Recommended

Why tax tobacco, alcohol, and sugary drinks?

Developing economies are currently experiencing significant fiscal pressures. Public debt has risen sharply in recent years, while government revenues have largely stagnated. Concurrently, spending needs are growing, both to finance urgent health and social programs as well as the investment needed to transition to a greener economy. Most recently, they have had to cope with the fiscal and growth spillovers of the conflict in the Middle East.

In this challenging environment, raising public revenue will be a critical part of the solution. More than 70 developing economies still collect less than 15 percent of GDP in taxes, below the threshold deemed necessary for sustained growth and effective state capacity (Baer and de Mooij, 2026).

Raising taxes is hard for any government, but one practical and effective solution that addresses both fiscal and public health concerns is taxing tobacco, alcohol, and sugary drinks (Cárdenas and Purisima, 2022). These products are major contributors to preventable diseases such as cancer, diabetes, and cardiovascular conditions. By increasing their prices through taxation, governments can discourage consumption and improve population health. At the same time, these taxes generate revenues that can help ease budget constraints. In doing so, they reduce dependence on external financing and create space for priority spending, including health care.

Revenue potential

A 50 percent increase in prices through taxation could generate an estimated $2.1 trillion over five years in developing economies—equivalent to roughly 40 percent of current public health spending in these countries and surpassing current levels of official development assistance (Task Force on Fiscal Policy for Health, 2019; 2024; Ahmed and Shafik, 2025). If effectively managed, these revenues could bolster public finances and expand access to essential services. These taxes do not slow growth or reduce employment during challenging economic times.

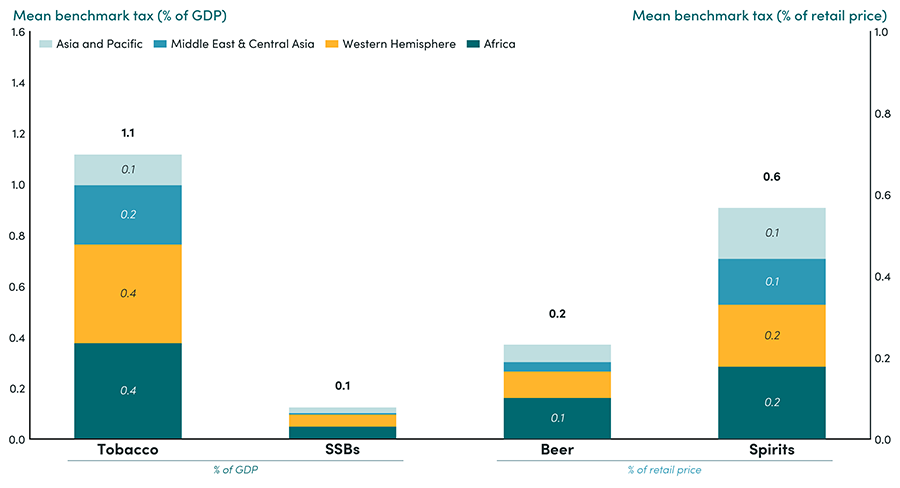

A cross-country benchmarking exercise shows that many countries could gain more revenue from health taxes. Tobacco excise revenues average only about 0.4 percent of GDP, below the estimated benchmarked level of around 1.5 percent (Gupta, Jalles, and Petri-Hidalgo, 2025). Alcohol taxes—especially on spirits—as well as taxes on sugary drinks are also underutilized (Figure 1).

In summary, governments are missing out on additional revenue and health benefits, particularly where consumption is high and administrative capacity exists to implement and enforce higher health taxes. Revenues from tobacco and spirits taxes, for example, remain below estimated benchmark levels in Africa, the Middle East and Central Asia, and the Western Hemisphere.

Figure 1. Estimated benchmark levels for health taxes

Note: Bars show estimated benchmarked levels in different regions. Europe and advanced economies are excluded.

