Recommended

Project

Blog Post

The Perils of a Declining Labor Force

Blog Post

Forecasting Global Growth to 2050

This note presents two scenarios for the world economy and development prospects to 2050 based on the forecasting exercises and analysis presented in a series of papers by Philip Adom, Augustin Kwasi Fosu, Dede Woade Gafa, Zack Gehan, Brian Webster, Ranil Dissanayake and Charles Kenny. "A World Off Course" outlines the downside scenario while "Momentum Regained" suggests the upside potential. The core growth forecasting exercise used the past cross-country relationship between income growth and lagged income, demographic features, climate, and education to predict a central estimate of future income per capita based on existing forecasts of education, demography and climate. We use error terms to set high and low bounds on country outcomes, and it is the high and low bound results that form the basis for scenarios presented here. It should be noted that the approach makes our optimistic scenario for poverty reduction particularly bullish -it assumes all of the countries home to the world's poorest people see comparatively rapid growth.

1. A world off course

The first half of the Twenty First Century saw strengthening headwinds against global growth.

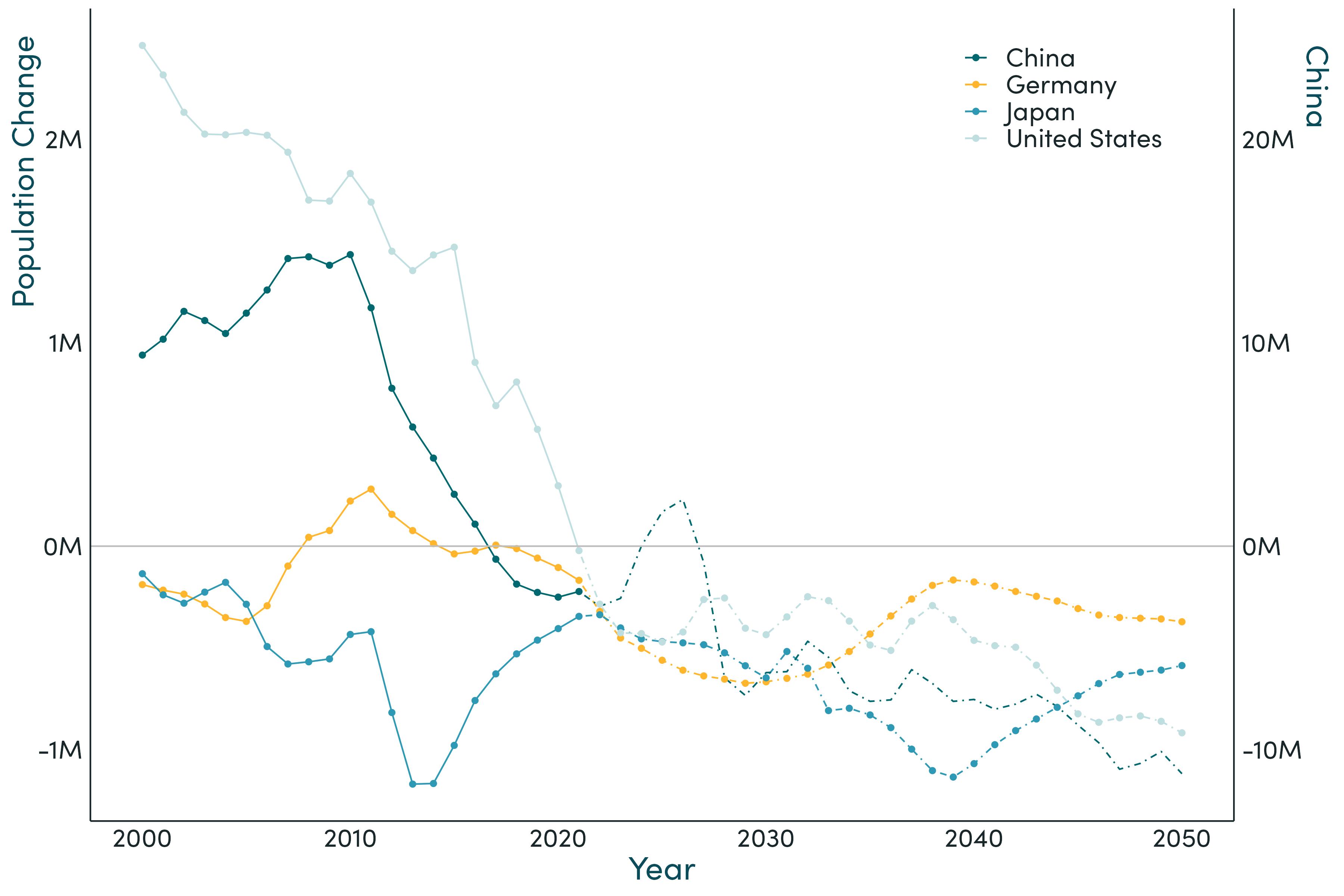

In the first half of the Twenty First Century the global economic landscape was considerably reshaped by demographics.Beginning for Japan in the 2000s and rapidly accelerating and spreading thereafter, high income and upper middle-income countries saw an unprecedented collapse in their workforce. The prime working-age populations of OECD countries shrank by more than 92 million people between 2015 and 2050. Italy's working age population shrank by nine million people, Japan's by 20 million. A number of wealthy countries saw their dependency ratios (children and retirees divided by working age people) rise above one. Between 2020 and 2050, South Korea went from one dependent for each two workers to more dependents than workers.

Beyond the rich country club of the OECD, Russia's working age population fell by 15 million and China's by 160 million.Poland, Romania, and the Ukraine all saw working age populations fall by 25 percent or more between 2020 and 2050. Theproblem extended across East Asia and Latin America, only leaving South Asia and Sub-Saharan Africa comparatively untouched.

With rising demand for care and health services from a growing population of retirees combined with a declining workforce, the result was tight labor markets and widespread labor shortages. By the late 2020s, the US was facing acute shortages of truckers, hospitality workers, construction staff, and farm labor. The UK found challenges filling positions in transport, butchering, bricklaying and welding, social care work, nursing, engineering, meatpacking, cheesemaking, factory work, and even daffodil and cannabis farming. Germany faced shortages of engineers, nurses, care workers, cooks, and metal workers.

Figure 1: Annual change in working age population (millions)

Historical then UN projected, no migration scenario.

Early hopes that robots and artificial intelligence could rapidly replace workers proved ill founded. While manufacturing and agriculture did see some further automation, progress in services was considerably slower. Self-driving trucks and cars did finally start to spread in the 2030s but consumer resistance (and related regulatory sclerosis) slowed adoption rates. Historians of technology were not surprised: trains that didn't require drivers had been operating since at least 1968, and yet most trains still had drivers sixty years later. Meanwhile, home help robots augmented rather than substituted human assistants, and the growing care industry remained overwhelmingly staffed by people rather than machines.

That slow progress in robotics was part of a broader trend across technologies: ideas were becoming harder to find. The number of patentable inventions produced per researcher restarted its long-term decline. Education rates in the wealthiest countries plateaued, and an older and shrinking cohort of scientists and engineers in countries home to most of the world's research potential had to engage in ever larger collaborative efforts to reach the frontier of knowledge, with the associated bureaucracy and transactions costs. New firm creation continued its decline as well. Furthermore, aging populations were associated with an acceleration in rising demand for services long associated with low productivity growth. These services now made up morethan four fifths of rich country economies. Total factor productivity growth contributed less and less each year to OECDoutput, another trend that had been ongoing since the Twentieth Century. In the US, long-term total factor productivitygrowth dipped below 0.5 percent a year, little more of a third of its average between the end of World War Two and 2010.

