For the world’s middle-income countries, the changes unleashed by automation, digital technologies, and the advent of increasingly more capable AI pose major challenges. They threaten to upend the few tried and tested development strategies.

I. The canonical development model is ageing fast

The majority of emerging economies have embraced urban industrialization to promote economic growth. The most successful among the middle-income countries are ones that rapidly deepened manufacturing capabilities, were able to participate in global value chains, and steadily increased their penetration of overseas markets. Among the successful exceptions are exporters of minerals or other resource based products and small economies that have relied on the export of services, primarily tourism. The common thread running through the strategies of all fast developers is structural change that led to the emergence and growth of more productive, export oriented sectors producing manufactures or resource-based products or services, or a combination of the three. Complementing this structural change was rising demand for emerging economy exports from advanced economies. Rapid growth was undoubtedly enabled by sound policies and strategic vision, however the fast movers were also advantaged by lower factor costs, the capacity to assimilate technologies, and by investment in both productive assets and supporting infrastructures. Globalization in its several forms lent added impetus to development underpinned by trade and technology transfers.

A half-century of unprecedented global growth starting in the mid 1960s entered the doldrums following the financial crisis of 2008. Growth of trade and GDP slowed after the financial crisis of 2008-09, and a few emerging economies worry that they may be in the grip of a middle-income trap. Reviving growth is the priority[1] but two significant developments argue for a recasting of past growth strategies. One is the likely secular decline in the increase in global trade—merchandise trade contracted by 10 percent between 2011 and 2015[2] (Timmer et al 2016; Auboin and Borino 2017; Constantinescu et al 2015; Hoekman 2015). The second, and arguably a more serious development with profound longer-term implications, is technological change that is capital and skill intensive, labor displacing, and could largely erode the (labor and land based) cost competitiveness that has powered the growth of emerging economies—unless they are quick to assimilate new technologies and raise productivity. The skill, capital intensity, and complexity of digital technologies that favor advanced economies and the likelihood that they will lead to a telescoping of global value chains are the worrisome problem for emerging economies; but digital technology and automation could also be a boon for all countries as they could lead to gains in productivity that is ultimately the driver of growth.[3]

The balance of this note briefly sketches the likely implications of the so-called fourth industrial revolution for emerging economies and for their development strategies.

II. Disruptors at the door

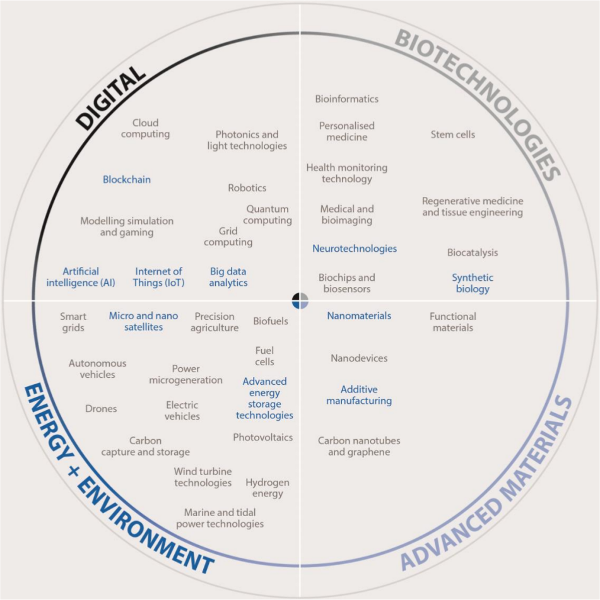

A host of technologies divided into four categories threaten to disrupt and reshape growth strategies for emerging economies. According to a convenient categorization by the OECD these are: digital, biotechnology, advanced materials, and energy and environment. See figure 1.

Figure 1: Frontier technologies

Technologies that could cause the most disruption by narrowing some opportunities for emerging economies while also opening alternative avenues for development are: (i) robotics and the automation not only of repetitive manual tasks but also of cognitively more demanding tasks with the help of intelligent/learning software systems capable of performing knowledge work of increasing sophistication;[4] (ii) additive (3D) manufacturing that permits rapid prototyping, as well as small lot, resource conserving, customized, and dispersed production; (iii) the industrial internet of things that will further reduce the labor intensity of production, monitoring, and maintenance and multiply the numbers of “lights out” factories and warehouses;[5] (iv) the mobile Internet and increased connectivity that will permit the use of mobile devices to access a wide range of banking, transport, medical, and other services; (v) Big Data and advanced data analytics; and (vi) cloud technology that delivers hardware and software over the Internet as a service (SAAS), a platform (PAAS) or an infrastructure as a service (IAAS).[6]

