Recommended

Blog Post

A Series on Education Finance Post-COVID

Blog Post

What Happens to Teacher Labor Markets Following Shocks?

This post is part of CGD’s education finance series, where we examine how the pandemic and subsequent economic crisis may impact resources to fund education. In our fourth post, we look at the potential consequences of the economic crisis on household finances, what that means for the education sector, and the ways it will disrupt children’s education in the coming years.

In the face of already stretched household budgets, evidence shows that shocks like the Global Financial Crisis or past epidemics increase the financial burdens families face in sending children to school, particularly in places where households must make up for cuts to government spending. The economic consequences of COVID-19 are likely to squeeze household budgets even further and reduce families’ capacity to fund their children’s education, or, in some instances, force them to make other difficult sacrifices (including cutting back on food or other necessities) to afford education.

It is too early to tell how this crisis will impact education spending at the household level, but past experiences and the expected magnitude of the current economic shock should make us cautious. Families are a major contributor to education spending and there is a substantial risk that this source of funding will be hit hard by the pandemic. While discussions of education finance often focus on government spending and donor money, fluctuations in household spending can have more immediate consequences and could have long-term consequences, including millions of children dropping out of school.

Before the crisis, households were an important source of education finance in many developing countries, including in places with fee-free policies

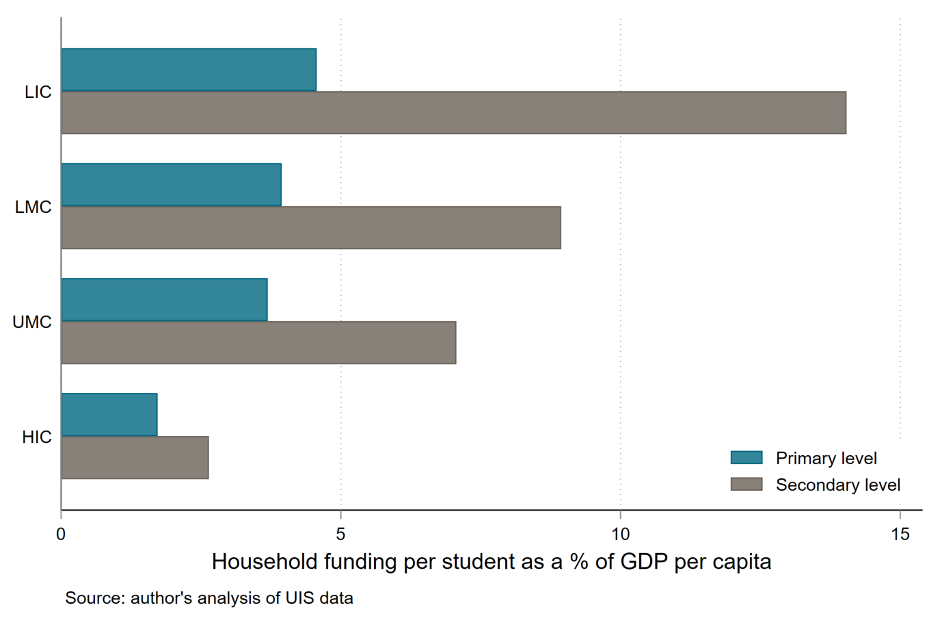

In some countries, families pay school fees to send children to school particularly at the secondary level, and even when schooling is technically free, complementary costs like parent-teacher association fees, supplies, transportation, and uniforms can make education expensive. Figure 1 shows that, in low-income countries, the cost per student of secondary education for families is close to 15 percent of the average income per capita and can be as high as 25–30 percent in some of the poorest countries in Africa. This is a considerable expense for many parents and can make the schooling of multiple children at the same time challenging to afford.

Figure 1. Cost of education to families as share of GDP per capita by income group

LIC: low-income countries, LMC: lower-middle-income countries, UMC: upper-middle-income countries, HIC: high-income countries.

In some contexts, household spending accounts for a large share of total education spending. In Nepal and Uganda, for instance, household contributions make up more than half of total national education spending. Across other developing countries, they typically account for 25–35 percent of total education expenditure. This means that shocks to household budgets could lead to substantial funding gaps, particularly in the poorest countries.