Source: Gupta, Sanjeev, João Tovar Jalles, and Ainhoa Petri-Hidalgo. 2025. Estimating Health Tax Capacity, Effort, and Potential: Evidence from a Global Panel. Center for Global Development.

Health taxes compare favorably against other taxes in terms of economic impact and progressivity

Policymakers must weigh the revenue potential of these taxes against alternatives such as VAT, whilst also considering broader objectives, including impact on economic growth and equity.

All taxes have economic effects, but the evidence suggests health taxes offer distinct advantages. Unlike many other taxes, their economic distortions are intentional: they discourage harmful consumption and encourage shifts toward healthier alternatives. For example, the literature finds no negative impact on employment, as consumers tend to redirect spending to other sectors that are equally or more labor-intensive.

Overall, health taxes are progressive policies. Evidence shows that poorer households are more responsive to price increases and therefore gain a disproportionate share of the health benefits. In addition, health taxes can improve welfare among the poor by reducing illness, increasing productive working years, and lowering out-of-pocket health expenditures (Task Force on Fiscal Policy for Health, 2024).

The IMF and health taxes

The IMF’s primary objectives include promoting international monetary cooperation, supporting trade and economic growth, and discouraging harmful economic policies. In this context, it advises member countries to maintain sound financial policies, including sustainable debt levels and efficient tax systems.

While health policy is not a core focus, the IMF advises member countries on raising domestic revenue in fair, efficient, and administratively feasible ways. As part of its advice on taxation, it recommends health taxes, where appropriate, as a component of a balanced and well-functioning tax system.

Evolution of health taxes in IMF surveillance

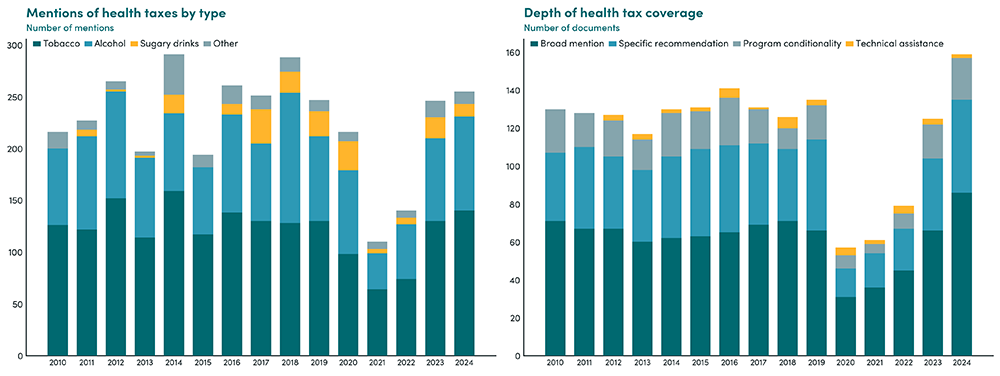

Most references to health taxes in IMF surveillance documents have centered on tobacco and alcohol excise taxes, often lacking concrete recommendations for action (Figure 2) (Gupta and Petri-Hidalgo, 2025). That said, the IMF's focus on health taxes has evolved alongside global conditions:

- Pre-pandemic emphasis: Between 2017 and 2019, the IMF increasingly highlighted excise taxes on tobacco, alcohol, and sugary drinks as fiscal reform and revenue mobilization tools (Figure 2).

- Pandemic and post-pandemic: The COVID-19 pandemic shifted focus toward emergency financing and macroeconomic stabilization, limiting focus on health taxes. However, since 2023, health taxes have regained attention alongside other pressing issues like debt sustainability and climate spending.

Within the context of surveillance, IMF advice to countries on health taxes was not systematically related to the revenue potential of these taxes nor to total tax revenue collections. This pattern holds across all regions.