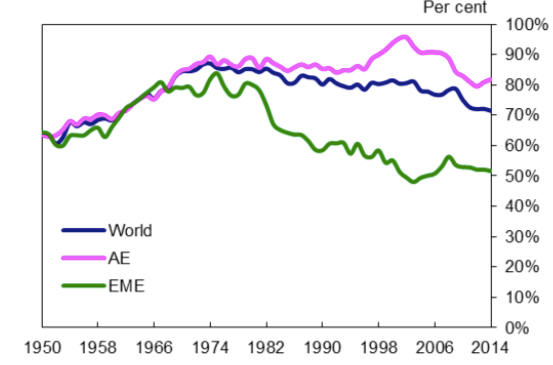

These and other technologies already making inroads are being refined and extended largely by advanced economies and are attuned to their factor endowments and capabilities. They reinforce the comparative advantage of high-income countries in manufacturing and services for which demand will be rising. The new technologies could widen the divergence in technologies and in productivity between the advanced and emerging economies (Haldane 2017, figure 2). In fact, emerging economies are threatened by a perfect storm unless they come to grips with the new technological realities, adjust policies, upgrade human capital, and adapt institutions.[7]

Figure 2: Productivity level relative to the United States by region

III. Will there be new jobs or no jobs?

There are those who believe that technological change will be a gradual process as in the past allowing institutions and labor markets ample time to adjust. The optimists are of the view that although automation, AI, and other technologies that are in the wings will in time eliminate a swathe of jobs, the pace of automation is likely to be slow and new occupations will appear to take the place of the ones that disappear as was the case in the past—assuming of course that economic growth is robust.[8] Past industrial revolutions gave rise to similar fears that proved to be unfounded (Pew Research 2014; Brynjolfsson and McAfee 2016; 2017).[9]

Could it be different this time around? Those who subscribe to the precautionary principle maintain that the pace of technological change has quickened making it harder for markets and institutions to make timely adjustments.[10] The better-paid jobs that might materialize will require higher levels of cognitive, non-cognitive, and technical skills that are not plentiful in emerging economies and will accumulate slowly.[11] Many emerging economies are currently coping with a large overhang of unemployed and underemployed workers and urgently need to ramp up employment in manufacturing and tradable services. With the share of manufacturing in GDP and in employment already trending lower, technological change that is labor displacing and constrains the growth of exports could worsen economic and social pressures in some countries.

The experience of India and other middle-income economies indicates that tradable services—the ones that drive growth—are unlikely to generate a sufficient number of “good” jobs to replace the ones lost by manufacturing or that are not being created by manufacturing industries as was the case in the past.[12] The jobs drought will only worsen if AI winnows a wide range of the routine white-collar occupations.[13] Jobless growth is already a specter haunting advanced economies. A frequently cited study by Frey and Osborne (2013)[14] found that 47 percent of all jobs in the United States could be eliminated by computerization and intelligent digital technologies.[15] Many more are at risk in the OECD and developing countries according to the World Bank (2016): 57 percent in the OECD; 69 percent in India; 72 percent in Thailand; 77 percent in China; and a massive 85 percent in Ethiopia.[16] Southeast Asia will experience a similar culling of jobs. On applying Frey and Osborne’s methodology to the data for five ASEAN countries, the ILO (2016) determined that 56 percent of current jobs were in jeopardy over the course of two decades. The hospitality sector, retail and wholesale trades, construction and manufacturing were the ones most susceptible to automation. Garment workers in Cambodia, office clerks in Indonesia, and shop assistants in Thailand were all likely to be out competed by the creations of digital technologies.

The jobs at risk span a wide spectrum of activities in the formal sector of the economy.[17] McKinsey Global Institute (2017)[18] estimates that the likelihood of jobs being automated away is greatest in accommodation and food services (73 percent)[19] followed by manufacturing,[20] agriculture, transportation and storage, wholesale and retail trade, and mining (51 percent).[21] The activities least threatened by automation are education (27 percent), management, professional services, information, healthcare, and administration (39 percent) in that order. But even these are not immune. The scope for substituting online and distance education for traditional teacher and classroom-based education are increasing by the day. Smart programs and AI are encroaching on professional services such as legal,[22] accounting, real estate, HR, architectural, and engineering. Healthcare is a candidate for disruption by cognitive computerized systems such as Watson, by mobile devices and numerous apps (West 2012), by implants and sensors that can be monitored by computers at a distance, and eventually by hospital based carebots currently being tested in Japan.[23] Digital technologies could also substantially reduce the administrative costs of healthcare in the process eliminating a large number of clerical jobs (Beisdorf and Niederman 2014).

