Recommended

From the final decade of the twentieth century, four small economies were quick to capitalize on the developmental advantages conffered by globalization. Although they did not escape buffeting from periodic regional and international crises, Dubai, Ireland, Panama, and Singapore managed to sustain moderately high average rates of gross domestic product (GDP) growth for well over 25 years (Figure 1).[1] Between 1990 and 2019, Ireland, Panama and Singapore had achieved close to sixfold increase in per capita GDP. Per capita GDP of the United Arab Emirates was 1.5 times higher—although that of Dubai, the second most prosperous Emirate, may have doubled (Figure 2).[2] By 2019, Dubai, Ireland, and Singapore were at or near the topmost rung of the global income ladder, while Panama, starting from a low base, had entered the ranks of the high-income countries.

Figure 1. Annual growth of GDP 1990-2019

Source: WDI (2021) https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?end=2018&locations=PA-IE-SG-AE&start=1990

Figure 2. GDP per capita: 1990-2019

Source: WDI (2021) https://data.worldbank.org/indicator/NY.GDP.PCAP.CD?end=2019&locations=IE-PA-SG-AE&start=1990

Economic performance of this order has eluded most other economies small and large, which is why the “fabulous four” have attracted analytic scrutiny from social scientists looking for a formula that other countries could apply. Research to date on the four has checked many of conventional boxes. But that does not suffice to explain the lead these economies have enjoyed over others in their regions.

Conventional growth enablers

Dubai, Ireland, Panama, and Singapore benefitted from geographical location (proximity to major markets, along trade routes, not landlocked), excellent connectivity, political stability, adequate or better quality of governance relative to their reference groups, a favorable business environment, and an entrepreneurial readiness to exploit opportunities[3]. All four (including Dubai[4]) are relatively resource poor. Industry or services, or in two cases both (Singapore and Ireland), have served as the drivers of growth. The consistent and far-sighted developmental focus of the state in Singapore and Dubai—and to a lesser extent of governments in Ireland and Panama—was instrumental in maintaining the tempo of economic activity. Growth was buttressed by a high or moderately high rates of gross investment albeit with considerable seesawing of levels as can be seen from Figure 3. In the 1990s, Singapore and Panama had the highest rates of investment. From around the turn of the century, capital formation in Singapore sank below 30 percent of GDP and since then, the average percentage has remained in the upper 20s fairly close to that of the United Arab Emirates (UAE). From 15 percent of GDP in 1993, the Irish investment rate rose to 32 percent in 2006, plummeted sharply during the financial crisis and its aftermath in 2009-2011 and has risen steeply since to 46 percent in 2019.[5] Investment in transport, telecom, and energy infrastructures and in urban services, supported industrialization and trade and steadily improved urban livability.

Figure 3. Gross capital formation: 1990-2019

Source: WDI (2021) https://data.worldbank.org/indicator/NE.GDI.TOTL.ZS?end=2019&locations=IE-PA-SG-AE&start=1990

Openness has been the hallmark of all four economies. Trade as a percentage of GDP was and is far above the global average, as is the exposure to capital flows. Tradable services have complemented manufacturing as sectoral sources of growth in Singapore and Ireland, while they have emerged as the mainstay of Panama and Dubai, which function as regional transport and financial hubs.[6] Revenue from international tourism added up to a fourth or more of total export earnings in 2019 for Ireland, Panama, and Dubai, with only Singapore trailing in the low single digits.[7]

Growth factors plus

Viewed through the lens of growth economics, the four met most of the enabling conditions, but to sustain a high rate of growth over an extended period, they drew additional impetus from three factors, which are somewhat unique and differentiate their strategies from other small open economies and from the strategies adopted by Korea and Taiwan.[8] Their growth performance was aided by: (i) large inflows of capital—foreign direct investment, equity capital and money from a variety of quarters seeking a secure haven; (ii) the influx of migrants both skilled and unskilled; and (iii) by the absorption of technology much of it channeled through foreign direct investment (FDI) and the knowledge capital of foreign workers.

