Recommended

Blog Post

Is “Catch-up” Growth a Thing of the Past?

CGD NOTE

Another Take on Automation

Introduction

Now that computers are capable of taking the jobs that require brain as well as brawn, it may appear there is little left for humans to do. There are many scary forecasts of the capacity of automation and AI to replace a lot of workers very fast. Self-driving vehicles may wipe out opportunities for taxi drivers and truckers, for example. Brynjolfsson, Rock, and Syverson note there are 3.5 million people employed driving vehicles in the US. If automation reduced that to 1.5 million, that alone would increase total US labor productivity by 1.7 percent,[1] but it would also leave two million drivers looking for work.

In 2013, Oxford economists Carl Frey and Michael Osborne made waves by predicting that 47 percent of US employment was automatable over the next two decades, with a higher estimate for developing countries.[2] Erin Winick of Technology Review subsequently produced a summary table of job losses and gains estimations on automation.[3] Some of the worldwide figures are in Table 1. There are clearly two sides to the ledger, but some of the predicted job loss numbers at the global level are considerable.

The forecasts suggest bad news for Africa in particular, given concentration in types of low-skill jobs that might be easy to automate, rising working age populations, and already far too few good jobs to occupy the existing population. Arntz et al. suggest the share of workers at high risk of automation is 40 percent amongst those with a lower secondary education and above 50 percent for those with primary or less education.[4]

Advanced manufacturing and AI applications including automated call centers might even reverse the trend towards manufacturing and low-skilled services moving to developing countries. That would imperil a recent run of global income convergence. And there have been cases of impact already: Foxconn replacing 30 percent of its workforce when it introduced robots, and 1,000 lost jobs in Vietnam when Adidas shuttered a factory and moved production to “speed factories” in Germany and the US. If this is the beginning of a trend, it would be harmful to African development prospects.

Dani Rodrik notes that the move towards fragmented production—global value chains that have proven important to manufacturing growth in countries including China—has declined since 2011. Worse, analysis by Rodrik and colleagues finds that for outputs produced in global value chains, the comparative advantage of those countries further behind was already loosening: wage competitiveness is not a significant determinant of participation but proximity to major markets, human and physical capital, institutional and logistics capacity all matter.[5] This compares to products that were not part of global value chains, where wage competitiveness was the (only) factor of those examined which mattered for location—an important reason why manufacturing traditionally helped lower-income countries catch up. Connected to and exacerbating these problems, we have seen a declining job-intensity of exports overall.[6] And the global shift in demand towards (less-traded) services suggests challenges for the next generation of countries hoping to use manufacturing exports to develop.

Table 1. Predictions of job losses and gains from automation

| When | Destroyed (m) | Created (m) | Estimate by |

|---|---|---|---|

| 2020 | 1.0-2.0 | Metra Martech | |

| 2020 | 1.8 | 2.3 | Gartner |

| 2021 | 1.9-3.5 | IFR | |

| 2022 | 1,000 | Frey | |

| 2030 | 2,000 | Frey | |

| 2030 | 400-800 | McKinsey |

Rodrik suggests that as a result of current trends, “[a] new [development] path will have to be invented. The broad contours of this alternative are easy to state. It will be a model based on services. It will focus more on soft infrastructure—learning and institutional capabilities—and less on physical capital accumulation—plants and equipment.” But productivity advances in services may be harder: partial sectoral approaches stimulating export-oriented industrialization will have to be replaced by “massive economy-wide investments in human capital and institutions.”[7] If that is true, Africa’s small markets, burdened with an expensive labor force and considerable infrastructure and institutional challenges, may well fall further behind.

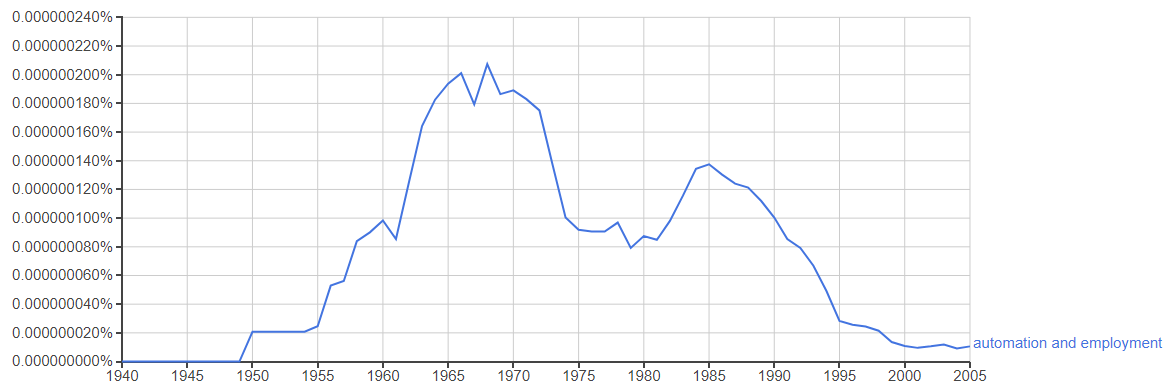

At the same time, there are reasons to doubt the pessimism. Concerns with the impact of labor-saving technology is a longstanding tradition. The robopocalypse has been nigh for at least 80 years, and the idea that automation would crush the working man has been around even longer (see Figures 1 and 2). Keynes predicted technological unemployment in the 1930s, Leontief in the 1950s, and Heilbroner in 1965.[8] There was another peak of concern in the mid-1980s (see Figure 3). Moore’s Law—the observation that the number of transistors on integrated circuits is doubling about every year—is increasingly invoked as evidence we are on the cusp of a revolution, but the law dates back over a half-century, to 1965. It was previously rolled out during discussions of the forthcoming US productivity miracle in the 1990s—but jobs did not go away then, and global development continued.

Figure 1. The New York Times blames machines for unemployment in 1928[9]

Figure 2. Der Spiegel predicts Robopocalypse in 1964, 1978, and 2016[10]

Figure 3. Appearance of the phrase “automation and employment” in books over time

This note reviews some of the literature around AI, automation, jobs, and development prospects with a focus on potential implications for developing countries and in particular for Africa.

It makes the following arguments: First, automation has long been a vital part of development, and Africa needs more of it. Second, the sector or occupational effects of labor-saving technical change on jobs and incomes can be negative, but (at least to date) new jobs keep being created in the economy as a whole thanks to the demand generated by greater productivity. Income concentration and job losses caused by robots and AI to date have been limited, and policy appears to have mattered far more to trends in inequality. Third, labor-saving technologies might reduce the convergence prospects of a region that has a lot more labor than capital, but manufacturing (export) jobs are not going away yet, and there are still hopes for developing countries to use the manufacturing route to development. And, fourth, the ongoing ICT revolution may present new opportunities to developing countries to speed growth. This is not to suggest the fears of development pessimists are ungrounded—challenges will surely appear. But the evidence to date suggests at least some reasons for optimism about Africa’s future economic performance even in the face of smarter robots.

Productivity is good

Automation has been a vital part of economic growth, and that growth has always involved shifting employment patterns. The mechanization of farms—replacing human and animal labor with tractors and combines—is a vital factor in allowing the US to produce far more food than it consumes despite the fact that the proportion of workers in agriculture has declined from 74 percent in 1800 to around 1.5 percent today.[11] Just between 1940 and 1980, agriculture lost four percentage points of its employment share each decade in the US.[12]

And automation helps to account for the fact that employment in pin factories in the UK fell about 99 percent between 1820 and 1960 while output exploded. Adam Smith suggested workers operating individually could produce about 10 pins a day. In a factory using the technology of his time (the 1770s) he estimated they produced 4,800 pins each a day. By the 1970s, pin factories were producing 800,000 pins per day per employee. Weaving productivity has increased over 200-fold over a similar period.[13] Again, William Nordhaus has explored the multiple-magnitude drop in the price of light over the last few centuries.[14] This is why really poor people worldwide can afford pins, cloth, and light. Robots are only one of the more recent entries in a huge long line of labor-saving technologies that have made the world better off.

