In brief: A straight proportional $650 billion SDR allocation is the smart thing to do. It provides quick and substantial help to low-income countries (LICs) and emerging markets (EMs) who need the liquidity the most. There are ways in which some rich countries could donate or lend some of their SDRs to either poor countries or to the IMF for lending to poor countries, but this will take longer to design and can be agreed and implemented after any general increase. Using SDRs to fund programs that lie outside of the IMFs core areas (e.g., health) will be even harder to implement without major changes in the IMF’s legal and policy framework.

With the Biden administration now setting US development policy, there are increased hopes for an new allocation of Special Drawing Rights (SDRs) from the IMF (For background see here and here). One sticking point continues to be the distribution of the new SDRs. Two problems are raised:

First, as new SDRs are distributed in proportion to IMF quotas (or ownership shares), the bulk of the new SDRs will go to rich countries. Low-income countries (LICs) would receive only 3.2 percent of any allocation, while G20 countries would receive 68 percent and the US, EU member countries and the UK would together receive 48 percent. To some this seems an inefficient way to distribute liquidity assistance.

Second, all IMF member countries in good standing with the institution get some SDRs. That means if the United States goes along with an SDR allocation, it goes along with giving Iran and Venezuela some SDRs. And India going along means approving liquidity for Pakistan.

We lay out the nitty gritty of the complex rules governing SDRs and their allocation in a new paper, published today. Here we give nine “bottom line” messages that we draw from our detailed analysis:

-

There is no quick way for the initial allocation of new SDRs to benefit some countries and not others. The only time SDRs were given to a subset of countries was when the countries formerly part of the Soviet Union joined the IMF, and the process took 12 years. It requires an amendment to the IMF’s Articles of Agreement (constitution) and would be seen by many to move away from the quota-based system that is the foundation of IMF operations.

-

That means that each member country will have to live with the reality that some of its antagonists will benefit from an SDR allocation. It will be incumbent upon each government to explain to its domestic critics why it is going along with an action that helps its antagonists. The answer is simple—for LICs and some middle-income countries that are critically short on foreign reserves, the boost in liquidity will go a long way to help them fight the crisis at no cost to domestic taxpayers in any country. But the allocation isn’t large enough to undo any financial sanctions that might be in play in global politics.

-

It also means that another way needs to be found to reallocate new SDRs away from rich countries and to poor countries. While a reallocation scheme could be agreed before the new SDRs are given out, it will only be effected afterwards.

-

Even without a reallocation, LICs get considerable benefit out of an SDR allocation. An allocation of around $650 billion worth of SDRs would yield almost $21 billion, which is more than the current IMF credit to LICs (about $17 billion) and over twice as big as the IMF spend on LICs in 2020. Emerging market economies, which have also been hit hard by the pandemic, would also benefit. And for all countries, this allocation is unconditional.

-

Rich countries could agree to donate their SDRs to LICs. There are some complications that would need to be worked through. Somehow a decision would have to be made on which LICs get how much. Every donating country could make its own decision, or a coalition of richer countries could decide. This could be worked out before the new allocation took place as a “side agreement” or after. Also, the donating countries will incur an interest cost (currently minimal given low interest rates) and receiving countries an interest bonus—some cost-sharing arrangement may be needed.

