Recommended

This note was originally published in draft form before Gavi’s March 2019 board retreat. You can view the original draft version here.

Introduction

Market shaping and procurement constitute a core approach to achieve Gavi’s mission to accelerate access to and increase equitable coverage of vaccines.[1] Gavi drives lower prices and ensures the supply of high-quality vaccines through a range of tools such as pooling demand with assured funding, offering multi-year contracts, and encouraging new suppliers to enter the market, among others.[2] Gavi has made notable progress, including securing a sustainable and affordable supply of pentavalent, pneumococcal conjugate (PCV), and rotavirus vaccines;[3] expanding and diversifying the manufacturer base;[4] and developing demand forecasts to give manufacturers longer-term market visibility.[5] These efforts have no doubt provided benefits to Gavi-supported countries, and they have also had some positive spillovers in Gavi-ineligible countries.

Yet several challenges—stemming in part from countries transitioning from Gavi support and an evolving vaccine manufacturer landscape—may impede Gavi’s ability to effectively deliver on its mission in the future. The next five-year strategy (Gavi 5.0) is an opportunity to evolve—and possibly broaden—Gavi’s role in market shaping and procurement. Looking ahead, Gavi will need to more carefully assess the implications of its market-shaping strategies beyond Gavi-supported countries—and consider ways to potentially extend its benefits to the entire universe of low- and middle-income countries. And as more countries transition, a scaling back of Gavi’s role in directly financing and purchasing vaccines will merit a concurrent scaling up of efforts to strengthen the procurement enabling environment. Supporting countries today to access affordable, high-quality vaccines through targeted market shaping and enhanced procurement support will empower them to make existing budgets go further in the future, freeing up resources to expand coverage and introduce new vaccines.

In this note, we diagnose key challenges that will strain Gavi’s model during the 2021-2025 period and beyond. We then offer recommendations for an evolving approach, which closely align with Gavi’s goal to maximize the impact of countries’ current and future domestic investments.

Challenges on the Horizon

Constraints in specific vaccine markets are putting pressure on Gavi’s market shaping tools, with broad-reaching implications for Gavi countries

Market constraints at the global level hinder countries’ abilities to access a timely, stable, and affordable supply of high-quality vaccines to meet their needs. Procurement inefficiencies and supply breakdowns can lead to disruptions in immunization programs and can be an important driver of under-vaccination; they may also contribute to delayed or deferred introductions.[6] Nevertheless, some Gavi-supported countries are introducing vaccines, even as data reveal a stagnation in coverage rates of basic vaccines and/or earlier-introduced new and underused vaccines at suboptimal levels.[7] One hypothesis suggests that Gavi’s approach to demand consolidation may emphasize new introductions to achieve sufficient volumes across countries to access favorable prices, underscoring the need to carefully balance trade-offs across priorities.