Automation does considerably change what people do for a living. In 1850 the average worker produced around one hundredth of a ton of steel or a yard of cloth each day. By 2000 it was more than half a ton or 200 yards of cloth.[15] The change was associated with both increased worker wages and increased consumption, as well as initially with increased employment, but price elasticity of demand did eventually fall—and we do not consume 200 times the cloth we did in 1850. (We consume closer to 100 times the amount). In both textiles and steel, suggests Bessen,[16] most of the jobs in rich countries have disappeared since 1950 because of growth in labor productivity without compensating growth in demand. (In textiles, the number of workers declined from 350,000 to 120,000 between 1950 and 1995.)

But Mokyr et al. [17] note that while the industrial revolution killed a lot of jobs in home weaving, it created new jobs for mechanics, supervisors, accountants. “Technological progress also took the form of product innovation,” they note, “and thus created entirely new sectors for the economy, a development that was essentially missed in the discussion of economists of this time.”

Elevator operators in the US demonstrate the full cycle of innovation creating and then destroying particular jobs. Their numbers in the US climbed from zero in 1860, to 497 in 1870, to 114,473 in 1950 before declining back towards zero by 1990. Pin setters at bowling alleys, motion picture projectionists, travel agents—a number of other activities have followed the cycle. Regarding new product innovation creating employment, there were 466,000 jobs related to mobile apps in 2012.[18] Again, Mandel estimates that jobs in fulfillment centers and ecommerce companies rose by 400,000 from December 2007 to June 2017 in the US, exceeding the 140,000 decline of brick-and-mortar retail jobs over the same period (fulfillment center jobs also pay 31 percent more than brick-and-mortar retail jobs in the same area). [19] New employment opportunities have spread to developing countries: Bangladesh has an estimated 650,000 online freelance workers. [20]

Again, it is worth noting that automation has long replaced brains as well as brawn. Medieval guild professions involved many years of apprenticeship for careers from knife-making, armorers, and shoemakers to harness makers. When people used to think of calculators they thought of human beings. Recoded music and television negated the need for live orchestras or wandering players at every performance. Not that live performances died out, of course—there are more people making a living from live performances than ever before, and this example points to the fact that automation can also complement rather than replace existing employment. Bessen provides an example related to a recent automation process: there are more bank tellers than ever before in the US despite a rise in the number of automated teller machines from zero in the 1970s to over 400,000 today (approximately one ATM for each human bank teller).[21] Bank tellers do a different combination of tasks than they used to—less counting cash, more advice on products—but they haven’t gone away.

That automation has not reduced employment helps to explain why the percentage of people aged 25 to 54 who are employed in the US, at 80 percent, is only 2 percentage points below its peak in 2000 and up 18 percentage points from 1950 (output per worker has increased more than threefold over that time).[22] Again, in 2016, there was no link between output per hour and the employment to population ratio across the OECD—it is not that places with higher capital stocks employed fewer people, they were just richer. Conversely, Mexico had a similar employment-to-population ratio to Luxembourg and Ireland but produced fourfold less output per hour (Furman and Seamans, 2018). The gap with poorer countries is even larger—with low-income, low-automation economies seeing the considerable majority of their workforce either self-employed in activities like subsistence farming or in informal, poorly paid jobs.

And until we meet the sated consumer, declining demand for one product will lead to greater demand for another. Autor and Salomons[23] suggest that across the OECD, industry-level employment does tend to fall as industry productivity rises, but country-level employment rises as aggregate productivity rises. Productivity increases raise incomes, consumption, and employment so that the negative own-industry employment effects are more than outweighed by positive spillovers to the rest of the economy. Again, this has involved a significant reallocation of workers into tertiary services which employ a disproportionate share of high-skilled labor, but it has not led to overall job losses.

Regarding the distribution of benefits from automation, looking at the world as a whole, if long-term rising productivity was consistently associated with rising inequality within countries, rich countries would be considerably more unequal than poor countries. They are not. And if global productivity advance was associated with decline in developing countries, greater output per capita in rich countries would be associated with lower output per head in poorer countries. It is not.

The reason why developing countries are poor is because they see low productivity, driven in part by limited automation. They are not intensively using technologies invented long ago to raise that productivity—technology including tractors and combine harvesters, spindles, Bessemer plants, and electricity.[24] What is behind the slow diffusion of such technologies is complex, but again, poverty and lack of well-paid formal sector jobs is associated with low use of productive technologies, not high use.

Thankfully, we are seeing rising productivity and shifts in employment share in low- and middle-income countries including in Africa. In those countries as a whole, employment in agriculture as a share of the total fell from 53 percent to 32 percent from 1991 to 2016.[25] Turning to Africa in particular, Yeboah and Jayne report that the period of strong regional growth since 2000 has been accompanied by a significant shift out of agricultural employment and rapid growth of wage employment.[26] And if global productivity further increases in manufacturing, this will have significant benefits for African consumers—cheap mobile phones, generic pharmaceuticals, bed nets, plastic sheeting, foodstuffs, and so on have already been a considerable benefit to poor consumers in developing countries, as have free services like Google Maps and Facebook.

All that said, it would be better news if the productivity gains of newer advances including robotics and AI were globally widespread on the production side as well as the consumption side, and so far the bigger effect of recent automation has been in advanced economies.[27] This does raise concerns that advances in automation may have inequitable effects within and between countries at least over the medium term, because of where and who gains from the increase in productivity. As Frey[28] illustrates, there was a considerable gap between the start of the industrial revolution and benefits flowing to most British workers. And Allen[29] notes that by the mid nineteenth century, wages were (finally) rising in the UK, but by that time workers in other countries were suffering. In the 1830s, the British Governor General in India reported, “The bones of the cotton-weavers are bleaching the plains.” Both India and China saw absolute de-industrialization.

The fear that the same phenomenon might occur—or already be occurring—today, with dramatic productivity gains appropriated by owners of capital in rich countries to the cost of workers in rich and poor countries, would be justified if (i) there was evidence of significant and rapid spread of productivity enhancing technologies in rich countries; (ii) job churn was rising as workers were rapidly replaced from automating industries facing saturated consumer demand; and (iii) manufacturing was declining in poor countries and global incomes were diverging. Later sections will suggest that evidence is still lacking for these concerns. There are significant challenges facing poor workers in rich countries and industry in developing countries including Africa, but (as of yet) we are some way from bleached bones.

Innovation, productivity, and hollowing out haven’t sped up in rich countries

Computers, robotics and AI have already had an impact on economies worldwide. The share of information processing equipment and software in nonresidential investment rose from 8 to 30 percent between 1990 and 2012.[30] A lot of jobs have been affected and some professions—including travel agents—notably shrank. Robot prices adjusted for quality fell 80 percent between 1990 and 2005 and research by Georg Graetz and Guy Michael from the London School of Economics suggests they have already increased productivity and overall economic growth.[31]

But evidence is so far absent of a major productivity shock. Robert Gordon notes the pressing question of the last few years in the US is “why has economic growth slowed when innovation appears to be accelerating?” He suggests the productivity growth slowdown can be attributed to “declining productivity of research workers, diminishing returns to drug innovation, and the evolutionary rather than revolutionary impact of robots and artificial intelligence, which are replacing workers slowly and only in a minority of industrial sectors throughout the economy.”[32]

Indeed, Bloom, Jones, Van Reenen, and Webb argue that “ideas are getting harder to find”–estimating, for example, that the number of researchers working on semiconductors has increased eighteenfold since 1971, but Moore’s law (the doubling of chip density every two years) has applied throughout that period.[33] They argue this demonstrates a declining return to research and find similar results in agricultural yields (25 times the researchers, a straight-line increase in yields since 1960 for corn) and drugs (measured by new molecular entities, clinical trials and publications). They note more broadly that aggregate growth rates are stable over time, but the number of researchers has increased enormously—twenty-three-fold since the 1930s.[34]

Meanwhile, trends in labor productivity, capital investment, and IT and software investment in particular all suggest a slowdown over the past 15 years.[35] Brynjolfsson, Rock, and Syverson accept the “paradox” of growing use of AI and robotics and slowing productivity in the US and elsewhere (29 out of 30 countries with OECD labor productivity data saw a deceleration in productivity growth between the periods of 1995–2004 to 2005–16).[36] They suggest a number of reasons why this may change, in particular that there is often a lag between the start of new technology adoption and productivity effects due to the need to restructure. It wasn’t until the late 1980s, more than 25 years after the invention of the integrated circuit, that the computer capital stock reached its plateau at about 5 percent of nonresidential equipment capital, they note, and complimentary capital is required on top of that as well as restructuring and broader institutional innovation. This is surely plausible, but also suggests once again the likely evolutionary rather than revolutionary effect of AI adoption.

