At the UN General Assembly last fall, President Biden pledged to increase US support for international climate efforts to $11 billion annually, representing a quadrupling of funding from current levels. Beyond the political challenges of delivering on this commitment, there are important questions about the form the money will take. Most likely, the administration will seek to rely on existing programs, whether grant-based aid through USAID or loans to private firms through the US International Development Finance Corporation. These efforts can be effective, but they may prove challenging in scaling up quickly. In order to meet its annual pledge, the administration will have to consider new instruments and approaches.

We see an opportunity to deploy a new sovereign bond guarantee program (the “Green SBG”), working with partner governments in the developing world to target their public finance toward climate change mitigation. US-backed guarantees can be highly cost-effective, they can be deployed quickly, and they put developing countries in the driver’s seat when it comes to programming their own public budgets.

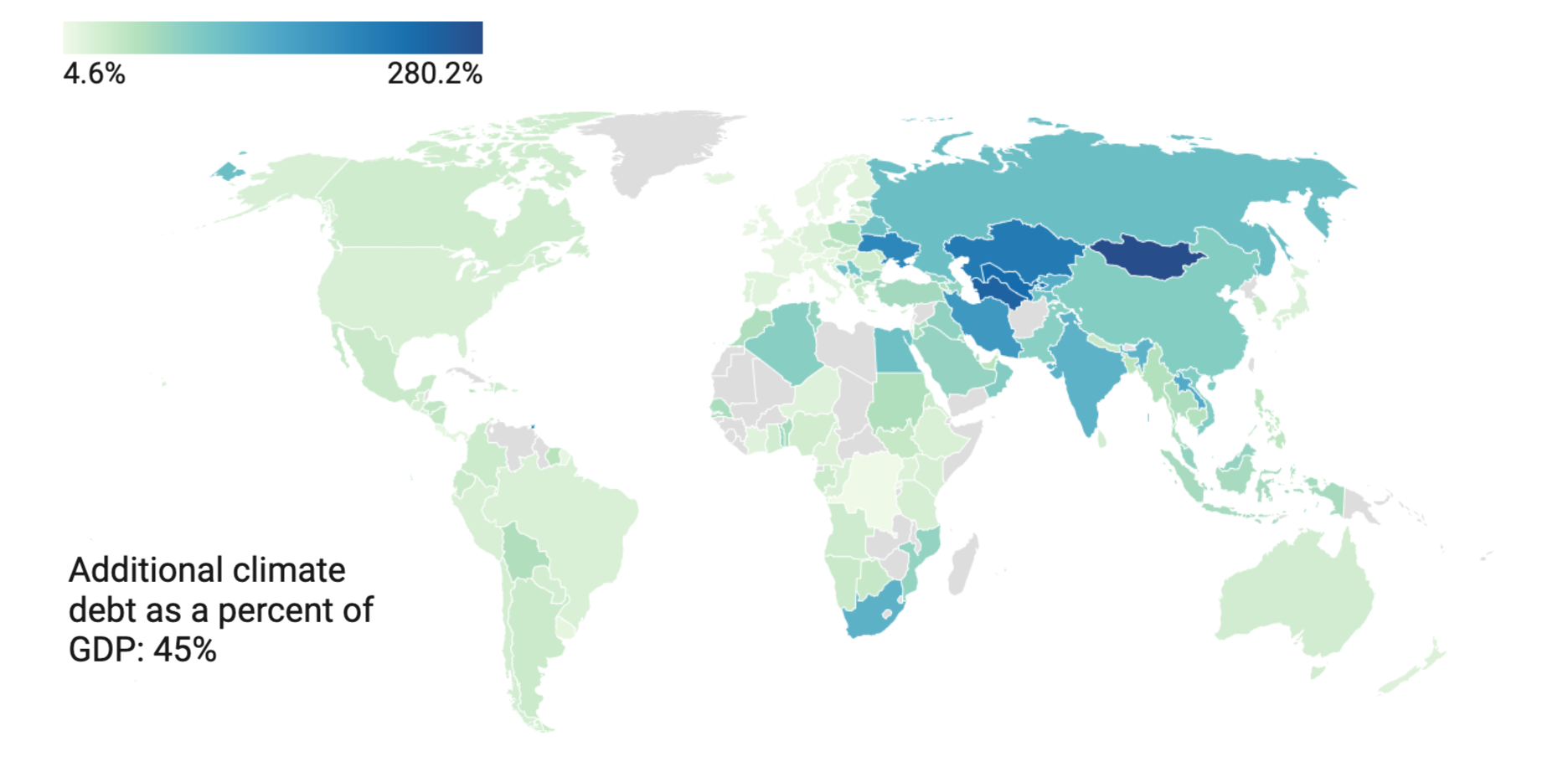

In a new CGD policy paper, we propose a new Green SBG program to help deliver the US climate finance commitment. Using climate change mitigation as a leading example, we demonstrate that a US outlay of $1.9 billion could mobilize $20 billion in climate finance for the 28 highest-emission emerging market countries. The reduction in borrowing costs associated with the US-provided bond guarantee represents budgetary savings of $4.4 billion for these countries—possibly more if a new tranche of SBGs prompts large index funds to include guaranteed bonds or incentivizes borrower-governments to seek third-party green bond certification. And for US taxpayers, the cost effectiveness of the program could improve dramatically over time as the subsidy outlays are recycled.

Looking ahead, a more challenging interest rate environment and tightening financial conditions will force emerging market governments to make difficult decisions about their budget priorities. In this environment, a Green SBG could be effective in easing financing terms and ensuring that climate investments continue to be prioritized.

Over the past thirty years, the United States has issued 13 sovereign bond guarantees, for countries that were foreign policy priorities at the time like Israel, Jordan, and Tunisia. In total, these guarantees helped borrower governments raise $26 billion in bond issuances. We estimate the guarantees saved these governments $2 billion in debt service payments by effectively conferring the US government’s cost of borrowing.

Importantly, these historical cases show that a guarantee is not appropriate in every circumstance or for every country. Where the risk of default is high, the subsidy cost of providing a guarantee will exceed the benefit in reduced borrowing costs. Alternatively, countries that already enjoy solid credit ratings will likely derive little benefit from a US-provided guarantee in the form of reduced borrowing costs and therefore will likely show little interest in it. Nonetheless, we estimate there are at least 65 countries where the benefit of reduced borrowing costs will exceed the subsidy cost associated with the guarantee.

Finally, our paper highlights the versatility of SBGs for financing a variety of global public goods. From climate change mitigation and adaptation to global vaccine deployment, SBGs offer the United States a cost-effective method for mobilizing low-cost capital for some of the world’s most pressing problems, and an approach to partnering with developing countries that moves beyond the donor-recipient relationship.