The World Bank/IMF Annual Meetings begin next week—against a backdrop of mounting economic crises and uncertainty. How can we reduce global debt? Rethink the MDB/IMF system to address pressing issues like pandemics, climate change, and food security? Support poor countries where they need the most assistance?

Our experts share what to watch at this year’s meetings, where the Bank, Fund, and shareholders need to step up—and what’s next.

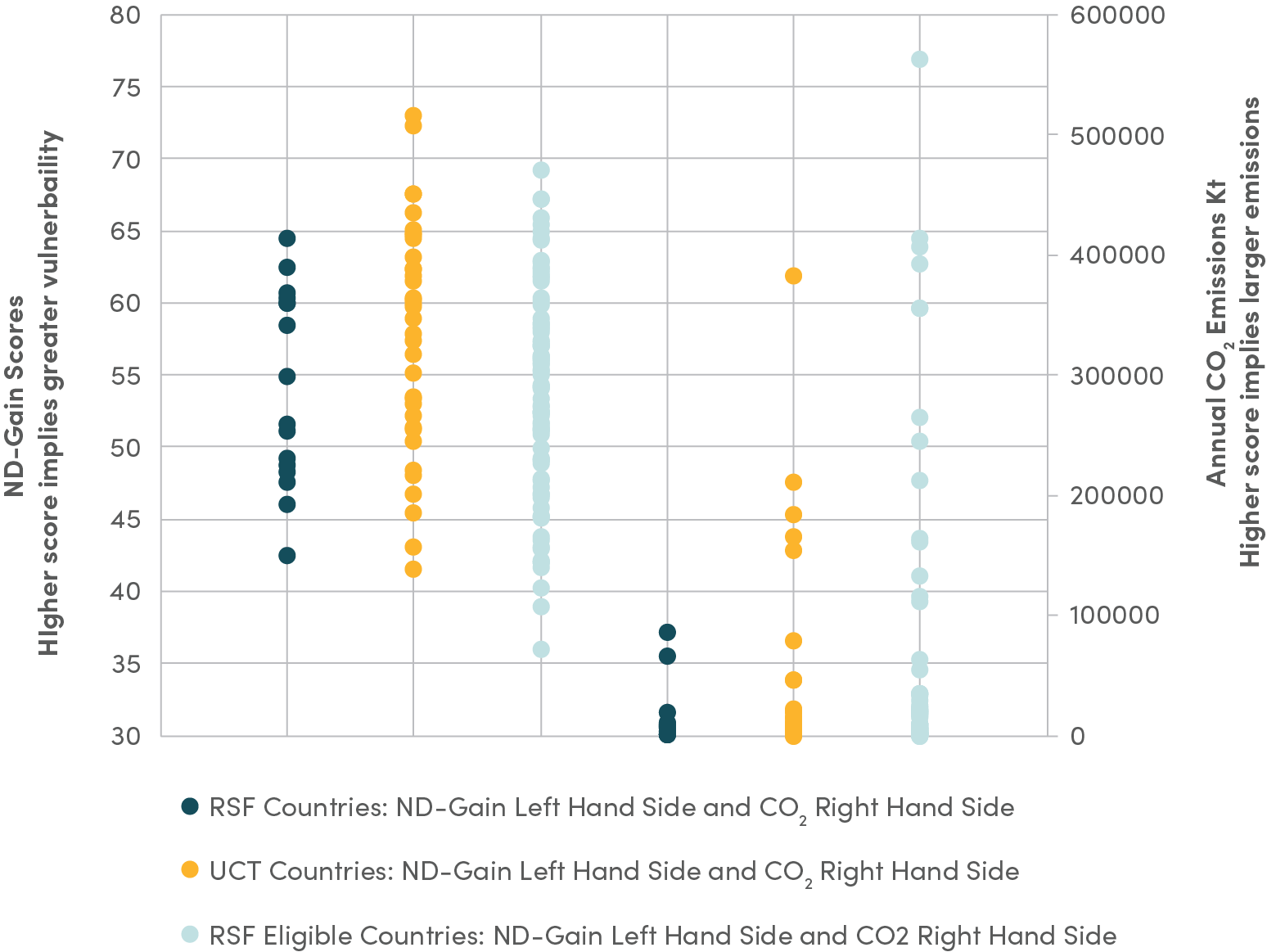

You can find our full list of Annual Meetings events here.

The Time for Debt Action is Now

Since the Spring Meetings, progress on debt sustainability and restructuring has been slow while the problem has only grown. Nearly two-thirds of LICs and almost one-third of LMICs are at high risk of, or in, debt distress as developing country debt payments doubled between 2010 and 2021, reaching their highest level in 20 years. Debt burdens are crowding out other urgently needed investments, such as in climate adaptation and social protection. The Vulnerable Group of Twenty (V20)—a group of 55 economies exposed to the fallout from climate change—expect debt service payments to rise to $69 billion by 2024, the highest level in the current decade. Meanwhile, in sub-Saharan Africa, governments are projected to allocate nearly 12 percent of their revenues to servicing external debt in 2022.