Foreign capital

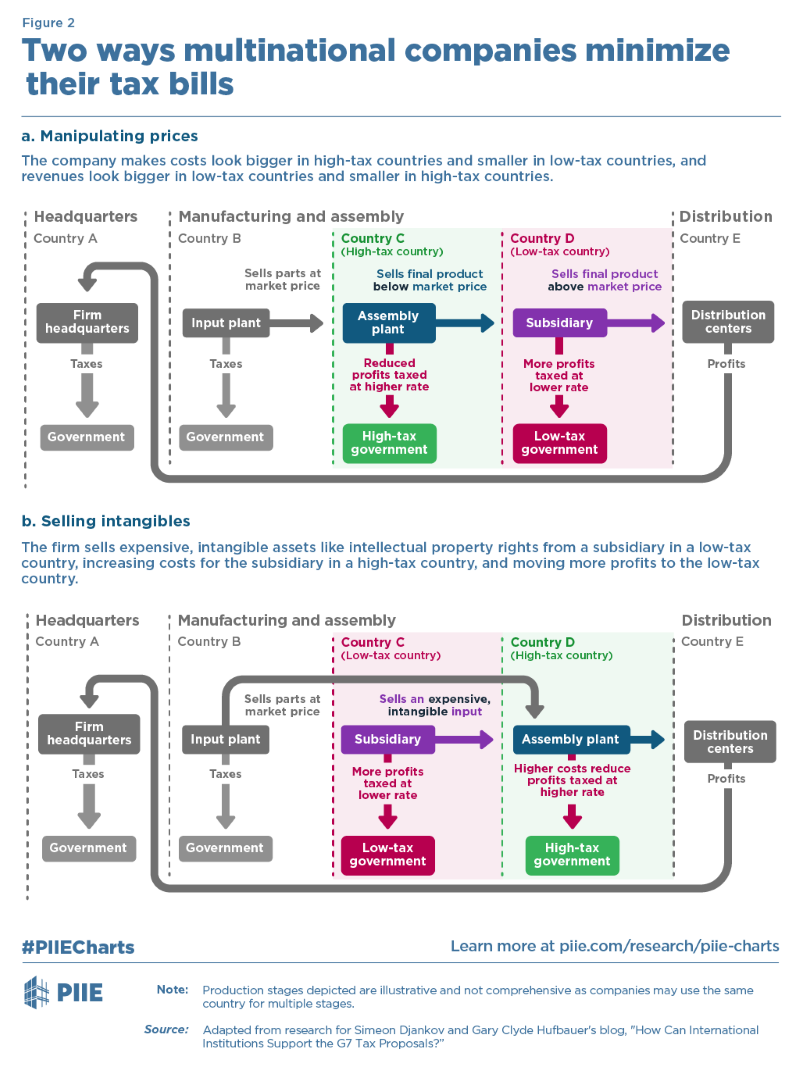

FDI has flowed into these economies for the reasons listed above but also because of numerous tax and other incentives.[9] Most notably, corporate tax rates were well below those levied by most advanced economies and the United States. Rates averaging 12.5 percent in Ireland, 17 percent in Singapore, and zero percent in the Free Zones of Dubai and Panama were a major draw for multi-national corporations (MNCs).[10] For example, Ireland became a magnet for American MNCs wanting to minimize their tax burdens, and MNCs from other countries with high corporate tax rates followed suit. That locating production facilities in Ireland allowed American companies tariff free access to the EU market was a bonus. The compressed,[11] export-oriented industrialization of Ireland and Singapore and their rapid diversification into complex, high tech products resulted from investment by MNCs. The contribution of homegrown firms was modest. Moreover, it was capital from abroad that led to the rise of the tradable services sector in Panama and Dubai. Panama consolidated its position as a regional business hub by incentivizing MNCs to establish their regional headquarters in the capital city (Law of Multinational Headquarters, SEM), with as many as 120 making it their home in Central America.[12] More than a third of companies on the Fortune 500 list have their regional headquarters in Singapore and they have been joined by 7,000 MNCs from around the world.[13]

But there is less to FDI than meets the eye. As Brad Setser noted (2019),[14] “A lot of financial globalization is driven by tax avoidance.”[15] To shelter their earnings, companies and individuals create corporate shells in tax havens and as much as 40 percent of what is classified as FDI—amounting to $15 trillion—does not take the form of plant and equipment but instead is “phantom FDI.”[16] It is not just Ireland that owes its prosperity in part to the influx of capital, phantom and other. Damgaard, Elkjaer, and Johannsen (2019)[17] estimate that “Eight major pass-through economies—the Netherlands, Luxembourg, Hong Kong SAR, the British Virgin Islands, Bermuda, the Cayman Islands, Ireland, and Singapore—host more than 85 percent of the world’s investment in special purpose entities, which are often set up for tax reasons. The characteristics of these entities include legal registration subject to national law, ultimate ownership by foreigners, few or no employees, little or no production in the host economy, little or no physical presence, mostly foreign assets and liabilities, and group financing or holding activities as their core business.” To these eight, one can add Dubai.

Figure 4. How MNCs shave their tax bills

Source: S. Djankov (2021) https://www.piie.com/research/piie-charts/some-ways-multinational-companies-reduce-their-tax-bills

Singapore, much like Switzerland, enhanced its appeal to high-net-worth individuals by instituting tight bank secrecy laws,[18] which by one estimate were responsible for bringing in $1.1 trillion in deposits from the Southeast Asian region and beyond and served to nurture Singapore’s banking and private wealth management industries.[19] Panama and Dubai are in a different league, as revealed by the Panama Papers, the Pandora Papers[20], and by a study conducted by the Carnegie Endowment. In both cases, the licit flows of capital were sharply augmented by “illicit streams borne from corruption and crime” (Page and Vittori 2020).[21] The contributors to this volume document the flow of “tainted” money into Dubai’s property market because of “weak regulations and lax enforcement;” the involvement of formal and informal financial institutions in money laundering; the import and refining of artisanally mined gold of uncertain provenance by Dubai based businesses;[22] and the facilitation of trade related over and under invoicing by Dubai’s FTZs.[23]

