Recommended

Blog Post

MIGA: The Little Engine That Should

World Bank Group President Ajay Banga has made the increased use of guarantees a key objective of his reform agenda, committing to a significant uptake in their use and facilitating this uptake by merging all instruments under the Multilateral Investment Guarantee Facility (MIGA), an arm of the World Bank Group.

The latest iteration of the reform effort is a new structure that combines three instruments:

- a development policy loan (DPL) from IDA (the concessional arm of the World Bank) or the IBRD (the non-concessional arm of the World Bank);

- a policy-based guarantee (PBG) from IDA or IBRD; and

- a non-honoring (NH) guarantee from MIGA.

DPLs are provided as budget support and typically include a range of macro-level (versus project) policy commitments to improve a country’s economic fundamentals and boost confidence in its debt service ability. Examples include reforms to diversify the tax base or reduce costly subsidies. The PBG and NH guarantees give private lenders cover against the risk of debt service default by the sovereign borrower. As a package, these instruments can support multiple aims, including short-term liquidity relief, lower debt service payments, improved market access, funding for development priorities and better macro management.

Since September 2025, operations have been approved for Côte d’Ivoire, Panama, Angola, and Rwanda; a proposal for Argentina is pending.

While good in theory, World Bank guarantees have had an inauspicious history

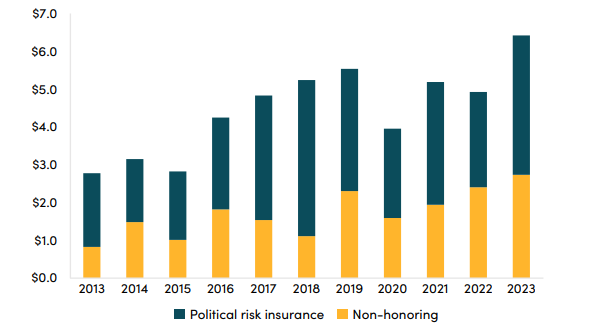

Many of us at CGD have been calling for greater and more innovative use of World Bank guarantees for a long time (see here, here, and here), emphasizing their relevance during periods of capital market volatility and risk aversion. Those factors, which are present today, coupled with declining official development assistance, necessitate that available instruments be used as efficiently and effectively as possible.

This structure is a good example of an initiative designed to improve reach and impact without the need for additional donor resources. That said, the World Bank’s record of guarantee use has been mixed. The PBG was first launched in 1999, with Argentina and Colombia the first two beneficiaries. But Argentina’s guarantee was called in 2002, ending World Bank use of the instrument for nearly a decade. Appetite for the PBG resumed in the context of the eurozone crisis, with PBGs approved for Serbia, Macedonia, Montenegro, and Albania between 2011–2015. Use of the PBG declined again after a 2015 guarantee for Ghana failed to generate any clear financial benefit. In addition, Ghana defaulted on the guaranteed bond (a $1 billion issuance) in 2022. Although the guarantee was not technically called, the default led to a messy, complex restructuring outside the legal scope of the agreement that included upfront payments from IDA to bondholders and termination of the guarantee.

The new framework

In the past we have identified two impediments to the use of World Bank guarantees: provisioning and eligibility. The new initiative addresses the second issue but not the first. The World Bank and IDA provision guarantees like loans (e.g., 100 percent of face value), even though loans are always disbursed and guarantees are rarely called. Reforming this policy would enable them to stretch balance sheets further, and would be consistent with the allocation policy, which is to have only 25 percent of an issued guarantee count toward the World Bank’s country exposure limit or IDA allocation.

The new framework expands borrower eligibility of MIGA’s NH product, which insures against non-payment of sovereigns, sub-sovereigns, and state-owned enterprises. Until recently, use of the NH guarantee was limited to countries with credit ratings of BB- or above, essentially ensuring that only middle-income countries could get coverage. In this 2023 paper, we argued for greater eligibility of the NH product (e.g., to B rated sovereigns) and for closer harmonization with the World Bank on its instruments to address complementary risks. This new structure does both: MIGA is now able to extend its NH product to B+, B, and B- countries, but only in conjunction with a PBG from the World Bank/IDA. These PBGs, in turn, can only be offered to countries at low or moderate risk of debt distress—although in 2015 an exception was made for Ghana, a high-risk country, when the World Bank board greenlighted the $400 million PBG. As we discuss below, it appears that the World Bank is preparing to make another exception, this time for Argentina, which is also at high risk of debt distress and is rated CCC+ by two out of three credit rating agencies. This begs the question of whether other CCC+ countries will benefit from the same consideration, especially as no similarly rated borrower has defaulted to the World Bank.

Thanks to the expansion of eligibility for the NH guarantee to B- countries, ten IDA countries and eight IBRD countries can now access the product under this structure. Expanding consideration to CCC+ would add two more IBRD countries (in addition to Argentina) and seven more IDA countries. (See figures 1 and 2.)

