The decision to allocate $650 billion of special drawing rights (SDRs) from the International Monetary Fund (IMF) to the global economy is welcome. An IMF reserve asset that countries can convert to foreign currency, the SDRs will give many liquidity-constrained low- and middle-income countries a boost to their reserves. At the same time world leaders have recognized that this liquidity boost is not essential for many rich countries. So there has been a call to reallocate or recycle rich-country excess reserves to countries who need them to address critical economic demands resulting from the current economic crisis.

One way to use this extra ration of global liquidity will be to bolster the concessional lending pot the IMF has to help low-income countries—the Poverty Reduction and Growth Trust (PRGT). New commitments from the PRGT grew from a yearly average of less that $1.5 billion between 2015 and 2019 to over $9 billion in 2020. The stock of outstanding credit from the PRGT doubled to $19 billion in 2020. Given projected LIC financing needs for the next five years, we expect PRGT lending to continue at least at 2020 levels – and this means the PRGT needs to be replenished.

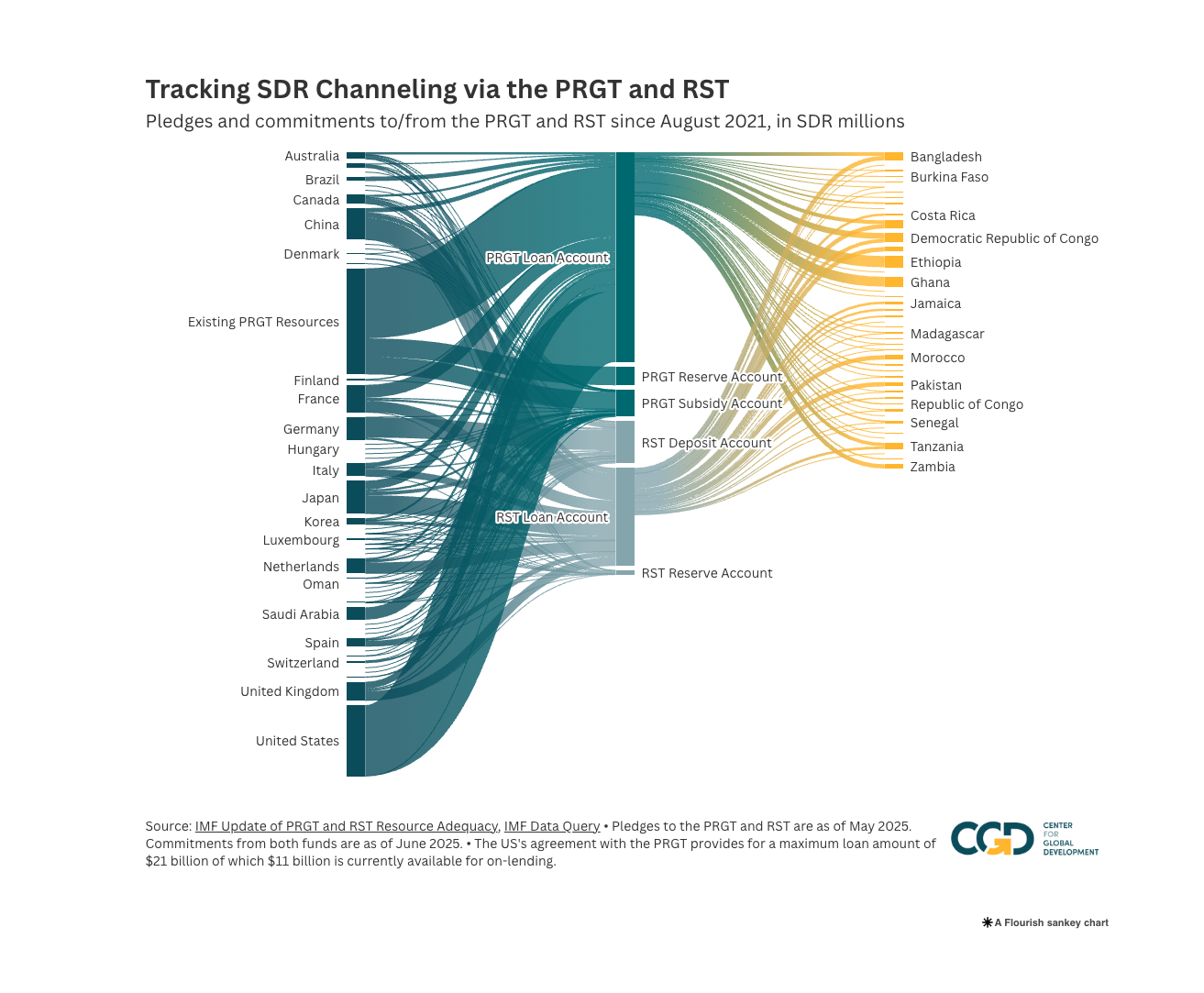

Channeling SDRs

There are several different ways to reallocate SDRs to support the IMF’s PRGT lending. Choosing between these various mechanisms requires an understanding of the set-up of the PRGT, the peculiar features of the SDR, and the preferences and institutional constraints of the country reallocating its SDRs.

As we have explained elsewhere the PRGT is in fact a hybrid. There are three pots of money: one for lending (the loan account), one to pay for the subsidies implicit in the IMF’s concessional loans (the subsidy accounts), and one to cover creditors in case of late payments (the reserve account, which also earns interest to meet subsidy costs). The subsidy and reserve accounts together comprise the PRGT endowment. Supporters of the PRGT can lend money to the loan account, which is then on-lent to low-income countries and eventually repaid. This increased lending will need to be accompanied by new resources for the other two pots of money. The PRGT’s subsidy costs will increase, and the subsidy accounts will therefore need replenishing at some point. Increased lending will also see the reserve account decline in relation to the stock of outstanding credit, weakening the assurance it provides to potential lenders. The subsidy and reserve accounts require permanent transfers, donations—grants—that never get returned, but there may be a way to use loans to generate such transfers. It will not make sense for any donor to donate SDRs to the loan account.

There are therefore three different ways to channel SDRs:

| Modality | |||

| Loans of excess SDRs | Donations of excess SDRs | ||

| Beneficiary | Loan Account | ✓ | N/A |