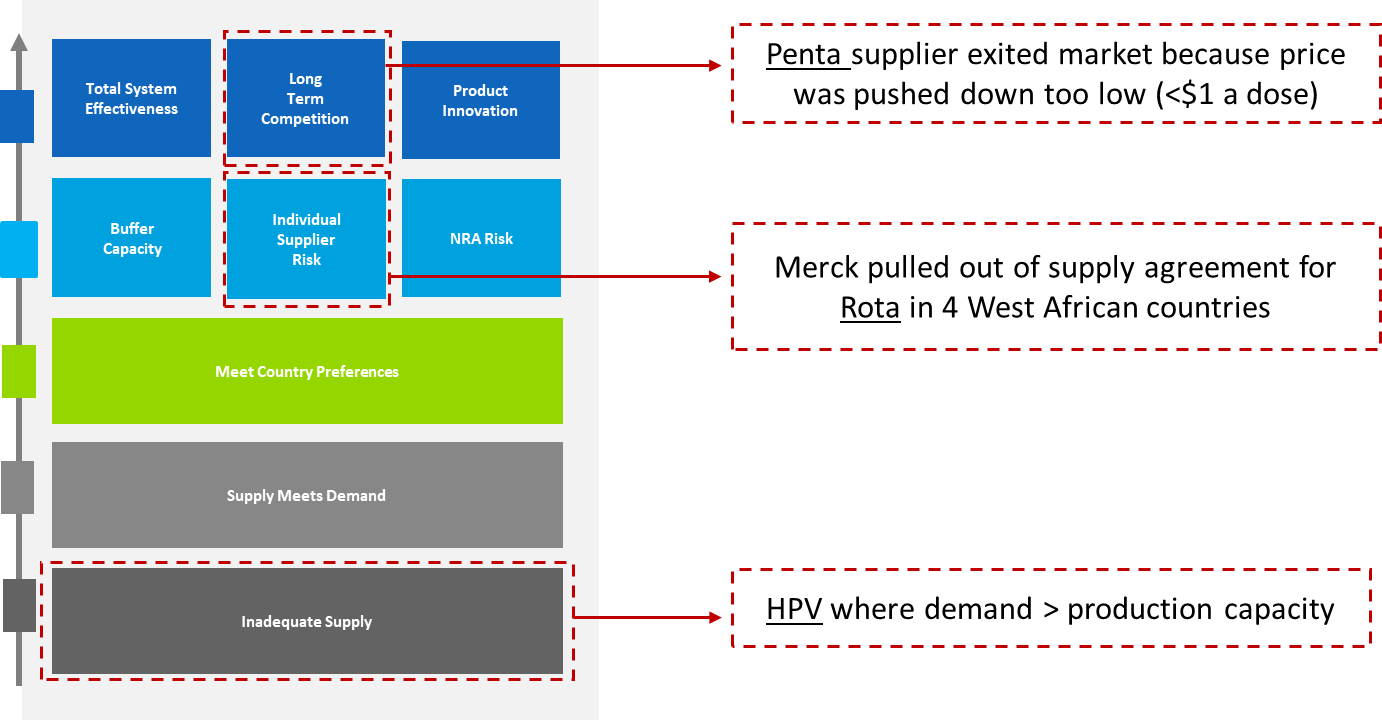

Further, constraints related to supply and competition for specific vaccines at the global level are putting increasing pressure on Gavi’s market shaping tools (see figure 1). In the case of the human papillomavirus vaccine (HPV), increased demand from countries, driven in part by Gavi’s own efforts to boost introduction, is outstripping production capacity.[8] For the pentavalent vaccine (Penta), where prices have been pushed below $1 per dose, one manufacturer exited the market in 2017.[9] While other manufacturers remain, this nevertheless illustrates the importance of balancing trade-offs between price and supply security. Last year, Merck pulled out of its agreement with Gavi and UNICEF to provide rotavirus vaccine (Rota) to four West African countries[10], potentially redirecting product to the more lucrative market in China, as some reports suggested.[11] This case underscores certain risks of nonbinding agreements where there may be little or no recourse when manufacturers renege on commitments. [12] Ultimately, it also highlights the need to better understand the implications of Gavi’s market shaping strategies on the broader market landscape.

Figure 1. Illustrative examples of pressures on Gavi’s market shaping tools, based on the healthy markets framework

Source: Authors, based on the 2015 Healthy Markets Framework developed by Gavi, UNICEF, BMGF, available here.

Countries that are not eligible for Gavi support face high and unpredictable vaccine prices, undermining coverage and new introductions; this may be indicative of future challenges for transitioning countries

