Recommended

Project

Mobile phones are ubiquitous in today’s world. Consumers can now tap their phones, or even scan their palms, to pay for goods and services. This seamless access to financial services is increasingly common in advanced economies. While some emerging and developing countries have made impressive strides in digital financial inclusion, many still lag behind. Millions continue to face significant barriers to using digital payments, limiting their ability to make safe transactions, save securely, and access credit.

There are many possible reasons for this lack of inclusion, so a key challenge is identifying which constraints matter most. What are the binding constraints that policymakers need to prioritize in their financial inclusion strategies? Without adequate prioritization, scarce resources risk being spent on dealing with secondary problems—delivering little impact unless more fundamental issues are addressed first.

What is needed then is a clear diagnostic tool to help uncover the root causes of exclusion. That’s precisely the problem that the Decision Tree framework and a new online course aim to solve.

The Decision Tree for Improving Digital Financial Inclusion

The Decision Tree provides a structured, step-by-step method for identifying the truly binding constraints to digital financial inclusion. Think of it as a diagnostic tool: users begin with the question “Why aren’t large segments of the population using digital payments?” and work through a series of hypotheses, supported by data and contextual insights.

Using a top-down approach, the framework systematically explores the potential causes of limited inclusion, starting from broad categories and drilling down to more specific explanations. Each of the potential cause—represented by a “branch on the tree”—can itself be broken down into further sub-causes.