Regarding employment, if automation was forcing lots of people to seek new jobs, we’d expect rates of both firings and hirings to be on the up. Furman[37] notes that labor market fluidity (both the job destruction and creation rate) has been declining since 1975. Atkinson and Wu suggest the level of occupational churn in 2010–15 is perhaps one-quarter of its level in the 1950-60 period and has been steadily declining since 1980s.[38] Similarly, employment share by occupation has been changing far more slowly in the last 15 years than in previous periods.

Autor and Salomons study the effect of automation across 18 OECD countries since 1970. Using TFP as well as instrumenting using foreign patent flows and robot adoption they find that recent automation has not reduced jobs but is associated with a declining labor share in value added within industries.[39] Again, Autor (2018) notes sales, office, and administrative workers, production workers and operatives accounted for 60 percent of US employment in 1979 compared to 46 percent in 2012.[40] And Autor (2019) suggests that non-college educated workers in the US perform substantially less skilled work than they did decades earlier—although some of that will be the result of selection effects.[41]

But Autor also accepts that the rate of decline of “mid skill” employment has fallen since 2000 compared to earlier periods, and there is an argument over how much hollowing out there is to explain at least in the United States. Mishel and colleagues suggest that lower-wage occupations have remained a small and stable share of employment since the 1950s (although their percentage share did climb 2.4 points 1999-2007) while middle-wage occupations have been steadily giving ground to higher-wage jobs over that time, and evidence for polarization is weak especially in the 2000s. Furthermore, occupational wage level has been a weak predictor of changing employment share.[42]

Again, Hunt and Nunn re-evaluate the hollowing out phenomenon, suggesting that previous studies have found polarization thanks to an artefact of occupation code redefinitions. They suggest the small change in workers earning middle wages in the United States since 1973 is largely accounted for by a strong increase in the share of workers earning high wages and a small decline in the share earning low wages. The evidence, they suggest “rules out the hypothesis that computerization and automation lie behind both rising wage inequality and occupation-based employment polarization.”[43]

Looking around the world, there is some evidence of hollowing out in developing countries, with increasing demand for nonroutine cognitive skills. That said, the demand for routine cognitive skills has increased in countries including Botswana, Ethiopia, Mongolia, the Philippines, and Vietnam. [44] More broadly, while people in developing countries do see a high return in investments in education—as high as 15 percent a year for tertiary education despite a considerable increase in the supply of such labor[45]—inequality in developing countries has not uniformly increased. From 2007 to 2015, 37 of 41 emerging economies with data saw inequality remain flat or decline.[46]

And we are not seeing the “cross-country hollowing” that would be expected were automation driving jobs away from mid-skilled workers. A. T. Kearney suggests that there were 300 cases of reshoring to the United States in 2014, a rise from previous years but still tiny considering that US MNCs have more than 25,000 foreign affiliates worldwide. And this does not account for continued offshoring amongst firms. Overall, US MNC imports from affiliates have continued to climb as a percentage of sales.[47] Based on an ex-post accounting exercise of Asian countries, Bertulfo and colleagues (2019) suggest that greater automation within global value chains does drive down the demand for routine relative to nonroutine jobs, but the demand created by the higher-paid workers that remain appears to offset employment losses within GVCs.[48] Furthermore the recent period of automation, AI and advances in robotics has been one of global income convergence.[49] For the 43 countries the World Bank classified as “low income” in 1990, 65 percent have grown faster than the high-income average since 1990, along with 82 percent of the 62 middle-income countries in 1990. This is the reversal of a pattern since at least the 1960s.

If not automation, what is driving the rise of inequality in some countries? The answer appears to be policy choice. Since the Industrial Revolution there has rarely been the demand for unskilled labor to drive wages up fast enough to reduce inequality. It has only happened in a few periods in a few countries—perhaps the UK in the mid-nineteenth century and in some East African miracle countries, but even then, only due to high export volumes. Usually, unskilled wages are kept higher by minimum wage laws, safety net systems, barriers to entry, and other interventions.

Rising inequality is a result of domestic policy choices—including anti-union legislation, lower corporate taxes, and less regulation of firms with monopsony power in the labor market. You do not have to look far beyond policy to explain inequality in the US, for example. The labor income share of the bottom 90 percent in the United States fell as a percentage of the total share 1979 to 2000, by about 10 percentage points, but has been flat since then.[50] Beyond reduced tax progressivity, that timing suggests a role for the collapse of private-sector unions may have big role to play. [51] The share was 24 percent in 1973 and had fallen to 13 percent by 2000.[52] Again, the OECD estimates the real hourly value of the US minimum wage was $9.80 in 1979, fell to $7.30 in 2000 and was still only $7.30 in 2017.[53]

Ignacio Gonzalez and Pedro Trivin conclude in their analysis of The Global Rise of Asset Prices and the Decline of the Labor Share that “we believe that the decline in the labor income share is not the irreversible consequence of technological or structural factors…but the result of policies that have boosted asset prices” and suggest the trend could be reversed by “increasing competition or by imposing higher taxes on corporate distributions, like dividends or share repurchases.”[54]

Across countries, globalization has long been used as an excuse to attack labor rights and (so) reduce the labor share. But there is no need for that to be true—highly globalized countries in Europe have considerably stronger labor rights and lower inequality than the US, for example. And Guerriero (2019) notes that the variation of labor share of income across countries is far greater than the variation of labor share of income within countries over time (1970-2015). The labor share is positively associated with measures of democracy and negatively associated with income.[55]

It is also worth noting here that, manufacturing jobs are not naturally “better” than the services jobs that are overtaking them—remember the child labor of the industrial revolution. The jobs were made better by strong unions and safety as well as wage regulation. Where that regulation is weaker, manufacturing jobs are not as prized.[56] With services jobs, Rodrik (2015) notes that in many countries they are associated with lower unionization, weaker job protections and norms of pay equality. But they don’t have to be associated with those features. Carre and Tilly (2017) study retail employment and suggest it does not need to be a low-quality largely part-time job as it is in the US.[57] In France, for example, supermarket cashiers are paid more, are mostly full time, have lower turnover and higher productivity. Social norms, rates of unionization and regulatory environments account for the difference. Even in the US, Costco and Trader Joe’s offer better quality jobs than Walmart, for example, and Walmart jobs are relatively more attractive in other countries.

The impact of robots is still hard to see

If the macro picture fits ill with a story of rapid innovation pushing national and global income divergence over the past few years, there is still some evidence that computerization and robotics may be having an effect on labor market outcomes. Bessen (2016) suggests that across occupations, greater computer use is associated with a rise in employment, although that impact is muted by the fact that other occupations in the same industry see a slight fall in employment.[58] And computer-using jobs are more skilled, potentially leading to growing wage inequality. Again, there is considerable OECD evidence of a move out of routine-task intensive jobs. [59]

Less can be said about the widespread impact of robots in particular precisely because robots are not widespread. Gordon notes that robots were first introduced into manufacturing in 1961 and by the 1990s were welding auto bodies and painting cars. But they have made few inroads outside of manufacturing and warehouses.[60] Half of all robots shipped in the US in 2016 were for the automotive sector, which has a stock of robots per worker (at a little more than one per ten) that is 14 times higher than outside the automotive industry (Furman and Seamans, 2018).[61] And while the number of robots shipped worldwide approximately tripled between 2004 and 2016, to around 300,000, this compares to about 77 million cars and 280 million computers that were sold worldwide in 2016.[62]

It is worth noting robot density worldwide is highest in Germany, Korea, and Singapore, and all have high employment rates. [63] (Germany has four times the number of robots per thousand workers that the US does.) That said, the introduction of robots was associated with rising wages for high-skilled workers, lower wages for low-skilled workers, and a higher capital share (Dauth et al. 2017). Acemoglu and Restrepo (2017) find that increased industrial robot usage by an industry in a commuting zone in the United States is associated with lower employment in that industry in that zone. However, their approach cannot detect many of the jobs created by automation (through lower prices, for example). And (even) taking the Acemoglu and Restrepo (2017) numbers at face value, robots account for less than 8 percent of the decline in the share of the working-age population with a job since the 1990s (or 0.34 percent of that population). Given they find non-robot IT investment is sometimes positively correlated with employment, the overall effect of automation is surely muted (Atkinson and Wu, 2017)

Mann and Puttmann link patents to their industrial use and though industry structure to their likely impact on commuting zones. The researchers suggest automation leads to declining manufacturing employment more than matched by increased services job growth. [64] This a broader measure of automation than “robots” and the authors conclude that their results combined with Acemoglu and Restrepo might suggest robots automating routine tasks in manufacturing may be bad for jobs while other types of automation outside of services may have a more positive effect on employment.