The digital transformation of government that is a major employer in many countries is already ongoing and with ever widening scope for e-governance that increases transparency, simplifies and streamlines regulations, and facilitates reporting, registration, licensing, and filing. In most emerging economies the digital transformation of government is at an early stage with much ground still to cover (Deloitte 2016).[24] Once governance becomes digitally mature, productivity and efficiency will increase, but many jobs will fall by the wayside.[25] India, which is still a long way from digital maturity, is a case in point. There were 19.5 million government jobs in 1996–7; by 2015–16 the number had shrunk to 17 million (Jaffrelot 2016). In most Middle Eastern countries, the public sector provides between 40 and 90 percent of the formal employment. E-government complemented by the desirable pruning of regulations and organizational restructuring would substantially enhance efficiency but it would also render more than half the workforce redundant.

The “autonomous economy” where digital processes talk to other digital processes and create new digital processes all without human intervention, as envisaged by Brian Arthur, is a distant prospect. AI is in the early adolescent stage but few computer scientists engaged in its development doubt that within a few decades it will penetrate every corner of the economy. When it does, the implications especially for jobs, will be far-reaching. Meanwhile, automation is diffusing inexorably through industry and extending its reach into services. Digital products and services are proliferating and as more people acquire smartphones[26] and gain access to the Internet,[27] production and consumption activities are all affected.

IV. Deconstructing the old and crafting a more relevant strategy

How this will play out for emerging economies is uncertain. What does appear indisputable is the need to rethink development strategy for emerging economies. This includes industrialized ones that have relied on the exports of manufactures and participation in global value chains—i.e. the Malaysias, Polands, and Thailands—as well as other economies—the Pakistans, Egypts, and Honduras—that are at earlier stages of industrialization and may need to chart a different course exporting a mix of services, agricultural products plus a few niche manufactures.[28] All emerging economies irrespective of where they are on the industrial scale will need to transition to strategies less reliant on manufacturing and exports for their growth and employment. Services are the dominant sector everywhere; now services (or in some cases agriculture and agroindustry) must drive growth with gains in productivity providing a major push and domestic consumption exerting more of the pull. All will need to harness the new technologies. The ones that are slow to do so will be left behind. And as they embrace the technologies, they must come to terms with the consequences for employment and income distribution. The simple export oriented industrialization recipe that was the staple of the latter two decades of the 20th century will no longer suffice. Development strategy will be a lot more complex and multi stranded with politics strongly influencing economic and technological decision-making.

Below are some of the factors that need to inform strategies for emerging economies. One size will not fit all; each will need to customize strategy. And there is no guarantee that growth will return to the trend rates of the 1990s and early 2000s.

- Rapid structural change that transfers labor from agriculture to the urban sector might not provide a productivity boost if most workers end up in unproductive informal jobs as is happening in most African, South Asian, and Central American economies. Furthermore, urban sprawl, congestion, informalization, and pressure on urban services could erode the productivity benefits accruing from agglomeration economies. Should structural change and urbanization be tempered by policy?

- For some countries e.g. in Central America and SSA, modernizing agriculture and developing agro industries with supporting physical, financial, extension, and research infrastructures might offer better growth prospects. Digital technologies/automation can usher in an agricultural revolution.[29]

- Manufacturing will remain a driver of growth for a few countries but for the majority it will be a minimal source of growth, of jobs, of exports. As Rodrik (2015) and others have pointed out, the industrializing trend has gone into reverse. Most emerging economies are unlikely to see the share of manufacturing in GDP pass the 15 percent mark. However, because of advances in technology, manufacturing can potentially deliver large gains in productivity. This is not evident as yet but may come. Should industrial policies deserve the attention they are receiving e.g. “Make in India,” “Made in China 2025”?

- If manufacturing takes a back seat, this will affect the composition and growth of exports from emerging economies. Export led growth of the sort that created the East Asian legend of the 20th century could be a thing of the past. If small and mid-sized economies are to ride the export escalator, they will need to rely more on the export of services, or of people—a safety valve of long standing for many countries.[30] What sort of tradable services can substitute for manufactures and generate the local employment multiplier effects?

- Slow growth of merchandise trade and higher entry barriers into tradable industries for emerging economies, and a persistence of sluggish increases in productivity (TFP)[31] could result in lower rates of GDP growth on average. Success might depend upon sustaining 1–2 percent rates of per capita growth and avoiding spells of negative growth. That is how the most of the advanced economies entered the high-income club. Will this suffice? Will it be politically palatable? How reliable are forecasts of TFP based on past trends?[32] The Chinese seem unable to settle for less than 6.5 percent per annum. Can they reverse or stabilize the slide in productivity growth since the turn of the century?

