On August 23rd, 2021, the IMF allocated $650 billion of Special Drawing Rights (SDRs) to its member countries, in proportion to their quotas. Much has been written to laud the allocation as the only global financing effort to stem the impact of the COVID-19 pandemic.

Yet many decried that the distribution of the new allocation was not aimed at those countries that needed it the most. Something had to be done, quickly, to get even more SDRs to vulnerable countries and to their citizens.

In the last six months, think tanks thought. Working groups wonked and zoomed. Advocates advocated. Bureaucracies toiled away. But what has landed in vulnerable countries’ accounts and what have their people received? Nothing more than the fruits of their initial allocation. Not a single SDR has yet been recycled from high-income countries.

No need to despair yet. The world can still walk the talk. Three things need to be done, between now and the allocation’s first birthday on August 23:

-

Firm-up country contributions in 2022 to the $100 billion G20 commitment to SDR recycling and pledge to look for more in 2023.

-

Establish a useable Resilience and Sustainability Trust (RST) at the IMF by the April meetings and get money out the door by the end of the year.

-

Find a way to recycle SDRs to multilateral development banks (MDBs).

If political leaders and the heads of the IMF and MDBs make these demands, say at the Spring Meetings of the IMF and World Bank, any remaining technical problems will be solved shortly. And by the end of 2022, recycled SDRs will be available to help vulnerable low and middle-income countries recover from the pandemic and begin the needed transition to a resilient, sustainable, and more equitable global economic order.

Here's what’s been done so far with the new SDR allocation:

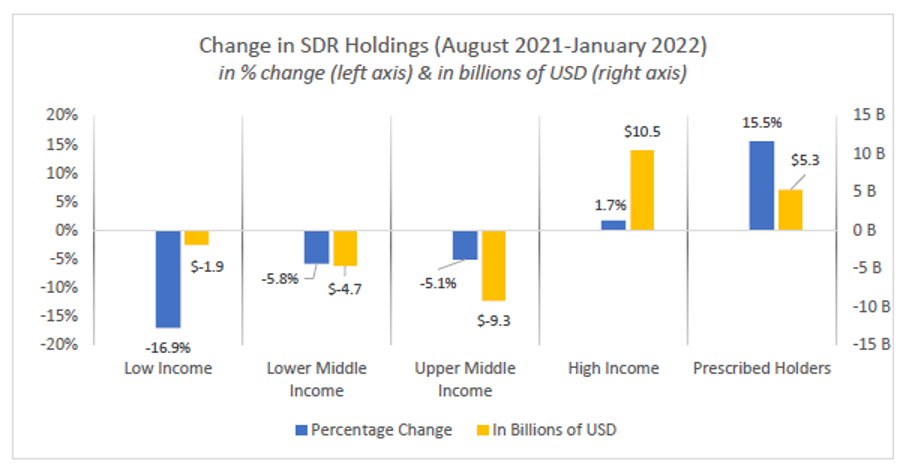

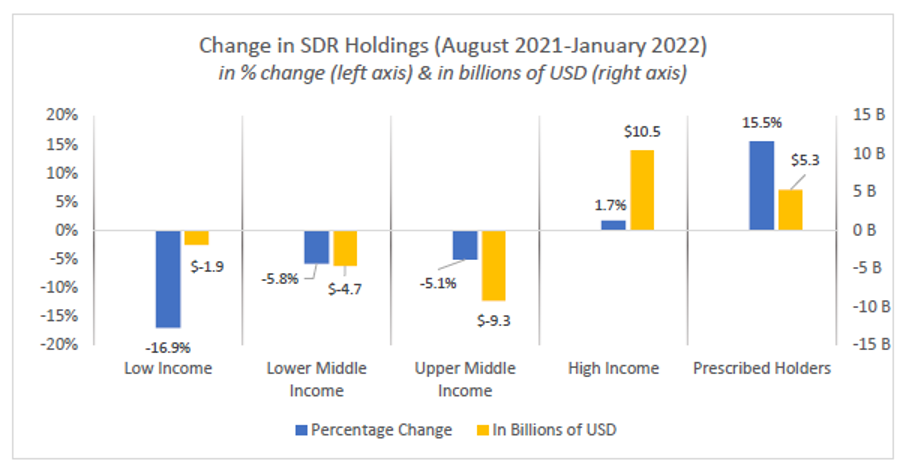

Raw numbers indicate that SDRs are just beginning to be used. From publicly available IMF data we can see that low-income countries have decreased their SDR holdings since August 31 by SDR1.4 billion (worth about $1.9 billion) or about 17 percent of their end-August holdings (see chart). Lower-middle-income countries decreased holdings by SDR3.3 billion (worth about $4.7 billion) or 6 percent, while upper-middle income countries used 5 percent of their end-August SDR holdings or SDR6.6 billion (worth about $9.3 billion), although more than half of that appears to have been Argentina paying debt service to the IMF. And recall that globally SDRs are never used up, they are just exchanged between countries and institutions for foreign exchange. So as low and middle-income country holdings fell, high-income countries holdings of SDR went up by 2 percent since August and institutional holdings increased by 16 percent, mostly the IMF’s own holdings.

But slow sales of SDRs don’t mean they were not useful from the outset. The IMF numbers cannot tell us exactly what was done with the SDRs that were exchanged for hard currency. And even if most SDRs were not exchanged for hard currency does not mean they were not useful. They may have given countries room to use other foreign reserves for imports. To understand the full story requires a detailed analysis of central bank balance sheets and government accounts that just aren’t available yet and some idea of what might happened had there never been a new SDR allocation.