For the poorest families, the supplementary costs of schooling can already be prohibitive in non-crisis times

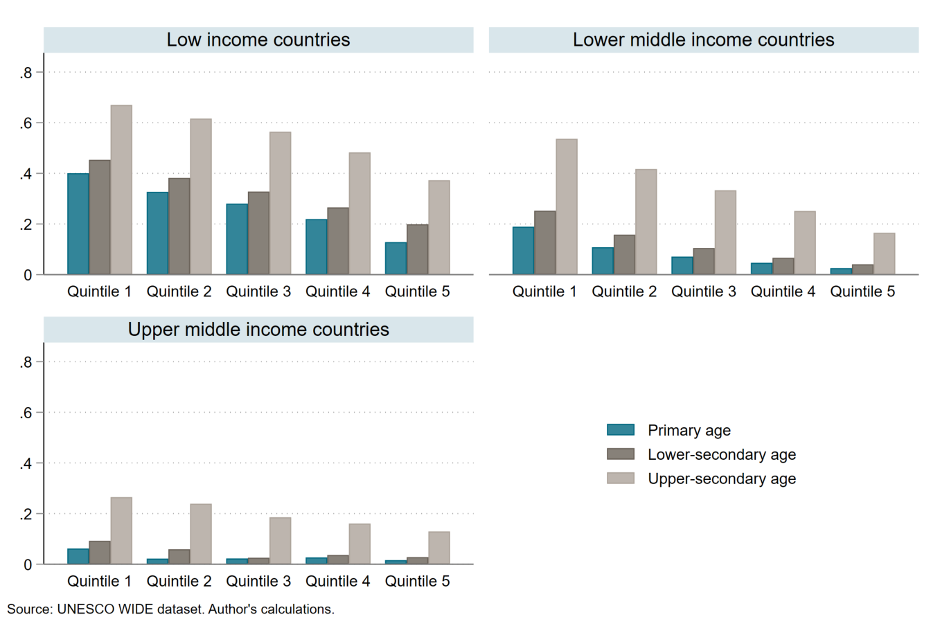

For example, evidence from Rwanda—a country which offers universal free education through secondary school—finds that 70 percent of the students who failed to transition from primary to secondary school cited the supplementary costs of schooling as the top reason. Children who are not able to pay supplementary fees are often sent home, disproportionately disadvantaging the poorest students and exacerbating socioeconomic gaps in access to secondary education. Figure 2 shows that in all regions of the world and across every level of education, there is a clear relationship between household wealth and the likelihood of children going to school. In low-income countries, primary-school-aged children from the poorest quintile are over three times more likely to be out of school than children from the wealthiest quintile.

Figure 2. Percentage of out-of-school children by income group, levels of education, and wealth quintiles

The pandemic’s economic shocks will squeeze household budgets, but the distributional effects—and effects on education—are not yet clear

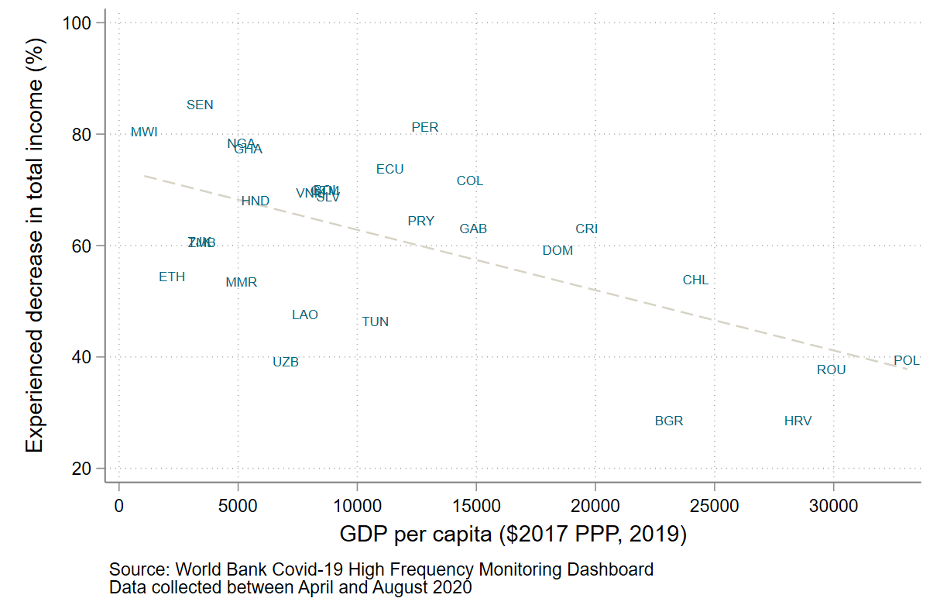

Now, as we enter the most severe global recession since the second world war, household budgets are already being squeezed. The IMF and the World Bank predict developing country GDP will fall by 3.3 percent this year. Early evidence illustrates the scope of this economic crisis: according to phone surveys from 28 countries in 2020, more than 60 percent of households have experienced a decrease in their family income. Poorer countries seem to have been hit harder, with more than 80 percent of households in Senegal or Malawi reporting loss of income (see figure 3).