The Panama Papers[24] uncovered the magnitude of the money laundering network centered on Panama facilitated by laws protecting bank secrecy and concealing ownership.[25] They made public what was an open secret—that tax havens with clusters of private wealth management professionals were providing legal and other means of evading taxes and were also permitting the underworld to whitewash money derived from criminal activities.[26]

Low corporate taxes, free trade zones, banking secrecy laws, “lite” monitoring of the financial system, and lax enforcement of anti-money laundering contributed in part to the growth and apparent prosperity of the four economies. The capital, which flowed into the financial systems of these economies also promoted growth by financing construction activities on a massive scale of residential and commercial real estate and transport systems.[27] The multitude of high rises and luxury dwellings in Singapore, Dubai, and Panama, the housing boom in Ireland from 1996 through 2007,[28] and the proliferation of malls in both Singapore and Dubai were among the principal drivers of growth if not the drivers.[29]

However, the apparent prosperity as measured by GDP and GNI per capita is a trifle deceptive. MNCs that re-domiciled their headquarters to Dublin even though they conducted very few business activities in the country were able to report their undistributed profits (5 percent of gross national income (GNI) in 2012) in Ireland. This substantially inflated Irish GNI and exaggerated Irish GDP growth.[30] Patrick Honohan (2021) the former governor of Ireland’s Central Bank acknowledges that the large profits earned by MNCs mostly by their foreign parents have inflated Irish growth performance. Both GNI and GDP are distorted by the capital assets owned by MNCs operating in Ireland some of which are comprised of IP or patents.[31] Ireland’s corrected GNI in 2019 was 40 percent lower than GDP.[32] To varying degrees, the GDP data for the three other economies was also distorted by the activities of MNCs arguably flattering per capita GDP and GDP growth. Undoubtedly all four have achieved superior economic outcomes than other countries in their regions, but the published national accounts data can be somewhat misleading.

Whether capital inflows affected the longer-term growth prospects of these economies by prematurely increasing the share of highly paid financial and business services[33]—especially less productive non-tradable ones—and income inequality,[34] is less easy to determine. Panama appears to have deindustrialized with the share of manufacturing in GDP shrinking from 15 percent in 1990 to 6 percent in 2019. Capital inflows do not seem to have hastened the deindustrialization of Singapore, Ireland, and Dubai (where manufacturing was a sideshow) because the import of labor dampened wage increases, and industrial competitiveness was maintained through an increasing focus on technology and capital-intensive products.

Human capital

The economic performance and diversification into higher value activities of the four economies was bolstered by large scale immigration of workers both skilled and unskilled. Foreign workers in Ireland accounted for half or more of the workforce in education, professional and technical services, construction, and healthcare and figured prominently in manufacturing and wholesale/retail activities (Figure 5).

Figure 5. Immigrants at work in Ireland in top 10 industries, 2016.

Source: https://www.cso.ie/en/releasesandpublications/ep/p-cp11eoi/cp11eoi/lfnmfl/

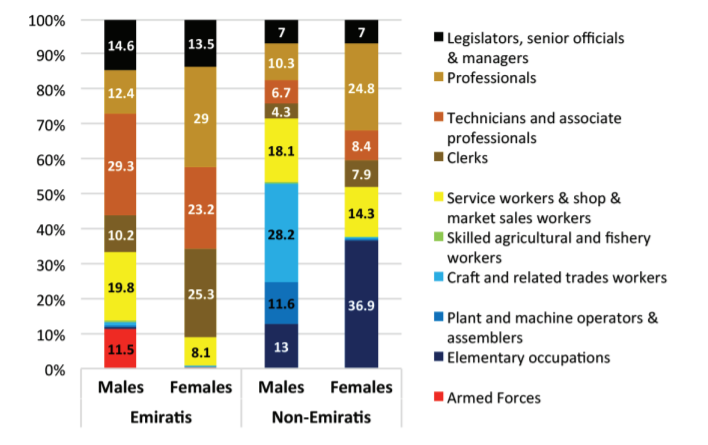

Singapore and Dubai have relied even more heavily on non-nationals for unskilled labor and to make up for shortages of managerial, professional, and technical personnel. In 2010 for example, foreign born workers constituted nearly 35 percent of Singapore’s workforce.[35] The share of non-nationals in Dubai’s workforce was much greater—96 percent in 2015—with private sector activities largely the preserve on non-Emiratis mainly from South Asia (Figure 6).[36] Panama also depends on expats who work for the MNCs that have set up shop in the country and to make good the shortage of human capital for jobs requiring knowledge intensive and complex skills. According to Hausmann et al (2017),[37] human capital was the binding constraint on Panama’s growth, hence it turned to immigrants. “[Because] banking, insurance, logistics, communications, information technology, and business and trade services are all dependent on sophisticated managerial and technical know-how [these positions have been filled by foreigners]. The share of foreign-born workers in managerial, professional, and chief executive jobs is 2.6 times higher than the average share of immigrants in the economy. The proportion is similar in the case of service workers, mid-level technicians, professionals and scientists.”

