Recommended

The World Bank's Global Jobs Challenge report gives a clear picture of the scale of the looming jobs problem. But this diagnosis—one that sees the challenge as creating jobs— does not match the proposed solution, which focuses on raising productivity. That mismatch is where the report runs into trouble.

Over the next decade, around 1.2 billion young people in low- and middle-income countries will reach working age—the largest such cohort ever. According to illustrative figures in a new World Bank report, just over 400 million of them would hold a job by 2035, while some 300 million would be neither working nor in school or training (the remaining 500 million or so would still be in education or training—many only recently of working age). The report is careful to call this what it is: an extrapolation that bends with its assumptions. Take it loosely, then; the order of magnitude is the point, and it is staggering.

Although the report is framed as a jobs study, its logic is really about growth—a tension it never fully resolves. The World Bank's president has planted a flag on jobs as the development outcome, the focus of the World Bank Group’s attention. Many economists probably think this is the wrong flag: that the right objective is productive growth, and that jobs are what you get when growth goes well, not a target you aim at directly. The report makes peace between those factions. It speaks the language of jobs and runs on the engine of growth: deliver infrastructure, improve the business environment, mobilize private capital, and the jobs will follow. In the most favorable interpretation, this manufactured peace is a Trojan horse for growth, a sound macroeconomic instinct smuggled in under the World Bank president’s favorite noun, jobs.

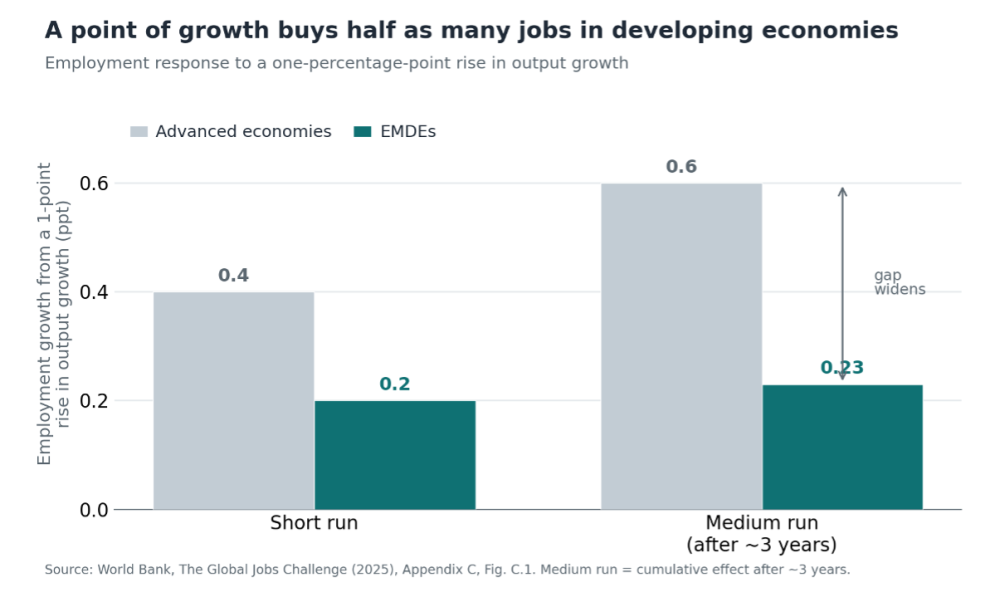

I am not opposed to this type of smuggling. If productive growth reliably creates jobs, then the horse is harmless. But this depends on context, and the report’s own appendix says as much. In emerging markets and developing economies (EMDEs), a one-point rise in output growth generates about two-tenths of a point of employment growth—half the advanced-economy rate—and the gap widens, not narrows, over the medium term. In other words, a flagship report that rests its case on growth delivering jobs also quantifies, in its own appendix, how few jobs growth actually delivers in EMDEs.

Two economists, two worlds

Robert Solow’s insights on growth came from looking at richer countries, where almost everyone who seeks employment finds it. He concluded that growth means making each worker more productive. Capital and knowledge are scarce; workers are valuable. Arthur Lewis, on the other hand, looked at poor countries and saw the opposite: a vast number of people working on farms, in street stalls, and in precarious jobs that produced next to nothing, and a virtually unlimited supply of labor waiting for a real position to open. In Lewis's world, the scarce thing is the job, and the abundant thing is the worker. Solow asks how we make more stuff with fewer inputs. Lewis asks where all these people are going to work.

