Recommended

Last week, the IMF revised the post-COVID growth forecasts it had made originally in the April World Economic Outlook (WEO). Taking account of the evolution of the pandemic and its impact so far, it revised growth down by another 2 percentage points for both advanced economies and developing countries (EMDEs).

The IMF’s Managing Director and Chief Economist struck an appropriately somber tone, highlighting the hardship and bleak outlook for the EMDEs. That was also true in April. But as we noted in a recent paper, that bleak message sat uncomfortably with the April growth forecasts numbers which projected a significantly more optimistic outlook for EMDEs compared with advanced economies. We argued then that the relative optimism could not be explained by the underlying vulnerabilities of EMDEs or their social distancing, lockdown, and fiscal responses compared to advanced economies.

It turns out that the latest June forecast maintains this relative optimism for EMDEs because the recent downgrade is uniform, as the bottom row in the table shows. In fairness, the IMF did downgrade its 2021 forecast for EMDE’s by 0.7 percentage points, while upgrading its 2021 outlook for advanced economies by 0.3 points; but why only growth for 2021 and not also 2020 should be differentially affected remains unclear.

IMF forecasts of growth in 2020, April versus June 2020

| Growth 2020 (%) | ||

|---|---|---|

| April forecast | June forecast | |

| Advanced economies | -6.1 | -8.0 |

| Emerging markets and developing economies (EMDEs) | -1.0 | -3.0 |

| Difference (advanced economies minus EMDEs) | -5.1 | -5.0 |

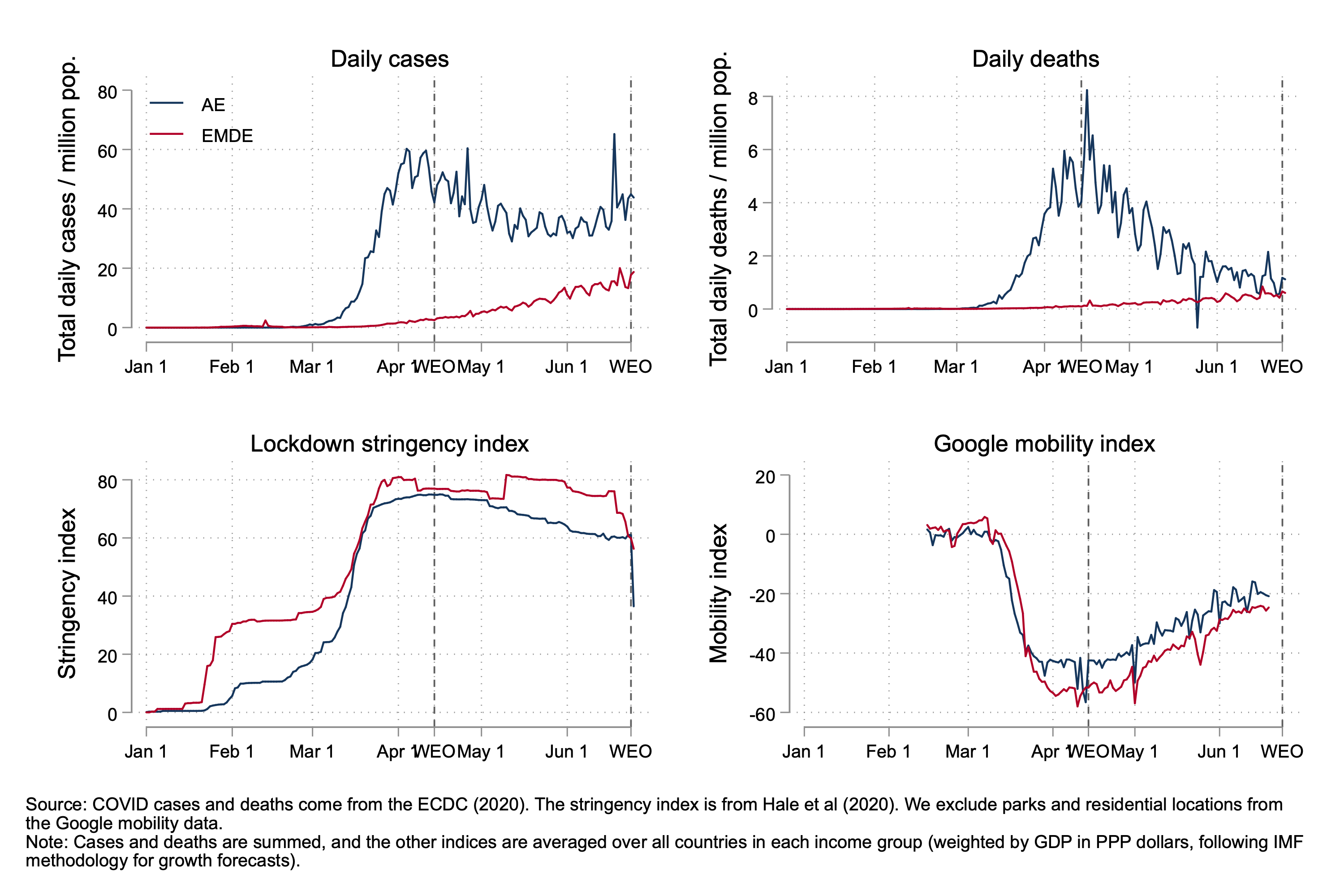

The continuing discrepancy between the somber narrative and relatively optimistic numbers in the June forecast for 2020 is puzzling because, since the April forecast, the key factors that might drive post-COVID growth—severity of the pandemic, social distancing, and lockdown policies—have moved more unfavorably for EMDEs than for advanced economies. The figure below captures the evolution in these key indicators over time. (We cannot re-do our earlier analysis with the new data because detailed growth revisions are only publicly available for a small set of countries.)

Figure. The evolution of the COVID crisis in advanced economies (AEs) and emerging markets and developing economies (EMDEs)

Since April (when the first forecast was made), the number of cases and deaths per million population have increased substantially for EMDEs while declining for advanced economies. The really alarming and striking recent development is that EMDEs are exiting from the first phase of the lockdown, but with the pandemic significantly still out of control. In contrast, advanced economies, with notable exceptions of course, are exiting with the pandemic more in control. In addition, the figure shows that the lockdown stringency index remains more severe in EMDEs than advanced economies. And economic mobility indicators are catching up slower in EMDEs. Even the fiscal responses continue to be more supportive in advanced economies than EMDEs.

Each of these post-April developments should make the growth outlook worse for EMDEs than for advanced economies, perhaps even substantially. In contrast, the IMF forecasts reflect an unchanged relative outlook between the two groups of countries.

Down the road, it will be interesting to see whether the reality validates the IMF’s somber message or its numbers for EMDEs which continue to be more optimistic for developing countries even as the COVID case and death counts surge in the South. It cannot validate both.

The code and data used in this blog post can be downloaded here.

Thanks to Julian Duggan for excellent research assistance.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.