Figure 6. Dubai’s employed workforce in 2015: Emiratis (nationals) and non-Emiratis

Source: F. de Bel-Air (2018) https://gulfmigration.org/media/pubs/exno/GLMM_EN_2018_01.pdf

Knowledge capital

FDI and skilled migrant workers have enriched the four economies by serving also as a conduit for technology embodied in capital equipment and disembodied/tacit knowledge transferred by human capital from abroad. The importance of this cannot be underestimated. FDI alone would not have sufficed to generate the performance achieved by the four countries as is apparent from the experience of other small developing nations. It was by combining physical capital incorporating the latest technologies with advanced skills needed to operate this capital most productively that Singapore and Ireland built industrial capabilities of a high order. Similarly, all four economies managed to create high value tradable services—financial, legal, transport, logistical, and others—which complemented manufacturing in Singapore and Ireland and served as the principal sources of growth in Dubai and Panama. By tapping the international market for skills—and for semi-skilled to work on production lines as in Singapore—the ‘fabulous four’ accelerated technological catching up, alleviated domestic shortages of human capital, enhanced productivity, and raised their growth performance over that of countries in the regional neighborhood.

Concluding observations

Small economies must try harder. Unlike a China or a United States—or even countries such as Brazil and Indonesia—they do not benefit from the opportunities presented by a large, relatively sheltered domestic market. To pull ahead of the pack, they need to learn fast and attain a high level of competitiveness in a limited range of products and services, exploiting geographic and other advantages to the fullest. Where Dubai, Ireland, Panama, and Singapore excelled was in exploiting their location, offering a smorgasbord of incentives for foreign capital, creating adequately stable socio-political and business environments, and relying on expatriate workers to close labor and knowledge gaps. By successfully juggling all of these, the four economies demonstrated rare resilience and growth dynamism over much of the past three decades.

Arguably, the measures employed to attract financial resources made the crucial difference and account for the lead that Dubai, Ireland, Panama, and Singapore were able to sustain over other countries that were in the race to develop. This was the secret—or not so secret sauce. It is a sauce that is approaching its sell by date as anti-money laundering/combating the financing of terrorism (AML/CFT) standards are tightened,[38] adopted by an increasing number of jurisdictions and subject to oversight by the Financial Action Task Force.[39]

Tax havens are also likely to be squeezed by the proposal to set a global minimum tax rate of 15 percent and require MNCs to pay their fair share of taxes based on where corporations sell their products or services rather than on the location of their headquarters.[40] This plan, backed by the G20 inevitably is resisted by some of the smaller developing economies and tax havens, however, Ireland has now dropped its objection and has joined the 140 countries signing on to the deal.[41] In one form or the other it may very well survive and be implemented—although as Timothy Taylor remarks, “rethinking the roots of multinational taxation in a way that would be acceptable to politicians in most countries is a genuinely herculean task.”[42]

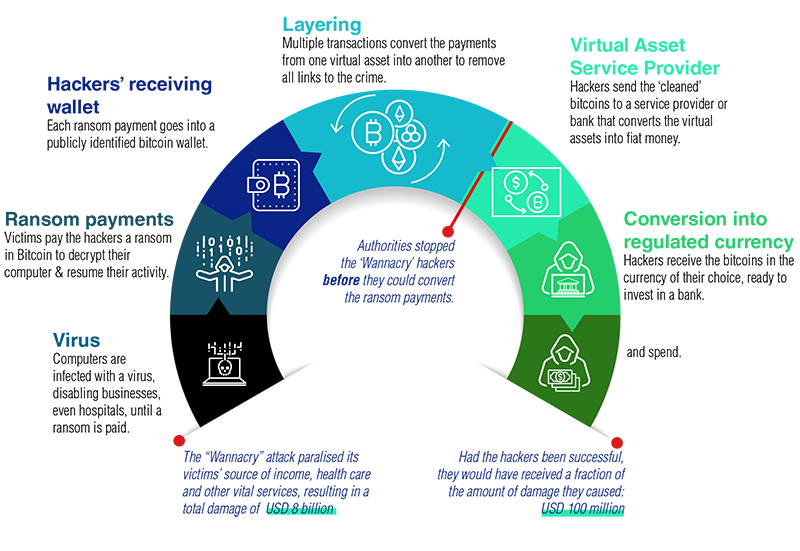

The scope for concealing transactions, conducting illegal activity anonymously, and accumulating untraceable assets could also be curtailed by withdrawing high denomination dollars, euros and yen currencies in circulation as has been recommended most recently by Ken Rogoff and Larry Summers.[43] For example, the $100 bill is the one with the widest circulation and 80 percent of these bills are held outside of the United States.[44] In 2017, the value of $100 bills in circulation amounted to 1,155 billion, or 79 percent of the total cash in circulation.[45] Another loophole that has emerged since 2010 and is receiving the attention of regulators results from the spread of cryptocurrencies such as Bitcoin, Ethereum, Litecoin, Bitcoin cash, Ripple, Dogecoin, Monero,[46] etc. They have created another (riskier) store of value and a means of payment for those wishing to conceal their transactions, wealth and illegally acquired assets (e.g. following ransomware attacks Figure 7). This risk is an increasing cause of concern because of the anonymity of cryptocurrencies, their global reach, and the widening acceptance in several emerging markets some with unstable currencies and limited access to financial products, among them being Nigeria, Ukraine, Russia, Venezuela, Argentina, and others.[47] Furthermore, the segmentation of infrastructure services used, and distribution of customer transaction records across several jurisdictions makes it difficult to monitor and regulate cryptocurrencies.[48] In response and to insulate the government issued digital currency from competition, China’s central bank made it illegal to engage in cryptocurrency related transactions on September 24th 2021.[49] A tightening of regulations by other countries could well follow.[50] However, Singapore is hoping to bolster its standing as a financial hub by accepting licenses from crypto exchanges such as Gemini and Coinbase, banking on the entrenching of cryptocurrencies in the global financial system and their widening attraction for high net worth individuals[51]. Whether the initiative will deliver the sought after gains financial and other remains to be seen.