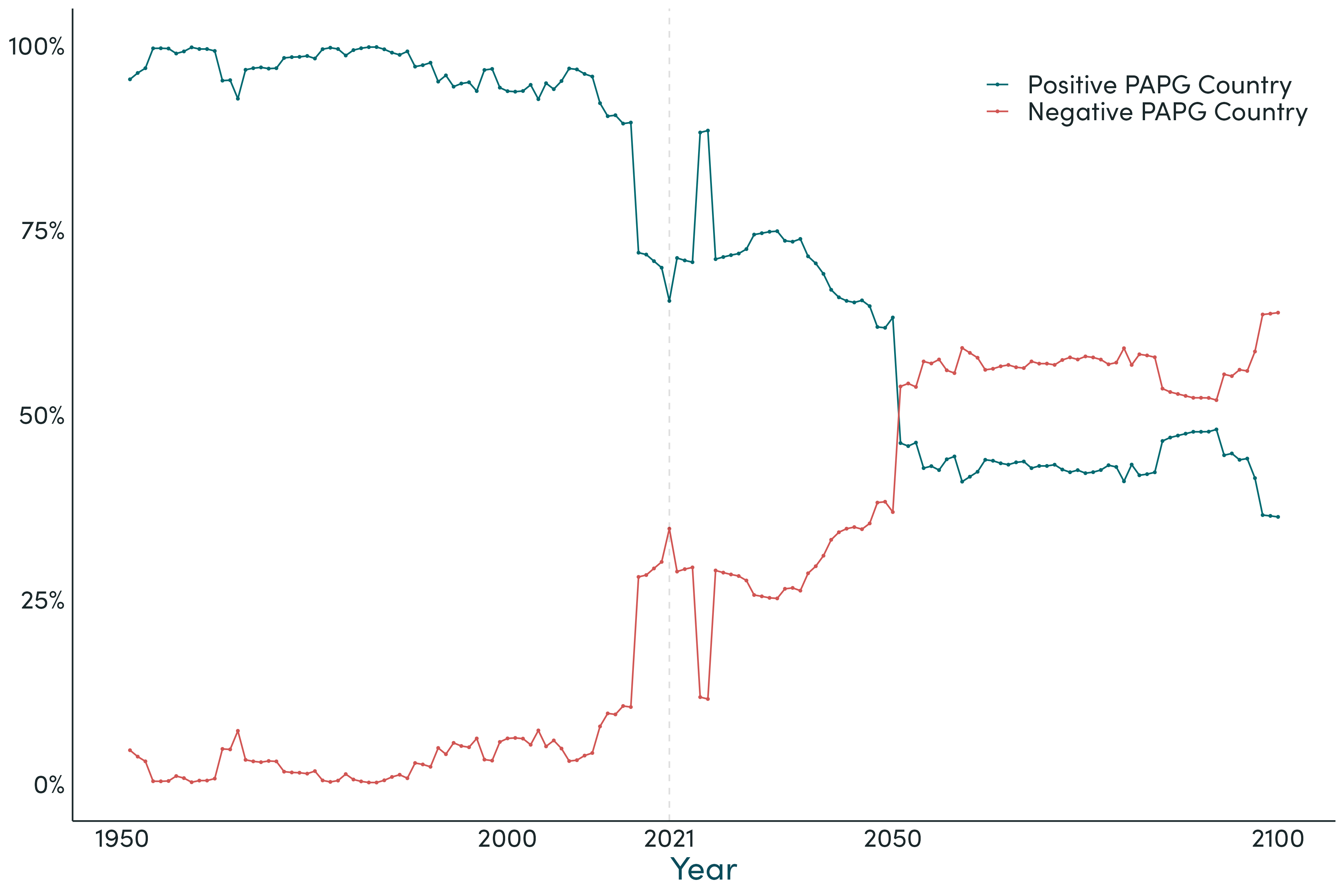

Figure 2: Proportion of world population in positive and negative working age population growth countries

Historical then UN projected, medium scenario.

The political response greatly exacerbated the problem...

These headwinds were in large part unavoidable. But the political reaction was both avoidable and irresponsible. A few countries including Germany, Canada and Australia responded to demographic challenges by actively recruiting potential migrants from low and lower middle income countries including India, Kenya and Nigeria-economies where the cohort ofyoung, educated workers was still expanding. But many aging economies took the opposite course. Led by a wave ofpoliticians who appealed to increasingly economically vulnerable retirees by promising law, or der and closed borders, these countries retreated toward autarky. Migrants replaced less than one quarter of the workforce lost to domestic demographicchange across Europe, and far less than that in East Asia.

In the name of industrial policy and national security, the EU and the US led the way in tearing down the authority and influenceof the World Trade Organization, raising tariffs on goods from steel through cars to solar panels and subsidizing inefficientdomestic industry that then struggled to find workers. Regulatory reforms designed to preserve existing firms and jobs in afragile economy further stifled high-productivity job creation and innovation. China continued its own subsidies but faced, if anything, an even greater challenge to find suitable employees. The result was far higher global prices and lower productivitygrowth.

Increasing geopolitical tensions, fanned by a successful lobbying effort by contractors, saw military spending rise. China's use of military spending as a Keynesian stimulus in the face of high savings simply made labor shortages in the productive part of theeconomy even worse.

Facing slower growth, greater military and subsidy spending, and rapidly rising financial obligations to retirees, all alongside higher costs of service provision, governments across Asia, Europe and North America slashed spending on education and safety nets for young and working age populations. This further eroded equality of opportunity and, combined with the constricted flow of migrants and less spending on research, exacerbated the decline in innovation and productivity growth.

