Recommended

Blog Post

A Bank for the World?

The problems facing our world today defy borders. Combatting climate change, preserving nature and biodiversity, and reducing pandemic risks are now at the top of the global agenda. These risks and those associated with global bads such as pollution, conflict, and disasters disproportionately affect the poorest and most vulnerable, and join well-established issues of accumulating physical, human, and institutional capital as part of the development mission. As these threats evolve, there is also a growing rationale for taking a global public goods (GPGs) approach to tackling them.[1]

As one of the only truly global institutions, the World Bank is uniquely positioned to be the world’s premier source funding for GPGs given its: (i) presence across countries and in sectors related to GPGs (climate, health, conservation, knowledge/R&D); (ii) experience in handling funds—including being entrusted by donors—and in financial markets; (iii) global governance structure and finance, foreign, and development ministry leadership on its Board; and (iv) substantial analytical capacity.

But despite its global coverage, the World Bank has never truly been oriented towards global challenges.[2] Its mission has been defined primarily by individual developing country problems and priorities. This country-model approach needs updating for a world in which the consequences of shared challenges are truly global, but where action against them may be needed—depending on the specific challenge—across a wide range of countries. The challenge ahead for shareholders is how to best evolve the existing institution—which has developed over a very long period—into a new one, quickly.

The World Bank is already a major source of external finance for global public goods.

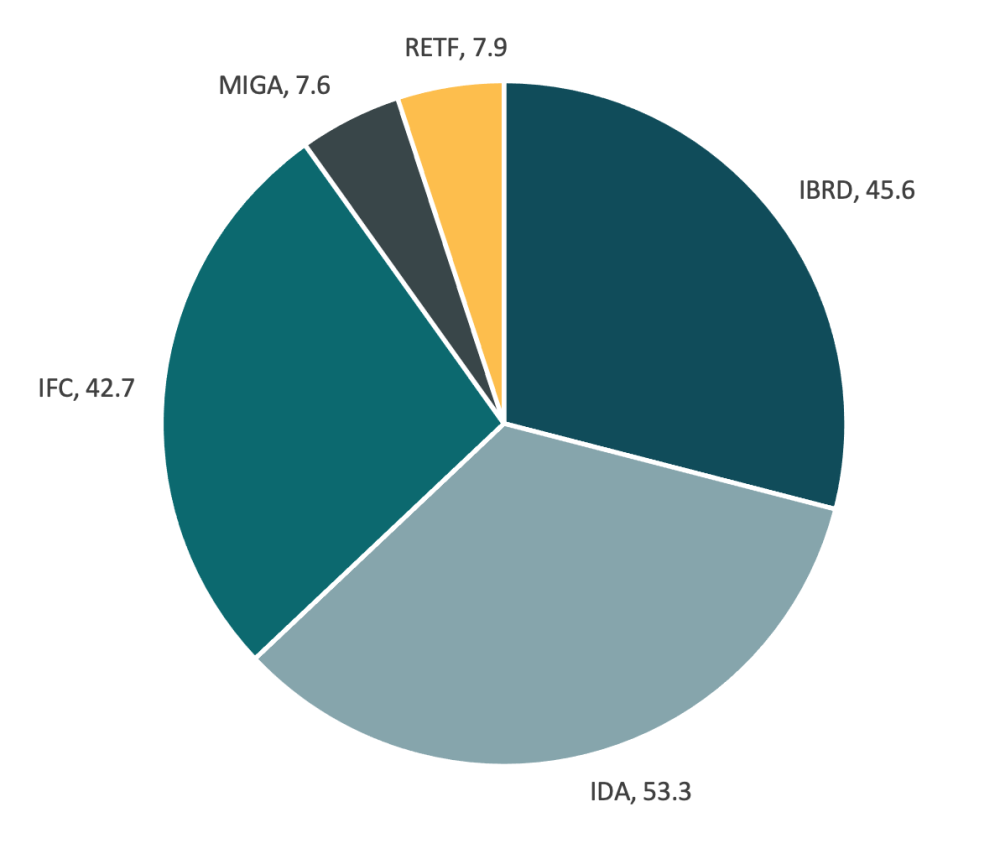

Using its existing IDA and IBRD country-based lending model, the World Bank is already providing large-scale financing for climate, pandemic, and disaster response, and other global public goods. Between 2015 and 2021, for example, the World Bank committed $109 billion to climate finance, with annual commitments now exceeding $20 billion.[3] Likewise, as part of the COVID-19 response, the Bank has deployed over $157 billion (in short-term finance, mobilization, and recipient-executed trust funds) over a 15-month period from April 2020 through June 2021, dwarfing any other source of external finance to low- and middle-income countries (Figure 1).[4]