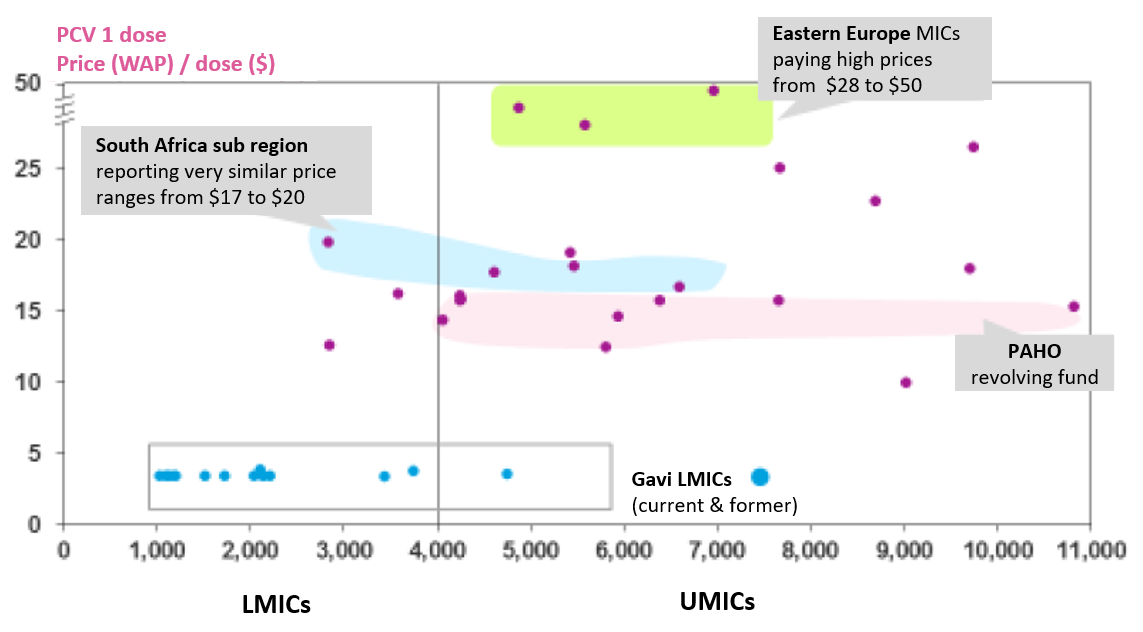

High vaccine prices pose a critical problem in many middle-income countries—and notably among the cohort of never-Gavi eligible countries. Figure 2 illustrates significant variation in prices paid across lower-middle and upper-middle income countries for a single dose of PCV. In comparison to the multi-year supply agreement price of $3.03 to $3.30 per dose available to Gavi countries, non-Gavi middle-income countries in Southern Africa pay $17 - $20 for a single dose, while those in Eastern Europe pay as much as $28 - $50.[13] While the underlying cause of price dispersion is not immediately obvious, it may suggest a tiered pricing strategy by suppliers. In theory, tiered pricing can help improve access, however in practice, higher prices have proven to be locally cost-ineffective in some middle-income country contexts (e.g., Thailand).[14] Other potential factors that may contribute to price variation include small purchase volumes, the type and length of contracts, and specific payment modalities or payment delays.[15]

Data also suggest that self-procuring middle-income countries may pay higher—and more variable—prices than those procuring through UNICEF Supply Division or PAHO’s Revolving Fund (see table 1). (The reasons why countries choose to self-procure are many-fold and may include laws or other political economy factors that prevent the use of external procurement agents; cash flow constraints to meet UNICEF’s pre-payment requirement;[16] the desire to exercise country preferences in product choice; and national industrial policies that favor local producers, among others.[17])

High prices are an important driver of underperformance on vaccine coverage, and may also deter new introductions. For example, never-Gavi countries lag behind current and former Gavi countries on PCV introduction.[18] This may be because PCV is locally cost-ineffective at current market prices, though it would be cost-effective at the Gavi price; it may also be an issue of limited fiscal space.

Figure 2. High—and highly variable—vaccine prices for PCV across middle-income countries

Source: Gavi Report to the Board, Annex B: Supplementary contextual analysis, available here. Data represent 2016 prices reported to the V3P database (country names are anonymized).