Much attention has been drawn to this problem, including by the heads of the World Bank and the IMF, while many salient proposals have been put forward to improve restructuring processes and the Common Framework for Debt Treatments beyond the DSSI, including a few from CGD. However, nearly two years since the establishment of the Framework, only Zambia is nearing completion of the process – with Chad and Ethiopia still in process. And, as a middle-income country, Sri Lanka has demonstrated the limitations of the current approach for countries not covered by the Common Framework. It is almost certain that more countries will need urgent help soon even though they could have benefitted from more proactive restructuring - but have been discouraged from coming forward. Ultimately, the problems and needs are clear, and the time is right for implementing concrete solutions. A clear statement from both organizations on actions that will be taken, as well as a more proactive role by them, would be a step in the right direction.

- Masood Ahmed

Realizing the Bank’s Potential on Climate and Beyond

World Bank President David Malpass’s recent wavering around whether climate change is man-made will loom large over the Annual Meetings. Prior to this maelstrom, key shareholders had already been voicing concern about the institution’s lack of ambition on climate. Shareholders will likely use this week to lay out an affirmative vision for a successful climate agenda at the institution. A practical way of doing this would be for governors to collectively press the Bank to be more ambitious with its own balance sheet.

A G20 panel report recently laid out a series of steps that the World Bank and other multilateral development banks could take to unlock hundreds of billions in new financing, but the World Bank has reportedly chafed at many of the recommendations. More funds aren’t just of vital importance for climate but growing the resource pot is essential to reconciling the tradeoffs between climate and development finance—which makes the Bank’s conservative stance all the more perplexing. But in the end, significant course correction for a ship the size of the World Bank needs unambivalent leadership from the top. And shareholders will need to take a hard look at what is really standing in the way of the Bank realizing its full potential on climate and other priorities.

- Clemence Landers

Expanding MDB’s Lending Capabilities

In July, the G20 published a report by the independent experts panel on MDB capital adequacy. The report's recommendations, if implemented, would support a major increase in collective MDB lending, potentially amounting to hundreds of billions of dollars over time. The report spells out how this expansion in lending can be achieved while maintaining strong MDB institutional ratings.

In fact, the findings make the case for MDB general capital increases stronger: the additional capital would be more productive. Significant analysis, information gathering, and consultations went into the report—but the next phase will be harder. The G20, MDB shareholders generally, and MDB managers now have to come together to decide on implementation strategies. We and other stakeholders will be watching to see what the G20 says and does, and which shareholders and MDB heads speak up and lead the way.

- Nancy Lee

LMICs Need More from the IMF

The IMF meetings will be focused on current global macroeconomic turmoil, especially the fragility of global capital markets exposed by the UK’s economic policy shift. But for LMICs, the focus will be on the IMF’s response to the food/fuel/financing crisis stemming from Russia’s invasion of Ukraine. While the IMF was quick to step up to the economic problems caused by the pandemic, the response to the second-wave crisis has been slower (see Charles Kenny’s recent blog).

The announcement of a “food price shock” window in the Fund’s emergency financing toolkit last week is welcome, but it is also weak, probably reflecting the lack of Board consensus on whether to extend more non-conditional financing to LMICs. And many LMICs see it as a guise to break IMF rules to help Ukraine.

The IMF is likely to make more announcements on mobilizing the Resilience and Sustainability Trust (RST), which to date has registered formally only one donor (Spain) and one potential recipient (Barbados). There may be an announcement of opening up SDR recycling to the AfDB—it is a work in progress. There will likely be hand wringing over the growing debt crisis, but it is unlikely a serious fix to the feeble Common Framework (CF) will be proposed. Instead Zambia will be cited as an example of how it can work —but that is a pretty poor result some two years after the CF was established.

LMICs will be calling for more from the Fund. Some want a new SDR allocation, which seems politically impossible given the 85 percent vote needed in the IMF’s Board. Others would like a more aggressive version of the Debt Suspension Initiative to be reinstated by creditors—again probably difficult to get through the IMF Board, as it would be seen to comfort commercial creditors and China.

What is really needed from the IMF is a clear global strategy as to how it will help LMICs through the current crisis. The official global financial community is pouring huge amounts of money into Ukraine, largely unconditionally. The rest of the LMICs suffer from the crisis and get relatively stingy conditional help from the IMF. It is not enough to get them through the current economic turmoil.

- Mark Plant

CGD blog posts reflect the views of the authors, drawing on prior research and experience in their areas of expertise.

CGD is a nonpartisan, independent organization and does not take institutional positions.