Recommended

On a slower connection? Download a smaller (2mb) version of the report.

There have been impressive gains in global health over the past 20 years, with millions of lives saved through expanded access to essential medicines and other health products. Major international initiatives backed by billions of dollars in development assistance have brought new drugs, diagnostics, and other innovations to the fight against HIV, malaria, tuberculosis, and other scourges. But behind these successes is an unacceptable reality: in many low- and middle-income countries, lifesaving health products are either unavailable or beyond the reach of the people who need them most. While each country’s context is unique, a reliable, affordable, and high-quality supply of health products is a vital necessity for any health system. In its absence, lasting health gains will remain elusive.

Access to medicines, diagnostics, devices, and equipment is driven in large part by the efficiency of their procurement. Procurement is, therefore, central to the efforts of low- and middle-income countries to improve health, meet the Sustainable Development Goals, and achieve universal health coverage. Health product purchasing in low- and lower-middle-income countries already makes up a sizeable share of overall health spending; in fact, in just a subset of these countries, spending on health products totals an estimated $50 billion per year.[1] Procurement is not only essential to the missions of global health entities like the Global Fund, Gavi, UNICEF, UNFPA, and PEPFAR, but it also represents big money. In the case of the Global Fund, health product procurement accounts for $2 billion per year,[2] or almost half of its 2017 disbursements.[3] Yet despite its importance, procurement is an underappreciated health system function. Today’s procurement systems are hobbled by inefficiencies that leave some of the poorest countries paying some of the highest drug prices in the world.

Within a changing global health landscape, a forward-looking approach is needed to anticipate tomorrow’s challenges and plan for the future. To this end, the Center for Global Development convened the Working Group on the Future of Global Health Procurement to review the evidence and formulate recommendations for how the global health community—international health organizations, their bilateral and foundation donors, and low- and middle-income countries—can ensure the medium- to long-term relevance, efficiency, quality, affordability, and security of global health procurement. Importantly, the group limited its focus to the procurement process: the journey of a health product from manufacturer to a centralized warehouse or other wholesaling facility. The downstream supply chain and delivery process—a product’s journey from warehouse to end user—was beyond the Working Group’s scope.

The triple transition in global health procurement

Global health procurement needs are evolving rapidly as countries face a triple transition:

First, with income levels rising, low- and middle-income countries face the prospect of a transition from donor aid. Health products procurement, especially in low-income countries, remains heavily reliant on donors; making up for lost financing following donor exit will stretch already-strained national health budgets. Many low-income and lower-middle-income countries also have limited experience and capacity in procurement-related functions.

Second, low- and middle-income countries face an epidemiological transition. As countries become wealthier, disease burdens shift from infectious to noncommunicable diseases such as cardiovascular disease, cancer, and diabetes. To meet their citizens’ evolving health needs, governments will need to purchase and make available a very different set of health products from those procured today.

Third, countries face a transition in health system organization as they move away from siloed disease-specific programs and out-of-pocket spending toward universal health coverage. As more governments commit to protecting their citizens against catastrophic health spending, national or subnational procurement processes will be a cornerstone of equitable and universal access to health products. Achieving universal health coverage within tight budgets will require national governments and their global health partners to make procurement decisions that deliver the most value for money.

