Recommended

REPORT

Building an EU-Africa Partnership of Equals

Despite their potential to achieve high development impact, projects in the poorest and most fragile countries, most in sub-Saharan Africa, are chronically underfinanced by European development finance institutions and private investors owing to real or perceived low risk-adjusted returns. The External Investment Plan and its risk-mitigation tools, if structured right, have the potential to mobilise investment where the need is greatest. To make this happen, the new European Commission should

- clarify the strategic objectives of external investment and steer it towards leveraging high-risk capital for underserved markets;

- explicitly focus assistance on the poorest countries through clear project selection criteria;

- provide demand-driven technical assistance and operationalise policy dialogue to improve the business environment; and

- federate the development finance institutions focusing on steering policy, encouraging best practice, and harmonising procedures and results amongst the development finance institutions and multilateral development banks.

The Challenge

The fundamental challenge at the heart of achieving the Sustainable Development Goals (SDGs) by 2030 is finance—especially mobilising private finance to ramp up development financing from “billions to trillions” of dollars. Almost every development finance institution (DFI) in Europe has made catalysing private capital a primary goal. Yet despite repeated rhetoric, analysis, and piloting since 2015, the trillions are nowhere in sight.

The shortfall is particularly acute in low-income countries (LICs) and fragile states, most of which are in sub-Saharan Africa,[1] where the demographics are challenging, environmental degradation is rapid, financial markets are nascent, and institutions are weak. Although official development assistance (ODA) remains critical to these countries, it is not going to be sufficient for the next development “leap.” The International Monetary Fund estimates that to meet the SDGs, LICs will need to spend an additional half-trillion dollars annually until 2030. For many, that represents an additional 15.4 percentage points of GDP.[2] Add to this the 40 percent of LICs that are in, or at risk of, debt distress as governments borrow heavily from public and private lenders to fund social spending and infrastructure.[3] Achieving the SDGs will require piling more public debt on top of what has already been borrowed by LICs.[4]

The alternatives are more domestic resource mobilisation, more mobilisation of private infrastructure and other SDG-related investments, or more concessional lending by multilateral development banks and DFIs that LICs can better sustain. And yet finance for early-stage firms and early-stage infrastructure remains scarce; infrastructure developers and small and medium enterprises (SMEs) often cannot access long-term finance in their local currency; finance for the social sectors (e.g., education and social inclusion) has been even harder to come by than infrastructure finance; women SME owners are still usually last in line to receive finance; and finance at scale for small farmers and their producer-groups remains elusive.[5] Too many projects are just too nascent and too risky to attract investment.

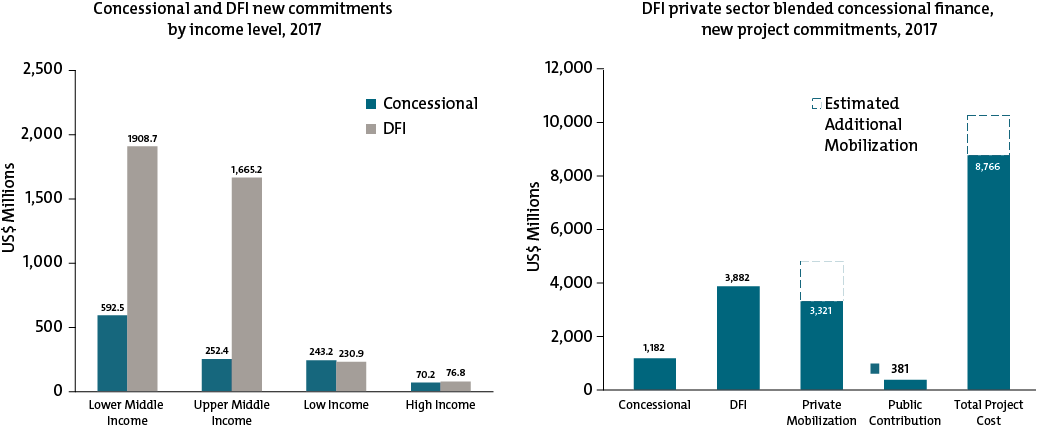

Multilateral DFIs commit just under $40 billion per year in finance for the private sector but only catalyse $60 billion in private finance.[6] Blended finance (the use of grants blended with finance on commercial terms) from multilateral DFIs amounted to only about $9 billion in 2017, or 22 percent of the total $40 billion. And the share of LICs in multilateral DFI blended finance is only about 6 percent, while the share of private finance mobilised by blended finance that goes to LICs is an even lower 4 percent.[7] So, to date, relatively little blended finance has been deployed to mobilise private finance and of that, very little goes to LICs (see figure 1).