| Subsidy and Reserve Accounts | ✓ | ✓ | |

The avenue through which countries choose to support the PRGT with excess SDRs will depend on their preferences and what is possible given domestic institutional arrangements regarding ownership and use of SDRs. Two general points are worth noting. First, the SDR is considered a reserve asset and this places limits on its use; and, second, when a country holds fewer SDRs than it has been allocated to it by the IMF, it must pay interest at the SDR rate. Thus, there is a potential cost to lending or donating SDRs to another member or to a fund like the PRGT. In normal times the SDR interest rate is a weighted average of 3-month bond rates for the currencies in the SDR basket, but it is now at its predetermined floor of 0.05 percent.

The three mechanisms for SDRs to support the PRGT are as follows:

1. Lending to the PRGT loan account is a well-established and relatively straightforward way for rich countries to use their excess SDRs. The PRGT relies on resources borrowed from IMF members which it then on-lends at a subsidized rate of interest (currently zero). All loans are denominated in SDRs, but more than half of the current borrowing agreements, by value, also stipulate SDRs as the media in loan transactions. Loans to the PRGT typically earn the SDR interest rate, thus offsetting the cost of a lender’s deficit in its SDR holdings. The borrower’s claims on the PRGT can be traded among official entities, and their liquidity is also supported by an “encashment” regime. This allows participating lenders to seek early repayment of their loans if needed while also authorizing their own loans to be drawn upon to meet early repayments to other lenders. These features, coupled with the low risk of lending through the PRGT, retain the reserve asset characteristics of the SDR. This has been flagged as important by the G20 it its recent communique.

2. Donations of SDRs could, in principle, quickly fill the need for grant resources for both the subsidy and reserve accounts. Donations of SDRs would lead to a permanent transfer to the PRGT and could be mobilized quickly. On the IMF’s side, to overcome the complication that the PRGT is not a designated holder of SDRs, the donated SDRs would need to be converted to hard currency through an intermediary—either another IMF member country or a designated holder—or, more straightforwardly, the country could donate hard currency that is freed up by their new SDR allocation. Domestic institutional structures and regulations on the use of SDRs will also need to be addressed. Although the SDR allocation can be seen as a free resource, turning this into a donation would probably require budgetary approval. The onus will be on countries to find ways of unlocking the “free resource” provided by the allocation and this is likely to require close coordination between the central bank and finance ministry.