Key insights on health product markets in low- and middle-income countries

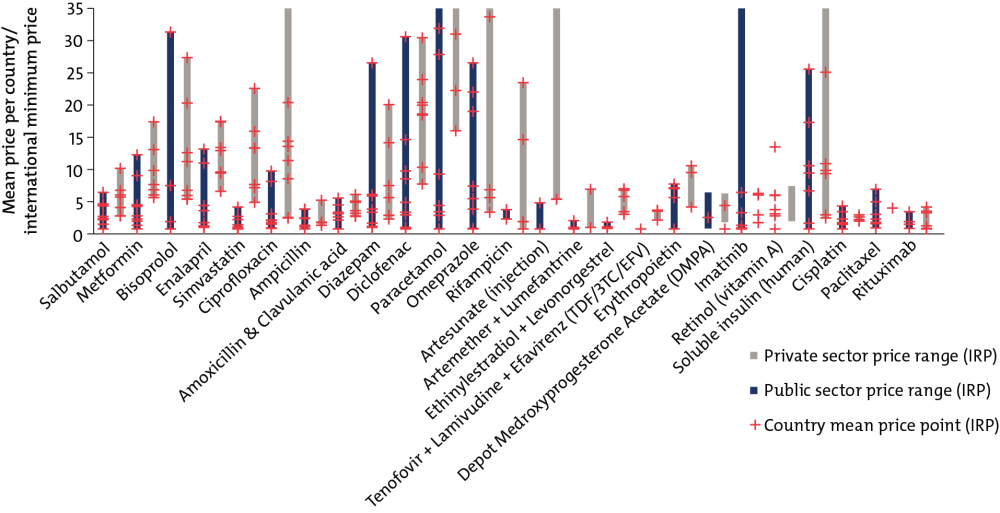

Key insight 1: In low- and middle-income countries, prices for basic generic medicines can vary and far exceed wealthy-country prices.

Purchasers in low- and middle-income countries pay as much as 20 to 30 times a minimum international reference price for basic generic medicines like omeprazole, used to treat heartburn, or paracetamol, a common pain reliever

Price Variation Across Seven Low- and Middle-Income Countries for Generic Pharmaceutical Products

Comparison of public and private pharmaceutical procurement prices (US$) across countries, relative to international minimum price

For source and notes see full report. Data copyright IQVIA AG and its affiliates. All rights reserved. 2017.

