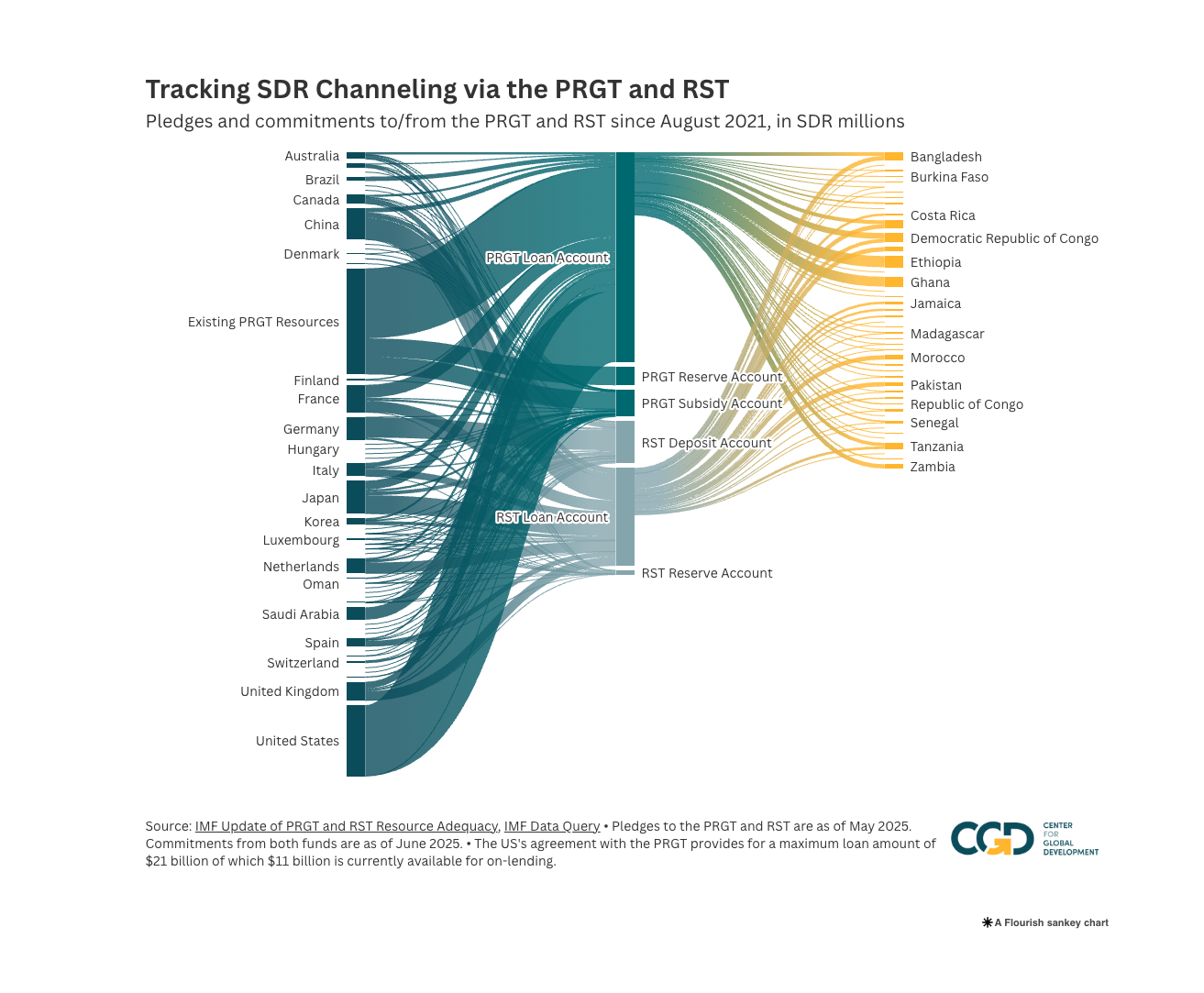

With the recent allocation of special drawing rights (SDRs)—a reserve asset issued by the IMF—to help countries weather the economic effects of the pandemic, the international discussion has shifted to ways to rechannel a portion of the SDRs that were allocated to high-income economies. The focus has been on the IMF itself as the channel for getting these resources from advanced countries to vulnerable low- and middle-income countries. Two options are on the table: enlarging the Poverty Reduction and Growth Trust (PRGT), which supports low-income countries, and establishing a new Global Resilience Trust (GRT) that would support middle-income countries as they recover from the pandemic and seek to transition to a more resilient, sustainable, and equitable future.

But IMF-based operations are limited in scale and scope. The PRGT and GRT are likely to re-channel only a small share of the SDR allocation and meet only a small fraction of countries’ long-term needs. In addition, even the IMF’s strongest advocates would admit that it lacks the expertise needed to address all the policy challenges of a green economic transition.