- At these rates of growth, urban unemployment and underemployment will be the dominant economic and social problem exacerbated by large cohorts of working age adults, and by technological change that steadily displaces the unskilled and those doing routine work that machines can do more effectively and cheaply.

- Managing population growth will be a priority for many Asian and African nations. Can such policies be implemented in countries that most need them? Some others where the fertility rates are dipping below replacement levels need to prepare for a shrinking of the workforce and rising dependency rates. For these countries, automation will be a way of sidestepping labor shortages.

- Emerging economies particularly in parts of Asia, the Middle East and Africa will be confronted with water scarcity and water shortages that will impact agricultural, industrial and energy production. Higher temperatures will also reduce the productivity of labor and land. Technology and electrification can ease the constraints imposed by warming and water shortages but they and pricing policies must be part and parcel of a strategy that also “greens” development.

- Growth will be led by services and/or resource based activities. This will be a big change as in the past it always involved industrialization. Industry was a source of jobs, innovation, exports, and productivity gains. It helped build the middle class. Manufacturing generated demand for many intermediate services e.g. finance, logistics, legal, engineering, insurance, and research. The new model of development will need to identify a prime mover to replace manufacturing. Are such new leading sectors beginning to surface in emerging economies?

- Improving the quality of education and developing skills for which there is a demand will be an even higher priority, except that it is a slow process dependent upon the recruiting of talented teachers and better coordination between employers and training institutions. Forecasting the demand for skills is tricky. If AI, automation, and wide spectrum digital technologies do take off, the number of highly skilled workers that will be needed might be relatively small.[33] The jobless growth in India and elsewhere could be a leading indicator of what is to come. Should EMEs more actively pursue manpower, VTEC, and lifelong learning policies? Will these pay off?

- Irrespective of what governments do, urbanization will continue (although it could be slowed). This structural change will increase the demand for the financing and funding of infrastructure and public services. Crowded cities with large numbers of unemployed people will be highly combustible. Managing urban populations, and urban access so as to maintain a degree of peace and harmony using “smart city” technologies some that the Chinese are pioneering might be intrinsic to sound development strategy. How would that effect individual rights, freedoms and privacy?

- A larger redistributive and (welfare) services providing role for governments is in the cards, absent the emergence of an effective, decentralized redistributive process.[34] Recent trends that could be reinforced by new technologies suggest that a concentration of income and wealth might continue with the share of labor declining further.[35] Slower growth will make it even more urgent to put in place mechanisms for sharing of work and income. The quality of governance and the capacity to raise and allocate revenues will take on greater salience. How ready are governments to use digital technologies for these purposes?

- One factor that carries over forcefully from earlier growth strategies is the level of gross domestic investment and national savings. Emerging economies will need to maintain rates of saving and investment in the high 20s (as percent of GDP) if they are to harness new technologies, develop productive activities and infrastructure, and sustain moderate rates of inclusive growth. In many of the EMEs, GDI/GDS are too low given the needs. Can they be raised and resources allocated more efficiently?

V. Concluding observations

Accelerating growth in EMEs was never easy. New technologies that potentially raise productivity might not make it easier to meet growth and inclusive development targets. AI, automation, digital, and bio technologies have the makings of a revolution but they have yet to demonstrate that they can improve growth performance and give rise to a multitude of jobs that will thicken the ranks of the middle class.[36]

Two decades of experience may be insufficient and deceptive, however what we are witnessing is the inability of labor markets in particular to adjust to rapid change—for many workers with only high school education or less acquiring the skills needed to work with smart machines or to compete for the occupations spawned by automation is a stretch. Moreover, governments are finding it difficult to chart out more viable development strategies to replace the ones that are of diminishing relevance. Too many remain wedded to the earlier manufacturing-led growth model. Meanwhile, income inequality appears to be worsening in many EMEs and populations are becoming increasingly restive and dissatisfied. The turn towards an inchoate populism is a symptom of slowing growth, narrowing job opportunities, and the inability of governments to define and implement remedial policies.

EMEs need a new strategy that takes account of the factors listed above. It needs to be based on a critical appreciation of the political economy of the development process that is being altered by technological change and also by demographic pressures, by global warming, and by urban populations empowered through their access to the Internet and to mobile telecommunications.

Notes

[1] The global growth forecast for 2017 is 3.5 percent increasing to 3.6 percent by 2018. IMF(2017) https://www.imf.org/en/Publications/WEO/Issues/2017/07/07/world-economic-outlook-update-july-2017

[2] World trade is increasing annually by less than 4 percent a far cry from the 6–7 percent rates registered during 1990–2008. Capital flows have also declined from $11.9 trillion in 2007 to $3.3 trillion in 2015. Steil and Smith (2017).