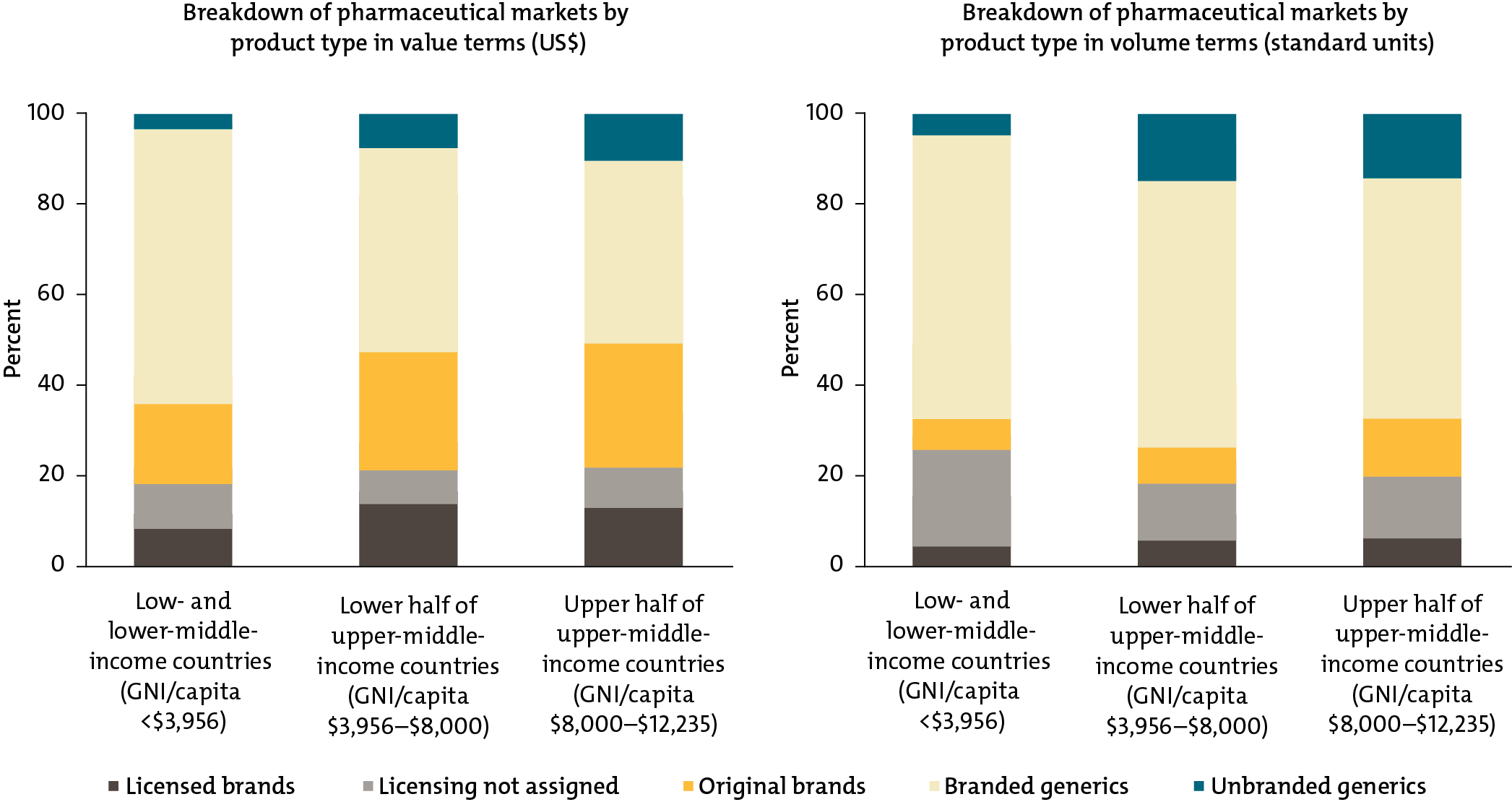

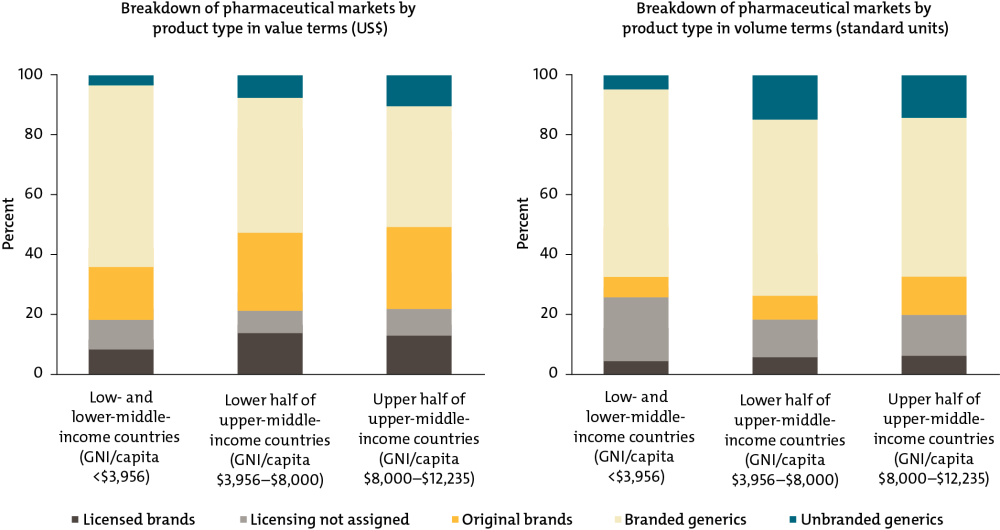

Key insight 2: Low- and middle-income countries disproportionately purchase expensive branded generic drugs rather than cheaper unbranded generics.

In the poorest countries, branded generics—which command a price premium—make up about two-thirds of the market by volume and value. Unbranded generics, usually the least expensive option, are a tiny sliver, only 5 percent of the market by volume and 3 percent by value. In contrast, in the United States and the United Kingdom, unbranded quality-assured generics account for 85 percent of the pharmaceutical market by volume, but only about a third by cost.

Health Product Markets in Low- and Middle-Income Countries by Brand and Licensing Status

For source and notes see full report. Data copyright IQVIA AG and its affiliates. All rights reserved. 2017.