Rechanneling SDRs to the multilateral development banks (MDBs) will extend the reach and power of the recent allocation. New MDB lending operations supported by SDRs could be an important foundation for multilateral collaboration supporting climate change adaptation and a green recovery from COVID-19. The MDBs have the institutional and technical knowledge needed to assist low- and middle-income countries (LMICs) in making needed investments. And together with the IMF they can provide a coherent international framework that brings together national policies and financing needs to catalyze the private sector financing that is expected to cover the bulk of transition costs.

Rechanneling SDRs through the MDBs has a clear technical advantage over other potential rechanneling targets. Most MDBs are prescribed holders of SDRs, which means they can use them as part of their financial operations. That makes rechanneling easier: other funds or institutions could not receive SDRs for financial operations so contributing countries would have to covert SDRs to hard currency. And to become a prescribed holder, other funds would need to garner an 85 percent approval by the IMF’s Executive Board—a steep challenge in today’s fractured political climate.

The scale of SDR recycling to LMICs through MDBs could be expanded using two possible approaches: on-lending schemes or capital injections (see here for more details):

-

Lending SDRs to the World Bank or other MDBs would increase their available loan funds for economic transition. These onlending schemes could copy the modalities of the PRGT to preserve the reserve asset characteristic of the SDR—an imperative stressed by the G20.

-

More boldly, SDRs could be used to provide capital injections to MDBs and in turn this increased capital could be used to leverage private finance, providing 4-5 times as much lending potential to LMICs.

The key technical challenge in lending SDRs for MDBs to on-lend would be to maintain the SDR’s reserve asset characteristics.

-

The liquidity of SDR claims could in principle be maintained using an encashment regime, modelled on that of the PRGT, but would need to be tailored to the financial structure of each MDB in a way that SDR lenders would find satisfactory. The IMF would have to be involved in the design.

-

Credit risks to lenders would be mitigated by the MDB’s lending policies. MDBs and SDR lenders would need to examine whether credit risks would be adequately mitigated, particularly if the MDBs sought to lend SDRs at maturities longer than the 10-year-maximum in the PRGT. Establishing a reserve account (like that in the PRGT) that could repay creditors in the event of delayed repayments by borrowers could also be part of the risk mitigation strategy. It would also be important for the MDB’s preferred creditor status to extend to SDR on-lending.

-

SDR lenders would be paid the SDR interest rate. If the MDB wanted to reduce rates on all or some of its SDR financed lending it would need to establish a subsidy account, funded with hard currency resources.

Capital contributions would be more valuable, but the technical challenges for MDBs, potential contributors, and the IMF are also greater. SDRs could in principle be donated as a capital contribution but in practice the donated SDRs would lose their reserve asset status from the perspective of the donor. Instead SDRs could be lent or pledged. However, there is a tension between the purpose of the loans or pledges—namely to provide a capital buffer that would allow the organization to take on some addition credit risks in leveraging greater lending—and the need to preserve reserve asset status which would require the near-absence of credit risk for the lent or pledged SDRs.

Channeling SDRs outside the IMF in any from would break new ground. Finding modalities that meet the requirements of the MDBs and SDR contributors will require close joint consideration of the constraints and possible tradeoffs. It may not be feasible to meet all the constraints of contributors, MDBs, and the IMF at once, so it will be important for contributors to determine whether they would be prepared to accept some liquidity or credit risks and thus some loss of reserve asset status on their SDR contributions. Alternatively, the option remains for countries to make use of the additional reserve buffer provided by the SDR allocation to provide contributions in the form of non-SDR assets and thereby avoid the complications that arise when using SDRs.

We see four concurrent first steps to finding ways to rechannel SDRs to MDBs, using both avenues described above:

-

MDBs, working with potential SDR contributors and the IMF would develop modalities to begin on-lending SDRs soon. At the same time, work would continue towards the bolder longer-term goal of using SDRs as capital contributions.

-

MDBs would need to see whether and what form their accounting and legal structures would allow SDR loans or pledges to be considered capital and whether this would this meet the requirements of rating agencies. There are likely to be significant differences in this area across MDBs.

-

Creditor countries would need to assess the flexibility in their own rules and regulations to allow SDRs to be used as capital contributions and gauge the extent to which they might use other reserve funds instead of SDRs to reinforce lending power of MDBs.

-

The IMF would need to confirm that exchanges of loans or pledges for equity stakes are covered by the existing approvals of prescribed operations.

The decision to rechannel SDRs to MDBs is ultimately a political one. The enormous global financial firepower of SDRs is lying dormant on countries’ balance sheets now. Global leaders need to decide if and how to put SDRs to use. MDBs are a relatively safe way of leveraging these resources to support LMICs and other vulnerable countries in recovering from the pandemic and beginning the transition to a green and sustainable future. While the technical hurdles presented above may seem daunting, they can be overcome if the global political mandate is clear.