Looking across the world, there are very few robots in developing economies outside of China. That reflects in part the relative costs of labor and capital. Jorg Mayer (2017) notes that “what is technical feasible is not always economically profitable”—job displacement is most likely tasks that are routine and well paid.[65] Food, beverages, and tobacco see high routine task intensity but also low compensation—the industry uses far fewer robots than transport equipment, with lower routine task intensity but far higher average compensation. Textiles see particularly low robot use and low compensation despite high routine task intensity. This suggests many of the manufacturing industries most common in developing countries are there precisely because automation remains comparatively expensive. Perhaps this will change over time, but there is not significant evidence of it yet.

Regarding shifting comparative advantage, Micco (2019) suggests there has already been some impact of robots: in the last few years, developed countries have begun importing less from Latin American countries in sectors at a particular risk of automation as their stocks of robots per worker climb.[66] Again, De Backer et al. (2018) suggest that in the period 2010–14, adoption of robots in high income country industries may have been associated with a slower rate of offshoring.[67] Giuntella and Wang find that cities in China home to industry especially prone to robot use have seen lower employment and wage growth 2000-16.[68]

That said, Artuc, Bastos, and Rijkers (2018) find that a 10 percent increase in robot intensity in an automating industry in a rich country leads to a 6.1 percent rise in imports sourced from less developed countries in the same industry (thanks to increased demand for parts and components) and a 11.8 percent increase in exports to those countries.[69] The authors suggest that this implies welfare gains to both rich and poor countries from robotization.

Again, Artuc, Christiaensen, and Winkler (2019) find that the increase of 0.5 robots per 1,000 workers in the US between 2004–14 lowered growth in exports per worker from Mexico to the US by 3.3 percent (this during a period where exports per worker grew on average by about 110 percent, suggesting a minor impact). Exposure reduced wage employment in areas where occupations were more susceptible to being automated but increased wage employment in other areas, leading to no net impact on manufacturing employment or employment overall.[70]

Manufacturing jobs have moved but not gone away

Hallward-Driemier and Nayyar, using data from 1994 for 19 countries, suggest the average export-to-output ratio of manufacturing is 68 percent compared to 6 percent for services, and the share of blue-collar workers is 74 percent in manufacturing compared to 31 percent in services. [71] Beyond being traditionally low-skilled and producing exportable goods, there is considerable evidence that manufacturing is a sector that benefits from economies of scale with strong forward and backward linkages, and that demonstrates technological spillovers within and between countries. These features have made it an important source for growth in lower-income countries, especially in the past. Rodrik has shown that manufacturing has shown unconditional productivity convergence over the long term, even in countries with very weak institutions or policies. He worries that automation and global value chains are eroding the advantage of low-income producers, increasing the share of skilled labor, and making other factors than low labor cost important to competitiveness. [72]

And Rodrik is concerned by the sustainability of growth by other means. While some parts of services share high productivity features, like automated manufacturing these are comparatively low-employment high-skilled activities, suggests Rodrik.[73] In Africa, service sectors with the best productivity performance typically shed labor while those that absorb labor have the worst productivity performance. [74] Similarly, Hallward-Driemier and Nayyar suggest most service industries that exhibit “productivity enhancing” characteristics (for example IT services) are unlikely to be associated with large scale employment creation for low-skilled workers while low-skilled sectors are less likely to drive productivity gains. Tourism and retail trade may be the exceptions.

More positively, the death of developing country manufacturing opportunity might have been over-played. Over the longer term it is developed countries that have witnessed the greater decline in manufacturing share of output—if from a higher starting point. In OECD countries, the average share of manufacturing as a percentage of GDP has been falling since at least 1950.[75] Lawrence (2018) notes the (decades long) trends of productivity growth in US manufacturing combined with comparatively unresponsive demand has led to a declining share of manufacturing employment (a trend only marginally impacted by growing globalization). The share of consumption spending on goods declined from 62 to 33 percent 1947–2017. [76] The US long-term pattern is typical of that seen in industrial countries including those (like Germany) that have a manufacturing trade surplus.

But turning to developing countries, while Szirmai (2009) notes developing countries on average have smaller manufacturing sectors and larger services sectors than now-rich countries did at the same stage of development, China experienced a peak in manufacturing employment share that was higher than the peak in the average advanced economy,[77] and China is a very large country. It may account for some of the premature peaking elsewhere. Haraguchi et al. (2016) find that across developing countries as a whole, manufacturing employment has climbed from below 10 to closer to 15 percent over the past few decades, largely driven by China.[78]

As developing countries get richer, and despite a likely decline in the share of consumption going to goods, global demand for manufactured products will continue to climb. And the associated manufacturing employment may shift. Hallward-Driemier and Nayyar suggest wages in Chinese manufacturing have climbed 281 percent 2003–2010.[79] There is already some evidence of jobs moving as a result: just in the first decade of the twentieth century, the share of the labor force employed in agriculture in sub-Saharan Africa declined by roughly 10 percentage points, with a rise of 2 percent in manufacturing and 8 percent in services. In Kenya between 2000–2007, the share of manufacturing in employment climbed more than 7 percentage points 2000–2010.[80] From a low point of 9 percent of exports in 1981, sub-Saharan Africa’s manufacturing share of exports was 27 percent in 2017.[81] Chinese FDI in manufacturing in the region has climbed considerably, and there were as many as 100,000 factories owned by Chinese businesspeople on the continent in 2017.[82]

Services opportunities are growing

At the same time, other pathways to prosperity appear to be emerging. There is evidence of a rising impact of services on growth compared to manufacturing.[83] Across the countries in Hallward-Driemier and Nayyar’s sample, average value added per worker in services, at about $27,000, is slightly higher than in manufacturing ($26,000).[84] Szirmai’s survey of the literature suggests that manufacturing as a source of growth was more important in the period 1950–73 than since then, when services have been the more powerful contributor. Ghani and O’Connell (2014) suggest services convergence across countries has been more rapid than manufacturing convergence 1990–2010, and services have experienced faster growth rates and created more jobs.[85] Productivity levels in a range of services is converging to the global frontier—including trade and accommodation (the fastest growing employer amongst service industries in developing countries), transport and communications, and financial intermediation and business services.[86] Note also that cross-country convergence began after the average share of manufacturing in GDP across developing countries began to decline in the 1990s.

Looking at India in particular, Amirapu and Subramanian (2015) find that services as a whole have seen labor productivity grow more rapidly than registered manufacturing 1984–2010, a level of productivity almost twice that of manufacturing as a whole and more than twice the productivity of aggregate economy as a whole.[87] Parts of the services sector including financial services and insurance as well as real estate and business services considerably outperform registered manufacturing. Eichengreen and Gupta also report the emergence of what might be thought of as stepping stone tradeable service jobs in the rural areas of India, employing workers with some high school education who can do basic data entry and read forms—they earn four times the agricultural wage which is still one half the wage of workers in Bangalore. [88]

Amirapu and Subramanian accept that while several service subsectors share the virtues of high productivity and domestic and international convergence, they also share the feature of formal sector manufacturing of being fairly skill intensive. In 2004/5 in India, 77 percent of employees in registered manufacturing firms had at least primary education and 43 percent secondary education. In services, 78 percent had at least primary education and 48 percent secondary education. The good news is that developing countries are far better placed to fill higher-skilled jobs than in the past. The stock of educated workers in low-income countries is far higher than it was in high-income countries when they were at a similar income level. The average number of years of education in the population 25 years and older in India climbed from 1.9 in 1980 to 5.4 in 2010.