Figure 1. Breakdown of World Bank Group commitments to COVID-19 response, April 1, 2020 – June 30, 2021 (in US billions)

Note: IBRD: International Bank for Reconstruction and Development; IDA: International Development Association; IFC: International Finance Corporation; MIGA: Multilateral Investment Guarantee Agency; RETF: Recipient Executed Trust Funds

But financing for GPGs must be much larger and more effective to make a meaningful and measurable difference.

The scale of the financing requirements to address global public bads vastly exceeds the World Bank’s current financing capacity, if needs estimates are reliable. The COP26 outcome document estimated that an additional $100 billion of financing was required for the long-term climate transitions needed to meet the global emissions goal, for example.[5] And while these financing requirements grow, the World Bank’s current contributions remain modest—at least pre-COVID—representing a small and shrinking share of client countries’ domestic financing over time, particularly in IBRD countries. The effectiveness and contribution of the Bank’s and countries’ investments against global targets is not well documented, and the economic analysis of returns and trade-offs still incipient. More could be done with the Bank’s policy instruments (Development Policy Loans, Program for Results), investments, and analytical work to create incentives for progress against GPG goals. In our view, setting up a new GPG-type fund or enhancing existing funds is not the right starting point. The Bank should bring the GPG agenda onto its balance sheet as part of its core business. The most logical way of doing this is through a GPG capital increase where shareholders would design the financing and policy architecture that would guide this new agenda.

The global public goods imperative complements the country-based lending model but requires adjustments in approach and new tools that are more attractive to recipient countries.

Country demand is at the heart of the World Bank’s existing model and borrowing for GPG programs domestically often fits uneasily with restricted fiscal space and domestically determined policy priorities. And the calculus of a government’s demand for borrowing in this area is different depending on the salience of differing GPG to different kinds of countries. For example: poor countries with a heavy existing burden of communicable and non-communicable disease may place a different priority on pandemic preparedness than those with health systems that broadly keep pace with challenges. This may be true irrespective of the high probability of a new pandemic risk ahead. While an externality may be priced similarly across countries, this does not mean that each country’s willingness-to-pay (or borrow) will be similar. Externalities may also be priced differently across countries; the effects of climate change are large in emerging markets whereas the health impacts of the current pandemic are (perhaps) smaller in the lowest-income countries to date, for example. In addition, countries willing to borrow for GPG uses are often not the highest-priority countries for global progress against GPG targets.

The $8.5 billion package to help reduce South Africa’s reliance on coal announced at the COP26 climate summit in November stands out as a potentially important approach to incentivize politically difficult—and expensive—national energy decisions.[6] There are already efforts underway to replicate this model in other coal-heavy emerging markets like Indonesia, which would have to reduce emissions by 41 percent to meet its Nationally Determined Contribution (NDC).[7] But doing more of this kind of packaging requires longer-term and lower-cost instruments and advice.

The GPG agenda has been supported via trust funds and sometimes via coordination with financial intermediary funds (FIFs), but these are small in size and ad hoc in relation to the Bank’s core agenda.