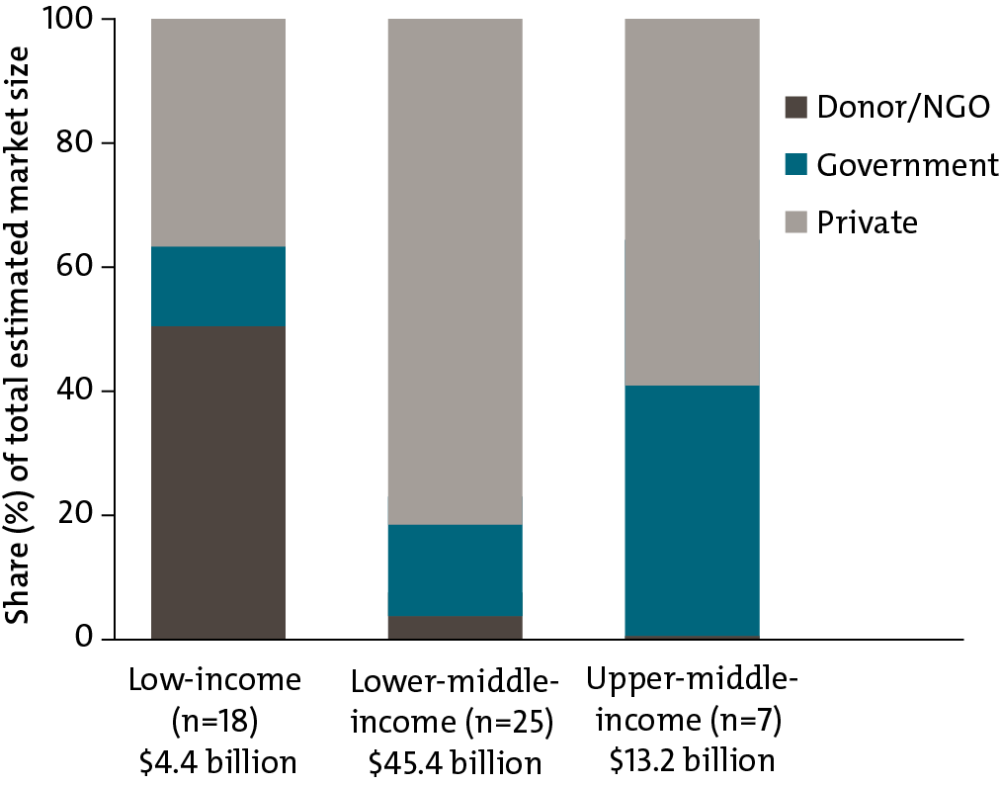

Key insight 3: As countries become wealthier, donor financing for health products becomes less important.

Donors account for half of all expenditure on health products in low-income countries; in contrast, in lower-middle-income countries, 80 percent of health products are procured through the private sector, where individuals pay directly for medicines out-of-pocket. Lower-middle-income country governments do not yet account for a large share of total purchasing in their countries for medicines and other health products.

Private, Government, and Donor/NGO Financing as a Share of the Total Estimated Market (Value) for Healthcare Products by Country Income Groups

For source and notes see full report.