Figure 1. A small portion of DFI blended finance goes towards mobilising private finance in the poorest countries

Source: DFI Working Group on Blended and Concessional Finance for Private Sector Projects, Joint Report, October 2018 Update.

Note: The blue bars in the above graph (right-hand side) show the numbers reported by all DFIs, including those that did not report private mobilization or total project cost. The white bar is an estimate of the additional private mobilization and total project cost that was not reported, based on the patterns of the institutions that reported these numbers.

However, the problem is not a lack of money or tools. It is that DFIs are not incentivised to make riskier investments in underserved markets due to operational, institutional, and behavioural impediments. The failure to shift towards catalysing finance rather than lending for their own account, to take more risk, to combine policy reform and project finance, to work together as a system, and to think and act globally has severely hampered the critical role of the DFIs in contributing to the achievement of the SDGs.[8] Part of the problem is the DFIs’ shareholders—DFIs are held accountable by their shareholders first and foremost for the volume of their own business and returns. Returns can trump mobilisation ratios, leading DFIs to focus on lending rather than more catalytic but less profitable tools, such as guarantees.[9] Furthermore, shareholders want to preserve triple-A ratings and at the same time finance impactful projects. But this is contradictory.

The European Union’s Added Value and Its Progress to Date

Collectively, the European Union (EU) invests more ODA in developing countries than the rest of the world combined. But the impact of that investment has, to date, been limited, partly as a result of the EU’s development finance architecture, which has been designed incrementally, responding to the needs of the moment.

There have been three notable trends in EU development finance during its current financial period (2014–2020):

- A marked shift in the deployment of EU grant finance towards blended finance and guarantees

- An increase in the number of actors eligible to access investment support

- A proliferation of new tools and modalities, which has led to a highly complex architecture

The External Investment Plan

In 2017, the European Commission launched an ambitious programme of investment mobilisation in Africa and the Neighbourhood: the External Investment Plan (EIP). Implicit in its creation is the EU’s ambition to rival the growing influence of China, whose vast programme of investment on the African continent has left other donors scrambling to catch up. The EIP aims to increase the scale, impact, and coherence of EU-supported external investment by introducing various innovations to the European financial architecture.

The EIP has two important components: (1) a guarantee mechanism to European and non-European DFIs and private investors; and (2) a unique “three pillar” approach to investment support which complements financial tools (pillar 1) with non-financial technical assistance aimed at building a project pipeline (pillar 2) and improving the business environment in partner countries through policy dialogue (pillar 3). The EIP’s financial arm, the €4.1 billion European Fund for Sustainable Development (EFSD), comprises a guarantee fund (for a total of €1.5 billion by 2020) and blended finance facilities (for a total of €2.6 billion by 2020).

The EIP is a positive development. Its ambition in scale, thematic and geographic coverage, and risk-sharing tools is unrivalled. Its three-pillar approach has the potential to significantly improve the quality and development impact of EU-supported investments. And it already has had some success in incentivising coordination and joint initiatives between DFIs. Most importantly, as the purpose of the guarantee is to cover losses of the counterparts in the event of default, it has a vital role to play in pushing the DFIs beyond “business as usual” and incentivising them to mobilise investment for higher-risk markets. But is it actually doing this? To date, the evidence suggests that the answer is no.[10]

The EIP is troubled by a lack of a clear policy steer on its multiple, ambitious objectives. It seeks to leverage private finance, focus on jobs and growth, tackle the root causes of migration, reach the poorest and most vulnerable, improve the investment climate, and at the same time, encourage innovation, demonstrate impact, and contribute to the SDGs. Its financial arm, the EFSD, has been designed accordingly, with maximum flexibility to respond to these various aims. It is this breadth and flexibility that has led to ambiguity over the EFSD’s primary purpose. It is particularly unclear whether the EFSD is intended to operate primarily as a high-leverage fund (mobilising the maximum quantity of investment for a given input of EU budgetary resources) or as a high-risk fund (mobilising investment for underserved markets with low risk-adjusted returns). Yet there is an inherent trade-off between the two: programmes with lower risk-adjusted returns will require larger injections of grant finance, either via blending or guarantees, to be commercially viable. That is, a higher risk fund will achieve lower leverage and vice versa.