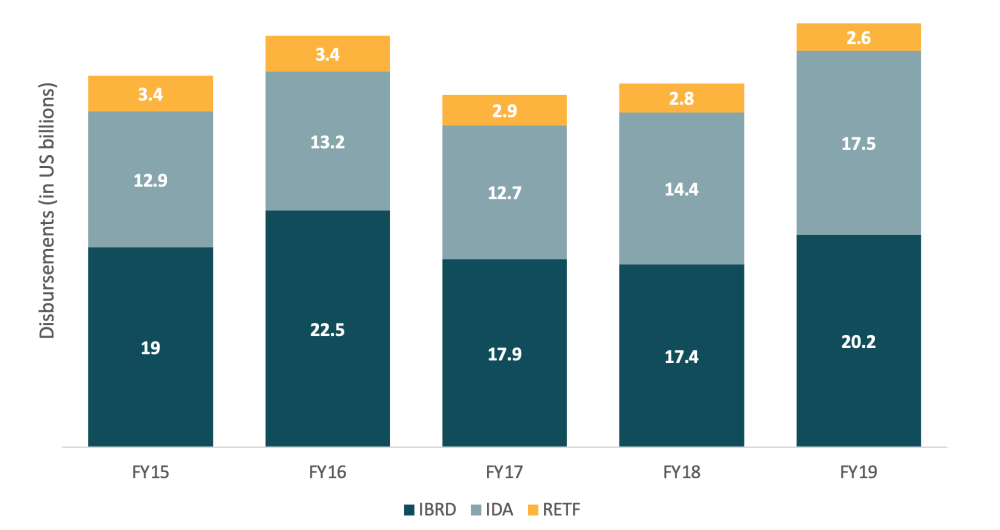

Disbursements from World Bank trust funds are marginal compared to those from IBRD and IDA (Figure 2). [8] A GPG agenda will need to consider how these structures interact more intentionally with the World Bank and MDBs more broadly. Supporting countries through the COVID-19 period, for example, has included a large volume of support for social protection; a much smaller share has been for the genuine GPG of stopping communicable disease transmission.

Figure 2. Disbursements from World Bank recipient-executed trust funds compared to IBRD and IDA, FY15-FY19 (in US billions)*

*Note: Chart includes overall data for recipient-executed trust funds, illustrating the relatively common use of trust funds across World Bank activities.

Alongside this, the Bank needs to directly confront trade-offs between development and GPG actions, and take a clear stand on where it makes sense to use the marginal dollar raised to address one or the other.

It may well be that in some countries, it is more efficient to use newly raised resources on development, until some absorption or returns bottleneck is reached, at which point spending shifts towards GPG priorities. In others, the marginal dollar may already be best spent on GPGs. In some cases, investments work towards both aims. The Bank has not developed a clear approach to this—and indeed, nor has anyone else. One way to address these tricky questions is to pursue a much larger increase in available resources via a capital replenishment, to take the sting out of trade-offs. We need much more money for both development and GPGs.

We need more money but also new policies, pricing, and incentives, and models of financing for GPGs.

There is an urgent need for leadership, analysis, and directed financing of different kinds in policy and operations that can drive long-term progress towards global goals. To operationalize these approaches, the Bank will not only need to find a practical way to define what is (and what is not) a GPG and measure externalities associated with investments, but also to understand the possibilities for differential subsidization of the externalities across projects of different kinds as well as countries at different income levels. One could argue that poor countries should expect subsidies of close to (or potentially greater than) 100 percent whereas middle-income countries might be expected to bear a larger share of the costs as part of their own funding for GPGs. Ultimately, the most important priority is to maximize achievements per dollar of resources available. This is an opportunity to show intellectual leadership, inform operations, and enable a more targeted system of financing for GPGs that will complement domestic investments and their returns. Set-aside and financing top-ups have helped the Bank generate country demand for GPG-type programs (i.e., the IDA regional refugee window), where countries receive extra financing above and beyond their regular country exposure for undertaking projects in specific areas. More should be done to define these strategies.

Any credible GPG agenda will also need to be underwritten by a large grants based-funding stream, including for middle-income countries.

Governments have little incentive to borrow to invest in programs where the benefits may not be directly captured by the country, but they still must repay the loan. This tension is likely to be particularly acute for GPGs around conservation and biodiversity, where the short-term economic losses could outweigh the national returns. One way to do this is to use IBRD’s net income to finance GPGs and bring reflows onto the IBRD balance sheet.

GPG solutions may require creative thinking and financing non-sovereigns in-country or at regional/global levels.