The sclerotic countries of Europe saw a rapidly shrinking share of the global economy but, supported by the US (keen onretaining its veto power), they opposed any realignment of vote shares in the World Bank. That stymied negotiations overcapital increases at the institutions, so that the IBRD stagnated. Meanwhile, declining aid budgets increasingly spent athome left little for IDA replenishments. A similar dynamic at the IMF left the organization undersized to respond to financialcrises or take up new challenges including disaster relief.

Global private financial flows declined in the face of reduced savings and regulation-enhanced risk-aversion in aging countries alongside weak growth in emerging economies. Overall aid volumes stagnated over the long term, never passing the $200 billion mark. And the quality of ODA continued to decline as the OECD DAC club of donors allowed ever more domestic spending in donor countries to qualify as assistance. Actual finance reaching low- and middle-income countries declined, and finance reaching the world's poorest declined more rapidly. Donors diverted remaining resources to small subsidy of mitigation projects in favored middle income countries in a Potemkin approach toward meeting climate finance commitments. China's Beltand Road initiative collapsed as slow growth and high interest rates spread debt distress. A number of international aid-fundedinstitutions simply closed for lack of funding, including the vaccines alliance Gavi-the result was a resurgence of infectious diseases including malaria, which had been declining thanks to early vaccination efforts.