Africa is seeing similar progress. In Kenya, for example, average years of schooling has gone from 2.5 to 6.2 years over the same period. Kenya’s average years of schooling for the population 25 and above in 2010 is the same as Italy’s was in 1980.[89] And Newfarmer et al. suggest that Africa is already on the path to “growth without smokestacks”: service industries alongside food processing and horticulture are beginning to play a role in the region analogous to that played by manufacturing in East Asia.[90]

Richard Baldwin suggests the future possibilities could be even larger. The “third globalization” is unbundling labor from its physical location through remote work, which could reduce (in production terms) the impact of migration controls, potentially allowing the global economy to benefit from some of the trillion dollar bills on the sidewalk left by constraints on labor mobility. Baldwin predicts a “globotics upheaval” in which US and European service sector and professional jobs are opened to direct competition from abroad—in other words, that large parts of the services sector will become as tradeable as manufacturing. He argues this trend will be supported by instant machine translation, improved remote communication, and collaboration.[91] If this occurs, there would be a huge upside for developing countries including Africa in terms of services exports. But it should be noted that the evidence for the third globalization is as nascent as that for the impact of robotics (with predictions of mass offshoring around for more than a decade), [92] and there are dissenting (if weakly evidenced) views suggesting improved communication might lead to concentration.[93]

Africa’s opportunity?

Will Africa be able to benefit from new opportunities presented by the potential decline of manufacturing in China alongside new service industries with the possibility to export? Most of African output is currently very low productivity. Eifert et al. estimate that the same stock of capital and labor produces around 75 percent less in Nigeria than it does in China, for example. The local business climate—the burdens of regulation, poor public service provision, and so on—is a very serious impediment for many firms, and recognized as such by local firms in surveys. The “indirect costs” of this poor environment on productivity are significantly higher in Africa than elsewhere. That suggests amongst other things that a strong services sector is important to both manufacturing and services export competitiveness, and helps to explain why so few countries outside of East Asia have managed to achieve rapid growth including through manufacturing exports. It also suggests that strong manufacturing export performance may proxy for a better environment for production in general—and that a better environment may in fact be the key to rapid growth.

Rodrik’s argument regarding the need for systemic reform still holds, then. Simons (2019) points out the challenges that African e-commerce startups or global operators operating in Africa face because the broader economic ecosystem is not in place to exploit models based on the institutional and infrastructural conditions of an OECD country. Especially players that aim to focus on the local market “consistently feel compelled to build out 'across the value chain' and take responsibility for multiple steps along that chain." Konga, a Nigeria e-commerce startup, had to “build its own payment platform, courier network, anti-fraud program, fulfilment centers, call centers, and training system."[94] Fixing the broader environment for business will be a key part of the challenge for the region to gain from the new opportunities presented by any diffusion of manufacturing jobs or Baldwin’s “third globalization.”

That said, some output in the region approaches the global production frontier, including Kenya’s agribusiness. It is not that the international system and the region’s institutional legacy simply makes African competitiveness an impossibility. And advances in e-commerce may help improve the underlying business environment to the benefit of firms and employees alike. Mobile financial solutions have already revolutionized banking services in parts of the continent. And Porteous and Ng’weno (2019) note that digital commerce and the gig economy are opportunities for informal workers rather than a threat, allowing a ladder towards formality through integration into the formal sector through finance, contracts, taxes, and eventual registration.[95]

Policies for the robopocalypse

It may be that we are on the cusp of a productivity revolution in rich countries that will create a global shockwave that flattens Africa’s manufacturing prospects. On the other hand we may not be: there are certainly reasons to doubt some of the forecasts suggesting massive technological change in the short term (not least, recent setbacks with autonomous driving, including the death of a pedestrian[96] and the apparent failure of IBM’s program to use the Watson supercomputer for cancer diagnostics).[97] Again, it may be that we are on the cusp of a revolution in the trade of services that will create huge opportunities for developing countries ready to grasp the opportunity. That said, previous over-estimates of the growth of global outsourcing might give us pause.

Either way, the policy prescriptions for robopocalypse or globotics revolution are similar. The World Bank’s World Development Report 2019 suggests automation calls for three main responses: investment in human capital and especially education; enhancing social protection; and taxes to support those policies, including property taxes, sin taxes, and carbon taxes. These all seem eminently sensible policies even if change is evolutionary than revolutionary, and whichever direction it takes.

The broad news for African development prospects is reassuring. Automation increases incomes and is associated with more, not fewer, good jobs. The region could still benefit from a considerable expansion in manufacturing, and while manufacturing jobs may be becoming more skill intensive, education levels in Africa are higher than they were in industrialized countries only a few decades ago (even if learning levels lag further behind). Again, there are increased opportunities in services exports as well as new tools to increase the productivity of domestic services. Evidence of an imminent third or fourth industrial revolution that might re-concentrate output in the richest countries is lacking, and policy tools are available to reduce domestic pressures towards greater inequality. All that said, the barriers that kept the region poor in the past are still likely to limit growth today, and efforts to expand markets, improve infrastructure and institutions, and build human capital remain as vital as ever.

References

Acemoglu, D., & Restrepo, P. (2017). Robots and Jobs: Evidence from US Labor Markets (Working Paper No. 23285). https://doi.org/10.3386/w23285

Allen, R. C. (2017). Lessons from history for the future of work. Nature News, 550(7676), 321. https://doi.org/10.1038/550321a

Amirapu, A., & Subramanian, A. (2015). Manufacturing or Services? An Indian Illustration of a Development Dilemma (SSRN Scholarly Paper No. ID 2623158). Retrieved from Social Science Research Network website: https://papers.ssrn.com/abstract=2623158

Andrew Arruda. (n.d.). Relax, Humans – Robots Are Not Going to Take Your Jobs. Retrieved September 18, 2019, from Evolve the Law website: https://abovethelaw.com/legal-innovation-center/2017/12/06/relax-humans-robots-are-not-going-to-take-your-jobs/

Anslow, L. (2016, May 22). Robots have been about to take all the jobs for more than 200 years. Retrieved September 18, 2019, from Medium website: https://timeline.com/robots-have-been-about-to-take-all-the-jobs-for-more-than-200-years-5c9c08a2f41d

Arntz, M., Gregory, T., & Zierahn, U. (2016). The Risk of Automation for Jobs in OECD Countries: A Comparative Analysis (OECD Social, Employment and Migration Working Papers No. 189). https://doi.org/10.1787/5jlz9h56dvq7-en

Artuc, E., Bastos, P. S. R., & Rijkers, B. (2018). Robots, Tasks and Trade (No. WPS8674; pp. 1–71). Retrieved from The World Bank website: http://documents.worldbank.org/curated/en/269231544735360818/Robots-Tasks-and-Trade

Artuc, E., Christiaensen, L., & Winkler, H. J. (2019). Does Automation in Rich Countries Hurt Developing Ones? : Evidence from the U.S. and Mexico (No. 8741). Retrieved from The World Bank website: https://ideas.repec.org/p/wbk/wbrwps/8741.html

Atkinson, R. D., & Wu, J. J. (2017). False Alarmism: Technological Disruption and the U.S. Labor Market, 185002015. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3066052

Autor, D. (2019). Work of the Past, Work of the Future (Working Paper No. 25588). https://doi.org/10.3386/w25588

Autor, D. H. (2015). Why Are There Still So Many Jobs? The History and Future of Workplace Automation. Journal of Economic Perspectives, 29(3), 3–30. https://doi.org/10.1257/jep.29.3.3

Autor, D., & Salomons, A. (2018). Is Automation Labor-Displacing? Productivity Growth, Employment, and the Labor Share (No. w24871; p. w24871). https://doi.org/10.3386/w24871

Bachmann, R., Cim, M., & Green, C. (2018). Long-run patterns of labour market polarisation: Evidence from German micro data (No. 748). Retrieved from RWI - Leibniz-Institut für Wirtschaftsforschung, Ruhr-University Bochum, TU Dortmund University, University of Duisburg-Essen website: https://ideas.repec.org/p/zbw/rwirep/748.html

Baily, M. N., & Bosworth, B. P. (2014). US Manufacturing: Understanding Its Past and Its Potential Future. Journal of Economic Perspectives, 28(1), 3–26. https://doi.org/10.1257/jep.28.1.3

Bakker, G., Crafts, N., & Woltjer, P. (2017). The Sources of Growth in a Technologically Progressive Economy: The United States, 1899–1941. The Economic Journal, 129(622), 2267–2294. https://doi.org/10.1093/ej/uez002

Baldwin, R. E. (2019). The globotics upheaval: Globalization, robotics, and the future of work.