[3] Digital technologies have the potential to raise productivity but they have yet to deliver. Total factor productivity has slowed worldwide with virtually all sectors affected most notably the producers of ICT equipment and the most intensive users of ICT. Acemoglu et al (2014); See for instance Conference Board (2017) https://www.conference-board.org/data/economydatabase/. As with electricity and the internal combustion engine, the adoption of technology requires parallel adjustments in organizations, work practices, logistic, and value chains al of which takes time. It is apparent from the data that a small number of superstar firms have embraced digital technologies and are exploiting AI and Big Data but the majority—70 percent or more—are lagging behind, which may explain why productivity gains are so meager. The rise of superstar firms also might account for the decline in the share of labor in GDP. (Autor et al 2017).

[4] Stuart Armstrong (2014, pp.14-15) observes that computers far exceed human capacity in an increasing number of areas because of focus, patience, processing speed, and memory. “In 2009, a robot named Adam became the first machine to formulate scientific hypotheses and propose tests for them- and it was able to conduct experiments whose results may have answered a long standing question in genetics… An AI that became adequate at technological development would soon become phenomenally good: unlike humans, the AI could integrate and analyze data from across the whole Internet. It would do R&D simultaneously in hundreds of subfields and relentlessly combine ideas among fields.” Nick Bostrom (2014), Stephen Hawking and Max Tegmark among others are of the view that super intelligent machines are a distinct possibility before the end of the century. For Tegmark (2014) a physicist, “intelligence is just a form of information processing by elementary particles moving around. There is no law of physics that says we cannot build machines more intelligent than us in al ways.” The AI cognoscenti are generally upbeat with some voices urging caution. https://futureoflife.org/2016/01/12/the-future-of-ai-quotes-and-highlights-from-todays-nyu-symposium/; https://futureoflife.org/2017/06/26/using-history-to-chart-the-future-of-ai-an-interview-with-katja-grace/; https://www.theverge.com/2017/8/29/16219754/max-tegmark-life-book-artificial-intelligence-superintelligence-existential-risk

[5] Until recently, jobs lost in retailing were being offset by increased employment in warehouses established by companies selling online. But as online businesses are less labor intensive than bricks and mortar stores and warehouse based fulfillment centers are becoming more automated, it is unlikely that a continuing decline in retail jobs will be made good by online commerce. (Thompson 2017). Amazon’s warehouse robots take a fraction of the space required by humans and can pick and pack an order in a fourth of the time.

[6] See McKinsey Global Institute (2013) http://www.mckinsey.com/business-functions/digital-mckinsey/our-insights/disruptive-technologies; Cloud computing can facilitate design, prototyping and fabrication. Moreover, it enables firms to make use of 3D manufacturing the IoT, and industrial robots. It can be tailored for firms of all sizes and lowers the entry barriers for firms because it is scalable, obviates the need to purchase expensive equipment and software and provides data security. Ezell and Swanson (2017).

[7] In their recent publication, McAfee and Brynjolfsson (2017, p.24) examine the implications for the business world and the risks for those companies that do not “bring together minds and machines, products and platforms and the core and crowd” in innovative ways.

[8] Atkinson (2017) is among the more optimistic. He cites estimates by ITIF suggesting that just 8 percent of jobs are at high risk of automation while 33 percent are at moderately high risk. The high-risk occupations include automotive workers, tellers, couriers, credit analysts, loading machine operators, farm laborers and others. In the moderate risk category are textile and construction workers and workers manning a variety of machines. https://itif.org/publications/2017/08/07/unfortunately-technology-will-not-eliminate-many-jobs

[10] “Whereas it took on average 119 years for the spindle to diffuse outside of Europe, the Internet spread across the globe in only 7 years. Going forward, as argued in the Citi GPS Disruptive Innovations III report, the cost of innovation continues to fall as cheaper smartphones will help bring 4 billion more people online. The next stage of connectivity will move from people to 'things' with Cisco estimating 500 billion devices will be connected by 2030, up from 13 billion in 2013. Increasing digital connectivity is fuelling a data boom, with data volume estimated to be doubling every 18 months, and computers are likely far better able to handle this volume than people.” Oxford Martin School (2016).

[11] Tyler Cowen (2013) maintains that only those with above average skills and capabilities soft and technical will thrive in the brave new world of AI and digital technologies. The rest will have to eke out a meager living lower down the food chain. How plentiful these new high-end jobs might be is open to question. According to a report by the Oxford Martin School (2016), “A downward trend in new job creation in new technology industries is particularly evident starting in the Computer Revolution of the 1980s. For example, about 8.2% of the US workforce shifted into new jobs during the 1980s, which were associated with new technologies; during the 1990s this figure declined to 4.4%. Estimates by Thor Berger and Carl Benedikt Frey further suggest that less than 0.5% of the US workforce shifted into technology industries that emerged throughout the 2000s, including new industries such as online auctions, video and audio streaming, and web design.”