Informal indications are that vulnerable countries have used their SDRs in three ways: to reinforce reserve holdings, to increase the spending power of their governments, and to pay back debt. This is based on press reports and events like the one held by CGD earlier this month where country officials report that SDRs were serving a multiplicity of purposes. In fact, in resource-constrained countries it may make good sense not to exhaust the new SDR allocation in short order, but to use it to gradually relaunch an economic recovery from the COVID-19 induced economic slowdown. And in some cases, the SDRs may be used to replenish reserves that were depleted during the depths of the COVID-induced crisis.

Here's what needs to be done by rich countries:

The G20 has heeded the call to recycle advanced countries’ SDRs by setting a global ambition of $100 billion worth of SDRs to vulnerable countries. There are firm commitments so far of $36 billion and strong indications of another $10-20 billion from advanced countries. The G20 reported commitments of $60 billion from its members. But this leaves a gap of at least $40 billion yet to be pledged.

Yet not a single SDR from the new allocation has yet been recycled. Donors appear to be awaiting a clearer picture of recycling options and needs. The one established vehicle is the IMF’s Poverty Reduction and Growth Facility (PRGT), which provides financial support to low-income countries. The IMF has indicated it needs an extra $30 billion in funding. Even so, new pledges to the PRGT will not lead to actual on-lending of SDRs to low-income countries until IMF-supported programs are agreed.

The IMF is on the road to establishing a new recycling alternative, the Resiliency and Sustainability Trust (RST). This trust will aim at a larger group of countries, including vulnerable middle-income countries, and support their transition to a more resilient, sustainable and equitable global economy. Estimates are that initial funding of up to $50 billion will be needed to get the trust up and running. Already the RST’s design is coming under criticism for being too constraining, raising doubts as to whether countries will ever borrow from the trust. Numerous civil society organizations offered RST design suggestions to increase the chances it would indeed be used, suggestions the IMF should consider carefully. There is also impatience at the slow pace at which the trust is being established, with the first disbursements unlikely before the end of 2022. Both recycling options through the IMF put high-income countries’ excess SDRs into an intermediate vehicle that then will on-lend to vulnerable countries, but at a rhythm determined by the IMF. The IMF will need to make loans quickly if the SDRs are to help countries face the current crises and prepare for future ones soon. To do this, vulnerable countries should seize the chance to develop their policy programs and be ready to submit early requests for financial support from the IMF trusts.

But advanced countries are looking for more recycling options. The IMF appears to be able to absorb at most $80 billion of SDRS in its two trusts, which leaves at least $20 billion without a possible placement. And we could hope for recycling beyond the G20 goal if there were a vehicle to do so. Many options have been put on the table, such as a fund to finance climate transition investment and a fund to increase liquidity for credit-constrained African countries.

The most promising non-IMF option appears to be recycling SDRs to multilateral development banks (MDBs). Many MDBs already have the right to hold SDRs in their accounts and they have strong international governance that would ensure proper stewardship of the SDRs. If SDRs were used to bolster MDB capital, they could leverage the SDRs to create much more borrowing space for vulnerable countries facing the climate transition. At a recent CGD event, the African Development Bank put forward a concrete proposal to use recycled SDRs in this fashion.

But there is a sticking point to use of SDRs at MDBs—maintaining the reserve asset characteristic of the SDR. This key element appears in the G20 communique committing to recycling of SDRs. It requires that SDRs that are recycled remain largely risk-free and liquid enough that the lending country’s central bank can still count them as a reserve asset on its balance sheet. This stricture has led, for example, the European Central Bank to pronounce that SDRs cannot be recycled to MDBs. However, a recent white paper from Lazard, a financial advisory and asset management firm, argues that the reserve asset characteristic and SDR recycling to MDBs can be designed to make the loans less risky and more liquid than many other assets already on central bank balance sheets.

So how do we get to a happy 1st birthday—can we walk the talk?

It’s time for the talking to stop. Most of what needs to happen requires political leadership and some strong and coordinated messages from the heads of the IMF, World Bank, and other MDBs, otherwise we will not cut through the technical hurdles.

There will have to be a bit of compromise and some rallying around a few actions. Many shareholders at the IMF had taken doctrinaire positions, limiting the staff’s options for the RST. Central bankers and others have been rigid in their interpretation of how SDRs can be used and still considered a reserve asset. And many global leaders have united behind the G20 in their calls for recycling, but then have not ponied up their share of SDRs for recycling, citing legal concerns or perhaps fearing political backlash. And the heads of the international financial institutions (the IMF and the MDBs) have hardly been united in the messages they are sending out.

The objective is clear—begin to get the recycled SDRs in the coffers of vulnerable countries before as fast as possible, certainly at least some by the end of 2022. After all, we are now well into the third year of the pandemic-induced economic crisis. To reiterate, three steps can make it happen:

-

Firm-up country contributions in 2022 to the $100 billion G20 commitment to SDR recycling and pledge to look for more in 2023.

-

Establish a useable Resilience and Sustainability Trust at the IMF by the April meetings and get money out the door by the end of the year.

-

Find a way to recycle SDRs to multilateral development banks.

Let’s get these done well before the new SDR allocation turns one on August 23, 2022.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

{kind=link}