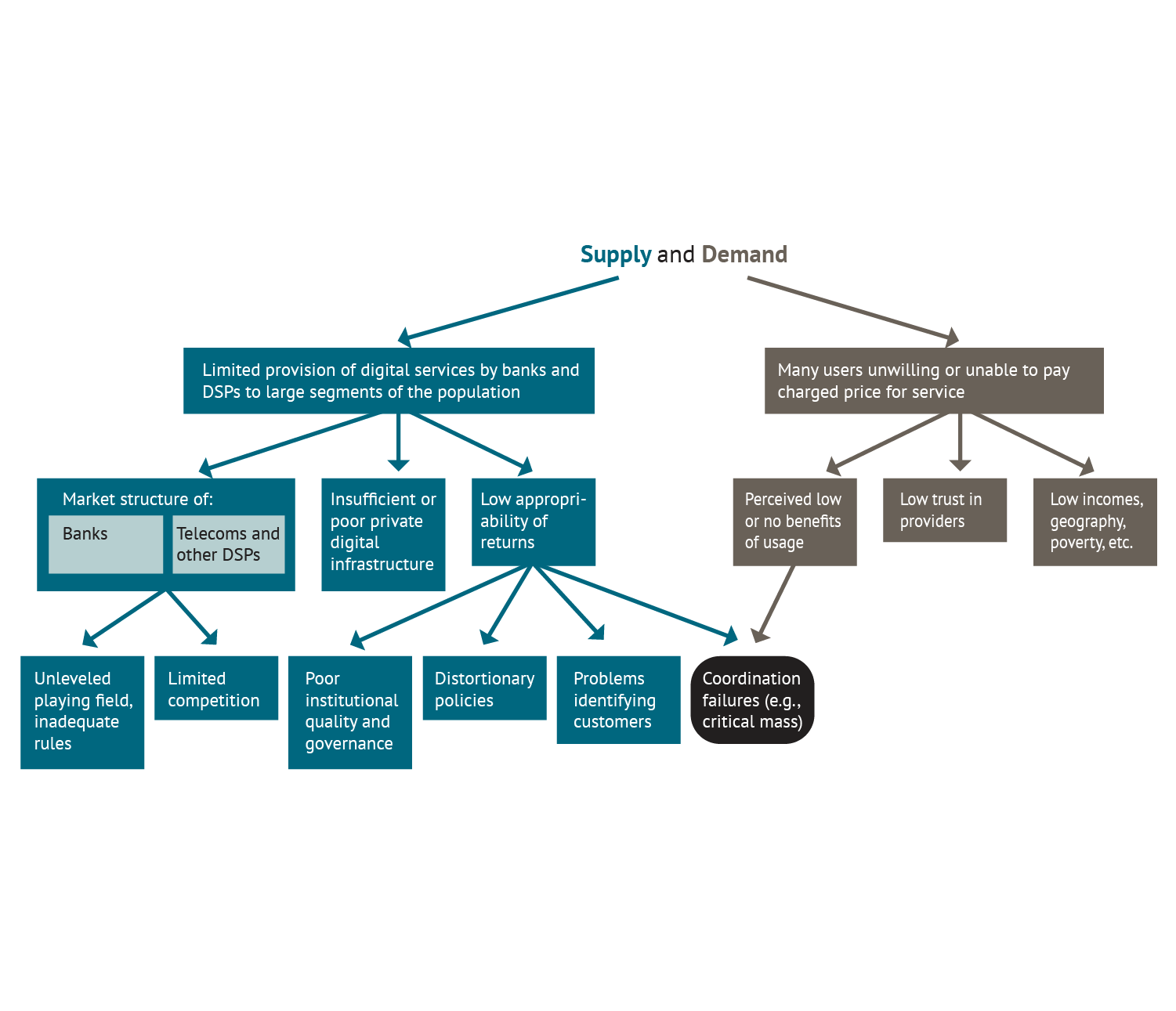

Figure 1. The Decision Tree for Digital Payment Services

Constraints are broadly divided between supply-side and demand-side factors:

- Supply-side issues relate to financial service providers—for instance, challenges stemming from market structure or limited digital infrastructure.

- Demand-side issues include users’ perceptions of low benefit, low trust in providers, or living far away from providers.

Each constraint, in turn, may have deeper roots. For example, insufficient market competition could arise from restrictive regulations or market dominance by a few players. Low perceived benefits might be linked to digital illiteracy or social norms, such as those limiting women’s use of financial services.

To help identify which constraints are binding, the methodology uses key guiding principles. One such principle involves examining the fees charged for using financial services. If fees are unusually high—either compared to similar services or relative to those in countries at similar development levels—it likely indicates that the root cause of the problem is on the supply side. Additional principles help assess each branch of the Tree to determine whether it may represent a binding constraint.

Application of the Decision Tree: case studies

The Decision Tree framework was piloted in five countries: Ethiopia, India, Indonesia, Mexico, and Pakistan. Collectively, these nations have nearly one billion adults who are not using digital financial services. While each country revealed its own unique binding constraint, some common patterns also emerged.

For example, in both India and Ethiopia, institutional reluctance to address market competition was identified as a major barrier. Yet context-specific challenges also played a role in affecting marginalized groups: India’s efforts were hindered by gender norms limiting women’s financial participation, while Ethiopia faced low awareness of digital financial services in rural areas.

These case studies highlight the Decision Tree’s ability to uncover both shared and context-specific barriers, making it a versatile diagnostic tool for policymakers.

A new tool to deepen financial inclusion

To make this framework more accessible, we are launching a new, free, online self-paced course: “A Decision Tree for Financial Inclusion Policymaking: An Application to Digital Payments.”

This course brings the methodology to a global audience, far beyond the reach of in-person workshops or technical assistance. It’s open to all and requires no prior background in economics or data science. Designed for policymakers, graduate students, and practitioners, the course includes short, structured lessons, optional data exercises, and real-world application guides. Participants are guided through a logical, evidence-based process to understand and respond to the most pressing barriers to digital financial inclusion.

To support hands-on learning, the course includes recent data on digital financial inclusion, financial service pricing, service coverage, market competition, user sentiment, financial literacy, social norms, and many other key variables both from the demand and the supply side of the Decision Tree. Users can work with data from their own country or another of their choosing, engaging in exercises that demonstrate how the data flows through the Decision Tree process and help reveal the binding constraints of their case study.

How to get started

Enrollment is simple—the course is hosted by the Center for Global Development and open to anyone. As part of CGD’s commitment to broad dissemination, the course will be shared over the coming months through events and blogs hosted by organizations, such as CGAP’s FinDev Gateway, the Alliance for Financial Inclusion and the Fletcher Leadership Program for Financial Inclusion (FLPFI). These collaborations will help broaden the course’s reach across policy, development, and academic communities.

As digital financial systems continue to expand, tools like the Decision Tree—and the knowledge to use them—are more critical than ever. By helping avoid both oversimplification and inaction, this tool ensures that focus and resources are directed where they are needed most. We hope this course becomes a go-to resource for all those committed to driving evidence-based, inclusive financial reform.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: Confidence/ Adobe Stock