Figure 3. Percentage of households reporting a loss in income in 2020 and GDP per capita

There is not yet clear evidence of the distributional impacts of the crisis within countries: for instance, data from phone surveys do not show whether rural areas are more affected by the crisis. Workers in the informal sector may be more likely to lose income, and those in the industries most directly affected by the pandemic like tourism, retail, or hospitality—all sectors which typically employ many low-wage workers—may be disproportionately impacted.

Which households are most at risk also varies within and across countries and regions. For example, in the UK, people in the lowest wealth quintile have experienced the worst labour shocks. In Latin America, Nora Lustig and co-authors predict that, in some countries, households in the middle of the income distribution will be the most affected by the crisis because they are not covered by social assistance. Similarly, results from a microsimulation model in South Africa show a decline in inequalities between the poorest and the middle-class because the poorest people are already covered by social assistance, thus easing the impact of the shock for them. In low-income countries where most people are not covered by social assistance, it is likely that economic impacts will be dire for the poorest households.

But we do know that the simultaneous tightening of household and government budgets caused by macroeconomic and health shocks can increase the financial burden on families of sending children to school

As household budgets tighten, evidence from past crises suggests that shocks are likely to increase the financial burdens families face in sending children to school, particularly if governments reduce public education spending. Graham Slater argues that public crisis recovery often falls to schools and education systems. If government resources and support don’t follow, the burdens of a macro-level financial shock can land with parents.

How this crisis will impact education spending for households remains to be seen and will likely vary within and between countries

Evidence from past crises suggests that household responses are likely to vary based on whether the shock has an income or substitution effect— that is, whether it creates a surplus or shortage of time or money—at the household level as well as on household perceptions of the role of education in overcoming the shock. For example, in higher income countries, we might expect to see an increase in graduate school applications during recessions in which labour markets are more constricted. Francisco Ferreira and Norbert Schady find that in richer countries, shocks have counter-cyclical impacts on education spending (i.e., households spend more on education during recessions). In some countries, middle- and upper-class households may increase expenditure on education during the current crisis as the need for private tutoring, distance learning materials, and other complementary costs rise. However in poorer countries, economic shocks are likely to result in less household spending, which can negatively impact education and health outcomes, especially for the poorest.

And we may see some pre-existing inequalities deepen as a consequence, which may disproportionately impact girls

In some cases, girls’ are disproportionately affected by household income shocks, with the risks increasing as they get older. However, differential impacts between boys and girls are not consistent across studies, suggesting that baseline differences in school participation and gender norms may be important contextual factors influencing whether girls are at greater risk following household shocks. Evidence from the East Asian financial crisis in 1997 finds that the recession deepened pre-existing gender and rural-urban disparities in education and found that poor households reduced spending on education more than wealthier households, but that the recession did not consistently lead to new disparities where they were not previously salient. For example, we were not likely to see gender gaps in education emerge if they were not there before, but we were likely to see pre-existing gender gaps deepen.

In an earlier CGD post, our colleagues Amina Acosta and Dave Evans find that health shocks coupled with household economic shocks can disproportionately impact girls, particularly if they need to become caregivers for sick family members. It can also put girls in the position of needing to earn income: following the Ebola crisis, adolescent girls often became the primary income earners in Liberia. In Sierra Leone, heighted economic needs led to greater risks of early marriage and transactional sex for adolescent girls.

A closer look at growth projections and education spending habits can tell us what we might expect in the coming years

In order to have a better sense of the magnitude of the effects on household education spending, we have modelled the income effects of the crisis on household budgets. We took the average of the IMF and World Bank growth forecasts for 2020 and 2021 released in October and adjusted by future population growth to predict changes in average incomes per capita in 2020 and 2021. Data on household education spending come from the World Bank Global Consumption database, which include data on level and shares of consumption by sector for 90 developing countries. We assume that after the crisis households will maintain their spending on education as a share of consumption. This means that all the changes in household expenditures on education will be due to changes in per capita income.