The World Bank’s jobs report describes a Lewis world but answers a Solow question. It attempts to bridge the two worlds, and human capital is the span it builds: educating and training surplus workers in the hope of transforming Lewis’s labor surplus into a Solow-style engine of productivity. The intuition is sound. However, education alters what a worker could produce, but it does not determine whether the capital needed to employ them actually exists. Where capital is scarce and free to leave, a better-trained workforce raises the value of each job created without creating more jobs. This bridge spans the wrong river.

A growth accounting identity deserves more attention than the report gives it. While the growth rate holds fixed, it splits between two uses: a point that shows up as higher output per worker is a point that does not show up as new jobs. Investment can enlarge the rate itself—a faster-growing economy can raise productivity and hire at once—so the bind is a feature of stagnant growth, not a law of it.

But in EMDEs, the growth rate is not rising on its own, and whether it does depends on whether the surplus generated by productivity is reinvested at home or sent abroad. Without that reinvestment, the split between productivity and jobs becomes unavoidable, and the appendix elasticities above show how nearly fixed the budget already is.

Where job-intensity is high, growth absorbs labor but productivity stagnates, producing the survivalist pattern of informal work piling up. Where it is negative, output rises while employment falls, resulting in jobless growth, which is increasingly the norm. Korea industrialized by absorbing labor; India has grown rapidly while its employment-to-population ratio has declined. The growth rates may look similar, but the employment outcomes are not. The World Bank’s report treats that difference as if it would sort itself out.

Counting the wrong thing

The report highlights five priority sectors, chosen in part for their potential to create jobs. But this misses the real problem. Labor intensity is measured in jobs per unit of output. But in developing countries, capital is the scarce factor, so the quantity to maximize is jobs per unit of capital, and the two ratios need not match; the report does not check whether they do. A simple job count also ignores where the inputs came from. The scarce capital, skilled workers, and foreign exchange a favored sector absorbs were already employed elsewhere. The real gain is the jobs it adds minus the jobs lost at the source. And the greatest gains in employment often come not from promoting a labor-intensive sector, but from easing the constraints that limit absorption in every sector downstream of it. The better question is not which sector to favor, but what blocks employment in the first place.

The obvious reply: if planners cannot pick sectors, they should step aside—eliminate frictions and let labor and capital move to their most productive uses on their own. This is both a tempting escape and a trap. On the one hand, it simply restates the report’s own business-environment pillar, so it cannot be the cure for its shortcomings. On the other hand, it points in the wrong direction. The unaided market directs capital to its highest return, which, in a capital-scarce economy, means the most productive firms. And by the identity above, maximizing productivity is what holds down the job intensity of growth. If the market is left to its own devices in a Lewis world, its natural objective is jobless growth. Eliminating frictions is necessary, but not sufficient, because what you want is not what a cleared market produces.

Buy the jobs, don’t pick the firms

Neither extreme works. Grouping workers into government-chosen sectors is a planning approach that the report's critics rightly distrust. The report's own response is to clear the way and trust the market, but it optimizes the wrong thing. The solution lies between two sides accustomed to confrontation: if the market does not set the desired price, then you have to set it yourself. The government chooses neither the sector nor the firm.

So, pay for the outcome you want. Do not choose the sector or the firm; choose the target and let firms compete for the subsidy. This is a reverse auction:

- a fixed pot of subsidy is tied to one clear target;

- it goes to whoever promises the most verified jobs for the least support;

- and it is paid only once the jobs show up.

No official picks winners: the bids do—which keeps both the planner’s thumb and the well-connected firm’s grab off the scale. Facilitation and allocation stop being opposites. Frictions get cleared and a price gets set for an outcome that clearing frictions alone could never deliver. The report does the first half well. It clears obstacles but then relies on the market in a setting where the market is likely to produce too few jobs.

The World Bank's Global Jobs Challenge is the best single account of how large the jobs problem is. It hits the mark on pointing out that infrastructure is the one pillar that lowers the cost of putting people to work. Yet, it describes a world characterized by an abundance of labor and a scarcity of jobs, while prescribing solutions as if the reality were the reverse. That leaves an important question unanswered: Once the jobs are created, will the capital that created them stay long enough to employ the next generation?

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: Enrico Fabian / World Bank