Recommended

As travelers cancel flights, businesses ask workers to stay home, and stocks fall, a global health crisis becomes a global economic crisis. In any health crisis, our first concern is (and should be) with the health of those affected. More than 4,000 people have died worldwide and more than 113,000 cases have been confirmed in over 110 countries. But unfortunately, the economic impacts also have dramatic effects on the wellbeing of families and communities. For vulnerable families, lost income due to an outbreak can translate to spikes in poverty, missed meals for children, and reduced access to healthcare far beyond COVID-19. While the spread in the United States and Europe absorbs much of the media coverage, confirmed cases from Bangladesh to Brazil, from Cameroon to Costa Rica, and in many other low- and middle-income countries mean that many of the economic impacts may affect the world’s most vulnerable populations.

Assessing the economic impact of COVID-19

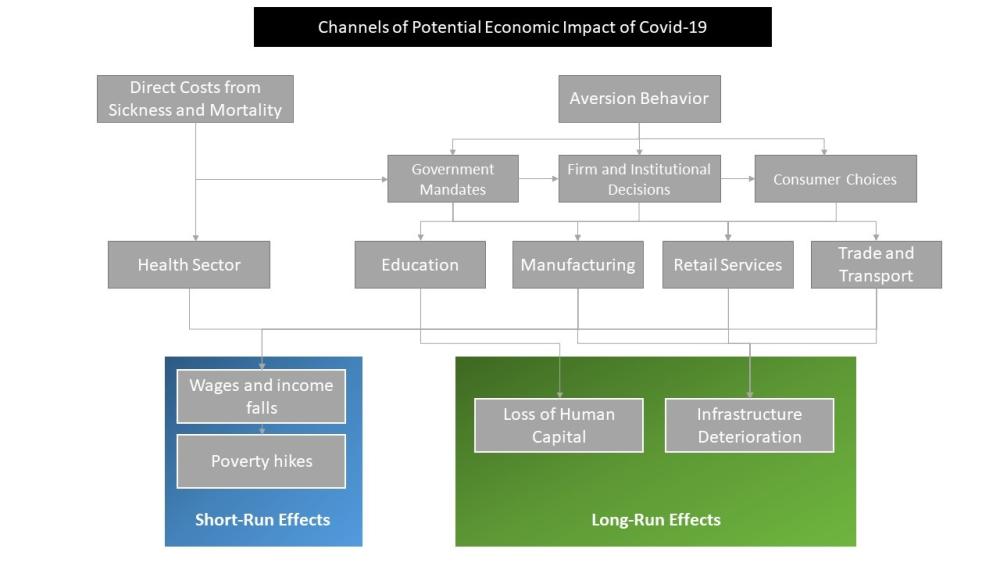

What are the channels of economic impact we can expect from COVID-19? (See the figure below for a summary.)

Beyond the human tragedy, there is a direct economic impact from lives lost in an outbreak. Families and loved ones lose that income and their in-kind contributions to household income such as childcare. Of note, the distribution of COVID-19 fatalities skews old, which means many of those most likely to die are no longer working and are less likely to be the primary provider for their families. (Keep in mind, though, that in many low- and middle-income countries, individuals work until a later age.) Though less likely to pass away from COVID-19, many working age adults still fall ill and their families will feel the financial burden as they miss work for days or weeks.

Figure 1. Broad Channels of Short-term Economic Impact of the Pandemic

Source: Authors’ construction, adapted from World Bank 2014.

Most of the economic impact of the virus will be—as we are already seeing—from “aversion behavior,” the actions people take to avoid catching the virus (which can, it should be noted, be a logical and proportional response). As depicted in the figure above, this aversion behavior comes from three sources:

- Governments impose bans on certain types of activities, as when the government of China orders factories to shut down or Italy closes most shops throughout the country.

- Firms and institutions (including private schools and private companies) take proactive measures to avoid infection. Business closures—whether through government bans or business decisions—result in lost wages for workers in many cases, especially in the informal economy where there is no paid leave.

- Individuals reduce trips to the market, travel, going out, and other social activities.

These actions affect all sectors of the economy—the health sector, manufacturing, retail and other services, trade and transportation, education, and others. These in turn translate into reduced income both through the supply side (reduced production drives up prices for consumers) and the demand side (reduced demand from consumers hurts business owners and their employees).

These short-term economic impacts can translate into reductions in long-term growth. As the health sector soaks up more resources and as people reduce social activities, countries invest less in physical infrastructure. As schools close, students lose opportunities to learn (hopefully briefly) but more vulnerable students may not return to the education system, translating to lower long-term earning trajectories for them and their families, and reduced overall human capital for their economies.

For example, unplanned pregnancies rose sharply in Sierra Leone during the Ebola epidemic, likely in part a result of school closures. Adolescent mothers are less likely to return to school, and their children will likely have fewer health and educational investments. Further, health workers are on the front lines of epidemics and losing some of them to the disease—especially in countries where they’re already in short supply—can lead to worsening health conditions in the long-term, such as maternal and infant mortality. These all have poverty implications well beyond their humanitarian implications.