[12] Growth in Nigeria has been equally jobless. In spite of growth rates averaging close to 6 percent per annum between 2009 and 2014, unemployment increased from 23.9 percent in 2011 to 25.1 percent in 2014. WDI http://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?locations=NG; Golubski (2016) https://www.brookings.edu/blog/africa-in-focus/2016/05/05/african-lions-nigerias-jobless-growth/

[13] Vijay Joshi (2017) writes that in the 10 years from 1999 to 2009, India’s workforce increased by 63m. “Of these, 44 million joined the unorganized sector, 22 million became informal workers in the organized sector, and the number of formal workers in the organized sector fell by 3 million.” See also Mitra (2017); Tejani (2016); Arya (2017); Jaffrelot (2016); Hindustan Times (2017) http://www.hindustantimes.com/editorials/jobless-growth-can-lead-to-social-unrest-india-must-be-careful/story-RbJyBYDeRK8oCMp9qk71DP.html. Mohan and Madgavkar (2017) find that the net increase in employment between 2011 and 2015 was 7 million—agriculture shed 26 million workers and 33 million jobs were created mainly by construction, transport, and commercial activities. Statistics released by India’s Labor Bureau showed that India created 135,000 jobs in 2015 as against 900,000 in 2011. With 550 jobs being lost each day, the Bureau projects that India will have 7 million fewer jobs whereas the population would have risen by 600 million. http://www.business-standard.com/article/current-affairs/7-million-jobs-can-disappear-by-2050-says-a-study-116101600378_1.html. Another 1.5 million jobs were lost in the first four months of 2017. http://www.business-standard.com/article/opinion/1-5-million-jobs-lost-in-first-four-months-of-2017-117071000571_1.html

[15] PwC (2017) arrived at a less forbidding forecast for the UK: 30 percent of jobs are susceptible to automation by the early 2030s. Forty six percent of workers with only high school diplomas could be replaced by robots but only 12 percent with undergraduate degrees. https://www.pwc.co.uk/economic-services/ukeo/pwcukeo-section-4-automation-march-2017-v2.pdf

[16] World Development Report (2016).

[17] A study by Acemoglu and Restrepo (2017) on the impact of industrial robots on employment and wages in the U.S. between 1990 and 2007 concluded that adding one robot reduced employment by 5.6 workers (0.34 percent) and wages by 0.5 percent. Thus far, the number of jobs lost to robots ranges from 360,000 to 670,000. However, if the number were to quadruple by 2025, the employment to population ratio would drop by between 0.94 percent and 1.76 percent.

[18] http://www.mckinsey.com/global-themes/employment-and-growth/automation-jobs-and-the-future-of-work; Another MGI study (Manyika 2017) concludes that close to a third of all activities in 60 percent of occupations worldwide could be automated. That encompasses one half of global GDP and puts 1.2 billion workers at risk from existing technology.

[19] Self-service kiosks are becoming more common in restaurants and in time could become the norm.

[20] In the United States for example manufacturing output has risen by 10-20 percent but jobs by only 2 to 5 percent. At this rate, Larry Summers believes that in a generation from now a quarter of all middle aged men will be out of work at any one time. http://www.businessinsider.com/larry-summers-a-third-of-men-aged-25-54-will-be-out-of-work-by-2050-2016-9 West (2016) https://www.brookings.edu/blog/techtank/2016/06/02/how-technology-is-changing-manufacturing/

[21] Open cast mines in Chile and Australia are being rapidly automated with remotely controlled self- driving trucks a commonplace.

[22] A report by Deloitte (2016) indicated that smart machines could imperil 114,000 jobs in the legal profession (39 percent of the total) within the next decade. https://www.legaltechnology.com/latest-news/deloitte-insight-100000-legal-roles-to-be-automated/

[23] http://www.japantimes.co.jp/news/2017/05/18/national/science-health/japans-nursing-facilities-using-humanoid-robots-improve-lives-safety-elderly/#.WVLU_zOZO8U; http://www.businessinsider.com/japan-developing-carebots-for-elderly-care-2015-11

[24] https://dupress.deloitte.com/content/dam/dup-us-en/articles/digital-transformation-in-government/DUP_1081_Journey-to-govt-digital-future_MASTER.pdf

[25] Hanna (2017) shows how both public services and governance could absorb and benefit from digital technologies.

[26] In ASEAN, smartphone penetration now exceeds 35 percent.

[27] Many activities are being conducted online including retailing and grocery shopping that is already impacting bricks and mortar establishments and will denude employment in conventional retailing.