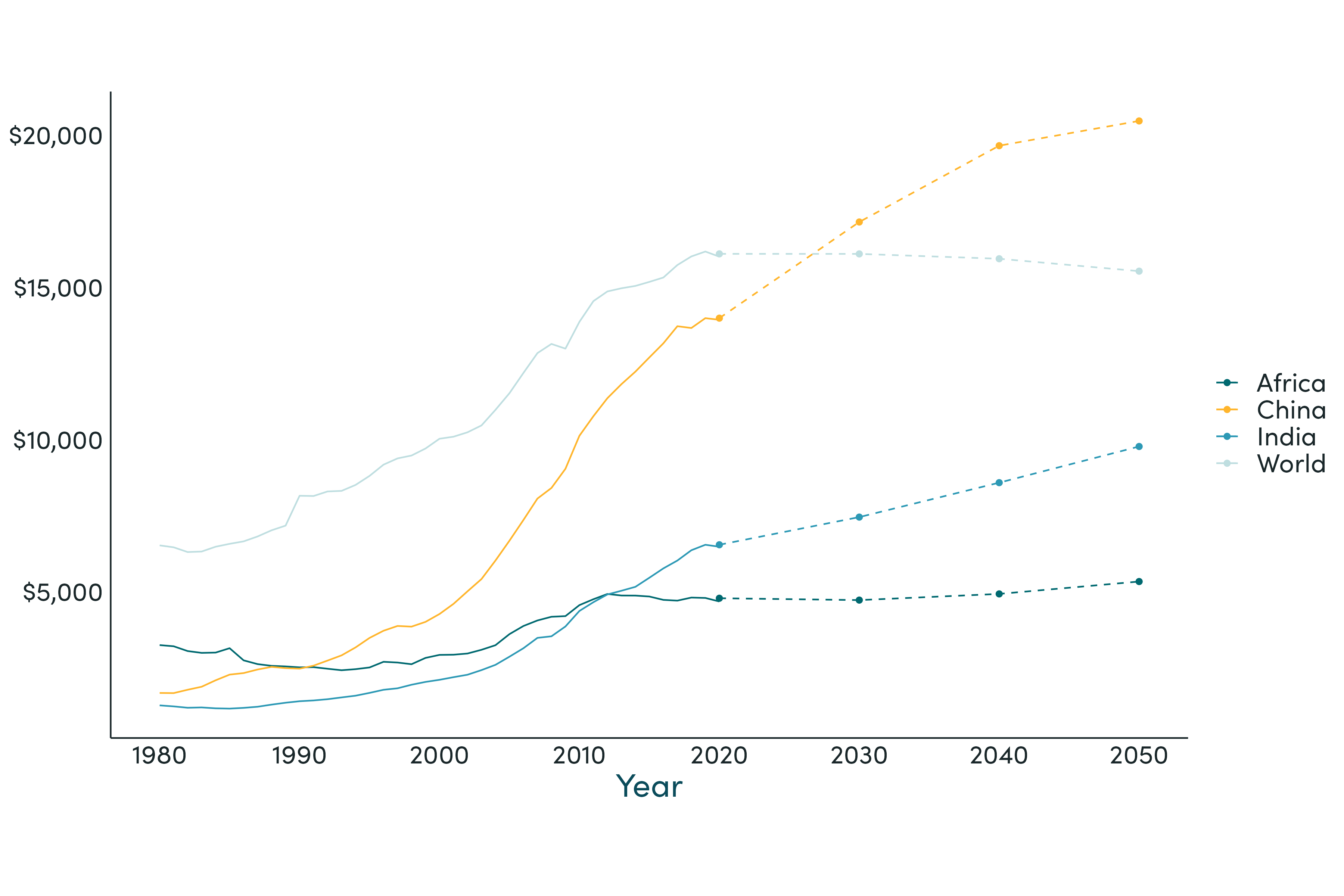

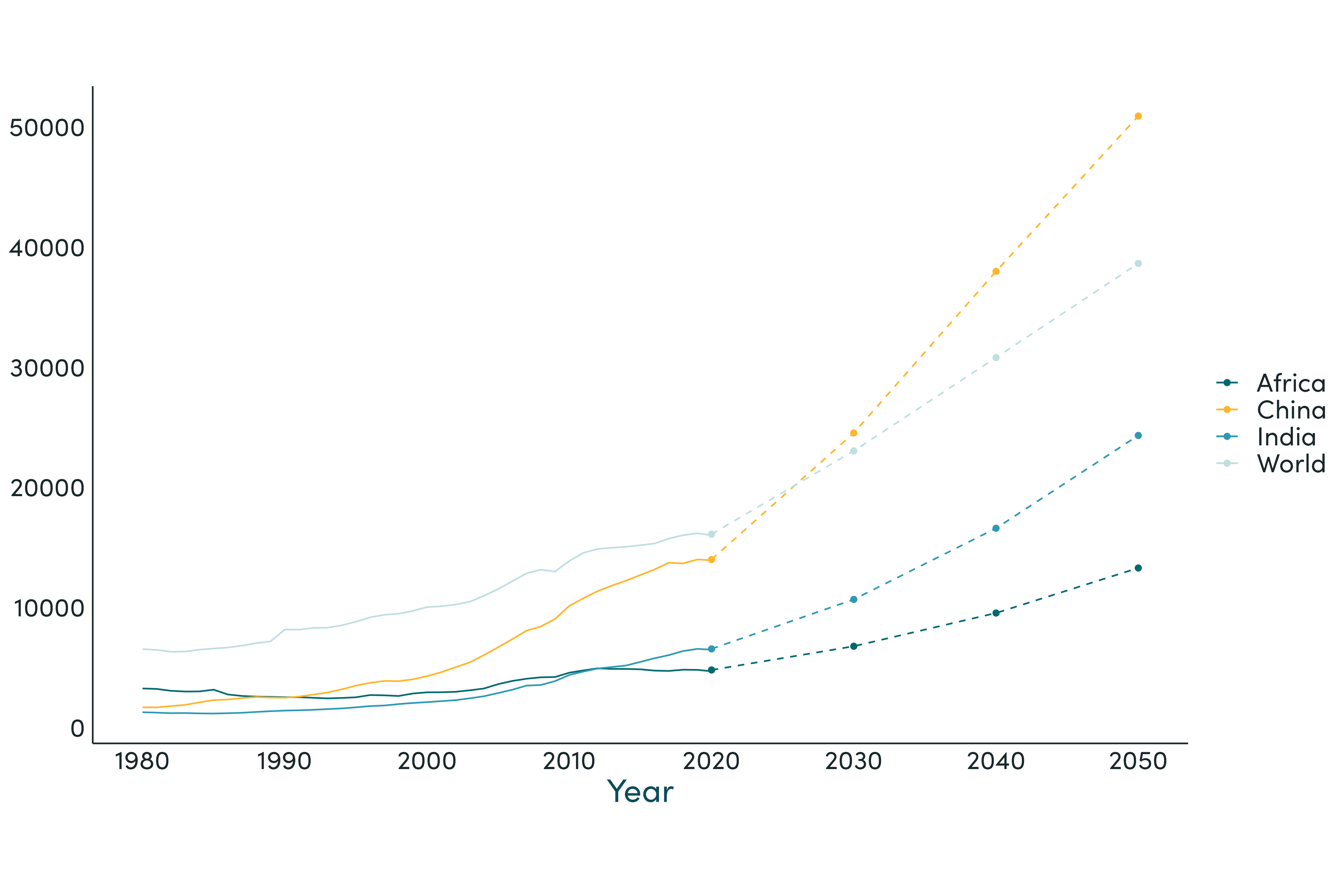

Figure 3: World, Africa, China and India GDP per capita (2017 USD)

Historical then KG negative scenario.