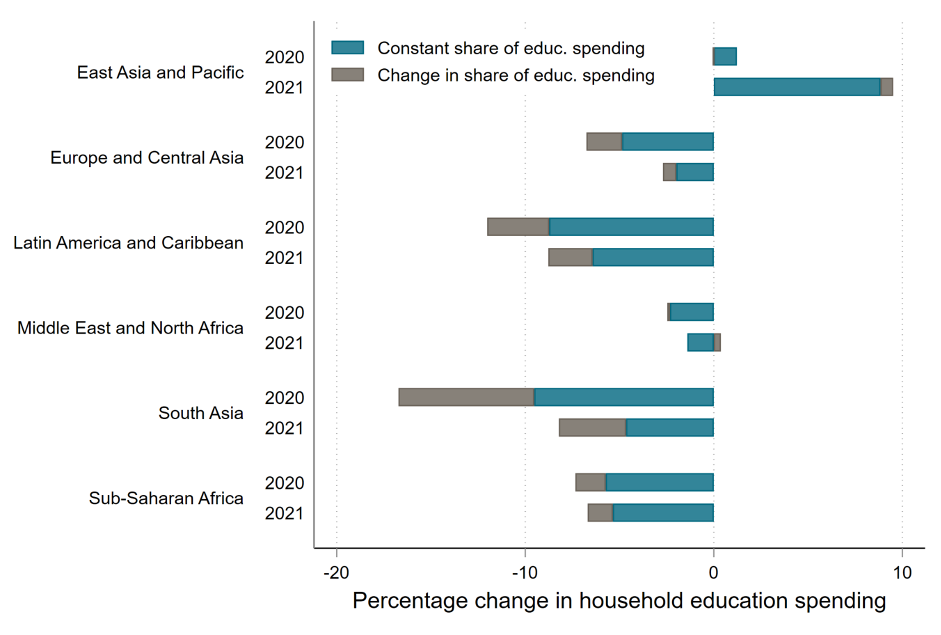

In developing countries, we find that household spending on education is expected to decrease by 1.8 percent in 2020 and increase by 4.3 percent in 2021 (as a percentage of 2019 levels). Despite the bounceback in 2021, household education spending will still be lower in 2021 than in 2019 in most regions, except East Asia and Pacific (see the teal bars in figure 4). In Latin America, South Asia, and sub-Saharan Africa, the drop in household education spending could be between 6 and 10 percent, assuming households manage to maintain their share of spending on education. Household spending growth will partly recover in 2021 in South Asia but in Latin America and sub-Saharan Africa it could remain at a similar level to 2019.

Figure 4. Forecasted changes in household education spending compared to 2019

As household incomes contract, the share of spending allocated to education is likely to fall

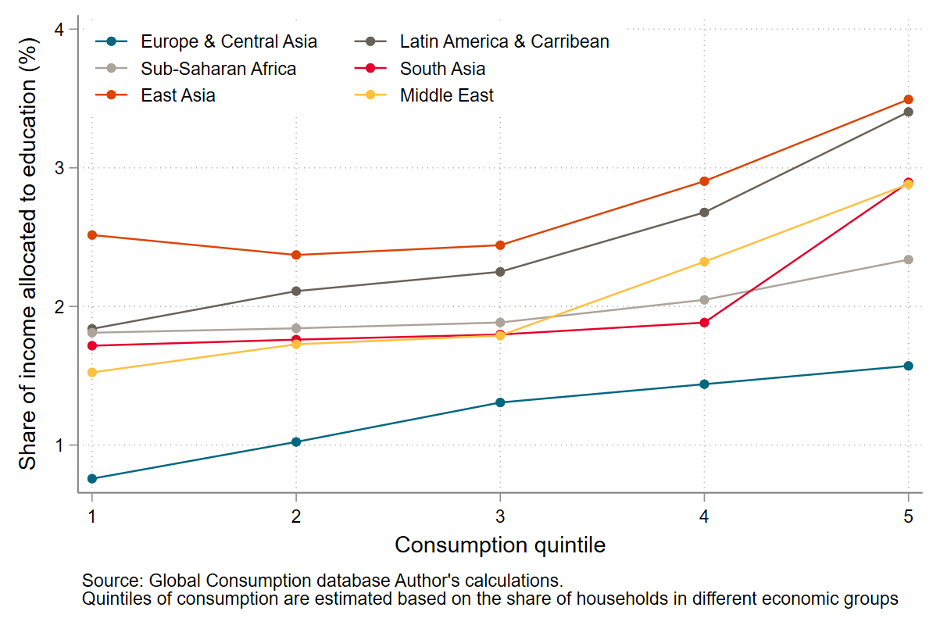

That scenario assumes households maintain the proportion of their spending on education, but it’s not clear that will be the case. In most countries, richer households tend to spend a larger proportion of their budgets in education, suggesting a positive income-elasticity of education spending (i.e., as income increases, spending increases). See Figure 5. Thus, as household incomes contract, the share of income allocated to education is likely to fall. To simulate this second scenario of household response to economic shocks, we estimated the income-elasticity of education spending based on the data from the Global Consumption database disaggregated by income groups for each country.