[28] Then there are African economies such as Malawi largely agricultural that have barely alighted on the first rung of the industrial ladder.

[29] Farming 4.0 could be every bit as transformative as industry 4.0. http://www.cema-agri.org/page/‘farming-40’-farm-gates

[30] Migration in search of jobs has helped ease unemployment and provided countries in Central America, South Asia and Southeast Asia with a flow of remittances. In 2016, developing countries received $429 billion in the form of remittances. http://www.knomad.org/data/remittances. Tightening restrictions by advanced countries could reduce cross border migration in the medium term but push and pull pressures might make it difficult to enforce these over the longer term.

[31] The growth of total factor productivity has declined since 2008 not only in the U.S and European countries but also in emerging economies.

[32] A slowdown in U.S. productivity growth over the past decade and a half is unmistakable, however, Crafts and Mills (2017) maintain that it would be unwise to forecast future productivity growth based on an extrapolation of these trends as past projections using econometric estimates of TFP trends have been repeatedly off the mark.

[33] Beaudry et al (2013) point to the great reversal in demand for skilled workers—many of whom are engaged in tasks requiring fewer skills.

[34] Will universal basic income become the norm? See the Boston Review Forum (Spring 2017) http://bostonreview.net/forum-ii; and van Parijs and Vanderborght (2017).

[35] The decline is evident worldwide and not just in the U.S. Karabarbounis and Neiman (2013); Elsby, Hobijn and Sahin (2013).

[36] It should be remembered that thinking and theorizing on AI commenced in the early 1950s with the term being coined by John McCarthy at a famous conference held at Dartmouth College in 1956. The first industrial robot—the Unimate—was invented 1954 by George DeVol. It was subsequently modified and commercialized by Joseph Engleberger in 1960 (in collaboration with DeVol) who founded a company called Unimation. The first industrial robot was sold to GM in 1961.

References

Acemoglu, D., Autor, D., Dorn, D., Hanson, G.H., and Price, B., 2014. Return of the Solow Paradox? IT, Productivity, and Employment in U.S. Manufacturing. NBER Working Paper No.19837. Cambridge Mass. National Bureau of Economic Research.

Acemoglu, D., and Restrepo, P., 2017. Robots and Jobs: Evidence from U.S. Labor Markets. https://economics.mit.edu/files/12763; http://voxeu.org/article/robots-and-jobs-evidence-us

Armstrong, Stuart, 2014. Smarter than Us. MIRI.

Arya, N., 2017. How India can Reverse the Trend of Jobless Growth. http://www.huffingtonpost.in/neha-arya/how-india-can-reverse-the-trend-of-jobless-growth_a_21655166/

Auboin, M., and Borino, F., 2017. The Falling Elasticity of Global Trade to Economic Activity. VOX CEPR. http://voxeu.org/article/falling-elasticity-global-trade-economic-activity

Autor, D., Dorn, D. Katz, L.M., Patterson, C., and van Reenen, J., 2017. The Fall of the Labor Share and the Rise of Superstar Firms. NBER Working Paper No.23396. Cambridge Mass. National Bureau of Economic Research.

Beaudry, P., Green, D.A., and Sand, B.M., 2013. The Great Reversal in the Demand for Skill and Cognitive Tasks. NBER Working Paper No. 18901. Cambridge Mass. National Bureau of Economic Research.

Beisdorf, S., and Niederman, F., 2014. Healthcare’s Digital Future. McKinsey Global Institute. http://www.mckinsey.com/industries/healthcare-systems-and-services/our-insights/healthcares-digital-future

Bostrom, N., 2014. Superintelligence: Paths, Dangers and Strategies. New York. Oxford University Press.

Brynjolfsson, E., and McAfee, A. 2016. The Second Machine Age. New York. W.W. Norton.

Brynjolfsson, E., and McAfee, A., 2017. Machine, Platform, Crowd: Harnessing our digital future. New York. W.W. Norton.

Constantinescu, C., Mattoo, A., and Ruta, M., 2015. Why the Globat Trade Slowdown May Matter. VOX CEPR. http://voxeu.org/article/why-global-trade-slowdown-may-matter

Cowen, T., 2013. Average is Over. New York. Dutton.

Crafts, N, and Mills, T., 2017. Economic models vs. Techno-optimsm: Predicting medium term total factor productivity rates in the U.S. VOX CEPR. http://voxeu.org/article/slow-productivity-growth-may-not-be-new-normal-us

Elsby, M.W.L., Hobijn, B. and Sahin, A. 2013. The Decline of the U.S. Labor Share. Brookings Papers on Economic Activity, Fall 2013.