Furthermore, the flexible framework has resulted in a user-driven approach to allocating EFSD resources. While the Commission has defined five thematic investment windows to guide the fund’s operations, their scope is extremely broad, and their budget is deliberately undefined. Moreover, the criteria for selecting investment proposals for EU support are vague and relatively subjective. Consequently, DFIs have maximum flexibility to propose investment programmes that suit their objectives, specialisation, and appetite for risk. Without any political steer or competitive incentive, DFIs are unlikely to undertake more complex or risky investment programmes that are struggling to get off the ground. Rather, they may simply use the EFSD’s risk-sharing tools to increase the expected return of investment that is slightly suboptimal or, worse, already commercially viable.[11]

The real question then is whether the EFSD is resulting in additional investments or just subsidising investments that would have otherwise taken place. The Commission assesses the additionality of each proposed investment programme using various criteria, including whether the EU guarantee would crowd-in private investment. However, neither the criteria nor the assessments are published. Anecdotal evidence suggests that the EFSD may not be pushing DFIs much beyond their day-to-day operations and that, in some cases, the EFSD is merely subsidising DFIs’ business as usual.

The New Investment Framework

In 2018, the Commission released a series of proposals for the next Multiannual Financial Framework 2021–2027, including a new investment framework for external action. The intention was to significantly scale up the EIP while also streamlining the EU’s external investment architecture. The proposed framework—the EFSD+—would adopt the same approach as the EIP but with an expanded financial arm comprising the EU’s regional blended finance facilities folded into a global blending facility and a new External Action Guarantee (EAG), replacing the current EFSD, with a ceiling of €60 billion. It would sit within the new Neighbourhood, Development and International Cooperation Instrument of €89.2 billion, with each operation funded from the instrument’s geographic envelope. The EAG would have a provisioning rate of 9 to 50 percent, suggesting that between €5.4 billion and €30 billion of the instrument’s total budget could be dedicated to guarantee operations.

Like with the current EFSD, the EFSD+ has multiple objectives: to foster sustainable and inclusive economic and social development and growth; to create decent jobs and economic opportunities; to eradicate poverty; to foster entrepreneurship; and to address the specific socioeconomic root causes of irregular migration. It focuses special attention on countries experiencing fragility or conflict, least developed countries, and heavily indebted poor countries. However, this approach of “letting a thousand flowers bloom” gives maximum flexibility to the multilateral development banks and DFIs to design investment programmes that they would do anyway.

Like the EFSD under the current system, the future EAG would be open to all eligible counterpart institutions (European and non-European), with a view to creating a level playing field. The difference relates to the treatment of the European Investment Bank (EIB). Under the current EU Multiannual Financial Framework (2014–2020), the EIB’s operations outside the EU benefit from an exclusive sovereign risk guarantee by the EU budget and the European Development Fund in African, Caribbean and Pacific countries. Under the proposed new investment framework, the EIB will lose this privilege and will need to compete alongside other multilateral development banks and DFIs for the EAG.

By removing the privileged position of the EIB, the Commission, through the proposed EFSD+, is positioning itself as the hub of the European development finance architecture. It will have the power to unilaterally change the priority areas, governance arrangements, and performance indicators of the EFSD+. This does, however, raise doubts about the capacity and expertise of the Commission to properly structure, manage, implement, and steer the whole process, particularly in terms of banking and financial expertise, which commonly rests with the multilateral development banks and DFIs rather than the Commission.

What Should the New Commission Do?