A closer look at the new guarantees

To date, the World Bank Group has used the combined loans and guarantees to support Côte d’Ivoire, Panama, Angola, and Rwanda. In mid-April of this year, the World Bank announced that it intends to provide $2 billion in guarantees to Argentina to help reduce refinancing costs, which, if approved, would be the largest guarantee so far.

Côte d’Ivoire (CIV): This operation was done in stages. In December 2024, the World Bank approved a debt-for-development swap aimed at improving the country’s debt profile while freeing up resources for education. The project included an IDA budget support loan of $311 million and an IBRD PBG of $574 million, part of which covered the swap and part of which covered a sustainability-linked loan (SLL), financed by Standard Chartered. Coverage of the SLL was augmented with a $433 million MIGA NH guarantee approved in September 2025, representing the first use of joint IBRD and MIGA projects. Under the SLL, CIV’s interest rate is tied to the achievement of performance targets related to conservation and renewable energy, validated by independent third parties. This complex arrangement is enabling CIV to support multiple objectives, including human development and green energy goals, while improving its debt management.

Panama: In December 2025, the board approved a package for Panama consisting of a $500 million IBRD DPL and two World Bank Group guarantees ($600 million PBG and a MIGA guarantee of $730 million) to back a commercial loan of up to $1.4 billion, generating estimated cost savings of $110 million. The guaranteed loan is intended to reduce Panama’s financing costs and support the “eventual recovery of its investment grade profile.” In fact, Panama is already rated investment grade by Moody’s and Standard & Poor’s (Baa3 and BBB- respectively). Only Fitch has rated Panama below investment grade, with a BB+ rating. It is hard to see the additionality here: Panama is a high-income country, and with an annual budget envelope of $35 billion, the savings of $110 million is a pittance, at 0.3 percent of the total, and represents only 8 percent of the $1.4 billion that the guarantees will help mobilize.

Angola: This operation aims to strengthen Angola’s fiscal policy, boost private-sector growth and job creation, and support human capital and digital development. It includes a $750 million DPL plus an IBRD PBG of $240 million and a MIGA guarantee of $140 million. The guarantees will help Angola buy back or prepay $400 million of commercial debt, generating an estimated $75 million in savings. In addition, the swap is expected to free up approximately $230 million in cash flow (in nominal terms) over the next three years, two-thirds of which will be used to increase education spending.

Rwanda: The Rwanda operation aims to create “resilient and inclusive jobs” by strengthening financial sustainability, with a focus on domestic resource mobilization, improving “foundational” infrastructure for job creation (e.g., telecom), and supporting interventions to accelerate industrial and agricultural modernization. It includes a $100 million credit from IDA, a first-loss IDA PBG of $240 million, and a second-loss MIGA guarantee of $187.5 million. The guarantees are intended to support $450 million in commercial financing and “compare favorably” to the estimated 8 percent cost for a Eurobond issuance. Final pricing will be determined through a request-for-proposal process for commercial lenders.

Argentina: Déjà vu all over again

A proposed $2 billion IBRD/MIGA guarantee for Argentina will likely be considered by the World Bank board ahead of an estimated $4.3 billion in commercial debt payments coming due this July. What makes this operation unusual is that Argentina does not technically qualify for the guarantees because it is rated below the B- cutoff by Moody’s (Caa1) and S&P (CCC+), although Fitch just upgraded Argentina to B- on May 5 of this year. Even more eyebrow raising is that Argentina is one of the very few countries that have defaulted to the World Bank, as well as to the IMF and private creditors. In fact, and as noted earlier, the World Bank’s inaugural PBG to Argentina was called in 2002, which led to the shelving of the instrument for nearly a decade. Compared to the four countries that have received the guarantees to date, Argentina’s debt-to-GDP ratio is the highest, at 80 percent. While we have been advocating for greater risk tolerance from the IBRD, this is not where we would have chosen to push.

Preliminary assessment

Our key observation is that net present value savings from these guarantees are not large: $65 million for Côte d’Ivoire, $75 million for Angola, and $110 million for Panama. These savings relative to total funds mobilized are 19, 13, and 8 percent respectively. In addition, we do not see a clear development case for upper-middle- and high-income countries.

That said, we think the structure is a good option for IDA countries because it can enable countries to stretch their IDA allocations (since only 25 percent of an issued guarantee counts toward their IDA envelope), cost savings can be used to finance development objectives, and countries can gain credibility with creditors, potentially reducing country spreads over time. A detailed analysis of the operation in Côte d’Ivoire found that it provided important gains, including reduced debt service obligations during a period of constrained liquidity while providing funding to build schools. It also concluded that an indirect effect was lower overall spread on its borrowings.

We hope that the risk-sharing principle underpinning this new structure will enable IDA to be more ambitious in scope and size, enhancing the benefits. Finally, we urge that the provisioning guidelines be revisited, in line with other capital adequacy reforms that the World Bank has undertaken, enabling both IBRD and IDA to further stretch their balance sheets.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.