Barro, R. J., & Lee, J. W. (2013). A new data set of educational attainment in the world, 1950–2010. Journal of Development Economics, 104, 184–198. https://doi.org/10.1016/j.jdeveco.2012.10.001

Bertulfo, D. J., Gentile, E., & Vries, G. J. de. (2019). The Employment Effects of Technological Innovation, Consumption, and Participation in Global Value Chains: Evidence from Developing Asia. http://dx.doi.org/10.22617/WPS190022-2

Bessen, J. E. (2016). How Computer Automation Affects Occupations: Technology, Jobs, and Skills (SSRN Scholarly Paper No. ID 2690435). Retrieved from Social Science Research Network website: https://papers.ssrn.com/abstract=2690435

Bessen, J. E. (2017). Automation and Jobs: When Technology Boosts Employment (SSRN Scholarly Paper No. ID 2935003). Retrieved from Social Science Research Network website: https://papers.ssrn.com/abstract=2935003

Bivens, J., & Shierholz, H. (2018). What labor market changes have generated inequality and wage suppression?: Employer power is significant but largely constant, whereas workers’ power has been eroded by policy actions. Retrieved September 20, 2019, from Economic Policy Institute website: https://www.epi.org/publication/what-labor-market-changes-have-generated-inequality-and-wage-suppression-employer-power-is-significant-but-largely-constant-whereas-workers-power-has-been-eroded-by-policy-actions/

Blattman, C., & Dercon, S. (2018). The Impacts of Industrial and Entrepreneurial Work on Income and Health: Experimental Evidence from Ethiopia. American Economic Journal: Applied Economics, 10(3), 1–38. https://doi.org/10.1257/app.20170173

Blinder, A. (2009). How Many US Jobs Might be Offshorable? World Economics, 10(2), 41–78.

Brynjolfsson, E., Rock, D., & Syverson, C. (2017). Artificial Intelligence and the Modern Productivity Paradox: A Clash of Expectations and Statistics (Working Paper No. 24001). https://doi.org/10.3386/w24001

Bureau of Labor Statistics. (2019a). CPI. Retrieved September 20, 2019, from https://data.bls.gov/PDQWeb/ap

Bureau of Labor Statistics. (2019b). Nonfarm Business Sector: Real Output Per Person. Retrieved September 19, 2019, from FRED, Federal Reserve Bank of St. Louis website: https://fred.stlouisfed.org/series/PRS85006163

Bureau of Labor Statistics. (2019c). Percent of Employment in Agriculture in the United States (DISCONTINUED). Retrieved September 18, 2019, from FRED, Federal Reserve Bank of St. Louis website: https://fred.stlouisfed.org/series/USAPEMANA

Cariolle, J., Goff, M. L., & Santoni, O. (2019). Telecommunications submarine cable vulnerability and local performance of firms in developing and transition countries (No. P195). Retrieved from FERDI website: https://ideas.repec.org/p/fdi/wpaper/3890.html

Chuah, L. L., Loayza, N. V., & Schmillen, A. D. (2018). The Future of Work: Race with-not against-the Machine (No. 129680; pp. 1–4). Retrieved from The World Bank website: http://documents.worldbank.org/curated/en/626651535636984152/The-Future-of-Work-Race-with-not-against-the-Machine

Comin, D. A. (2014). The evolution of technology diffusion and the Great Divergence. Presented at the Brookings Roundtable. Retrieved from https://pdfs.semanticscholar.org/d818/b1ff0e7cda768ac87d7378ea27683958d267.pdf

Dao, M. C., Das, M., Koczan, Z., & Lian, W. (2017). Why Is Labor Receiving a Smaller Share of Global Income? Theory and Empirical Evidence. Retrieved from https://www.imf.org/en/Publications/WP/Issues/2017/07/24/Why-Is-Labor-Receiving-a-Smaller-Share-of-Global-Income-Theory-and-Empirical-Evidence-45102

Das, M., & Hilgenstock, B. (2018). The Exposure to Routinization: Labor Market Implications for Developed and Developing Economies. Retrieved September 20, 2019, from IMF website: https://www.imf.org/en/Publications/WP/Issues/2018/06/13/The-Exposure-to-Routinization-Labor-Market-Implications-for-Developed-and-Developing-45989

De Backer, K., DeStefano, T., Menon, C., & Suh, J. R. (2018). Industrial robotics and the global organisation of production. https://doi.org/10.1787/dd98ff58-en

De Loecker, J., & Eeckhout, J. (2017). The Rise of Market Power and the Macroeconomic Implications (No. w23687; p. w23687). https://doi.org/10.3386/w23687

Diao, X., McMillan, M., & Rodrik, D. (2017). The Recent Growth Boom in Developing Economies: A Structural Change Perspective (Working Paper No. 23132). https://doi.org/10.3386/w23132

Eichengreen, B., & Gupta, P. (2009). The Two Waves of Service Sector Growth (Working Paper No. 14968). https://doi.org/10.3386/w14968

Farber, H., Herbst, D., Kuziemko, I., & Naidu, S. (2018). Unions and Inequality Over the Twentieth Century: New Evidence from Survey Data [Working Paper]. Retrieved from Princeton University, Department of Economics, Industrial Relations Section. website: https://econpapers.repec.org/paper/priindrel/620.htm

Frey, C. B. (2019). The technology trap: Capital, labor, and power in the age of automation.

Frey, C. B., & Osborne, M. A. (2017). The future of employment: How susceptible are jobs to computerisation? Technological Forecasting and Social Change, 114, 254–280. https://doi.org/10.1016/j.techfore.2016.08.019

Furman, J. (2018). Prepared Testimony to the Hearing on “Market Concentration.” Retrieved from https://one.oecd.org/document/DAF/COMP/WD(2018)67/en/pdf

Furman, J., & Seamans, R. (2018). AI and the Economy (SSRN Scholarly Paper No. ID 3186591). Retrieved from Social Science Research Network website: https://papers.ssrn.com/abstract=3186591

Ghani, E., & O’Connell, S. D. (2014). Can service be a growth escalator in low-income countries ? (No. WPS6971; pp. 1–25). Retrieved from The World Bank website: http://documents.worldbank.org/curated/en/823731468002999348/Can-service-be-a-growth-escalator-in-low-income-countries

Giuntella, O., & Wang, T. (2019). Is an Army of Robots Marching on Chinese Jobs? 56.

Gordon, R. J. (2000). Does the “New Economy” Measure up to the Great Inventions of the Past? (Working Paper No. 7833). https://doi.org/10.3386/w7833

Gordon, R. J. (2018). Why Has Economic Growth Slowed When Innovation Appears to be Accelerating? (Working Paper No. 24554). https://doi.org/10.3386/w24554

Graetz, G., & Michaels, G. (2015). Robots at Work (SSRN Scholarly Paper No. ID 2589780). Retrieved from Social Science Research Network website: https://papers.ssrn.com/abstract=2589780

Greenberg, B. (2018). Adam Smith’s Pin Factory. Retrieved September 18, 2019, from EconAir website: https://bennettgreenberg.blogspot.com/2013/08/adam-smith-and-pin-factory.html

Guerriero, M. (2019). Democracy and the Labor Share of Income: A Cross-Country Analysis. Retrieved from https://www.adb.org/publications/democracy-and-labor-share-income-cross-country-analysis

Hallward-Driemeier, M., & Nayyar, G. (2017). Trouble in the Making?: The Future of Manufacturing-Led Development. World Bank Publications.