Beyond China and Iran, most documented cases of COVID-19 to date have been in high-income countries. Latin America and Africa have had particularly few cases, with a few dozen documented in Brazil and fewer in other countries in the regions. It is difficult to know how much of that is due to health systems in some Latin American and African countries not being set up to diagnose cases effectively and how much is due to the virus not yet spreading widely. It is certainly possible that—in the absence of aggressive action—the spread in poorer nations may come later, even as the epidemic gets under control in higher-income countries. As a result, the health consequences and the economic impacts from aversion behavior may reverberate in poor countries longer after the epidemic subsides in rich countries.

What we know so far—and what to expect

Economic estimates of the likely global impact vary dramatically, with Orlik and others at Bloomberg hypothesizing $2.7 trillion in lost output, the Asian Development Bank releasing scenarios from $77 billion to $347 billion, and an OECD report talking about a halving of global economic growth.

Here’s a roundup of analysis of the actual and potential economic impacts of the crisis so far in low- and middle-income countries:

- Baker-McKenzie reviews the likely impact across sectors in African countries, mostly focusing on the impact that stems from slowdown in the Chinese economy, with reduced Chinese demand for raw materials, likely reduced investments in energy, mining, and other sectors, and a fall in travel and tourism. (March 10)

- An Asian Development Bank brief proposes four scenarios—best-case, moderate impact, worse case, and worst case—for 22 Asian countries, projecting the largest impacts in the Maldives, Cambodia, and Thailand. (March)

- DW documents how shutdowns in Chinese factories affect consumers in Africa. “About a fourth of Ugandan imports come from China. Supply chains have been interrupted for weeks because many Chinese factories shut down production. Small traders selling textiles, electronics or household goods are in trouble… In Niger, stocks of certain goods, including groceries, from China have already been significantly decimated, leading to higher prices.” In Zimbabwe and Angola, exports to China have crashed. (March 3)

- Jeremy Stevens of Standard Bank in Beijing points to an array of likely disruptions but highlights that once the epidemic is under control, “much of the rationale for China’s endeavors in Africa (or Belt and Road, for that matter) are to leverage China’s competitive advantage in infrastructure, offshore some overcapacity sectors, and heavier industry, and tap into fast-growing consumer markets. All of this remains.” (February 28)

- Strategy& estimates “a potential loss of at least R200 million in Chinese tourist spending” in South Africa. (February 20)

- Dai, Hu, and Zhang report from the Enterprise Survey for Innovation and Entrepreneurship in China that “20 percent of surveyed firms will be unable to last beyond a month on a cash flow basis, and 64 percent beyond three months, presenting a dire picture for [small and medium-sized enterprise] bankruptcies under an extended epidemic scenario.” (February 28)

As you can see, most of the data and observed impacts in the developing world so far stem from production and export stoppages from China, and pre-date the worsening economic conditions in Europe and the United States. But as the economies of other countries slow down with the spread of the disease, we’ll see these impacts show up more clearly in economic data and likely grow over time.

What should we do to minimize COVID-19’s economic impact? Recommendations from the IMF

What actions can policymakers and donors take to lessen the economic impacts of the COVID-19 pandemic for low- and middle-income countries? Here are three actions beyond the stimulus and liquidity recommendations from the International Monetary Fund:

- Contain the pandemic. As our colleague Jeremy Konyndyk puts it, “To assuage market reactions to the outbreak, you have to present a viable plan to defeat *the outbreak*.” As long as the outbreak is actively spreading, many aversion behaviors may well be rational and wise. Containing the disease is the first step to mitigating not only the health impacts but also the economic impacts.

- Strengthen the safety net. The most vulnerable households are those most likely to be affected economically. Low-wage workers are often those most likely to lose their jobs if they miss work due to an extended illness. They are often the least able to work remotely to avoid contracting the virus. And they are the least likely to have savings to survive an economic downturn. Making sure there is an economic safety net—cash transfers, sick leave, subsidized health coverage—in place helps the most vulnerable survive and provides support to enterprises that serve those populations.

- Measure the impact. Systematic data on which populations are experiencing the greatest hardships and which industries are failing is essential to providing assistance. During the Ebola epidemic of 2014-2015, researchers used phone surveys in Sierra Leone and Liberia—building on the sample frames from existing surveys—to gather just-in-time information on the impacts of both ill health and aversion behavior on households and enterprises across the countries. Even as we monitor the health situation across and within countries, monitoring the economic situation and providing support to households in need can mitigate the most urgent needs.

David Evans and Mead Over worked with a team to estimate the potential economic impact of the 2014 Ebola epidemic. Amina Mendez Acosta provided research assistance for this post.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.