Figure 2. Health tax mentions in IMF documents, 2010–2024

Note: Panel (a) counts all keyword-level mentions by tax type in IMF Staff Country Reports; a single document may generate multiple mentions across categories. "Other" includes generic health-tax language and any health-tax mention not explicitly tagged as tobacco, alcohol, or SSB. Panel (b) collapses to document–year level and shows the depth of coverage across IMF Staff Country Reports, Program Documents, and Technical Assistance Reports. Broad mentions refer to general references to health taxes without specific policy detail, while specific recommendations indicate concrete policy advice (e.g., changes to tax rates, structure, or design).

Source: Gupta, Sanjeev, and Ainhoa Petri-Hidalgo (2025), "Health Taxes and the IMF: What 15 Years of Policy Advice Reveal." Center for Global Development.

IMF lending programs and capacity development

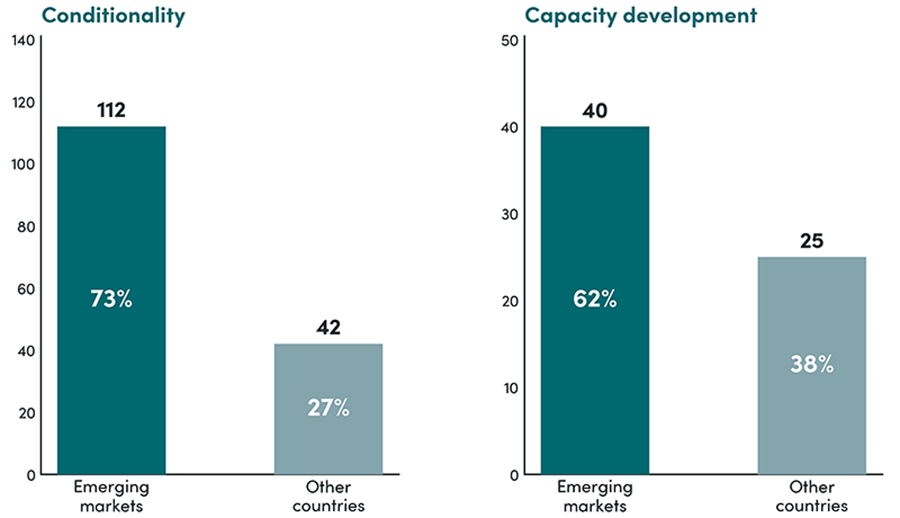

The preceding section showed how IMF advice on health taxes has evolved within its core function of surveillance of member country policies. At the same time, during 2010 to 2019, health taxes became more actively embedded in fiscal reforms supported by IMF lending programs. This engagement intensified in the latter part of the decade, coinciding with growing global attention to noncommunicable diseases, reflected in key publications by the World Health Organization (2017), the UN (2018), and the Task Force on Fiscal Policy for Health (2019). The IMF also released guidance on tobacco excise design during this period (Petit and Nagy, 2016). The IMF's engagement with health taxes has largely been concentrated in emerging markets, with comparatively less emphasis on low-income economies (Figure 3).

Health tax-related conditions in IMF-supported programs have been dominated by tobacco taxation, followed by alcohol, with only a small number of cases referencing sugary drinks. These conditions have been concentrated in emerging market economies, which account for roughly three-quarters of all identified cases (Figure 3). Most measures take the form of structural benchmarks or prior actions under arrangements such as the Extended Credit Facility (ECF) and Extended Fund Facility (EFF).

IMF capacity development—providing hands-on support for tax design and administration—has played an important role where it has been deployed. However, this support has been episodic, reflecting its demand-driven nature, with peaks in selected years such as 2012, 2016, 2018, and 2022. IMF technical assistance that encompasses health taxes has largely focused on emerging market economies (Figure 3).

Limited public availability of technical assistance reports has constrained knowledge sharing and made it difficult to assess the broader impact of these efforts.

Figure 3. IMF health tax engagement is concentrated in emerging markets

Note: Emerging markets defined per IMF WEO classification (EMMIEs). Other includes advanced economies and low-income developing countries. Conditionality counts reflect IMF program-related policy commitments on health taxes at the country–year–document level. Capacity development counts reflect unique country-year pairs where IMF technical assistance on health taxes is documented, whether through published TA reports or references in IMF country documents. Because not all TA reports are published, capacity development activity may be understated.