Hawkins, A. J. (2018, May 24). Uber self-driving car saw pedestrian but didn’t brake before fatal crash, feds say. Retrieved September 20, 2019, from The Verge website: https://www.theverge.com/2018/5/24/17388696/uber-self-driving-crash-ntsb-report

Herrendorf, B., Rogerson, R., & Valentinyi, Á. (2013). Growth and Structural Transformation (Working Paper No. 18996). https://doi.org/10.3386/w18996

Hjort, J., & Poulsen, J. (2019). The Arrival of Fast Internet and Employment in Africa. American Economic Review, 109(3), 1032–1079. https://doi.org/10.1257/aer.20161385

Hruska, J. (2018). IBM Watson Recommends Unsafe Cancer Treatments—ExtremeTech. Retrieved September 20, 2019, from https://www.extremetech.com/extreme/274453-ibm-watson-recommends-unsafe-cancer-treatments

Hunt, J., & Nunn, R. (2019). Is Employment Polarization Informative About Wage Inequality and Is Employment Really Polarizing? (Working Paper No. 26064). https://doi.org/10.3386/w26064

IMF. (2018). World Economic Outlook, April 2018: Cyclical Upswing, Structural Change. Retrieved September 20, 2019, from IMF website: https://www.imf.org/en/Publications/WEO/Issues/2018/03/20/world-economic-outlook-april-2018

Lebergott, S. (1966). Labor Force and Employment, 1800–1960. Output, Employment, and Productivity in the United States after 1800, 117–204.

Mandel, M. (2017). How Ecommerce Creates Jobs and Reduces Income Inequality. Progressive Policy Institute, 28.

Mann, K., & Püttmann, L. (2018). Benign Effects of Automation: New Evidence from Patent Texts (SSRN Scholarly Paper No. ID 2959584). Retrieved from Social Science Research Network website: https://papers.ssrn.com/abstract=2959584

Mastercard Foundation. (2019). Digital Commerce and Youth Employment in Africa. Retrieved from Mastercard Foundation website: https://mastercardfdn.org/wp-content/uploads/2019/03/BFA_Digital-Commerce-White-Paper_FINAL_Feb-2019-aoda.pdf

Mayer, J. (2017, October 11). Industrial robots and inclusive growth. Retrieved September 20, 2019, from VoxEU.org website: https://voxeu.org/article/industrial-robots-and-inclusive-growth

McMillan, M. S., & Harttgen, K. (2014). What is driving the “African Growth Miracle”? (Working Paper No. 20077). https://doi.org/10.3386/w20077

Micco, A. (2019). The Impact of Automation in Developed Countries (No. wp480). Retrieved from University of Chile, Department of Economics website: https://ideas.repec.org/p/udc/wpaper/wp480.html

Mokyr, J., Vickers, C., & Ziebarth, N. L. (2015). The History of Technological Anxiety and the Future of Economic Growth: Is This Time Different? Journal of Economic Perspectives, 29(3), 31–50. https://doi.org/10.1257/jep.29.3.31

Newfarmer, R., Page, J., & Tarp, F. (2018). Industries without Smokestacks: Industrialization in Africa Reconsidered. Retrieved from https://www.oxfordscholarship.com/view/10.1093/oso/9780198821885.001.0001/oso-9780198821885

Nordhaus, W. (1997). Do Real-Output and Real-Wage Measures Capture Reality? The History of Lighting Suggests Not. In T. F. Bresnahan & R. J. Gordon (Eds.), The economics of new goods. Chicago: University of Chicago Press.

Nuvolari, A., & Russo, E. (2019). Technical progress and structural change: A long-term view (No. 2019/17). Retrieved from Laboratory of Economics and Management (LEM), Sant’Anna School of Advanced Studies, Pisa, Italy website: https://ideas.repec.org/p/ssa/lemwps/2019-17.html

OECD. (2019). Determinants and impact of automation: An analysis of robots' adoption in OECD countries. https://doi.org/10.1787/ef425cb0-en

Oldenski, L. (2016). Reshoring by US Firms: What Do the Data Say? Retrieved from https://www.piie.com/publications/policy-briefs/reshoring-us-firms-what-do-data-say

Organisation for Economic Cooperation and Development. (2019). Real minimum wages. Retrieved September 20, 2019, from OECD.Stat website: https://stats.oecd.org/Index.aspx?DataSetCode=RMW#

Organization for Economic Cooperation and Development. (2019). Market concentration. Retrieved September 19, 2019, from https://www.oecd.org/daf/competition/market-concentration.htm

Rodrik, D. (2018). New Technologies, Global Value Chains, and Developing Economies (Working Paper No. 25164). https://doi.org/10.3386/w25164

Schmitt, J., Shierholz, H., & Mishel, L. (2013). Don’t Blame the Robots: Assessing the Job Polarization Explanation of Growing Wage Inequality. Retrieved from https://www.epi.org/publication/technology-inequality-dont-blame-the-robots/

Simons, B. (2019). Why “Leapfrogging” in Frontier Markets Isn’t Working. Retrieved September 20, 2019, from Center For Global Development website: /publication/why-leapfrogging-frontier-markets-isnt-working

Statista. (2019). Global car sales 1990-2019. Retrieved September 20, 2019, from Statista website: https://www.statista.com/statistics/200002/international-car-sales-since-1990/

Subramanian, A. (2018, October 15). Everything You Know about Cross-Country Convergence Is (Now) Wrong. Retrieved September 20, 2019, from PIIE website: https://www.piie.com/blogs/realtime-economic-issues-watch/everything-you-know-about-cross-country-convergence-now-wrong

Sun, I. Y. (2017). The next factory of the world: How Chinese investment is reshaping Africa.

Szirmai, A. (2009). Industrialisation as an engine of growth in developing countries (No. 010). Retrieved from United Nations University - Maastricht Economic and Social Research Institute on Innovation and Technology (MERIT) website: https://ideas.repec.org/p/unm/unumer/2009010.html

Tilly, C., & Carré, F. J. (2017). Where bad jobs are better: Retail jobs across countries and companies. Retrieved from http://public.eblib.com/choice/publicfullrecord.aspx?p=5050423

Winick, E. (2018, January). Every study we could find on what automation will do to jobs, in one chart. Retrieved September 17, 2019, from MIT Technology Review website: https://www.technologyreview.com/s/610005/every-study-we-could-find-on-what-automation-will-do-to-jobs-in-one-chart/

World Bank. (2019). World Development Report 2019: The Changing Nature of Work [Text/HTML]. Retrieved from https://www.worldbank.org/en/publication/wdr2019

Yeboah, F. K., & Jayne, T. S. (2016). Africa’s Evolving Employment Structure (No. 259511). Retrieved from Michigan State University, Department of Agricultural, Food, and Resource Economics, Feed the Future Innovation Lab for Food Security (FSP) website: https://ideas.repec.org/p/ags/miffrp/259511.html

[1] (Brynjolfsson, Rock & Syverson, 2017)

[2] (Frey & Osborne, 2017)

[3] (Winick, 2018)

[4] (Arntz, Gregory & Zierahn, 2016)

[5] (Rodrik, 2018)

[6] Ibid.

[7] (Rodrik, 2015)

[8] (Acemoglu & Restrepo, 2017)

[9] (Anslow, 2016)

[10] (Arruda, 2017)

[11] (Lebergott, 1966; Bureau of Labor Statistics, 2019a)

[12] (Autor, 2015)

[13] (Greenberg, 2018)

[14] (Nordhaus, 1997)

[15] (Bessen, 2017)

[16] Ibid.

[17] (Mokyr, Vickers & Ziebarth, 2015)

[18] (Atkinson and Wu, 2017)

[19] (Mandel, 2017)

[20] (World Bank, 2019)

[21] (Bessen, 2016)

[22] (Bureau of Labor Statistics, 2019b)

[23] (Autor and Salomons, 2018)

[24] (Comin, 2014)

[25] (Chuah, Loayza & Schmillen, 2018)

[26] (Yeboah & Jayne, 2016)

[27] According to the IMF, advanced economies have been more exposed to automation of routine tasks and experienced a larger fall in investment good prices than developing countries. This will reflect the gap between “technically automatable” jobs and “economically automatable” jobs. Countries that have very cheap labor and a weak business climate will have a lot of technically automatable jobs that are not economically automatable. (Dao, Das, Koczan, & Lian, 2017)

[28] (Frey, 2019)

[29] (Allen, 2017)

[30] (Autor, 2014)

[31] (Graetz & Michaels, 2015)

[32] (Gordon, 2018)

[33] (Bloom, Jones, Van Reenen & Webb, 2017)

[34] A more positive take would be that in 1971–2, X researchers added 2,300 transistors to the chip each two years, today 18X researchers are adding 2.3 billion transistors to the chip in two years and similarly, the researchers in the economy as a whole are adding considerably more to GDP each year than their forebears. Nonetheless, TFP growth has fallen over that period. And for endogenous growth to continue, the same number of researchers have to continue to produce the same percentage increase in TFP, something that they are clearly failing to achieve. (Note also there has been an attack on the great inventions theory of economic history. Gerben Bakker, Nicholas Crafts and Pieter Woltjer (2017) looked at the sources of growth in the US between 1899 and 1941 using new sectoral TFP estimates that better account for labor quality. They conclude TFP growth was lower than previously thought and that it was not predominantly caused by Robert Gordon’s four “great inventions” (2000) or spillovers from those inventions including electricity. Instead, they argue for “the creative-destruction friendly American innovation system” as a whole.

