagues Liliana Rojas-Suarez, Catherine Pattillo, and Clemence Landers discuss the fiscal and monetary implications of the war for low- and middle-income countries on the CGD podcast).

“Building resilience” means losing some of the benefits of global value chains

A longer-term concern is how the decline in economic and political cooperation is forcing firms and countries to build resilience and redundancy into supply chains at high cost. It’s not mainly the cost of extra storage capacity or of choosing a more expensive, closer supplier, though both are high. The larger, but harder-to-quantify, cost is the loss of economic dynamism that comes from the hyper-integrated world of global value chains (GVCs).

GVCs allow production to be divided into many small tasks, with the most efficient country and firm selected for each mini part of the process. GVCs allow low- and middle-income countries (LMICs) to take a piece of a production process they are good at and capture the productivity learning gains from being part of international trade, even when they are not yet competitive at the full product. But this rests on reliable rules and political stability. One way to assess the long-term economic damage of “building resilience and redundancy” is the World Bank’s 2020 estimates of the benefits of tighter integration into GVCs. This suggests that a 1 percent increase in participation in GVCs increased GDP per capita by over 1 percent. Firms in GVCs employ more women, and regions within countries with higher shares of GVCs saw bigger reductions in poverty.

So where were the rays of hope?

The IMF, after weeks of being remarkably quiet about its response to the Iran war, signaled that it expects to extend $20 billion to $50 billion in lending to those impacted.

Coalitions of the concerned are discussing practical ways to respond to a changed world:

1. Debt suspension clauses that respond to objective triggers. Many have focused on climate-specific suspension clauses, but climate shocks turn out to be less frequent than other shocks, so it's better to have clauses that cover all large shocks. A simple quantitative benchmark—like negative growth—could provide substantially more liquidity to countries in need than borrowing from international financial institutions. For example, Hurricane Melissa caused $8.8 billion in damage in Jamaica in 2025. The country got $150 million from the payout of its catastrophe bond and $415 million from IMF emergency lending. Temporary suspension of its Eurobond and multilateral development bank (MDB) debt service would have freed up $1.1 billion. See the proposal here, and watch Carmen Reinhart and others discuss it here.

Figure 1. Frequency of large exogenous shocks in LICs and LMICs (2000-2024)

Source: EM-DAT; UCDP; World Bank, WDI.

Note: The number to the right of each bar indicates the average share of years in which the countries in our sample were affected by the given shock. Our sample consists of 79 LICs and LMICs.

Definitions: Exogenous shocks are those not driven by domestically determined economic or financial policies. A country was considered a LIC or LMIC if it fell into either category for at least twelve years over the period. Conflicts are defined as years with more than 1,000 conflict-related deaths. Terms of trade shocks are defined as declines in the terms of trade index two standard deviations below the median. The terms of trade index is defined as the ratio of the import value index to the export value index. Non-COVID epidemics are defined as epidemic disease events for which states of emergency were declared. Climate-related disasters and earthquakes/tsunamis are defined as such events with more than $1 million in associated damages. Climate-related disasters include droughts, extreme temperatures, floods, storms, and wildfires.

2. MDBs taking a more central role in financing health in low- and middle-income countries. With grant aid for health declining, there is a need to finance the emerging gaps and focus grant aid where it is most needed (much of it currently goes to middle-income countries). MDBs are well placed to provide loans for this purpose. Representatives from middle-income countries also argued at a private CGD roundtable that MDBs should give them greater control over funding and that MDB loans should go through country systems, not parallel systems. MDBs seem open to this move, although there was discussion about different options on how to do this, including joint work between MDBs and vertical funds, or a special subsidized health window at MDBs.

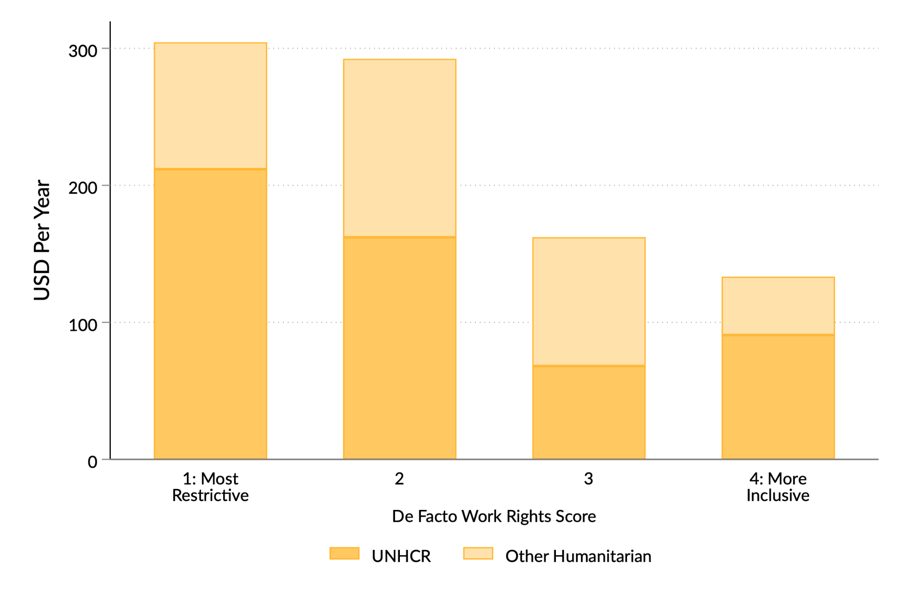

3. Changing how we finance refugees in LMICs. Refugee camps are terrible for refugees, who value work; host countries, who lose out on the innovation and productivity of refugees; and donors, who cover the basic needs of people who can and want to work. The World Bank refugee window in IDA means countries receive additional IDA money for refugee-related projects in exchange for policies that integrate refugees into the local economy, schools, and health care system. There was wide acceptance from donors and hosting countries that this is the way to go. However, the World Bank needs to push harder on linking payments under the window to policy. Too many countries have been rewarded for plans rather than action: as my colleagues Helen Dempster and Thomas Ginn point out, the countries with the most restrictive right-to-work laws receive the most funding per refugee.

Figure 2. Average humanitarian aid per refugee (USD), 2020–2021

Source: Ginn et al. (2025). Data sources are UNHCR Budget and Expenditure Dashboard (see https://reporting.unhcr.org/ dashboards/budget-and-expenditure); OECD (2023) UNHCR Refugee Data Finder (see https://www.unhcr.org/refugeestatistics/download); and Ginn et al. (2022)

4. More information on returns in LMICs. There seemed to be real momentum towards the private sector providing (anonymized) data on the returns to their investments in LMICs via the Emerging Market and Developing Economies Investor Task Force. Reducing the cost of acquiring information about new markets and reducing asymmetric information can reduce borrowing costs. I found greater transparency in sovereign bond markets reduced borrowing costs by 11 percent, while S&P used new data on MDB sovereign lending (GEMs) to conclude MDBs could deploy an additional $600–800 billion in lending capacity over the next decade without jeopardizing their ratings.

This is just a sample of the positive, practical work going on in global development. Of course, there are challenges ahead, but the Spring Meetings were an opportunity for people from around the world to brainstorm practical ways forward, including through groups like the Future of Development Cooperation Coalition.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: Paul Blake / World Bank