When we take these potential changes in the proportion of spending into account instead of simply holding it constant, we find household education spending at the global level could decrease by as much as 3.1 percent in 2020 (the grey bars in figure 4). That’s followed by an increase of 3.9 percent in 2021 (as a percentage of 2019 spending). Similar to the previous scenario, the relatively positive global trend in household education spending is driven by East Asia, notably China, which is the only region with positive forecasts. South Asia has the largest drop, 17 percent, in this scenario because spending on education there tends to be most elastic as income changes. Sub-Saharan Africa and Latin America have large forecasted declines of 7 and 12 percent respectively in 2020.

Figure 5. Share of income spent on education by consumption quintiles

The distributional effects of the economic crisis are still unclear, and the average decreases in education spending could be much larger for some groups if they are hit harder by the crisis. Our very simple model actually predicts a larger decrease in education spending for the richest quintiles, as their share of education spending tends to decrease more rapidly due to income elasticity.

A decline in household education budgets could have severe consequences for students and schools

Dropouts will likely rise

With less money to spend on education, households will have to make tough choices and more students are likely to drop out of school. Based on data on the relationship between dropout rate and income elasticity and what we knew at the time about the depth of the recession, in June the World Bank forecast that 6.8 million additional students, mostly aged 12 to 17, would drop out because of the COVID-19 economic crisis. But that forecast was based on the assumption that the recession in developing countries would be less severe, a 1 percent drop in GDP rather than the 3.3 percent drop now forecast. It’s likely that the number of dropouts will be even larger.

Countries in which household spending makes up a larger share of education finance may have more severe funding gaps

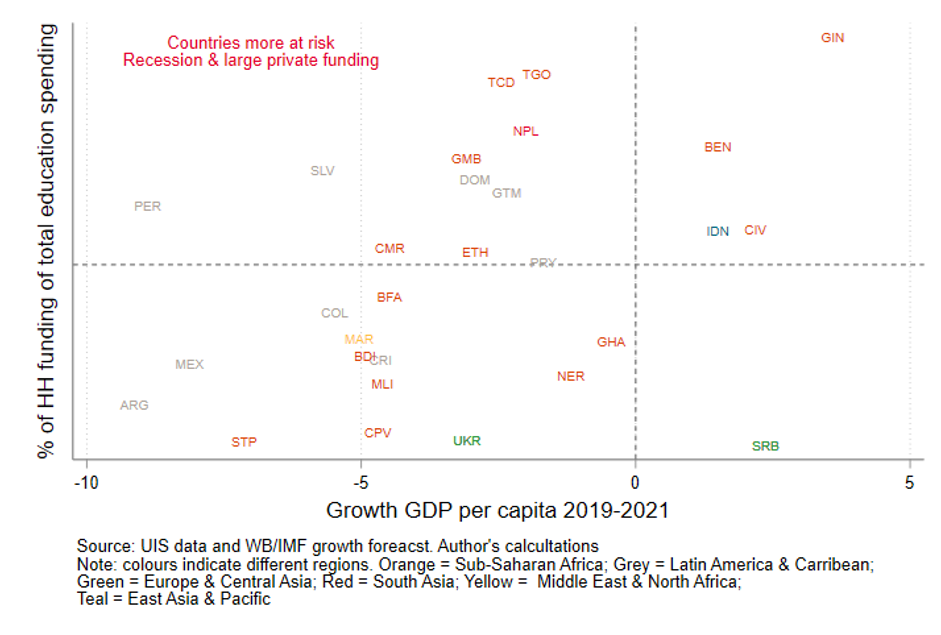

The second impact will be to stretch education budgets even more. In countries where households are a large contributor to total education spending, the decrease in household spending will compound expected drops in government spending. The countries most at risk are those where a larger economic shock is predicted and where households contribute a larger share of education spending. These countries that rely more heavily on household spending will experience additional challenges because households, unlike governments, will struggle to maintain their level of spending by borrowing.

Moreover, in these countries governments will need to account for the losses in household funding by mobilizing extra resources to ensure the functioning of their education sector. There is a risk that if countries ignore this source of funding in their budgetary forecasts, schools could be left with large funding gaps as a result of parents not being able to pay schooling fees or contribute to the supplement costs of education.

Figure 6. Forecast economic growth and share of household funding of total education spending

We are grateful to Justin Sandefur and Lee Crawfurd for helpful comments.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.