The difficulty in providing an early guarantee or lending to COVAX, the vaccine arm of the Access to COVID-19 Tools Accelerator (ACT-A), for example is a recent example of this kind of need.[9] The Bank’s lending tools are limited in these cases, and are constrained by the Bank’s financial framework, safeguard policies, and approach to risk. The Bank needs a mechanism to jointly accept and manage risks as shareholders when the client or counterparty cannot manage on its own and where the global stakes in avoiding negative outcomes are high. And there may be instances where financing to non-governmental organizations is vital in fragile or conflict-affected states, or where non-state actors are vital in determining the quality of economic data or disease surveillance, for example. Unlike IBRD, IDA’s charter allows it to provide grant financing to non-sovereigns, so this is an avenue worth exploiting further.

|

Table 1. Proposed modifications of the World Bank’s role in global public goods, according to World Bank staff (2007) |

|---|

| 1. Enhance cooperation with partner countries on the integration of country priorities and global/regional public goods 2. Strengthen its capacity for advisory services and lending related to global and regional public goods 3. Participate strategically in global partnerships 4. Explore new financing modalities for global public goods 5. Continue to promote informed debate on global issues, and advocate constructively for developing countries 6. Increase action at the regional level |

Source: Global Public Goods: A Framework for the Role of the World Bank, prepared for the 2007 Development Committee Meeting, prepared by the staff of the World Bank (2007) https://www.cbd.int/financial/interdevinno/wb-globalpublicgoods2007.pdf

We must take advantage of GPG tailwinds.

COVID-19, with the climate crisis on its heels, has made the GPG agenda—which the World Bank laid out a framework to achieve 15 years ago (Table 1)—more tangible and freshly relevant for many policymakers. This is a unique window of opportunity for the Bank and shareholders to advance and gain consensus around a bold agenda that truly equips the Bank for 21st century challenges. Shareholders may not be as far apart on this agenda as the politics suggest. Likewise, the 2022 G7 under the German presidency is an opportunity to find common ground and move ahead.

Finally, it’s not just about the money.

There is a clear hunger for the World Bank to be a leader on GPG issues, not only as a financier or vehicle. The Bank brings analytics, capacity building, and intellectual leadership to both country development and global challenges. In addition, the World Bank and multilateral development banks more broadly must interact with goal-setting and other kinds of planning efforts in different parts of the global system of organizations that work on GPGs, bringing country realities to bear and grounding financing requests.

Authors listed in alphabetical order. Thanks to Masood Ahmed, Scott Morris, and Alan Gelb for inspiration and comments.

[1] See Proceedings from a World Bank Workshop on Global Public Policies and Programs in 2001: https://ieg.worldbankgroup.org/sites/default/files/Data/reports/gpp.pdf

And a 2007 background report “A Framework for the Role of the World Bank”:

https://www.cbd.int/financial/interdevinno/wb-globalpublicgoods2007.pdf

And other literature:

https://www.cgdev.org/sites/default/files/CGD-Note-Birdsall-Diofasi-Global-Public-Goods-How-Much.pdf

https://ycsg.yale.edu/sites/default/files/files/meeting_global_challenges_global_public_goods.pdf

https://www.oecd.org/development/pgd/24482500.pdf

[2] https://www.cgdev.org/sites/default/files/world-bank-75-revised-3-26-15_0.pdf

[3] https://www.worldbank.org/en/news/factsheet/2021/10/29/10-things-you-didn-t-know-about-the-world-bank-group-s-work-on-climate

[4] https://thedocs.worldbank.org/en/doc/bb1b191f6b1bd1f932d0ddc5492987ec-0090012021/original/WBG-Responding-to-the-COVID-19-Pandemic-and-Rebuilding-Better.pdf

[5] https://ukcop26.org/wp-content/uploads/2021/11/COP26-Presidency-Outcomes-The-Climate-Pact.pdf

[6] https://ukcop26.org/political-declaration-on-the-just-energy-transition-in-south-africa/

[7] https://www.un-page.org/files/public/low_carbon_development-_a_paradigm_shift_towards_a_green_economy_in_indonesia_1.pdf

[8] There is a small GPG fund financed by IDA reflows but amounts and functions to date have been too small to yet be significant.

Topics

CITATION

Dissanayake, Ranil, Amanda Glassman, Clemence Landers, and Eleni Smitham. 2022. A Bank for the World: Better Terms and Conditions for Global Public Goods. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.