Table 1. 2016 price per dose for PCV across middle-income countries, by Gavi eligibility and procurement mechanism

| PCV 2016 | Gavi/Non-Gavi | Procurement Mechanism | Average Price | Price Range | N |

|---|---|---|---|---|---|

| LMIC | Gavi | UNICEF SD | 3.58 | $3.05-7.89 | 24 |

| Non-Gavi | Self-procurement |

16.9 |

$12.51-19.83 | 4 | |

| UMIC | Gavi | UNICEF SD | 3.41 | $3.14-3.68 | 5 |

| Non-Gavi | UNICEF SD | 20.50 | $16.00-25.00 | 2 | |

| Non-Gavi | PAHO Revolving Fund | 13.71 | $7.62-15.58 | 8 | |

| Non-Gavi | Self-procurement | 25.81 | $9.85-49.99 | 15 |

Source: Authors based on 2016 price data for PCV reported to the V3P database (country names are anonymized).

This reality may be indicative of future problems for Gavi graduates. Transitioned countries can access multi-year supply agreement prices through manufacturer commitments via UNICEF or PAHO (Gavi’s designated procurement agents). This support helps smooth the transition process. However, it applies to select vaccines, is time limited with varying lengths, and has many exceptions, and the nonbinding nature of commitments can create uncertainty.[19] Moreover, the unpredictability of vaccine prices offered in response to national tenders affects budgeting and planning for self-financing countries. For example, India’s recent domestic inactivated polio vaccine (IPV) tender saw an unexpected 80 percent price increase, prompting the government to request 50 percent cost-sharing support from Gavi of $40 million over 2019-2021.[20] This is a unique case, but it may illustrate the nature of challenges to come.

Several large middle-income countries that are top recipients of Gavi support—notably Nigeria, India, Pakistan, and Bangladesh—are projected to be fully self-financing by 2030.[21] Accordingly, Gavi’s leverage in negotiating lower prices through pooling demand alone may become constrained. This could exacerbate pricing challenges, as manufacturers may, for example, face greater unpredictably related to payments and tendering; in some cases, they could raise prices to account for higher transaction costs to serve more fragmented markets.

Many middle-income countries have weak capacity in procurement and related functions

The sustainability of Gavi’s approach to transition will ultimately hinge on countries being able to manage the procurement process and related functions themselves.[22] Yet numerous impediments to successful procurement remain. Key barriers, as identified by CGD’s Working Group on the Future of Global Health Procurement[23] and other studies,[24] include weak capabilities, institutions, and processes to assume self-procurement, as well as weak regulatory capacity, most notably in transitioning countries. Furthermore, Gavi-supported technical assistance, delivered by Gavi partners, appears more geared toward vaccine delivery. While downstream supply chain issues certainly pose a critical barrier to effective and equitable coverage, procurement processes further upstream merit greater attention.

Recommendations for Gavi’s Future Approach

1. Offer stronger incentives to manufacturers to ensure a stable vaccine supply and assure that market shaping efforts prioritize outcomes achieved beyond Gavi markets.

Gavi should continue to broaden the scope of its market analyses to better understand the (positive and negative) implications of its market shaping strategies on non-Gavi markets, with priority to limited competition vaccine markets. Similarly, Gavi should also continue to prioritize a wide range of market shaping tools to attract new suppliers to market and drive innovation, including advance purchase commitments and volume guarantees, where applicable. One possibility could be an AMC/APC-type mechanism for an IPV-containing hexavalent vaccine, though attention should be paid to creating the kinds of incentives that would enable adequate and growing future supply while still assuring viable markets for pentavalent and standalone IPV as hexavalent is gaining acceptance and adoption.

At the same time, Gavi should invest in strategically expanding the menu of procurement modalities, in collaboration with partners such as UNICEF. As one example, Gavi could systematically pilot, evaluate, and adopt auction-like tools in vaccine markets with adequate supply and competition. (Currently, only the Penta market has adequate supply and competition but Gavi and partners could look to apply auction designs to other vaccine markets that meet this description in the future.) A range of design instruments could help achieve supply security and lower prices—such as a phased approach where portions of total forecasted quantities are awarded in multiple rounds (as was the case with the 2016 pentavalent tender[25]) or allocation of quantities across multiple suppliers.

