Click here to read in Spanish.

How resilient would emerging market economies be if another global slowdown were to happen? In this case, past weakness may be a good gauge of future vulnerability.

Liliana Rojas-Suarez looked back at pre-crash conditions in 2007 (the year before the global financial crisis) in 21 developing and emerging economies and compared them to conditions at the end of 2014. In a new essay, she constructs a tool that allows countries to measure their economic and financial resilience to future shocks and compare their performance against each other.

It’s a resilience test for emerging economies, and this is what it shows:

- Latin American economies should be worried.

- India is more vulnerable now than in 2007.

- The Philippines is in a stronger position than in 2007.

Why This Matters

It matters for two main reasons. First, it works: Rojas-Suarez’s resilience test produces country rankings for 2007 that reflect the actual observed effects of the global financial crisis on emerging markets. It shows Emerging Europe economies to have been the most vulnerable in 2007: the same economies were among the worst hit in 2008.

Second, whichever way you think the barometer is pointing for advanced economies — either deflation that suppresses global demand or higher US interest rates that divert capital flows toward rich countries — there are tough headwinds coming for smaller, less robust economies and some countries that were once thought of as future powerhouses. Add to this lower prices for commodities and oil, and greater geopolitical uncertainty, and you start to see turbulent times ahead for developing countries and emerging markets.

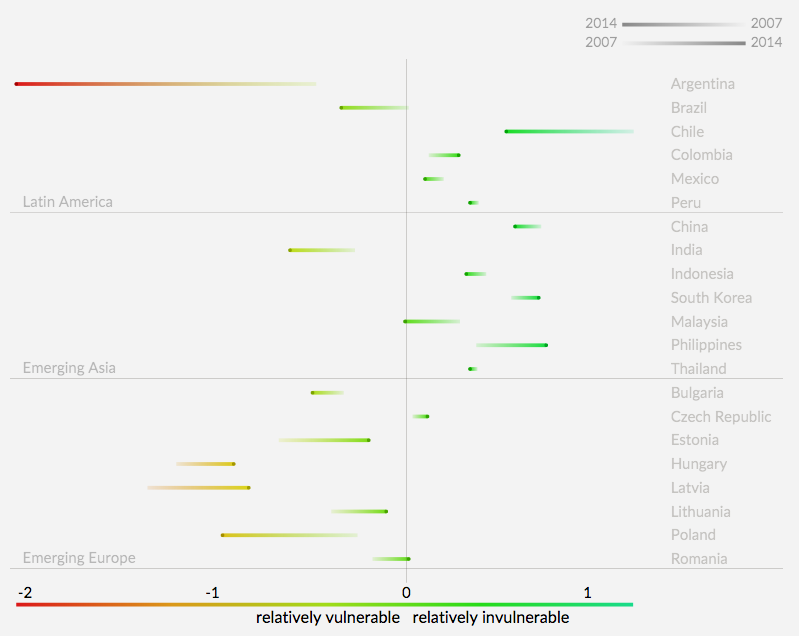

In the figure below, we’ve constructed a relative resilience chart. For the 21 economies that Rojas-Suarez studied, the chart shows their resilience to shocks now compared to 2007, and compared to each other.

An Indicator of Resilience to External Shocks, 2014 versus 2007

Your browser does not support SVG graphics, or JavaScript is disabled.

Click here to download an image.

A country’s individual performance goes from light (2007) to dark (2014) and all 21 countries lie along a color gradient: the red end of the spectrum indicates greater relative vulnerability, flowing through to light blue (relative resilience). Argentina is the worst performer, but all Latin American economies save Colombia are less resilient now than in 2007. India’s position is weakest of Emerging Asia economies by this measure, while nearly all the Emerging Europe economies shown have improved but remain vulnerable.

How We Made It

The resilience test is based on a CGD Working Paper produced by Rojas-Suarez and Carlos Montoro. Building on that, Rojas-Suarez looks at seven indicators that together give a measure of a country’s economic and financial resilience to external shocks. These indicators fall into two categories:

- A country’s ability to withstand the impact of an adverse external shock

- The authorities’ capacity to rapidly implement policies to counteract the effects of the shock on economic and financial stability

In category 1, Rojas-Suarez argues that a country’s ability to withstand an external shock depends upon its ability to raise external financing and, therefore, on its solvency and liquidity positions. She uses three indicators to measure these:

i. Current account balance as a ratio of GDP: this represents a country’s external financing needs.

ii. Ratio of total external debt to GDP: this is a solvency indicator.

iii. Ratio of short-term external debt to gross international reserves: this is a measure of liquidity. Both Malaysia and Argentina’s positions weakened markedly from 2007 to 2014 by this measure.

In category 2, Rojas-Suarez asserts that a country’s ability to react to an adverse external shock largely depends on its authorities’ capacity to implement countercyclical fiscal and monetary policy (this is especially true of developing countries with less developed capital markets). The four variables here relate to fiscal and monetary position:

i. Ratio of general government fiscal balance to GDP: smaller deficits, or surpluses, give greater scope for fiscal measures. Of the emerging economies studied, only Hungary and Romania have stronger fiscal positions in 2014 than in 2007.

ii. Ratio of government debt to GDP: most governments in the sample increased their debt ratios between 2007 and 2014, indicating greater vulnerability.

iii.Squared deviation of inflation from announced target: this suggests how constrained a government is in responding with monetary policy tools. It is squared to show that deviations from inflation targets — both positive and negative — are equally pernicious. Brazil and Indonesia show heightened vulnerability over the period.

iv. A measure of financial fragilities: this measures the presence of credit booms or busts, both of which limit a government’s monetary policy options. This indicator shows Emerging Europe economies going from boom to bust over the period.

Overall, the resilience test, which Rojas-Suarez admits is limited in scope, serves to emphasize that the lessons from the global financial crisis should not be forgotten. In particular, initial conditions at the onset of a severe adverse external shock matter a lot for future resilience. Investors’ enthusiasm for previous high-achievers such as the BRICS nations could be tempered by this analysis. Meanwhile policymakers could unpack the resilience test to understand where they should focus their efforts now, so they are better prepared should things get suddenly much worse.

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

{kind=link}