Figure 7. Ransomware attacks and use of cryptocurrencies to evade detection

Source: https://www.fatf-gafi.org/publications/virtualassets/documents/virtual-assets.html?hf=10&b=0&s=desc(fatf_releasedate)

Looking ahead, it is unlikely that other small (or larger) late starting economies will be able to follow in the footsteps of a Dubai or a Panama and use large inflows of capital and migrant workers as a springboard for development to the same extent. The recipe adopted by the four economies worked but it has had its day.[52] The partially overlapping lessons from the Korean and Taiwanese experience are more likely to endure. Three deserve to be singled out:

-

The factors, which rendered these countries attractive for investors domestic and foreign and helped sustain high rates of investment and business formation, are as valid now as they were in the past.

-

An open, export-oriented strategy backed by domestic investment in physical, human, and digital capital—globalization permitting—is more likely to deliver adequate rates of growth. In fact, for small economies, there is no other.

-

FDI in productive activities and infrastructure, complemented as needed by human capital from abroad, can substantially improve growth prospects. However, countries may have to be more judicious in their use of incentives to attract capital, which underpins development.

[1] Each is an economic star in its own region—Central America, the Middle East, Western Europe, and Southeast Asia. Each was and is resource poor. Each started out with populations of less than 3 million in 1990 and all had populations of less than 6 million in 2019. https://data.worldbank.org/indicator/SP.POP.TOTL?locations=IE-PA-SG

[2] This depends on how the population is measured. GDP at current prices in 2019 converted into US dollars amounted to $119 billion. https://www.dsc.gov.ae/en-us/Themes/Pages/National-Accounts.aspx?Theme=24

[3] https://info.worldbank.org/governance/wgi/Home/Reports; World Bank (2019) Doing Business https://www.doingbusiness.org/en/rankings. Panama, however, has remained a laggard in this respect.

[4] Dubai’s oil resources are modest, production peaked in 1990 and has declined since. The petroleum sector accounts for only 5 percent of GDP—or 1 percent according to another source. https://www.businessinsider.com/dubai-rapid-development-skyscrapers-expansion-warning-2018-12

[5] Ireland benefitted from EU Structural and Investment Funds, which helped narrow infrastructure gaps. https://eufunds.ie/

[6] Panama has five seaports in the vicinity of the Panama Canal. Dubai’s port Jebel Ali is the largest in the region, the 9th busiest in the world and it shipped 15 million TEU containers in 2015. It is the largest man-made port in the world. https://www.ship-technology.com/projects/jebel-ali-port-dubai/. In 2016, there were 93 banks with a presence in Panama: two official, 47 with a general license (29 foreign), 27 with an international license and 17 with a representation license. Hausmann et al (2017) https://growthlab.cid.harvard.edu/files/growthlab/files/panama_growth_diagnostics_wp_325.pdf

[8] Korea and Taiwan relied mostly on domestic savings to finance investment, on home grown companies, and the domestic workforce. FDI contributed to industrialization in the early stages but to a lesser degree from the 1980s onwards, especially so in Korea.

[9] https://taxsummaries.pwc.com/singapore/corporate/tax-credits-and-incentives; https://www.cga.ct.gov/PS98/rpt%5Colr%5Chtm/98-R-0299.htm; https://www.idaireland.com/how-we-help; https://dublin.ie/invest/move-your-business/tax-incentives/; https://www2.deloitte.com/content/dam/Deloitte/ie/Documents/Tax/IE_T_invest_in_ireland_0517.pdf; https://www.visitdubai.com/en/business-in-dubai/newsroom/news-insights/tax-government-incentives-support-businesses; https://santandertrade.com/en/portal/establish-overseas/panama/investing; https://www.lowtax.net/information/panama/panama-foreign-investment-regime.html

[10] Panama operates 12 FTZs. https://www.healyconsultants.com/panama-company-registration/free-zones/; Dubai has over 30 FTZs. https://en.dubai-freezone.ae/articles-about-bussines-in-uae/what-is-ftz-in-the-uae-and-what-are-they-for.html; S. Beer R deMooij and L. Liu (2018) International corporate tax avoidance. https://www.econstor.eu/bitstream/10419/185382/1/cesifo1_wp7184.pdf; S Djankov (2021) Some of the ways MNCs reduce their tax bills. PIIE. https://www.piie.com/research/piie-charts/some-ways-multinational-companies-reduce-their-tax-bills; S. Djankov (2021) How do companies avoid paying international taxes. https://www.piie.com/blogs/realtime-economic-issues-watch/how-do-companies-avoid-paying-international-taxes

