Click here to read in in Spanish.

At a dynamic event, CGD’s Latin America Initiative gathered experts to discuss the major economic constraints Latin America is facing in a less favorable international environment and what we can expect for the region’s economic growth and poverty reduction in the coming years. Speakers, including representatives from the World Bank, Inter-American Development Bank, Tulane University and CGD, began the event with a focus on macroeconomic issues and then shifted their attention to microeconomic issues (productivity) and poverty. The event served to define a clearer policy agenda for Latin American in the context of falling commodity prices, increased current account deficits, and negative productivity gaps.

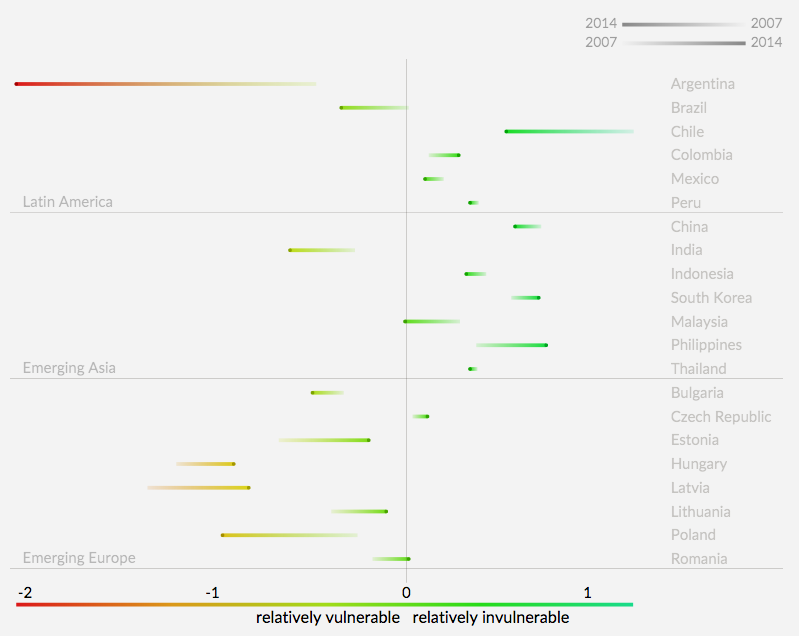

I kicked-off the event by expressing concern about Latin America’s economic and financial vulnerabilities. Specifically, I’m concerned that, relative to other emerging markets, Latin America’s economic resilience to adverse external shocks has significantly declined since the global financial crisis. I showed this point through my new Indicator of Macroeconomic Resilience to External Shocks, which I recently laid out in an essay and in my recent blog post with Rajesh Michandani. Below is a quick illustration of the Resilience Indicator. For a sample of 21 countries, the graph compares the value of the indicator in 2007 (the pre-global financial crisis year) with the respective values at the end of 2014. A country’s performance goes from light (2007) to dark (2014) and all 21 countries lie along a color gradient: the red end of the spectrum indicates greater relative vulnerability, flowing through to light blue for relative resilience.

Macroeconomic Resilience Indicator

Your browser does not support SVG graphics, or JavaScript is disabled.

Click here to download an image.

With the exception of Colombia, the indicator of relative macroeconomic resilience has deteriorated in all Latin America countries in the sample, albeit at very different degrees. This is mainly due to large current account deficits in the region caused by the drastic fall in commodity prices and deteriorated fiscal positions. Thus, some bad luck in unfavorable terms of trade, but also the squandering of opportunity to implement needed reforms in the good post-crisis years are the main reasons behind this outcome.

However, while experience has shown policy-makers that a high current account deficit, and therefore low domestic savings ratio, is inconsistent with sustained growth, standard theory doesn’t shed a clear light on why this is the case, particularly in middle income countries. In his presentation, Augusto de la Torre, chief economist for Latin America and the Caribbean at the World Bank, provided an alternative theoretical explanation on how increased savings leads to higher economic growth. Consequently, de la Torre said, a savings mobilization agenda should make sense for many Latin American countries. In his view, raising savings is doable in the region through a combination of fiscal, financial and safety net reforms. Moreover, at all times it is essential to have in place the right policy mix that addresses the long-term growth objective with the short-term macroeconomic goals. For example, in the current adverse international environment, “the best way to adjust would be tightening the fiscal and loosening the monetary… Tightening the fiscal [policy] will create a more robust saving environment that will help long term growth, and loosening the monetary [policy] will lower interest rates, and investment will pick-up,” he said.

Shifting the conversation to microeconomic issues, Santiago Levy, vice president for Sector and Knowledge at the Inter-American Development Bank, said that beyond short run macroeconomic issues and world commodity cycles, Latin America’s growth problem is mostly a productivity problem. “Productivity is a reflection of a country’s institutions, policies and programs” said Levy. “What makes the difference between Asia and Latin America is that [Asia’s] institutions have been more conducive to productivity and pragmatism, dealing with the redistribution issues in a better way, while Latin America hasn’t been able to do that.” To reignite growth in Latin America, Levy strongly suggested the formation of a productivity agenda that (i) channels resources to their most productive uses and (ii) increases the quantity and quality of human capital. While the first task would yield results in the short run, the second would be essential for long term productive transformation. Furthermore, such an agenda would avoid wasting resources (e.g., engineers becoming taxi drivers) and prevent the loss of resources (i.e., “brain drain”).

Finally, CGD non-resident fellow Nora Lustig suggested that declining inequality will be key for sustaining the reduction of poverty and the expansion of the middle class in the region, given growth in Latin American countries is expected to remain low. Lustig forecast that inequality will depend on three main determinants: labor earnings, government transfers, and private transfers (i.e., remittances). Among these determinants, she said, private transfers are likely to continue to be the main positive equalizing force for Latin America as the United States recovers from the financial crisis. Much of Lustig’s presentation echoed her work on the Commitment to Equity project, which analyzes the impact of a country’s fiscal policy package on poverty and inequality.

You can watch the entire event here. If you want to know more about what challenges Latin America is facing towards world trend dynamics, check out CGD’s Latin America Initiative.

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

{kind=link}