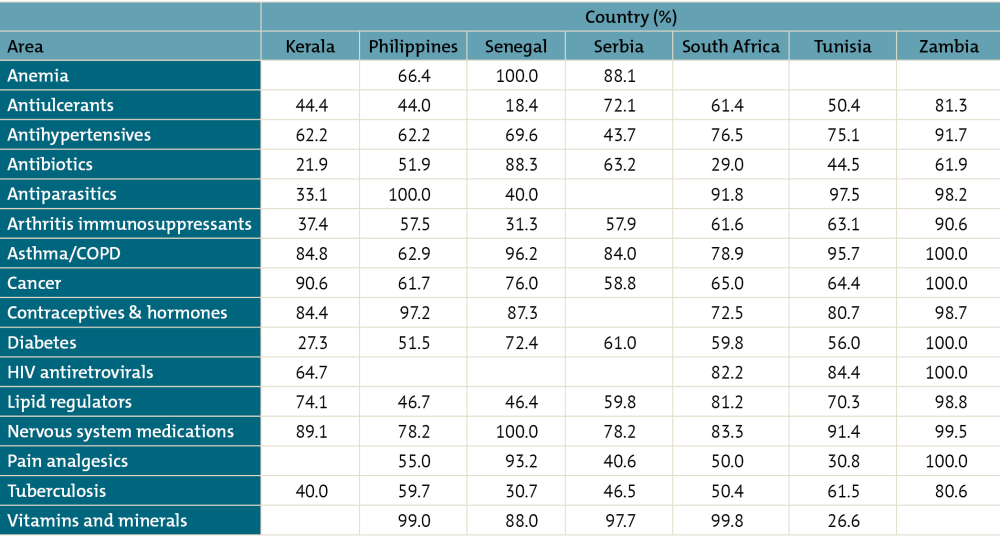

Key insight 4: There is little competition in the supply of essential medicines in low- and middle-income countries—these markets are dominated by a single or a small number of suppliers, which directly affects the prices paid by public procurers and consumers.

In some low- and middle-income countries, the largest seller of certain therapy and product classes accounts for upwards of 85 percent of all sales, such as contraceptives in Zambia, Philippines, Senegal, and Kerala; cancer medicines in Zambia and Kerala; diabetes medicines in Zambia; and antiparasitics in Philippines, Zambia, Tunisia, and South Africa.

One-Firm Concentration Index by Therapy Area for Selected Countries/States (Sample of 40 Molecules Only)

For source and notes see full report. Data copyright IQVIA AG and its affiliates. All rights reserved. 2017.

Institutional inefficiencies, market failure, and unorganized demand lead to suboptimal procurement outcomes

The Working Group found that a wide range of factors lead to suboptimal procurement outcomes—institutional inefficiencies, market failure, unorganized demand, supply chain and delivery challenges, and absolute resource constraints. The first three categories can be addressed, at least in part, by improved procurement policies and practices at the global, regional, and national levels.

Institutional inefficiencies include constraints related to the capacity of procurement entities and supporting institutions to create the right conditions for efficient and effective procurement. These include:

-

Institutional, administrative, and legal barriers, such as onerous registration processes, inefficient local purchasing preferences, and legal strictures against more effective procurement modalities, which artificially constrain competition, raise transaction costs, and inflate prices

-

Inefficient product selection, which directly affects what is purchased and can thus lead to inefficient use of scarce budgetary resources for health

-

Limited procurement capacity and expertise across the entire procurement process, which can lead to suboptimal procurement outcomes

-

Inadequate and inconsistent tracking, monitoring, and evaluation, which limit the ability to track and effectively manage products along the supply chain and identify effective procurement instruments and reforms

-

Parallel and duplicative supply chains, which drive inefficiencies and undermine efforts to build national capacity

Market failure occurs when free-market forces lead to an inefficient distribution of goods and services. Several characteristics of global health commodity markets make them susceptible to market failure and create welfare losses for producers, consumers, and society as a whole. These include:

-

Imperfect information about product quality, which may allow substandard products to enter and/or dominate the market and/or lead consumers to pay higher prices for branded generics that signal quality

-

Barriers to entry (e.g., the costs to receive approval for a generic equivalent or register an existing generic in a new market), which may prevent new suppliers from entering the market, thereby limiting competition and potentially raising prices

-

Externalities that shift costs and benefits beyond the user of a given product may, for example, lead to the overuse and misuse of antibiotics, undermining their efficacy, or lead to underuse of a relatively expensive vaccine with important global benefits

-

Public and common goods in global health—such as antimicrobial efficiency and research and development on new health technologies—lead to diffuse benefits to all of society and thus actors may have insufficient incentives to invest in, purchase, conserve, and/or provide such products

-

Present bias, whereby people undervalue preventative health measures, may contribute to low expenditure on preventive health technologies such as contraceptives, bed nets, or immunization