[11] On compressed development, see D. Hugh Whittaker et al (2008) Compressed Development. https://ipc.mit.edu/sites/default/files/2019-01/08-005.pdf

[12] R. Hausmann, L. Espinoza and M.A. Santos (2017) state that MNCs have gravitated towards Panama because it offers, “A favorable business environment, a stable economy, and significant improvements in personal security…enhanced by fiscal and migratory benefits.” Shifting Gears: A growth diagnostic for Panama. https://growthlab.cid.harvard.edu/files/growthlab/files/panama_growth_diagnostics_wp_325.pdf https://www.pardinilaw.com/EN/padela/articles/91/foreign-investment/panama-regional-headquarters-for-multinationals-companies/; https://morimor.com/the-republic-of-panama-a-hub-for-multinationals-2/

[13] https://www.hawksford.com/knowledge-hub/2018/mncs---why-you-should-set-up-a-subsidiary-in-singapore; https://www.edb.gov.sg/en/our-industries/headquarters.html

[14] B. Setser (2019) It is time to change how we view FDI. https://www.cfr.org/blog/it-time-change-how-we-view-foreign-direct-investment

[15] A study by the Institute of Taxation and Economic Policy (2017) revealed that close to three fourths of Fortune 500 companies maintained at least one subsidiary in a tax haven. All told, 366 companies had established 9,755 tax haven subsidiaries. Offshore Shell Games. https://itep.org/offshoreshellgames2017/

[16] https://www.internationalinvestment.net/news/4004737/tax-avoidance-drives-nearly-global-fdi-imf

[17] Piercing the Veil. https://www.imf.org/external/pubs/ft/fandd/2018/06/inside-the-world-of-global-tax-havens-and-offshore-banking/damgaard.htm

[18] This has its roots in the section 47(1) of the Singapore Banking Act, which was passed in 1970. S. Yu (2019) Still keeping secrets? https://www.researchgate.net/publication/332983047_Still_Keeping_Secrets_Bank_Secrecy_Money_Laundering_and_Anti-Money_Laundering_in_Switzerland_and_Singapore

[19] A Brookings study based on data from an Isle of Man bank found that deposits held by shell companies and trusts were actually owned by high income elites with a significant share traceable to “politically exposed” persons. The study also concluded that a substantial share of the deposits was not reflected in the accounts published by the BIS. M. Collin (2021) What lies beneath. https://www.brookings.edu/research/what-lies-beneath-evidence-from-leaked-account-data-on-how-elites-use-offshore-banking/; This finding was corroborated by the information uncovered by the Pandora Papers. Washington Post (2021, October 3rd) Pandora Papers. https://www.washingtonpost.com/business/2021/10/03/takeaways-pandora-papers/

[20] Guardian (2021) Pandora Papers. October 3rd. https://www.theguardian.com/news/2021/oct/03/pandora-papers-biggest-ever-leak-of-offshore-data-exposes-financial-secrets-of-rich-and-powerful; https://www.icij.org/investigations/pandora-papers/;

[21] M.T. Page and J. Vittori (2020) Dubai’s role. https://carnegieendowment.org/2020/07/07/dubai-s-role-in-facilitating-corruption-and-global-illicit-financial-flows-pub-82180; K. Greenaway (2020) observes that “Dubai’s economy relies heavily on promoting itself as a diamond and precious metals commodities trading and financial hub… As a result, Dubai has had little incentive to address the problems of domestic or foreign corruption and money laundering… The FATF’s 2020 evaluation report noted that …between 2013 and 2018, it prosecuted just fifty individuals for money laundering and convicted thirty-three. Of those prosecutions, only seventeen took place in Dubai. The report specifically noted “the low number of [money laundering] prosecutions in Dubai is particularly concerning, considering its recognized risk profile.” [Moreover]there was a “noticeable absence of consistent investigations and prosecutions of [money laundering] related to other high risk predicate crimes (such as drug trafficking), professional third-party [money laundering], and those involving higher risk sectors (such as money value transfer services or dealers in precious metals or stones).” https://carnegieendowment.org/2020/07/07/how-emirati-law-enforcement-allows-kleptocrats-and-organized-crime-to-thrive-pub-82187

[22] https://carnegieendowment.org/2020/07/07/dubai-s-problematic-gold-trade-pub-82184; https://www.reuters.com/article/emirates-dubai-gold/gold-industry-shifts-east-as-dubai-plans-huge-refinery-spot-contract-idINKBN0DL0LJ20140505

[23] David Brooks (2013) provides a snapshot of Dubai’s explosive development in, A History of Future Cities. https://nextcity.org/daily/entry/how-dubai-became-dubai

[24] https://www.theguardian.com/news/2016/apr/03/what-you-need-to-know-about-the-panama-papers; N. Vall (2018) Cracking Shells. https://scholarship.law.tamu.edu/lawreview/vol5/iss1/7/; F. Obermaier and B. Obermaier (2016). The Panama Papers. Oneworld Pub.

