At the annual meetings of the World Bank and International Monetary Fund last week, concerns about rising debt risks in developing economies were front and center. And for good reason: The number of low-income countries in debt distress or at high risk of distress has increased dramatically, from just six countries three years ago to 22 today.

For many, the Heavily Indebted Poor Country Initiative (HIPC) of the 1990s serves as a useful reference point as we anticipate a new round of debt crises. Invoking HIPC may be a way to bolster confidence that there will be appropriate action should crises arise. After all, the earlier debt relief initiative is broadly viewed as a success for the indebted countries and a credit to the lenders who tapped their aid budgets to write off much of these debts. While there have been debates about the degree to which HIPC debt forgiveness boosted growth and reduced poverty in these countries, or how much of the success should be attributed to HIPC’s policy conditionality, it is now conventional wisdom that HIPC was the right and necessary thing to do.

But HIPC as a reference point for the 2020s is misguided. While, sadly, many of yesterday’s HIPC countries are also today’s high debt risk countries, the creditor community today looks much different from the HIPC creditor community.

HIPC depended on the collective political will of traditional donor countries

Consider the World Bank’s estimate of who bore the costs of writing down HIPC debt. Primarily this was a multilateral development bank and IMF debt relief initiative, with the IMF, World Bank, Inter-American Development Bank, African Development Bank, and other smaller multilateral creditors accounting for 44 percent of the cost. Next, the Paris Club, which included the major official bilateral creditors at the time, accounted for 36 percent of the costs. And finally, other bilateral creditors (13 percent) and commercial creditors (6 percent) accounted for the rest. For the MDBs, the true cost of writing down their loans was ultimately shouldered by their donors, who agreed to compensate the institutions for the lost revenues. These donors happened to be the same Paris Club creditors who were also paying for more than one-third of the initiative’s costs by writing down their bilateral loans to HIPC countries.

It is reasonable to think that a deal was struck on HIPC largely because one of the largest Paris Club creditors, the United States, was also the largest shareholder at the World Bank and IMF. And the US government at the time decided that debt relief was the right thing to do.

From this perspective, it matters as much who is not a creditor to today’s high-risk countries as it does who is. Because of HIPC itself, in which donor governments had to allocate budgetary resources to large-scale debt write downs, there’s been an aversion among these countries to do a lot of lending to low income governments in the years since HIPC. As a result, risky borrowers now face a different creditor community.

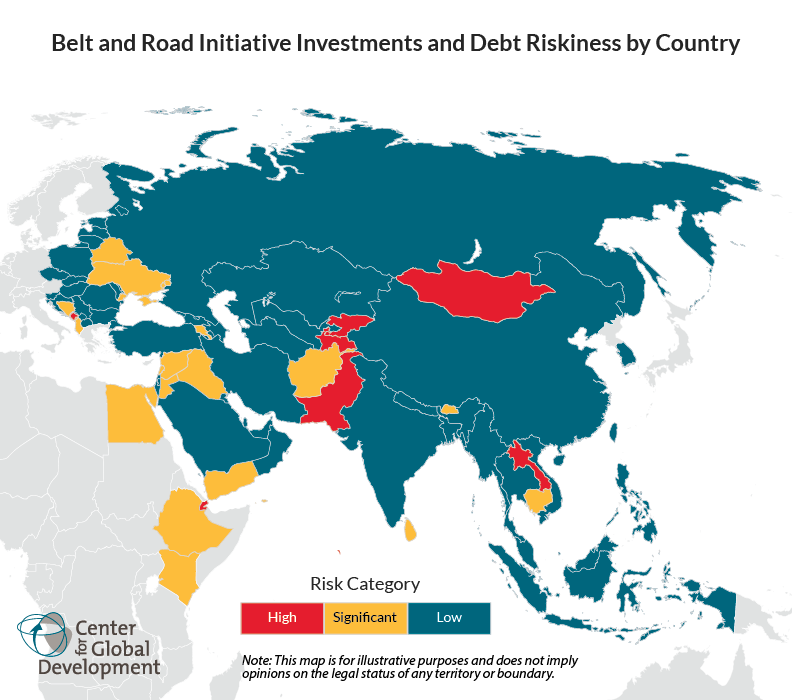

But high-risk countries are borrowing from different lenders today—mainly China

Just as the United States played the leading role in HIPC, both as a leading creditor itself and the largest shareholder in the World Bank and IMF, China today clearly stakes that claim. While it is arguably a less powerful shareholder in the multilateral institutions, it is a vastly bigger creditor relative to other bilateral creditors than the United States was at the time of HIPC. For example, The multilateral institutions remain among the largest official creditors to low income country governments, but as HIPC’s history indicates, the behavior of these institutions depends a lot on the views of their shareholders.

So, what does China’s current outsized creditor role mean for debt crisis response should the need arise, particularly across an array of low-income countries? Certainly, a US-led HIPC is not in the cards. But what about China? Is it reasonable to consider the features of a HIPC with Chinese characteristics?

First, we should acknowledge that the Chinese government is by no means averse to debt restructuring and to some debt forgiveness. One recent estimate suggests there have been at least 140 restructurings or write-offs since 2000. At the same time, there is little evidence of coordination with other creditors. China is notably not a member of the Paris Club. As a starting point then, there is reason to be skeptical that the Chinese government will take a sudden interest in driving a multilateral agreement on debt relief.

Restructuring and forgiveness are very different. For official creditors, restructurings do not typically entail a commitment of current budgetary resources, whereas write-downs do. And China seems far more inclined toward the former than the latter. So even if China did seek to lead on an agreement with other official creditors, the push might favor stretching out loan maturities over more painful debt reductions.

Conditionality was a core and controversial feature of HIPC. Indeed, policy conditions meant that a small number of HIPC eligible countries continued to wait for debt relief decades after the initiative’s launch. In fact, Somalia’s HIPC debt relief was announced at last week’s annual meetings! In contrast, it doesn’t appear that HIPC style conditionality is a feature of Chinese debt relief. While there is much speculation about quid pro quos attached to these deals, observers typically identify issues far removed from economic policy as the “quo”—things like recognition of Taiwan.

Finally, as much as HIPC was a complicated endeavor, HIPC with Chinese characteristics would have added complexity due to the ancillary features of Chinese lending. China’s official lenders like China Development Bank and China Exim appear to make frequent use of collateral or otherwise pursue financing arrangements that go well beyond the conservative approaches of traditional official lenders—such as funding through state-owned or nominally private enterprises, where government guarantees and liabilities are unclear. These various features greatly complicate the task of identify the true scale of financial burden, let alone finding a path toward resolving debt problems.

With these various features in mind, it may be that HIPC with Chinese characteristics will in the end mean no multilateral agreement on debt relief at all. But we should also recognize that HIPC itself did not feel inevitable until it became so and particularly as views solidified around the unsustainability of HIPC countries’ debt burdens. Chinese officials may ultimately need to learn the dictum of the American economist Herb Stein: “If something cannot go on forever, it will stop.” The question will be what the stopping point looks like in Beijing.