Source: Gupta, Sanjeev, and Ainhoa Petri-Hidalgo (2025), "Health Taxes and the IMF: What 15 Years of Policy Advice Reveal." Center for Global Development.

Way forward

With fiscal pressures mounting and health burdens rising, the IMF is well positioned to elevate health taxes from underused instruments to a central pillar of domestic revenue mobilization, delivering both stronger public finances and better health outcomes. In this regard, it could consider:

- Embedding health taxes in Medium-Term Revenue Strategies, alongside VAT and income tax reforms, particularly in countries with large revenue gaps and relatively stronger administrative capacity.

- Promoting the expansion of taxes on tobacco where they remain low, emphasizing excise structures that are easier to administer and more effective in reducing consumption that also minimize illicit trade. Staff should also continue to explore the scope for raising excises on alcohol and sugary drinks where feasible.

- Assessing the scope for greater use of health tax measures in IMF-supported programs, including structural benchmarks where appropriate—extending beyond tobacco to alcohol and sugary drinks.

- Capacity development on tax policy and administration in developing countries should more systematically incorporate health taxes, with a focus on excise design, tax administration, and compliance enforcement—including measures to curb illicit trade. Expanding public access to technical assistance reports would strengthen knowledge sharing and support better evaluation of what works.

The authors are grateful to Ainhoa Petri-Hidalgo for her contributions to this brief.

References

Ahmed, M. and Shafik, M. (2025) ‘The case for health taxes’, Finance & Development, March. Washington, DC: International Monetary Fund. Available at: https://www.imf.org/en/publications/fandd/issues/2025/03/point-of-view-…

Baer, K. and de Mooij, R. (2026) ‘The art of taxation’, Finance & Development, March. Washington, DC: International Monetary Fund. Available at: https://www.imf.org/en/publications/fandd/issues/2026/03/back-to-basics…

Cárdenas, M. and Purisima, C. (2022) ‘Excise taxes on tobacco, alcohol, and sugary beverages benefit health and public budgets’, STAT News, 30 November. Available at: https://www.statnews.com/2022/11/30/excise-taxes-on-tobacco-alcohol-and…

Gupta, S., Jalles, J.T. and Petri-Hidalgo, A. (2025) Estimating Health Tax Capacity, Effort, and Potential: Evidence from a Global Panel. CGD Working Paper 726. Washington, DC: Center for Global Development.

Gupta, S. and Petri-Hidalgo, A. (2025) Health Taxes and the IMF: What 15 Years of Policy Advice Reveal. CGD Working Paper 733. Washington, DC: Center for Global Development.

Gupta, S. and Petri-Hidalgo, A. (2026) ‘Health Taxes and the IMF: Are Support and Reform Aligned?’ CGD Blog, 16 April. Available at: https://www.cgdev.org/blog/health-taxes-and-imf-are-support-and-reform-…

Petit, P. and Nagy, J. (2016) How to Design and Enforce Tobacco Excises? Washington, DC: International Monetary Fund.

Task Force on Fiscal Policy for Health (2019) Health Taxes to Save Lives: Employing Effective Excise Taxes on Tobacco, Alcohol, and Sugary Beverages. New York: Bloomberg Philanthropies.

Task Force on Fiscal Policy for Health (2024) Health Taxes: A Compelling Policy for the Crises of Today. New York: Bloomberg Philanthropies.

United Nations (2018) Third UN High-level Meeting on Non-communicable Diseases. 28 September. New York: United Nations.

World Health Organization (2017) Tackling NCDs: “Best Buys”. Geneva: World Health Organization.

Topics

CITATION

Ahmed, Masood, and Sanjeev Gupta. 2026. Health Taxes and the IMF. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: KC Shum/Upsplash