Recommended

Blog Post

Eroded Prospects for Tax Reforms in Sub-Saharan Africa

The rapid rise of dollar-backed stablecoins—cryptocurrencies pegged one to one to the US dollar—has emerged as one of the most transformative developments in blockchain technology. Now representing about 10 percent of the $4 trillion global crypto market, these tokens can be exchanged anonymously, much like cash.

In sub-Saharan Africa, stablecoins such as Tether (USDT) and USDC are gaining traction in economies plagued by currency volatility and limited access to US dollars. They already account for roughly 43 percent of the region’s total crypto transaction volume, with usage accelerating. In Nigeria, crypto transactions amounted to $59 billion between July 2023 and June 2024.

The rapid adoption of stablecoins could affect domestic resource mobilization in sub-Saharan Africa. For countries already struggling to raise sufficient revenues to finance development and the climate transition, unregulated crypto growth presents a new challenge. Without robust regulatory frameworks and strengthened tax administration, stablecoins could narrow the tax base and undermine fiscal and development goals.

Erosion of local currency demand and seigniorage

In countries with weak or unstable currencies, US dollar–backed stablecoins are increasingly preferred as both a store of value and a medium of exchange. This “digital dollarization” reduces the need to hold local currency for savings, cross-border trade (including remittances), or even domestic transactions—and can facilitate capital flight in economies with exchange controls.