-

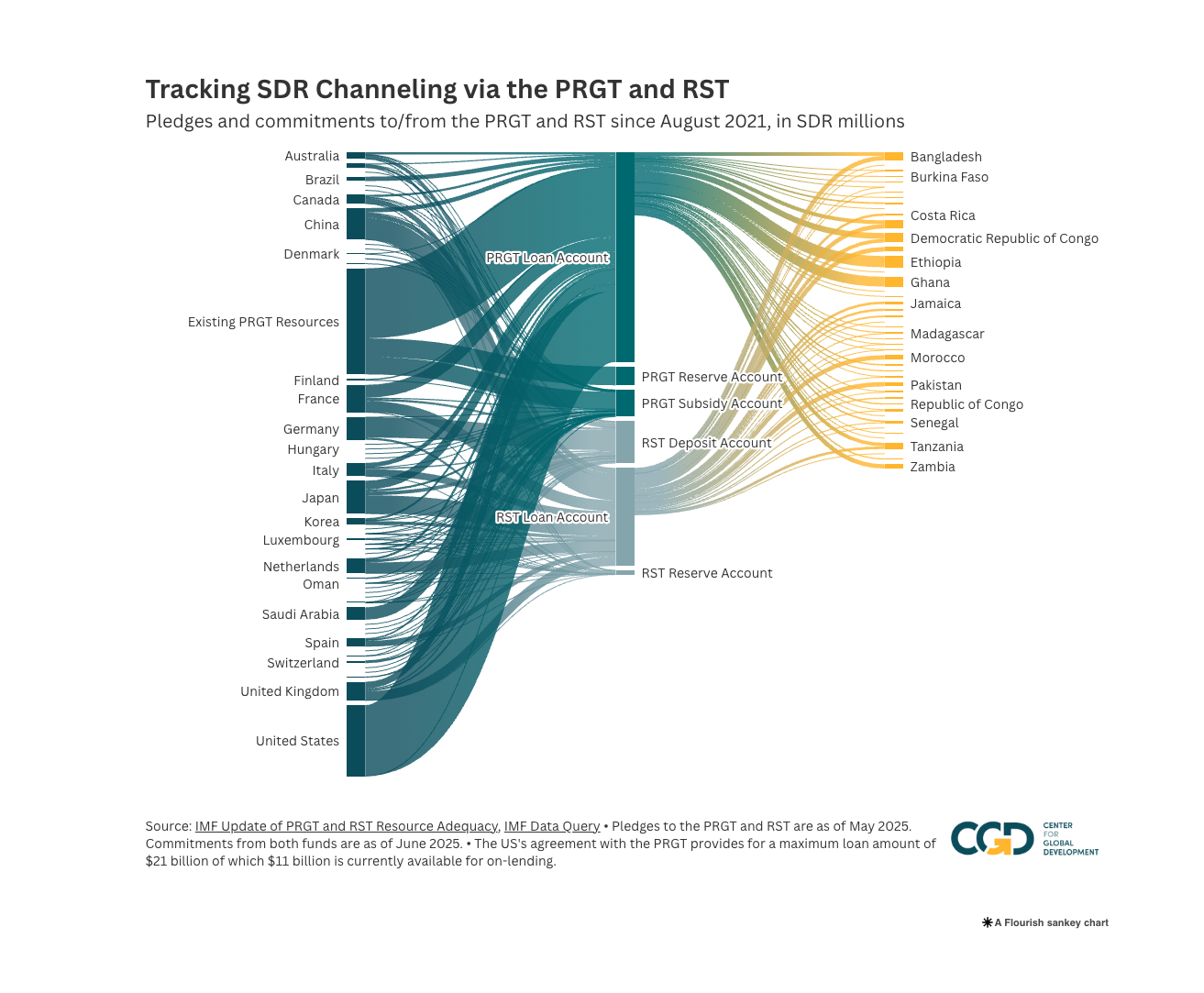

An alternative to outright donation is lending SDRs from rich to poor countries, in two possible ways. One possibility, used in the past, is to lend new SDRs to the Poverty Reduction and Growth Trust (PRGT), which is the pot of money used to make concessional loans to LICs. These resources would then be on-lent to LICs through the existing IMF loan facilities. There are two advantages to using SDRs in this way: first, the lending country assets are protected by the IMF’s safeguards embedded in the PRGT (see paper); second, the SDRs will be on-lent only to LICs whose policies conform to IMF macroeconomic management standards, as enshrined in their IMF-supported programs.

-

The second possibility—to lend directly from rich countries to LICs or other countries—is less attractive. Like the donation schemes, donors or groups of donors could lend their SDRs to selected LICs, according to their own preferences, without the IMF’s intermediation. But the rich countries’ assets would not be protected should any LIC confront serious liquidity constraints that would impede repayment.

-

The idea of reallocating new SDRs to a special purpose fund, either within or outside the IMF’s purview, has been mooted by many, but is hard to put in place. The idea here is for countries to use their SDRs to provide financing for certain international purposes, such as vaccine provision or climate mitigation or adaptation. While these ideas are not new, they have not been put to test and face a difficult series of policy and regulatory hurdles within the IMF and with its shareholders. Such a fund would need to be designated to receive SDRs as capital by an 85 percent vote of the IMF’s Executive Board, with their use seen as consistent with the IMF’s Articles of Agreement. The Articles also restrict the types of operations that can be conducted with SDRs, particularly so their use does not run counter to the function of the SDR as a global reserve asset. While innovative thinking, backed by a strong consensus of the shareholders, may be able to overcome these hurdles, it will require considerable technical and political efforts to make an SDR-based special purpose fund operative.

-

But an SDR allocation could give rich countries more flexibility to use their own reserves to credit a special purpose fund. New SDRs would increase overall reserves of all countries. If this increased reserve position is not necessary, countries with stronger reserve positions at the outset could then donate non-SDR reserves up to the equivalent of their share of the SDR allocation to a special purpose fund. This fund, consisting of non-SDR reserve donations of various countries, would not be subject to the restrictions imposed by the IMF’s Articles of Agreement. The feasibility of such a step would depend on each country’s domestic laws, regulations, and policies governing the use of central bank assets.

Overall, the IMF’s Articles of Agreement impose a certain inflexibility in the use of SDRs that is appropriate to their standing and use as international reserves. The global community can decide to increase the flexibility in their use, but it will require a broad international consensus (85 percent vote of the IMF’s shares) and it will take time.

While a new SDR allocation, without reallocation, has its drawbacks it can be done relatively quickly, meeting in part the pressing need for liquidity of both LICs and emerging market economies.

A prior agreement on a reallocation would be desirable to ensure greater support for LICs. And a smaller allocation that is subsequently retargeted could help lessen the concerns we noted at the outset. But the best must not become the enemy of the good. It will take time to build the necessary political consensus and technical apparatus for a “precooked” reallocation, and an immediate allocation should not be sacrificed to this end.