Finally, Gavi could expand demand forecasts to include self-financing and/or self-procuring middle-income countries in select vaccine markets where demand predictability may be an issue. This could be built into the existing Vaccine Product, Price, and Procurement (V3P) platform, managed by WHO, which aggregates vaccine purchase data for some 150 countries.[26] This may also be relevant within the framework of an Innovation Partnership with one or more middle-income countries to drive vaccine research and development.[27]

2. Consider a better-adapted set of modalities related to vaccine support for transitioning and, where relevant, ineligible countries.

Where specific vaccines exceed local cost-effectiveness thresholds, Gavi could consider providing a modest subsidy to fill the gap between the vaccine price and the level at which it becomes locally cost-effective. This modality would be relevant to self-financing transitioned countries—and in certain never-Gavi countries—for specific high-priority vaccines. It would help ensure adequate volumes to be sustained to enable further market shaping work that relies on aggregated volumes to achieve sustainable pricing.[28]

For limited competition vaccines, Gavi could also enable buy-ins from non-eligible countries and secure appropriate tiered pricing tied to local affordability and cost-effectiveness through globally negotiated agreements. This could potentially help address constraints to vaccine introductions in some Gavi-ineligible countries where market prices exceed local cost-effectiveness thresholds.

In collaboration with UNICEF, Gavi could expand the Vaccine Independence Initiative (VII) to make bridge funding available to a greater number of self-financing countries that face liquidity constraints to pre-payment. The VII—whose scope was expanded to all essential commodities in 2015—has a current capital base of $100 million; pre-financing requests are expected to reach an estimated US$225 million by 2020.[29]

In a similar vein, Gavi could work with partners and manufacturers to achieve greater predictability in pricing agreements available to transitioning and transitioned countries to facilitate more accurate, reliable budgeting and planning.

3. Taking a longer-term view, prioritize the underlying enabling environment for vaccine procurement in transitioning, transitioned, and potentially never-Gavi countries.

Incorporating a standardized assessment of procurement bottlenecks and performance indicators (see below) into multi-partner Transition Assessments, as Gavi and partners are working to do, would help ensure barriers are sufficiently addressed during the transition planning processes. Where applicable, Gavi should continue to prioritize greater investments in targeted assistance for procurement and procurement-related functions (e.g., product selection, regulatory capacity, etc.) through existing modalities, including Gavi Transition Plans and Post-Transition Engagement. A more deliberate focus on building capacity over the long-term is a necessary complement to short-term support. This support could include trainings to boost demand for and use of data and market information currently available through the V3P/MI4A project to improve decision-making. Gavi’s targeted support in this area could consider a results-orientation, linking financing to the achievement of measurable outcomes.

In collaboration with partners, Gavi should also consider extending technical assistance for priority-setting around adoption/introduction, product selection, and procurement processes to never-Gavi countries that are lagging in these capacities.

Finally, working closely with partners and funders (e.g., UNICEF, WHO, PAHO, BMGF, and the World Bank), Gavi should prioritize the provision of procurement-related public goods available to all countries, such as:

-

standardized procurement performance indicators (KPIs)

-

building an evidence base of strategic practices for vaccine procurement to achieve price reductions while also maintaining supply security (recommendation 1, above)

-

support for expedited drug registration processes at country-level to lower transactions costs and barriers to entry.

This note is part of a series on the future of Gavi. You can find the full list of notes here:

[1] See the accompanying note in this series titled, “Gavi’s Approach to Health Systems Strengthening (HSS): Reforms for Enhanced Effectiveness and Relevance in the 2021-2025 Strategy” which focuses on delivery platforms to ensure those vaccines reach their target populations —another key pillar of Gavi’s vaccine support.