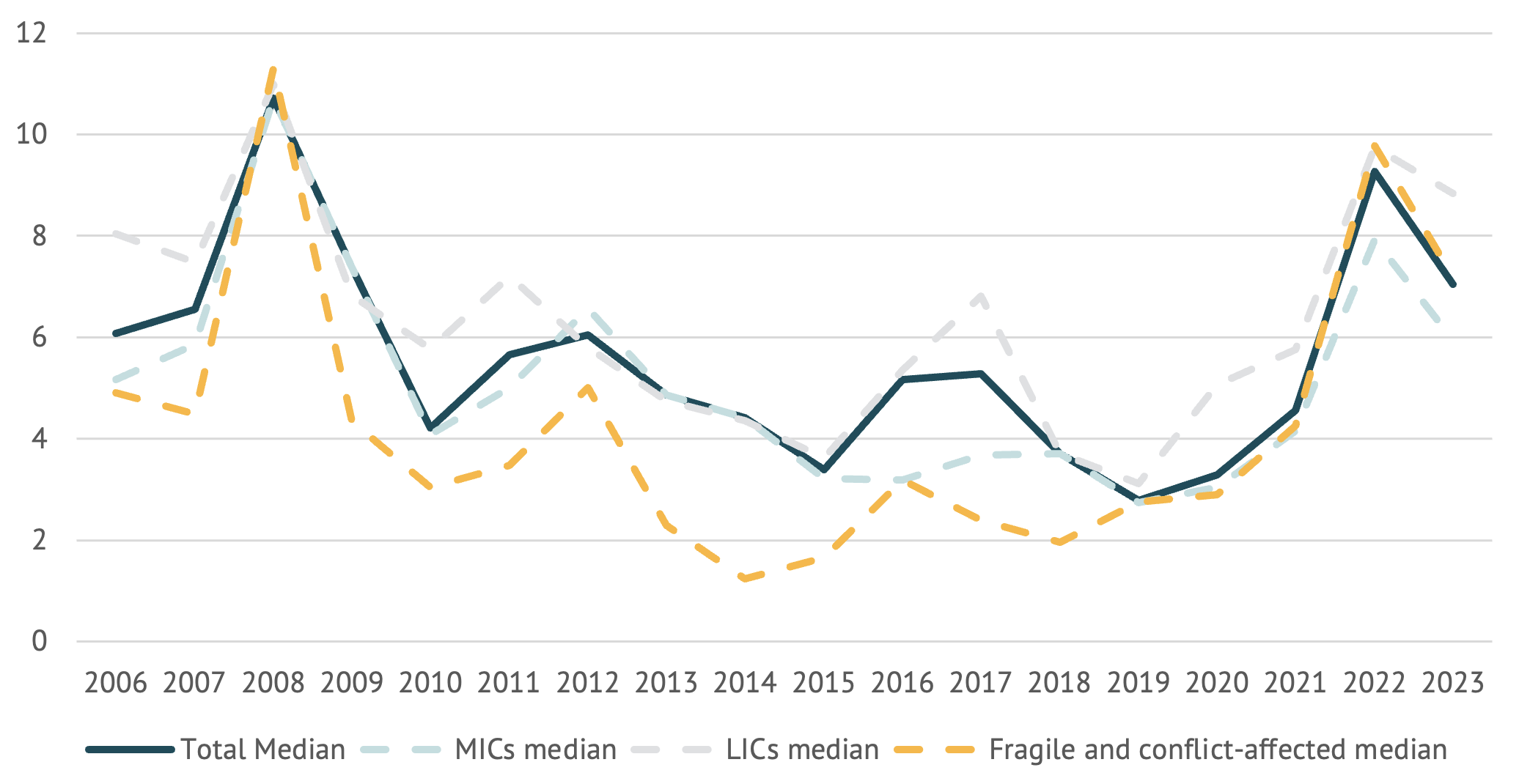

All governments earn a profit from issuing currency because the cost of producing and distributing currency is far lower than its face value. The IMF estimates that seigniorage revenues—measured by changes in the monetary base (currency held by the public plus bank reserves at the central bank)—average about 1.0 to 1.5 percent of GDP annually in Africa. A portion of these revenues is transferred to government budgets each year, depending on national rules (Figure 1), and they are recorded as nontax revenue in government budgets. In developing Asia and advanced economies, seigniorage often exceeds 2 percent of GDP. However, central banks such as the US Federal Reserve and the European Central Bank have not made any transfers in recent years because of losses incurred from quantitative easing policies implemented during the COVID pandemic years.

The spread of stablecoins is likely to shrink this revenue stream in sub-Saharan Africa. The overall fiscal impact will depend on the responsiveness of tax systems to changes in nominal GDP and whether other tax revenues can compensate for the loss. Sub-Saharan Africa’s public finances are especially vulnerable, as the region’s revenue performance has stagnated in recent years and a large share of tax revenues is devoted to interest payments on domestic and external debt--exceeding 30 percent in some countries, such as Ghana, Malawi and Zambia. This leaves many governments struggling to sustain essential spending on education and health.

As Ken Rogoff has noted, over 30 percent of income in developing countries comes from the underground economy, where taxes are routinely evaded. The growing use of cryptocurrencies risks further expanding this unreported sector, compounding revenue mobilization challenges.