. . . And the result was stagnation, inequality and financial crisis.

China's financial crisis, brought on by the collapse in housing prices in the mid-2020s, pulled the country into a recession thatextended over nearly a decade. Policies to raise birth rates through two-earner tax penalties simply exacerbated labor shortages and productivity. The country was hardly alone. The US dollar remained the global reserve currency for lack of other options, but market volatility and a declining savings rate nonetheless fostered debt distress. In 2039, the UK introduced a health ration book system for the majority who could not afford 'voluntary payments' for treatment. This did not save the UK from its own financial crisis in 2046 as a number of pensions funds collapsed. Most other European countries did little better.

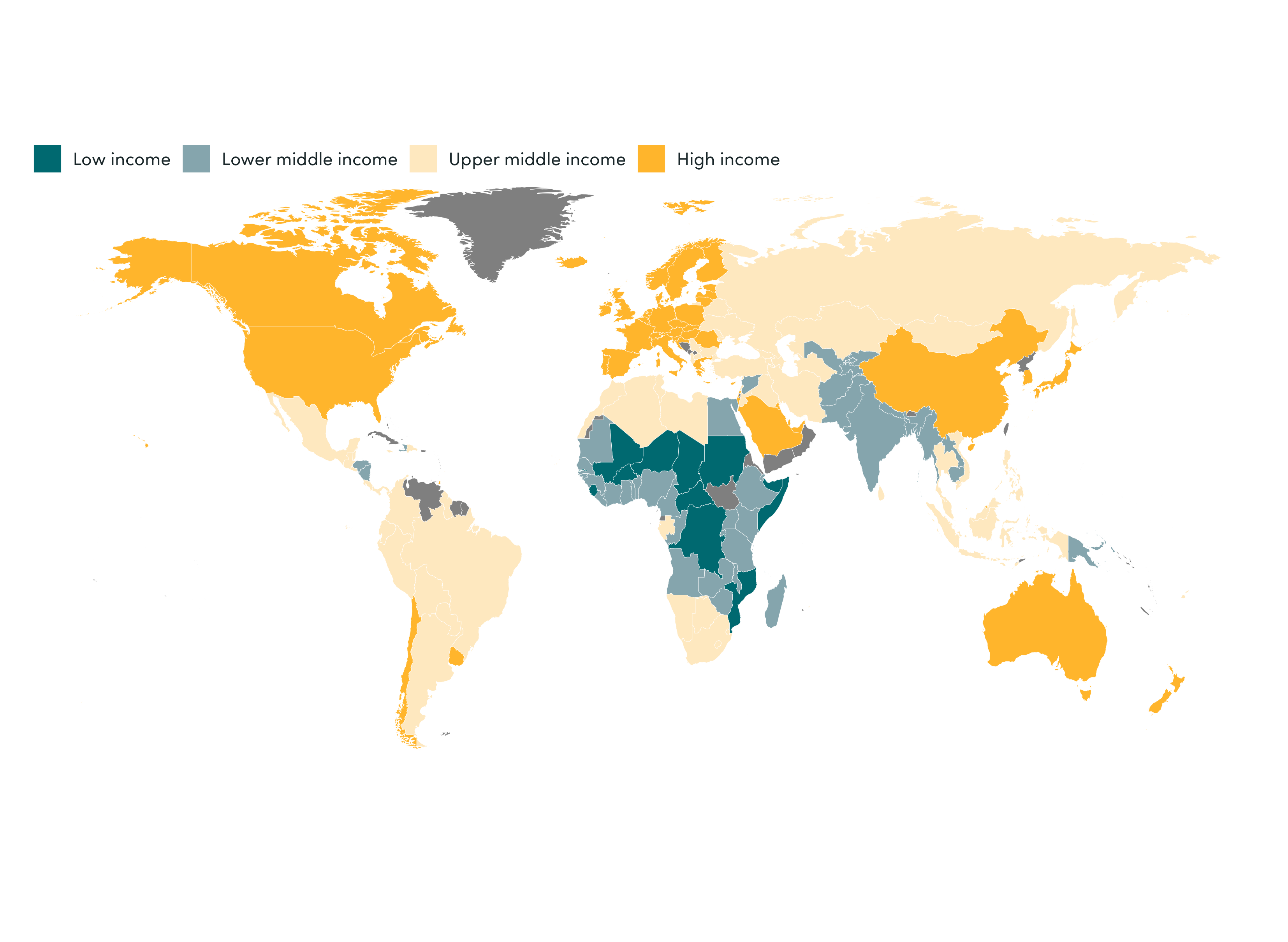

Global average income per capita growth was extremely low-below one percent a year over a thirty-year period. While global income convergence continued, it did so at a snail's pace. China did finally enter the ranks of the world's high-income countries in the late 2030s, but the proportion of the world's population living in low and lower middle-income countries remained almost unchanged-at about half of the population of the planet. A global map of countries by income categorization looked sadly similar to the same map from thirty years before.

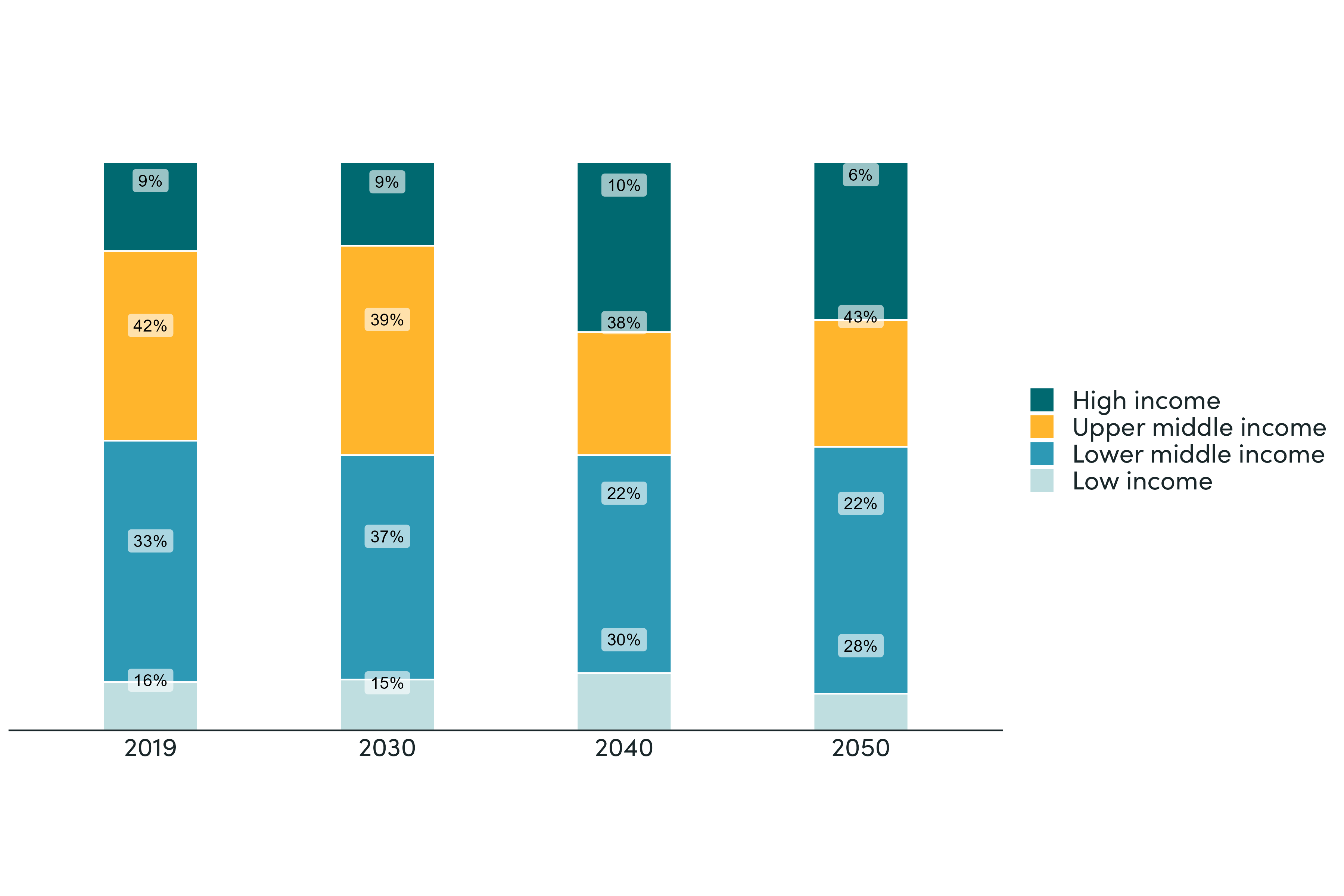

Figure 4: Percent of world population in each country income level

Historical then KG negative scenario.

