Recommended

Blog Post

The Bread and Butter of Global Health Financing

Blog Post

The 2024-2025 Replenishment Traffic Jam

The grants model: how we got here

Over the last twenty plus years, global health has benefited from the emergence of new financing models and “global health initiatives” (GHIs), including Gavi, the Vaccine Alliance and the Global Fund to Fight Aids, Tuberculosis, and Malaria.

These innovative GHIs were created to provide rapid reductions in mortality to address perceived slow responses by both the United Nation system e.g., the UNAIDS, World Health Organization (WHO) and international financial institutions, such as the World Bank. In the case of HIV/AIDS at least, the world has seen dramatic reductions in deaths and in new HIV infections over the past two decades, which has, in turn, contributed to equally dramatic reductions of health inequalities across countries.

However, staple features of the GHI model are now becoming risks: the reliance on large and fast spending usually bypassing government systems in the form of grants and the emergence of vertical single-focus agencies and channels (specific to a new disease, population, or technology). Over time, the model may display inflexibility to reforms that strengthen country ownership, ensure financial sustainability, and address new health challenges such as non-communicable diseases.

By failing to adapt to a changing world, GHIs risk perpetuating the incentives that gave little reason for governments to sustainably finance or deliver health services due to aid fungibility. This problem occurs when an additional (typically grant) dollar of development assistance fails to crowd-in—and may lead to a decrease in—domestic government financing. Worse, donor fragmentation and weak national health care resource tracking systems making financial flows less transparent and harder to coordinate. This is not to say that grant funding is not important (indeed, there should be a lot more of it), but it is not always well targeted or focused on leveraging the right financing or policy actions.

At a time when there are major financial rethinks occurring in the development finance world, the GHI system stands out for its relative lack of change. A key question is how many of the financial innovations occurring at the multilateral developments are relevant and applicable for the GHIs?

Towards a better grant allocation framework and financing transition

In the global health community, we need to first recognize that grant financing of vertical disease programs may no longer be the right tool for certain countries and health conditions. We should also accept that financing runs on a spectrum from grants to loans based on a country’s debt bearing capacity and its ability to self-finance, just as the International Development Association (IDA) uses the IMF-World Bank Debt Sustainability Framework to inform its allocation of grants. The global health community should embrace a similar mechanism to transition a country from grants to concessional finance.

A health financing transition refers to the changes in the prevailing pattern and the trade-offs between different sources of financing. One health financing transition is the transition between government health spending and out-of-pocket spending (government health spending increases as economies grow, which can reduce the share of out-of-pocket spending on total health spending). A second transition is between government health spending and external assistance (external assistance eventually reduces as government health spending increases). We propose a third and related transition in which the concessionality of external assistance tapers off as government health spending increases. Central to all three transitions is the increases in government health spending that not only reduce financial risks from medical impoverishment (as evident in the declining share of out-of-pocket in total health spending), but also in which the amount and the kind of external assistance eventually declines.

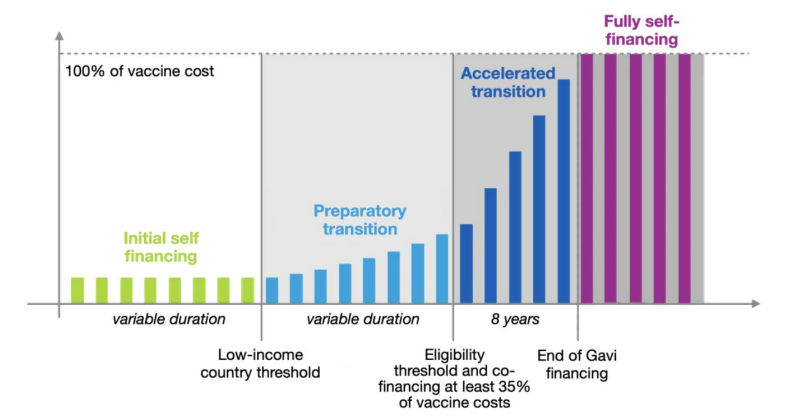

Of the global health funds that recognize this challenge, Gavi is perhaps the poster child with its clearly defined framework (unfortunately named the ‘cofinancing policy’ as we discussed here)—see annex figure. Allocations, eligibility, and domestic financing policy are the legs of a three-legged stool for which the grants sustainability framework must consider simultaneously, not separately. We’ve offered an illustration of how this sustainability framework could work, but it needs in-depth analysis (see Figure 1).

Figure 1. Illustration of a grant sustainability framework as third health financing transition

The framework for Gavi, however, also needs revision—because a country reaching middle-income status and facing the cliff of eligibility does not ensure sustainable financing. As Gavi revises its framework, it needs not reinvent the wheel. Meanwhile, PEPFAR—the largest and most life-saving bilateral health program in the world—is also considering introducing country domestic financing requirements.