Figure 1. Seigniorage revenue, average 2010-18

Source: IMF

Implications for domestic resource mobilization

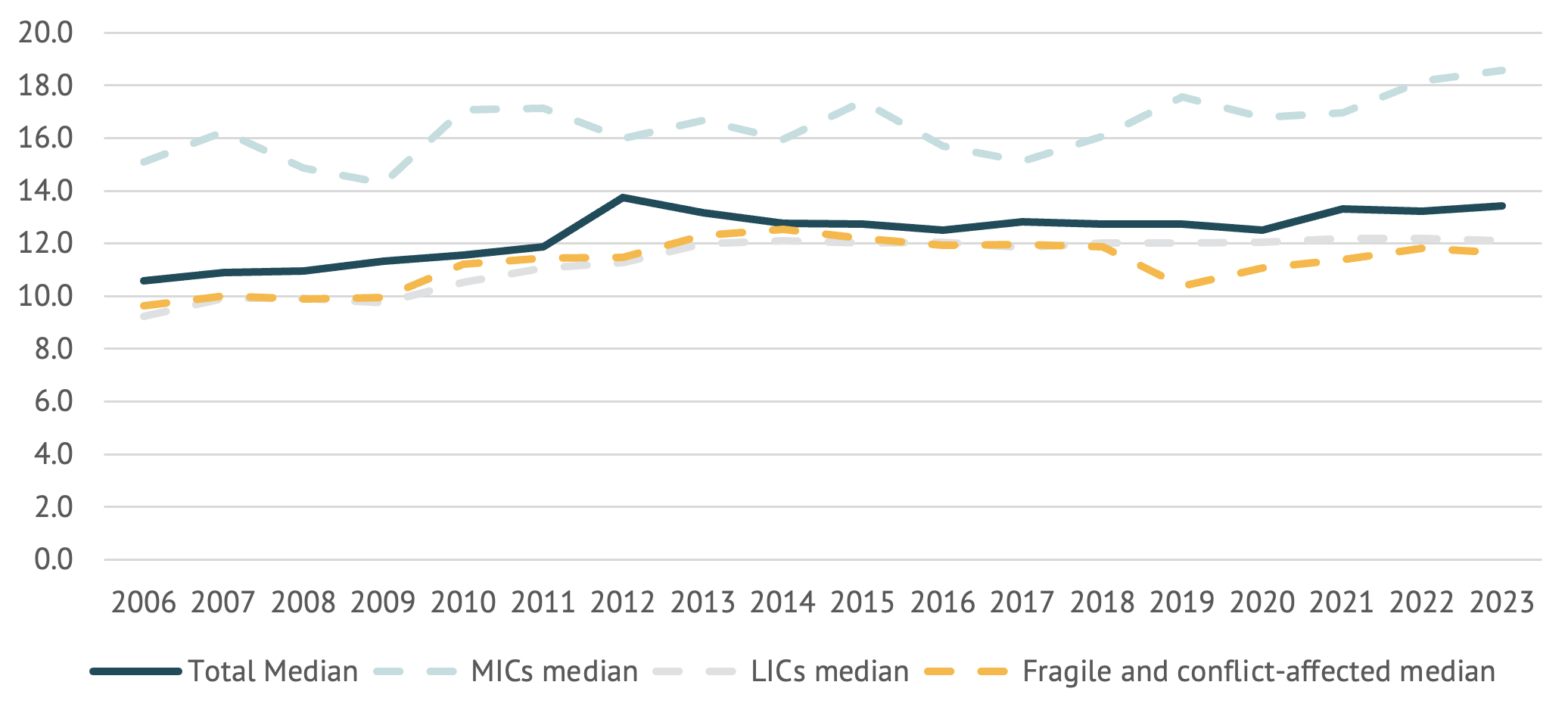

The median tax-to-GDP ratio in sub-Saharan Africa remained virtually unchanged at around 13 percent of GDP between 2012 and 2020—below the IMF’s recommended threshold of 15 percent for sustained development (Figure 2). The expansion of stablecoin use could reduce both seigniorage transferred from central banks to treasuries and the taxable base for income and capital gains, given the greater potential for tax evasion via untraceable transactions. While taxes on income and capital income had begun to grow in some economies, such as Nigeria, this progress risks reversal.

The main fiscal beneficiary of dollar-backed stablecoins will likely be the United States. As US Treasury Secretary Scott Bessent has observed, stablecoins backed by high-quality, liquid assets like Treasury bills could drive at least $2 trillion in annual demand for US Treasuries, funding a substantial share of US budget deficits and lowering borrowing costs—already exceeding 3 percent of GDP in interest payments. In effect, part of the seigniorage revenue now generated in sub-Saharan Africa could flow to the US Treasury, further eroding the tax base of countries already struggling to finance development. The Bank for International Settlements warns that such trends risk loss of monetary sovereignty and capital flight in developing economies.

Figure 2. Sub-Saharan Africa median tax-to-GDP ratio

Source: IMF World Economic Outlook (WEO) General Government taxes, percent of fiscal year GDP. The classification of countries into middle-income, low-income, and fragile and conflict-affected situations is based on the IMF’s Regional Economic Outlook. Note: Chad, Eritrea, Gabon, Somalia, and South Sudan are not included due to a lack of data.

The policy response

To mitigate these risks, sub-Saharan African countries must strengthen macroeconomic management to avoid instability that incentivizes currency substitution. They will need to establish strict regulatory frameworks for cryptocurrency and stablecoins, such as mandatory exchange registration, tax reporting for cryptocurrency transactions, and targeted capital flow measures. Some African countries are moving in this direction. Central banks could also explore offering central bank digital currencies (CBDCs) as a safer, regulated digital alternative to local currency. At the same time, governments should work to unlock their untapped tax potential—about 8 percent of GDP, according to the IMF—through comprehensive tax policy and administration reforms.

I wish to thank Benedict Clements and Udaibir Das for helpful comments.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: jroballo / Adobe Stock