[2] Market shaping is the fourth strategic goal in the 2016-2020 strategy. See: https://www.gavi.org/about/strategy/phase-iv-2016-20/market-shaping-goal/

[3] The weighted-average-price of immunizing a child with a full course of pentavalent, pneumococcal conjugate, and rotavirus vaccines fell from $35 in 2010 to less than $17 in 2017. (“Supply and Procurement Strategy 2016-20.” Gavi, the Vaccine Alliance, n.d. https://www.gavi.org/library/gavi-documents/supply-procurement/supply-and-procurement-strategy-2016-20/;

“2016-2020 Mid-Term Review Report.” Gavi, the Vaccine Alliance, November 2018. https://www.gavi.org/library/publications/gavi/gavi-2016-2020-mid-term-review-report/)

[4] The number of manufacturers supplying Gavi-eligible countries has increased from 5 in 2000 to 17 in 2017. (“Supply and Procurement Strategy 2016-20.”; “2016-2020 Mid-Term Review Report.”)

[5] “Supply and Procurement Strategy 2016-20.”

[6] “Pre-empting and Responding to Vaccine Supply Shortages.” WHO SAGE, April 2016. https://www.who.int/immunization/sage/meetings/2016/april/1_Mariat_shortages_SAGE_2016.pdf

[7] For more details, see the accompanying note in this series titled, “Vaccine Introduction and Coverage in Gavi-Supported Countries 2015-2018: Implications for Gavi 5.0.”

[8] “2016-2020 Mid-Term Review Report.”; “Report to the Board—2016 -2020 Strategy: Progress, Challenges, and Risks.” Gavi, the Vaccine Alliance, November 2018. https://www.gavi.org/about/governance/gavi-board/minutes/2018/28-nov/minutes/03---2016-2020-strategy---progress-challenges-and-risks/

[9] “2016-2020 Mid-Term Review Report.”

[10] “2016-2020 Mid-Term Review Report.”; “Report to the Board—2016 -2020 Strategy: Progress, Challenges, and Risks.”

[11] Doucleff, Michaeleen. “Merck Pulls Out Of Agreement To Supply Life-Saving Vaccine To Millions Of Kids.” National Public Radio (NPR), November 2018. https://www.npr.org/sections/goatsandsoda/2018/11/01/655844287/merck-pulls-out-of-agreement-to-supply-life-saving-vaccine-to-millions-of-kids

[12] We acknowledge that the current structure of agreements can have benefits and drawbacks. In some instances, nonbinding agreements can be of good service to stewardship of donor funds, by not requiring Gavi to procure doses it may not need if there is a delay in country readiness pushing out a vaccine introduction date, for example.

[13] “Report to the Board—Annex B: Supplementary Contextual Analyses.” Gavi, the Vaccine Alliance, November 2018. https://www.gavi.org/about/governance/gavi-board/minutes/2018/28-nov/minutes/11---annex-b---supplementary-contextual-analyses/

[14] See Thailand example cited in the accompanying note in this series titled, “New Modalities for a Changing World.”

[15] Silverman, Rachel, Janeen Madan Keller, Amanda Glassman, and Kalipso Chalkidou. “Tackling the Triple Transition in Global Health Procurement.” June 2019. Final Report of CGD’s Working Group on the Future of Global Health Procurement. /better-health-procurement; Kaddar, Miloud, Helen Saxenian, Kamel Senouci, Ezzeddine Mohsni, and Nahad Sadr-Azodi. “Vaccine procurement in the Middle East and North Africa region: Challenges and ways of improving program efficiency and fiscal space.” Vaccine, volume 37, issue 27 (2019): 3520-3528. https://doi.org/10.1016/j.vaccine.2019.04.029

[16] UNICEF’s Vaccine Independence Initiative (VII), discussed later in this note, helps address this issue.