Ezell, S., and Swanson, B., 2017. How Cloud Computing Enables Modern Manufacturing. AEI/ITIF. http://www2.itif.org/2017-cloud-computing-enables-manufacturing.pdf?_ga=2.218587289.1802769062.1498483609-1058723113.1488819082

Frey, C. B., and Osborne, M. A., 2013. The Future of Employment: How Susceptible are jobs to Computerization. Oxford. Martin School. http://www.oxfordmartin.ox.ac.uk/downloads/academic/The_Future_of_Employment.pdf

Haldane, A., 2017. Productivity Puzzles. Bank of England. http://worldmanagementsurvey.org/wp-content/uploads/2017/03/boespeech_220317.pdf

Hanna, N, K., 2017. How Can Digital Technologies Improve Public Services and Governance? New York. Business Expert Press.

Hoekman, B., 2015. The Global Trade Slowdown: A new normal. VOX CEPR. http://voxeu.org/content/global-trade-slowdown-new-normal

International Labor Organization, 2016. ASEAN in Transformation. Geneva. http://www.ilo.org/public/english/dialogue/actemp/downloads/publications/2016/asean_in_transf_2016_r1_techn.pdf

Jaffrelot, C., 2016. India’s Jobless Growth is Undermining its Ability to Reap the Demographic Dividend. Carnegie Endowment. http://carnegieendowment.org/2016/04/29/india-s-jobless-growth-is-undermining-its-ability-to-reap-demographic-dividend-pub-63495

Joshi, Vijay, 2017. India’s Long Road. New York. Oxford University Press.

Karabarbounis, L., and Neiman, B., 2013. The Global Decline of the Labor Share. NBER Working Paper No. 19136. Cambridge Mass. National Bureau of Economic Research.

Manyika, J., 2017. Technology, Jobs and the Future of Work. McKinsey Global Institute. May. http://www.mckinsey.com/global-themes/employment-and-growth/technology-jobs-and-the-future-of-work

McAfee A, and Brynjolfsson, E., 2017. Machine, Platform, Crowd. New York. Norton.

Mitra, D., 2017. India on a Jobless Growth Path. Bloomberg. https://www.bloombergquint.com/union-budget-india/2017/01/11/india-on-a-jobless-growth-path

Mohan, R., and Madgavkar, A., 2017. The Changing Face of Work in India. Project Syndicate. https://www.project-syndicate.org/commentary/rebutting-india-jobless-growth-fears-by-rakesh-mohan-and-anu-madgavkar-2017-07

OECD, 2016. Science Technology and Innovation Outlook, 2016. Paris. http://www.oecd.org/sti/STIO%2010%20key%20technology%20trends%20for%20the%20future.pdf

Oxford Martin School. 2016. Technology at Work:v2.0. CitiGPS Global Perspectives and Solutions. http://www.oxfordmartin.ox.ac.uk/downloads/reports/Citi_GPS_Technology_Work_2.pdf

Rodrik, Dani, 2015. Premature Deindustrialization. NBER Working Paper No. 20935. Cambridge Mass. National Bureau of Economic Research.

Steil, B., and Smith, E., 2017. The Retreat of the Renminbi. Project Syndicate. June.

Tegmark, Max, 2014. Consciousness as a State of Matter. https://arxiv.org/pdf/1401.1219.pdf

Tejani, S., 2016. Jobless Growth in India: An investigation. Cambridge Journal of Economics. 40(3): 843-870.

Thomson, D., 2017. The Silent Crisis of Retail Employment. Atlantic. https://www.theatlantic.com/business/archive/2017/04/the-silent-crisis-of-retail-employment/523428/

Timmer, M., Los, B., Stehrer, R., De Vries, G., 2016. Production Fragmentation and the Global Trade Slowdown. VOX CEPR. http://voxeu.org/article/production-fragmentation-and-global-trade-slowdown

Van Parijs and Vanderborght, 2017. Basic Income: A radical Proposal for a Free Society and a Sane Economy. Cambridge Mass. Harvard University Press.

West, D, M., 2012. How Mobile Devices are Transforming Healthcare. Washington, DC. Brookings. https://www.brookings.edu/research/how-mobile-devices-are-transforming-healthcare/

West, D, M., 2016. How Technology is Changing Manufacturing. Washington, DC. Brookings. https://www.brookings.edu/blog/techtank/2016/06/02/how-technology-is-changing-manufacturing/

World Development Indicators, 2017. Washington, DC. World Bank. http://databank.worldbank.org/data/reports.aspx?source=world-development-indicators

World Development Report, 2016. Digital Dividends. Washington, DC. World Bank. http://www.worldbank.org/en/publication/wdr2016

Topics

CITATION

Yusuf, Shahid. 2017. Automation, AI, and the Emerging Economies. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.