3. If donations of excess SDRs prove infeasible for some countries, subsidized lending of SDRs could bolster subsidy resources. This can be accomplished in two ways, each of which has some precedent.

-

First, subsidy costs for the surge in PRGT lending could be reduced directly. In all of the discussion so far, it was assumed that the lenders to the PRGT would, as usual, earn the SDR interest rate. But the subsidy needs of the PRGT during this period of exceptionally high lending could be contained by the simple expedient of lenders accepting a lower interest payment. And in this context, it is notable that at least one current borrowing agreement—with the UK—caps the interest rate at the floor of 0.05 percent. The loan in effect provides resources to the subsidy account and the value of the implicit donation could be acknowledged.

-

Second, subsidy resources could be provided by way of low-interest loans to the PRGT which are in turn invested to earn a premium for the subsidy account. This mechanism is not new and has been used to raise a small proportion of the PRGT’s subsidy needs. To cover the ongoing interest subsidy of PRGT lending, any sums lent by donor countries to benefit the PRGT subsidy and reserve accounts for investment would have to be a multiple of the PRGT loans to low-income countries. To scale up the use of this option using SDRs, some form of “encashment” regime might be needed, mirrored on the arrangements described above for lending of excess SDRs to the PRGT loan account. This approach would also require conversions out of SDRs if the PRGT were to invest these resources.

How much support will the PRGT need?

Some simple—purely hypothetical—calculations are useful to illustrate the broad magnitudes of what it would take to bolster the various components of the PRGT.

Loans to the loan account. Maintaining PRGT lending at the pace seen in 2020 for 5 years could be covered by new loan resources of $45 billion. Although this would be a very large number for the PRGT, these new loan resources would be a relatively small share of rich countries’ excess SDRs. For example, the 17 countries with current borrowing agreements supporting the PRGT will receive over $300 billion in the forthcoming SDR allocation; the EU, US, and UK combined will receive $340 billion; and the G20 as a whole $440 billion.

New subsidy resources. In broad terms, assuming an SDR interest rate of 2 percent is paid to lenders over the average loan maturity of about 7 years, the incremental subsidy cost of each $10 billion lent is about $1.4 billion. The total additional subsidy costs of $45 billion in new loan commitments made over the five years 2021-25 would therefore be about $6 billion. Although subsidy payments are made over the life of the loans, the IMF needs to be confident that it will have the resources to meet these future costs when committing new PRGT support. This should not be a problem in the initial years, as the subsidy account currently stands at about $5.5 billion, but the replenishment of the subsidy accounts with grants will become more pressing over time.

The reserve account. This has remained at about $5.5 billion but has already fallen below a third of the stock of credit outstanding for the first time and would fall below 15 percent of credit in the near future if commitments stay at 2020 levels. This could prove to be a more immediate constraint on lending, as creditors see a continued erosion of the assurance provided by these reserves. Annual commitments of $9 billion for the next five years would bring the outstanding stock of credit to over $50 billion by 2025 and maintaining a reserve account of one-third this stock would require donations of an additional $10 billion. These reserves can be built up over time but should be in place before repayments to the PRGT begin to rise sharply in 2025, echoing the surge in lending that began in 2020.

Donations will be needed for both the subsidy and reserve accounts. The third avenue described above—of using subsidized loans to bolster subsidy resources or lessen subsidy costs—is unlikely to provide more than a supplement to the grants that will be needed. We discuss elsewhere the possibility of gold sales to bolster the subsidy and reserve account as well as internal policies the IMF could implement to take some pressure off these accounts.

Looking beyond the next few years, the desired scale of PRGT operations over the longer term will be a key determinant of financing needs. Before the pandemic, the PRGT was operating under a self-sustaining framework in which returns from the subsidy and reserve accounts (which together comprised the PRGT’s endowment of about $11 billion) were sufficient to maintain annual commitments of about $1.75 billion. This capacity would, in broad terms, be restored by the grants of $6 billion needed to replenish the subsidy account as noted above. An injection of $10 billion into the reserve account, as also noted above, would then bring the endowment to almost double its size before the pandemic and the self-sustained capacity would also broadly double to about $3.5 billion.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.