[17] Note that a country may choose to use an external procurement agent such as UNICEF or PAHO for certain vaccines but opt to self-procure others. (Arias, Daniel, Cheryl Cashin, Danielle Bloom, Helen Saxenian, and Paul Wilson. “Immunization Financing: A Resource Guide for Advocates, Policymakers, and Program Managers.” Washington, DC: Results for Development. 2017.

https://www.r4d.org/resources/immunization-financing-resource-guide-advocates-policymakers-program-managers/; Kaddar et al 2019)

[18] “Report to the Board—Annex B: Supplementary Contextual Analyses.”; “Report to the Board—Gavi 5.0: The Alliance’s 2021-2025 Strategy.” Gavi, the Vaccine Alliance, November 2018. https://www.gavi.org/about/governance/gavi-board/minutes/2018/28-nov/minutes/11---gavi-5-0---the-alliance-s-2021-2025-strategy/

[19] “Vaccine Pricing: Gavi Transitioning Countries.” WHO Vaccine Product, Price and Procurement (V3P) project, December 2017. http://lnct.global/wp-content/uploads/2018/02/Vaccine-Pricing-for-GAVI-Transitioning-Countries-1.pdf; Saxenian, Helen, Robert Hecht, Miloud Kaddar, Sarah Schmitt, Theresa Ryckman, and Santiago Cornejo. “Overcoming Challenges to Sustainable Immunization Financing: Early Experiences from Gavi Graduating Countries.” Health Policy and Planning, volume 30, issue 2 (2015): 197-205. https://doi.org/10.1093/heapol/czu003

[20] Although Gavi eligible, the government of India agreed to self-fund its IPV program. The India IPV decision was approved by Gavi’s Board in November 2018. See: https://www.gavi.org/about/governance/gavi-board/minutes/2018/28-nov/presentations/12---gavi-s-support-for-ipv-post-2020/

[21] See the accompanying note in this series titled, “New Modalities for a Changing World.”

[22] Kallenberg, Judith, Wilson Mok, Robert Newman, Aurélia Nguyen, Theresa Ryckman, Helen Saxenian, and Paul Wilson. “Gavi’s Transition Policy: Moving From Development Assistance To Domestic Financing Of Immunization Programs.” Health Affairs: Vaccines, vol 35, no. 2 (2016): 250-258. https://doi.org/10.1377/hlthaff.2015.1079

[23] Silverman, Rachel, Janeen Madan Keller, Amanda Glassman, and Kalipso Chalkidou. “Tackling the Triple Transition in Global Health Procurement.” June 2019. Final Report of CGD’s Working Group on the Future of Global Health Procurement. For more details see: /better-health-procurement

[24] Cernuschi, Tania, Stephanie Gaglione, and Fiammetta Bozzanic. “Challenges to sustainable immunization systems in Gavi transitioning countries.” Vaccine, vol 36, issue 45 (2018): 6858-6866. https://doi.org/10.1016/j.vaccine.2018.06.012; Kallenberg et al 2016; Saxenian et al 2015; Kaddar et al 2019.

[25] “Supply of Children’s Five-in-One Vaccine Secured at Lowest-Ever Price.” UNICEF, October 2016. https://www.unicef.org/supply/files/UNICEF_release_penta_pricing_19OCT16.pdf

[26] “Global Vaccine Market Report.” WHO V3P project, October 2018. https://www.who.int/immunization/programmes_systems/procurement/v3p/platform/module2/MI4A_Global_Vaccine_Market_Report.pdf?ua=1

[27] See accompanying note in this series titled, “New Modalities for a Changing World.”

[28] See accompanying note in this series titled, “New Modalities for a Changing World.”

[29] “The Expansion of the Vaccine Independence Initiative (VII): Protecting Children with Life-Saving Supplies.” UNICEF Financial Innovation Lab, n.d. https://www.unicef.org/supply/files/INNOVATION_LAB_LFLT_Ver1_Single_Pages.pdf; Arias et al 2017.

Topics

CITATION

Madan Keller, Janeen, and Amanda Glassman. 2019. Gavi’s Role in Market Shaping and Procurement: Progress, Challenges, and Recommendations for an Evolving Approach. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.