[36] (Brynjolfsson, Rock, & Syverson, 2017)

[38] Atkinson & Wu (2017)

[39] Autor & Salomons (2018). Analysis of the impact of broader automation to date in Europe suggest minimal impact on employment overall (displacement being offset by increased product demand and net employment growth) but some evidence of skill-biased employment changes.

[40] Autor (2018)

[41] Autor (2019)

[42] Schmitt, Shierholz & Mishel (2013)

[43] (Hunt & Nunn, 2019). Bessen (2016) similarly suggests that automation has had a small negative effect on job growth in jobs that were low-wage occupations in the US in 1980 and a strong positive effect on high-wage occupations.

[44] (World Bank, 2019). Das and Hilgenstock (2018) estimate exposure levels to routinization for 85 countries since 1990. They suggest overall exposure is lower than for high-income countries (because so much labor is in low-skilled services), but for those countries more exposed there is greater evidence of labor market polarization (compared to little evidence overall). They also note that while the decline in the relative price of investment goods was a factor in labor displacement in high income countries, there is no evidence of such a decline in developing countries—which might help to explain the broad lack of polarization.

[45] World Bank (2019)

[46] Ibid.

[47] (Oldenski, 2016)

[48] (Bertulfo, Gentile & Vries, 2019)

[49] (Subramanian, 2018). There are concerns about its sustainability: Diao, McMillan and Rodrik (2017) note that rapid East Asian growth in the past was driven by a combination of structural change towards more productive sectors (out of agriculture) as well as productivity gains within sectors. The recent growth acceleration in Latin America has been driven largely by within-sector productivity growth while in Sub Saharan Africa it has been driven by sectoral change.

[50] Bivens & Shierholz (2018)

[51] Autor’s data on real weekly wages for different genders and education levels over time is similarly instructive. The decline is 1980 to early 1990s—although admittedly continued stagnation for men less than bachelors from then until about 2010—when they started to pick up again (Autor, 2019).

[52] (Bureau of Labor Statistics, 2019c; Bivens and Shierholz, 2018). Evidence from a new dataset of union membership in the US over the long term suggests that unions work: they have had a significant, equalizing effect on the income distribution over a long sample period that has stayed fairly constant over time (Farber et al., 2018).

[53] (OECD, 2019a)

[54] (De Loecker & Eeckhout, 2017). Similarly, De Loecker and Eeckhout suggest over the last 35 years we have seen a rise of price level relative to cost at the firm level of 1 percent a year—markups have gone from 18 to 65 percent, suggesting a dramatic rise in market power, and one concentrated in the top percentiles of the firm distribution.

[55] (Guirrero, 2019)

[56] (Blattman & Dercon, 2018)

[57] (Tilly & Carre, 2017)

[58] (Bessen, 2016). Computer-using occupations have been growing at 1.7 percent a year (partial automation can help). That said, non-computer using occupations in the same industry have been declining, with a net effect of computer use in industry of 0.45 percent.

[59] See for example Bachmann, Cim & Green (2018).

[60] (Gordon, 2018)

[61] OECD analysis of the distribution of robots finds they are disproportionately used in high-income countries (with China the only middle-income country in the top 10 of robot stocks worldwide) and in a few industries—75 percent of all robots are in transport equipment and electronic, electrical and optical equipment. Worldwide, there are fewer than a million robots in operation, 80 percent of which are in rich countries. The analysis also suggests that robots are associated with a decline in both low- and middle-skilled occupations in affected industries (rather than polarization), but that different categories of robots have heterogeneous impacts on different occupations, which vary by country (OECD, 2019b).

[62] (Furman and Seamans, 2018; Statista, 2019)

[63] (World Bank, 2019)

[64] (Mann & Puttmann, 2018)

[65] (Mayer, 2017)

[66] (Micco, 2019)

[67] (De Backer et al., 2018)

[68] (Giuntella & Wang, 2019)

[69] (Artuc, Basters & Rjikers, 2018)

[70] This might be because Mexico benefited from being able to import lower-cost inputs from the US thanks to automation. Regardless, effects were small. (Artuc, Christiaensen & Winkler, 2019)

[71] (Hallward-Driemeier & Nayyar, 2017)

[72] Rodrik (2018)

[73] Ibid.

[74] Ibid.

[75] (Szirmai, 2009)

[76] Herrendorf, Rogerson, and Valentinyi (2013) report that consumption of manufactured goods as a percentage of total consumption has been trending downwards for quite a while in rich countries, if less rapidly than food (services makes up the difference). Similarly, Baily and Bosworth (2014) report manufacturing employment share has been declining at the same percentage rate since about 1970, while the share in real GDP has remained fairly constant. Note manufactured goods share of expenditure in the US has fallen from 50 percent in 1970 to 34 percent in 2010 while manufacturing net imports have increased—suggesting considerable productivity gains. [US Manufacturing: Understanding its Past]

[77] (IMF, 2018)

[78] IMF World Economic Outlook April 2018 [chapter 3] notes that at the global level there has been a broadly parallel movement in manufacturing and employment shares reflecting the combination of rising productivity within countries combined with a movement of manufacturing jobs to lower-productivity developing countries.

[79] (Hallward-Driemeier & Nayyar, 2017)

[80] (McMillan & Hartgen, 2014)

[81] World Bank databank, https://data.worldbank.org/indicator/TX.VAL.MANF.ZS.UN?locations=ZG, accessed 10/1/2019.

[82] (Sun, 2017)

[83] (Nuvolari & Russo, 2019)

[84] (Hallward-Driemeier & Nayyar, 2017)

[85] Ghani and O’Connell (2014)

[86] (IMF, 2018)

[87] They also report that only registered manufacturing firms demonstrate convergence in India (and they see labor productivity four times the labor productivity of the rest of the economy). (Amirapu & Subramanian, 2015)

[88] (Eichengreen & Gupta, 2009). In rich countries they report that education, health, hotels and restaurants have seen what appears to be negative total factor productivity increases 1990-2005 across OECD countries, trade and transport has seen slow growth while posts and communications saw 7 percent per year TFP gains.

[89] (Barro & Lee, 2013)

[90] (Newfarmer, Page & Tarp, 2018)

[91] (Baldwin, 2019)

[92] In 2007, Alan Blinder estimated that “somewhere between 22% and 29% of all U.S. jobs are or will be potentially offshorable within a decade or two.”

[93] Countering fears that improved communication will help support concentration of production, Hjort and Poulsen (2019) exploit the rollout of submarine cable networks to find that, across 12 African countries, improved Internet connectivity is associated with an increase in high skilled jobs that more than offsets a slight decline in low-skilled jobs, leaving low-skilled workers employment rate higher than it as before the arrival of terrestrial Internet connections. The researchers also suggest rising productivity, firm entry and exports result [the arrival of fast internet and employment in Africa]. See also Cariolle, Le Goff and Santoni’s work on broadband infrastructure deployment (2019).

[94] Simons (2019)

[95] (Mastercard Foundation, 2019)

[96] (Hawkins, 2018)

[97] (Hruska, 2018)

Topics

CITATION

Kenny, Charles. 2019. Automation and AI: Implications for African Development Prospects?. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

More Reading

SPEECH

The Future of Global Development and Implications for Aid

Blog Post

Using Space to Spark Global Prosperity