To develop a plan for financial sustainability, not only do donors (and board members of global health funds) need to address eligibility, (grant) allocations, and domestic financing, policy makers also need to deliberately incorporate innovations in financing mechanisms and instruments as part of this plan.

What are major recent innovations in development finance?

The rise of the “hybrid model” for concessional funding

Multilateral development bank (MDB) funds have historically operated on a “cash-in, cash-out basis”, in which an MDB obtains the bulk of finances from donors during a regular fundraising exercise and then passes along these funds to countries as grants or cheap loans. But in recent years, several funds have reshaped their funding structures in profound ways that have added significant new resources.

In this regard, IDA has led the pack. IDA is the largest source of concessional and grant finance for the world’s poorest countries. Unlike the global health or climate funds, IDA provides both loans and grants to governments. IDA calibrates its terms to a country’s debt ratings and income. The poorest countries at high-risk of debt distress get pure grants, while other countries get varying levels of concessional terms.

This model has allowed IDA to provide significantly more financing to countries in recent years with the reflows accounting for more of IDA’s financing than donor contributions. This model has also allowed IDA to build up a significant equity base—to the tune of $180 billion. In 2018, IDA launched a new “hybrid financing model” and started going to capital markets to supplement reflows and donor grants as a major source of financing. IDA has been able to pass on much of its market borrowing to clients on concessional terms by blending its market loans with reflows and grants. As a result, donor grants accounted for only a quarter of contributions in the most recent IDA funding round, which achieved a $93 billion headline number.

IDA has not been the only fund to innovate its model. The International Fund for Agriculture and Development (IFAD), originally set up as a grant-making fund, became the first UN fund to receive credit rating, launching a borrowing program in 2020. More recently, in 2024 the Climate Investment Funds (CIF) launched a “Capital Markets Mechanism” and started issuing debt backed by their reflows. This could allow the CIF to increase their financing commitments by $500 million a year over the next ten years.

Proliferating donor guarantee mechanisms

MDB guarantees mechanisms are donor-backed funds that take risk off an MDB balance sheet by guaranteeing to backstop repayments for a subset of its loans, which in turn frees up fresh capital for new lending. They can be country-based (i.e. several countries guaranteed World Bank lending to Ukraine to allow the institution to expand its headroom in Ukraine beyond its prudential limits), or thematic—by guaranteeing a specific type of project. These include the International Finance Facility for Education (IFFEd), Innovative Finance Facility for Climate in Asia and the Pacific (IF-CAP) established by the Asian Development Bank, and the World Bank’s new Global Solutions Accelerator Platform (GSAP), which is a guarantee and hybrid capital mechanism to fund global challenges, including for health. While guarantee facilities offer relatively low-cost options for donors to ramp up MDB lending, they do not generate better lending terms. As a result, so far, they have only been relevant for middle-income countries (MICs) that borrow from the MDB hard loan windows.

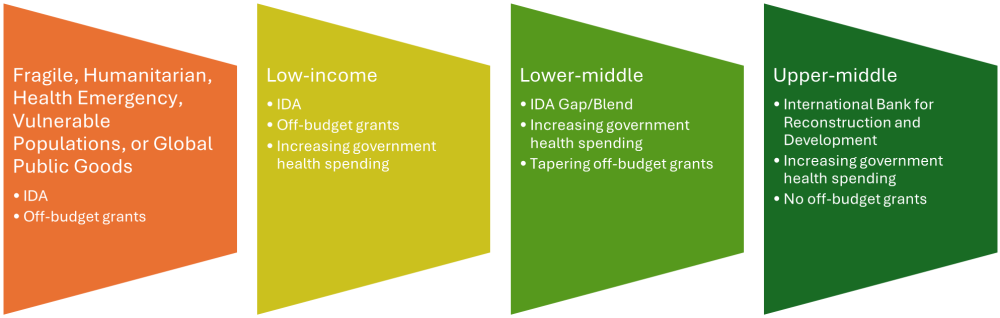

However, the MICs remain the big question mark in global health—with Gavi needing to adapt its middle-income policy to be more generous, whereas the Global Fund’s allocation methodology is largely driven by disease burden, and to a lesser extent, income levels resulting in 10 percent of allocations going to upper-middle income countries (see Table 1). The case for investing in upper-middle income countries still receiving substantial grants while not systematically considering joint or blended investment, needs strong articulation.

Table 1. Global Fund Allocations for 2023–25, by World Bank income group

|

Country income group |

Global Fund Allocations 2023–25 |

Share of Global |

Number of countries |

|---|---|---|---|

|

Low-income |

5,516 |

42.72% |

27 |

|

Lower-middle-income |

6,094 |

47.20% |

45 |

|

Upper-middle-income |

1,299 |

10.06% |

32 |

|

High-income |

2 |

0.02% |

1 |

|

Total |

12,911 |

100% |

105 |

Source: authors analysis of Global Fund 2023–25 allocations with regional recipients excluded. The sole high-income country receiving Global Fund support is Mauritius.