Despite their potential to achieve a high level of development impact, projects in the poorest and most fragile countries are chronically underfinanced by European DFIs and private investors because of real or perceived low risk-adjusted returns. The EIP and its risk-mitigation tools, if structured right, have the potential to mobilise investment where the need is greatest, in sub-Saharan Africa and beyond. To realise the EIP’s full potential, the new Commission should:

-

Clarify the EIP’s ultimate purpose and how it is translated into its financial arm. The EIP’s purpose should be to leverage high-risk capital for underserved markets, particularly in fragile environments with inherent political uncertainty, and to address real market failures.

-

Allocate blended finance and guarantees in a way that incentivises investment where there are gaps. If the Commission wants the private sector to invest, it will need to increase the return and reduce the risk through a combination of blended finance and guarantees. The EFSD+ should include project selection criteria that explicitly prioritise underserved markets.

-

Expand technical assistance and enabling environment support. Investment in high-risk environments requires extensive technical assistance during the pipeline development and project preparation stages, as well as ongoing improvements to the enabling environment. The Commission has the reach (139 delegations) to add value in these areas, yet progress in articulating and implementing these second and third pillars (technical assistance and policy dialogue, respectively) has been slow. It should earmark resources for pillars 2 and 3, clarify pillar access for the DFIs and multilateral development banks, and strengthen linkages between the pillars.

-

Capitalise on the Commission’s federating role to drive collective action, coordination, impact, and efficiency among the users of the EFSD and its successor, the EFSD+. It should focus on steering policy and encouraging best practice among the DFIs and multilateral development banks. And it should agree to standardised, general terms for the guarantee contracts, a common results framework to increase transparency and efficiency, and a common understanding of what constitutes impact. The EIP should be used as a platform for increased coordination and shared analysis.

[1] According to the World Bank, out of the 35 remaining low-income countries, 27 are in sub-Saharan Africa. See World Bank Lending Groups, https://datahelpdesk.worldbank.org/knowledgebase/articles/906519-world-bank-country-and-lending-groups.

[2] Gaspar, V. et al. (2019) “Fiscal Policy and Development: Human, Social, and Physical Investments for the SDGs,” International Monetary Fund Staff Discussion Notes No. 19/03, www.imf.org/en/Publications/Staff-Discussion-Notes/Issues/2019/01/18/Fiscal-Policy-and-Development-Human-Social-and-Physical-Investments-for-the-SDGs-46444.

[3] Lee, N. (2018) “Domestic Resource Mobilization in Low-Income Countries: Proposal for a Surge in Multilateral Support,” Center for Global Development Note, www.cgdev.org/publication/domestic-resource-mobilization-low-income-countries-proposal-surge-multilateral-support.

[4] Plant, M. (2018) “SDG Arithmetic,” Center for Global Development blog, www.cgdev.org/blog/sdg-arithmetic.

[5] Lee, N. (2019) “Trillions for the SDGs? Time for a Rethink,” Center for Global Development blog, www.cgdev.org/blog/trillions-sdgs-time-rethink.

[6] Ibid.

[7] DFI Working Group on Blended Concessional Finance for Private Sector Projects (2018) “Joint Report, October 2018 Update,” https://www.ifc.org/wps/wcm/connect/3aaf1c1a-11a8-4f21-bf26-e76e1a6bc912/201810_DFI-Blended-Finance-Report.pdf?MOD=AJPERES&CVID=mpvbN7c.

[8] Ahmed, M. (2019) “Financing Options for Low-Income Countries,” Center for Global Development blog, /blog/financing-options-low-income-countries.

[9] Lee, N. (2018) “The Eight Virtues of Highly Effectives DFIs,” Center for Global Development blog, www.cgdev.org/blog/eight-virtues-highly-effective-dfis.

[10] Gavas, M. and Timmis, H. (2019) “The EU’s Financial Architecture for External Investment: Progress, Challenges, and Options,” Center for Global Development Policy Paper 136, www.cgdev.org/publication/eus-financial-architecture-external-investment-progress-challenges-and-options.

[11] Ibid.

Topics

CITATION

Gavas, Mikaela. 2019. Redesigning the External Investment Plan to be a Game-Changer for Africa. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.