-

Principal-agent problem, which occurs when purchasers (agents) face strong personal or financial incentives that do not align with the interests of end users—for example, different levels of risk aversion or the opportunity for kickbacks from suppliers

-

Anti-competitive behavior, which can involve unilateral practices that a dominant firm uses to exclude rivals or explicit or tacit agreements between firms to set prices above market-clearing rates

Unorganized demand—including relatively low levels of pooling/high levels of procurement fragmentation coupled with uncertain and unreliable demand—can, under some circumstances, also contribute to procurement inefficiency. The high transaction costs in serving fragmented markets are oftentimes passed down to purchasers. This includes:

-

Fragmentation of demand in the case of products purchased in small quantities may lead to high transaction costs, prevent suppliers from entering low-volume markets, and/or deter suppliers from offering preferential pricing

-

When demand is uncertain and/or unreliable, suppliers may limit investment in research, development, and manufacturing capacity

Four recommendations for reform

We propose four recommendations for smarter, more strategic procurement policy and practice. Together, these recommendations offer a vision for how today’s global health procurement bodies can reimagine and redefin their roles to stay relevant in a changing world.

-

Sustain and expand global cooperation for procurement and targeted innovation. The global community should seek to sustain and possibly expand global cooperation to address specific global challenges—particularly supply security and targeted innovation—even after most countries transition from current global health mechanisms. Avenues for continued or expanded global cooperation should include pooled demand or cooperative purchasing; targeted investments in research and development; monitoring and managing the supplier landscape; information sharing, market intelligence, and e-platforms; support to nascent and start-up private sector innovations; common standards and principles for quality assurance; and continued subsidy for specific products—that have important positive externalities or that are marginally cost-effective, for example—even after countries have largely transitioned from external aid.

-

Reform WHO guidance and policy to support modern and agile procurement policy and practice. To reassert itself as the global standard-setting body and better support modern and agile procurement policy and practice, the WHO should set and execute a prioritized guidance reform agenda, which may include expanding efforts to facilitate common or expedited drug registration at the country level; providing guidance on and working with countries to adapt the WHO essential medicines, diagnostics, and medical devices lists and technical guidance to local contexts and resource constraints; and comprehensively updating guidance for pharmaceutical policy.

-

Professionalize procurement by building capacity and driving strategic practice. A concerted push is needed to professionalize procurement and broaden capacity from the global to national level. A partnership or network of existing entities including procurement universities or accreditation bodies, multilateral institutions, and resource platforms could support the creation of the following components: Procurement University; mentoring and exchange, including through a community of practice or learning network; global health-specific procurement guidance including toolkits, decision trees, and other resources; standardized set of performance measures for global health procurement; and evaluation of procurement policies and approaches.

-

Support in-country procurement policy reform. Global funders interested in ensuring more efficient national procurement processes and sustainable access to essential global health products should provide dedicated support to governments leading in-country procurement policy reforms. Potentially, development policy lending from the International Bank for Reconstruction and Develop¬ment or IDA could be leveraged to facilitate procurement reforms, with attention to ensuring that there is domestic leadership and commitment. Country-led procurement reforms should consider the following dimensions: purchasing and contracting modalities, procurement-related functions, industrial policy requirements, and product regulation.

[1] This estimate is based on a subset of 43 countries: 18 LICs and 25 LMICs where spending on global health products totals $4.4 billion and $45.4 billion, respectively; /publication/initial-estimation-size-health-commodity-markets-low-and-middle-income-countries

[2] The Global Fund. Procurement Strategies & Implementation with a focus on ARVs. May 2, 2017.

[3] Based on $4.2 billion annual disbursements for 2017. See https://www.theglobalfund.org/en/financials/

Topics

CITATION

Bonnifield, Rachel, Janeen Madan Keller, Amanda Glassman, and Kalipso Chalkidou. 2019. Tackling the Triple Transition in Global Health Procurement. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

More Reading

Blog Post

Big Lead is Still Downplaying the Harms