Innovations in health

Among the several innovative finance options tested in health, perhaps the more successful of models has been the bonds issued by the International Finance Facility Immunization (IFFIm). The IFFIm model works by receiving “long term, legally binding pledges from donor countries and, with the help of the World Bank, turns these pledges in Vaccine Bonds. Money raised via Vaccine Bonds provides immediate funding for Gavi’s immunization programs.” In short, IFFIm leverages donor pledges to issue debt and raise monies from international capital markets (even as the leveraged money, from our understanding, still needs to be repaid to bondholders). Such frontloading matters because it can allow for Gavi to shape the market for vaccines.

Following this approach, an IFFIm Contingent Finance Mechanism (CFM) has been discussed as part of the Day Zero Financing Facility (DZF), with planning underway with donors and the World Bank. More recently, WHO launched the Health Impact Investment Fund in collaboration with Regional Development Banks (RDBs) such as the European Investment Bank and Islamic Development Bank, and with a focus on primary health care investment.

What’s relevant for health funds?

In global health, the billion-dollar question is whether innovations in these financial models can be applied to other financiers besides IFFIm (and Gavi by extension). The Pandemic Fund, as well as the Global Financing Facility (see section 5.2 here) with linkages to the World Bank’s financing model, have already incorporated these blended financial considerations. The Global Fund has experimented with loan buydowns, including most recently in Indonesia.

Scaling this kind of ‘innovation’ will require changes in the Funds’ mandates and modus operandi and even in the culture and expectations of global health donors and recipients of aid. It is time for global health agencies, which have grown accustomed to grants, to mature and pivot to an IDA-type model, all while ensuring additional domestic government spending on health.

While rethinking the off-budget grants model, the global health community should also reconsider its value-add compared to the prevailing MDB country-level concessional model. Global health agencies as well as donors can consider the role of regional or multi-country pools as well as for aligning cofinancing policies such as the new joint MDB co-financing platform. In addition, at the country level, leveraging country platforms (see here and here) for better coordination and improved quality and quantity of funds may be attractive.

We are not advocating for wholesale transition of grants to loans. Indeed, there are logical and obvious reasons why grants are necessary and should even increase, particularly for global public goods, vulnerable populations, the poorest countries and health emergencies. But we think there is room to rethink the use, targeting and allocation of grants to make them as effective as possible.

With thanks to participants at the World Bank’s Asia-Pacific Health Financing Forum in Colombo, Sri Lanka over June 25-27, 2024, as well as colleagues from the Center for Global Development, WHO, and World Bank.

Annex Figure 1. Illustration from Gavi’s eligibility and transition policy document

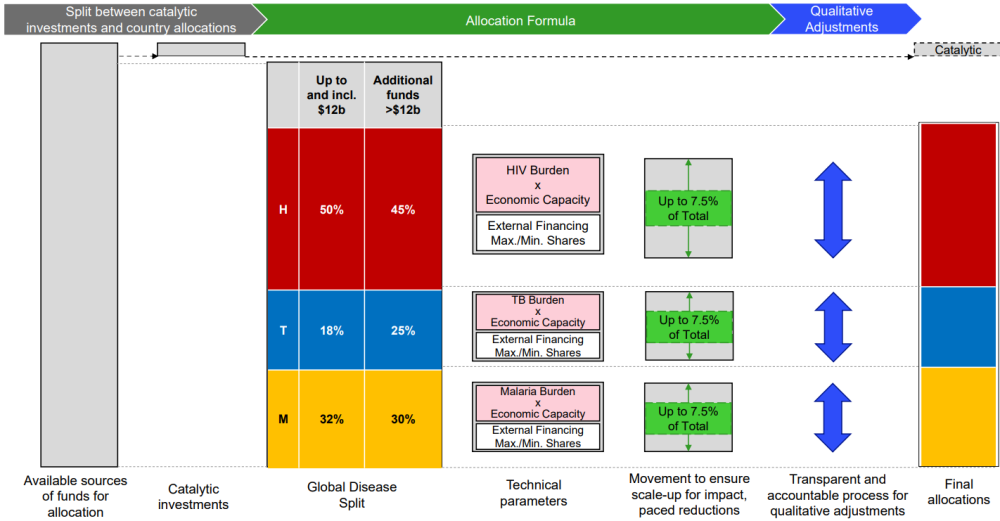

Annex Figure 2. Illustration from Global Fund’s GC7 allocation methodology

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: utah51 / Adobe Stock