[26] https://www.independent.co.uk/news/world/americas/panama-papers-why-money-laundering-so-easy-panama-a6968666.html; https://www.theguardian.com/commentisfree/2017/nov/18/paradise-papers-tax-havens-mafia-roberto-saviano

[27] In addition to residential and commercial construction, Panama embarked upon “Large public infrastructure investments such as the expansion of the Canal, the development of the Metro in Panama City, Tocumen Airport, road expansions and upgrades in the Panama-Colón axis…all [of which] boosted an extraordinary construction boom.” R. Hausmann, M.A. Santos and J. Obach (2017) Appraising the economic potential of Panama. https://growthlab.cid.harvard.edu/files/growthlab/files/panama_policy_wp_334.pdf

[28] On the credit financed construction boom in Ireland see M. Norris and D. Coates. How Housing Killed the Celtic Tiger. https://www.ucd.ie/t4cms/WP15%20How%20Housing%20Killed%20the%20Celtic%20Tiger.pdf; The housing boom came to a sharp close during 2008-2010, however as the economic recovery gathered momentum, a second boom gained traction in 2017. https://www.ashurst.com/en/news-and-insights/insights/construction-in-ireland---a-new-boom/

[29] Many of the luxury apartments in Panama, Dubai, and Singapore are owned by absentee owners as investments or second homes and sit vacant for part of the year or all year round.

[30] B. Setser (2018) Tax avoidance and the Irish BOP. https://www.cfr.org/blog/tax-avoidance-and-irish-balance-payments

[31] P. Honohan (2021) Is Ireland the most prosperous country in Europe? https://www.centralbank.ie/news/article/press-release-economic-letter-is-ireland-really-the-most-prosperous-country-in-europe-04-january-2021

[32] In 2020, household consumption as a percent of GDP in Ireland was a low 26 percent. The world average was 64 percent. This also highlights the apparent distortion of the GDP numbers. https://www.theglobaleconomy.com/Ireland/household_consumption/

[33] https://www.economist.com/free-exchange/2009/08/27/what-good-is-finance; L. Zingales (2015). Does Finance benefit society. NBER. https://www.nber.org/system/files/working_papers/w20894/w20894.pdf

[34] M. Brei et al (2019) How finance affects income inequality. VoxEu https://voxeu.org/article/how-finance-affects-income-inequality; M. Bittencourt et al (2019) Does financial development affect income inequality. https://privpapers.ssrn.com/sol3/papers.cfm?abstract_id=3424190

[35] https://www.migrationpolicy.org/article/rapid-growth-singapores-immigrant-population-brings-policy-challenges; S.Y. Chia (2011) cites the six reasons for Singapore’s dependence on foreign workers. “First is to grow the Singapore population beyond the size determined by a declining total fertility rate. Second, is to mitigate rapid population ageing and the consequent loss of societal dynamism and rising health care costs. Third is to increase labor supply and skills, so as not to constrain economic growth and economic restructuring. Fourth is to act as buffer for cyclical demands for labor. Fifth is to contain rising wage cost of businesses and maintain international competitiveness. Finally, there is a need to fill vacancies in lowly paid and “dirty, demeaning, and dangerous” (3D) jobs shunned by better-educated and increasingly affluent Singaporeans.” The latter three reasons to varying degrees are why Dubai, Ireland and Panama have recruited workers from overseas. Foreign labor in Singapore. https://dirp4.pids.gov.ph/webportal/CDN/PUBLICATIONS/pidspjd11-singapore.pdf

[36] F. de Bel-Air (2018) Demography, Migration, and the Labor Market in the UAE. https://gulfmigration.org/media/pubs/exno/GLMM_EN_2018_01.pdf

[37] https://growthlab.cid.harvard.edu/files/growthlab/files/panama_policy_wp_334.pdf; There were approximately 140,000 foreign nationals employed in Panama in 2010 from Colombia, other neighboring countries, and China.

[38] IMF (2019) Article 4 report on UAE. https://www.imf.org/en/Publications/CR/Issues/2019/02/01/United-Arab-Emirates-2018-Article-IV-Consultation-Press-Release-Staff-Report-and-Statement-46571

[39] https://www.fatf-gafi.org/publications/high-risk-and-other-monitored-jurisdictions/documents/increased-monitoring-june-2021.html

[40] N. Nersesyan (2021) The current international tax architecture: A short primer. IMF. https://www.elibrary.imf.org/view/books/071/28329-9781513511771-en/ch003.xml; E. Dabla-Norris et al 2021) How to Tax in Asia’s Digital Age. https://outlook.live.com/mail/0/inbox/id/AQMkADAwATZiZmYAZC1hODAyLTA3ZWYtMDACLTAwCgBGAAADFcVmjJENv0mMjrzecnvzMwcAkAEdhyrwrUCDnH%2FjZ2V23wAAAgEMAAAAkAEdhyrwrUCDnH%2FjZ2V23wAFcPx%2FGwAAAA%3D%3D; https://www.cnbc.com/2021/07/10/g-20-financial-leaders-agree-to-move-forward-on-international-tax-crackdown.html; https://www.g20.org/wp-content/uploads/2021/07/Communique-Third-G20-FMCBG-meeting-9-10-July-2021.pdf; https://www.cnbc.com/2021/07/16/oecd-tax-reform-g-20s-crackdown-may-create-a-new-kind-of-tax-haven.html

[41] Financial Times (2021) Ireland poised to sign up for global tax deal. September 24th. https://www.ft.com/content/866dee09-4a09-4cad-830c-9eb39618ce8f

[43] K. Rogoff (2014) Costs and benefits of phasing out paper money. And The Curse of Cash. https://scholar.harvard.edu/files/rogoff/files/c13431.pdf; L. Summers (2016) In defense of killing the $100 bill. http://larrysummers.com/2016/02/25/liberty-and-the-100/

[44] https://www.washingtonpost.com/business/2019/03/04/there-are-more-bills-circulation-than-bills-it-makes-no-cents/; https://www.cnbc.com/2019/04/04/100-bills-in-circulation-soar-to-a-record-hinting-at-rise-in-global-criminal-activity.html

[46] This is a private untraceable currency, which ensures complete privacy with the help of ring signatures. However, its capitalization as of September 2021 was $245 million. Others include Grin, Zcash and Dash.

“While bitcoin leaves a visible trail of transactions on its underlying blockchain, the niche “privacy coin” monero was designed to obscure the sender and receiver, as well as the amount exchanged. As a result, it has become an increasingly sought-after tool for criminals such as ransomware gangs, posing new problems for law enforcement.” https://www.ft.com/content/13fb66ed-b4e2-4f5f-926a-7d34dc40d8b6

[47] Surprisingly, according to the crypto adoption index, the highest level of crypto adoption is in Vietnam followed by India and Pakistan. Cryptocurrencies using blockchain are also gaining in popularity as a way of remitting funds across borders at lower cost relative to traditional means. Financial Times (2021) Emerging markets take a punt on crypto. September 4th. https://www.ft.com/content/1ea829ed-5dde-4f6e-be11-99392bdc0788; R. Sharma (2021) Why Crypto is coming out of the shadows. https://www.morganstanley.com/im/en-us/financial-advisor/insights/articles/why-crypto-is-coming-out-of-the-shadows.html

[48] FATF/OECD (2014) https://www.fatf-gafi.org/media/fatf/documents/reports/Virtual-currency-key-definitions-and-potential-aml-cft-risks.pdf

[49] WSJ (2021) Beijing declares crypto dealings illegal. September 25th. https://www.wsj.com/articles/china-declares-bitcoin-and-other-cryptocurrency-transactions-illegal-11632479288; R. Auer (2018) Regulating cryptocurrencies. BIS. https://www.bis.org/publ/qtrpdf/r_qt1809f.htm; W. Buiter (2021) Schrodinger’s Bitcoin. https://www.project-syndicate.org/commentary/bitcoin-bubble-price-volatility-investment-risk-by-willem-h-buiter-2021-02?barrier=accesspaylog; In its Annual Report, BIS (2021) was critical of cryptocurrencies. “Cryptocurrencies are speculative assets rather than money, and in many cases are used to facilitate money laundering, ransomware attacks and other financial crimes. Bitcoin in particular has few redeeming public interest attributes when also considering its wasteful energy footprint. Stablecoins attempt to import credibility by being backed by real currencies. As such, these are only as good as the governance behind the promise of the backing. They also have the potential to fragment the liquidity of the monetary system and detract from the role of money as a coordination device.” https://www.bis.org/publ/arpdf/ar2021e3.pdf; Nevertheless, stablecoins are acquiring a following. By September 2021, the value of coins issued had reached $130 billion. Financial Times (2021) Policymakers’ fears reflected in BIS paper. October 1st. https://www.ft.com/content/b102160a-f326-4c17-8005-7d8b57bc7442

[50] A. Siripurapu (2021) Cryptocurrencies, digital dollars, and the future of money. https://www.cfr.org/backgrounder/cryptocurrencies-digital-dollars-and-future-money

[51] Financial Times (2021) Singapore faces fight for Asia crypto crown. October 1st. https://www.ft.com/content/1f948b38-2061-416d-951d-69415b879c17

[52] Although El Salvador made Bitcoin legal tender in September 2021 alongside the dollar, this action might facilitate remittances from Salvadoreans working overseas, but it will not make San Salvador into a financial hub rivaling Panama City. https://www.reuters.com/business/finance/el-salvador-leads-world-into-cryptocurrency-bitcoin-legal-tender-2021-09-07/; J. Frankel (2021) El Salvador’s Bitcoin folly. https://www.project-syndicate.org/commentary/el-salvador-dangers-of-adopting-bitcoin-as-legal-tender-by-jeffrey-frankel-2021-09

CITATION

Yusuf, Shahid. 2021. How Four Small Successful Economies Improved Upon the Standard Growth Recipe. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}