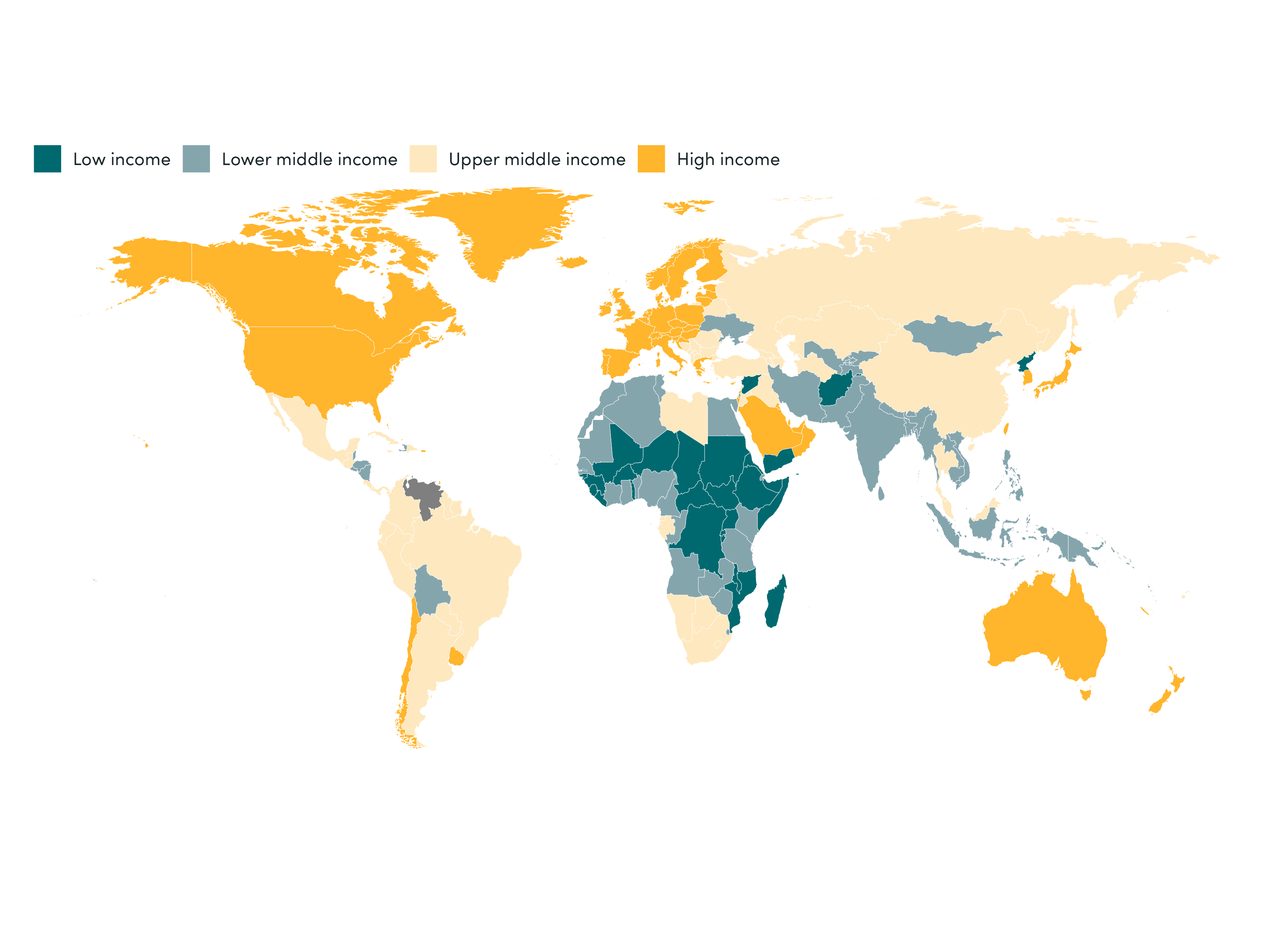

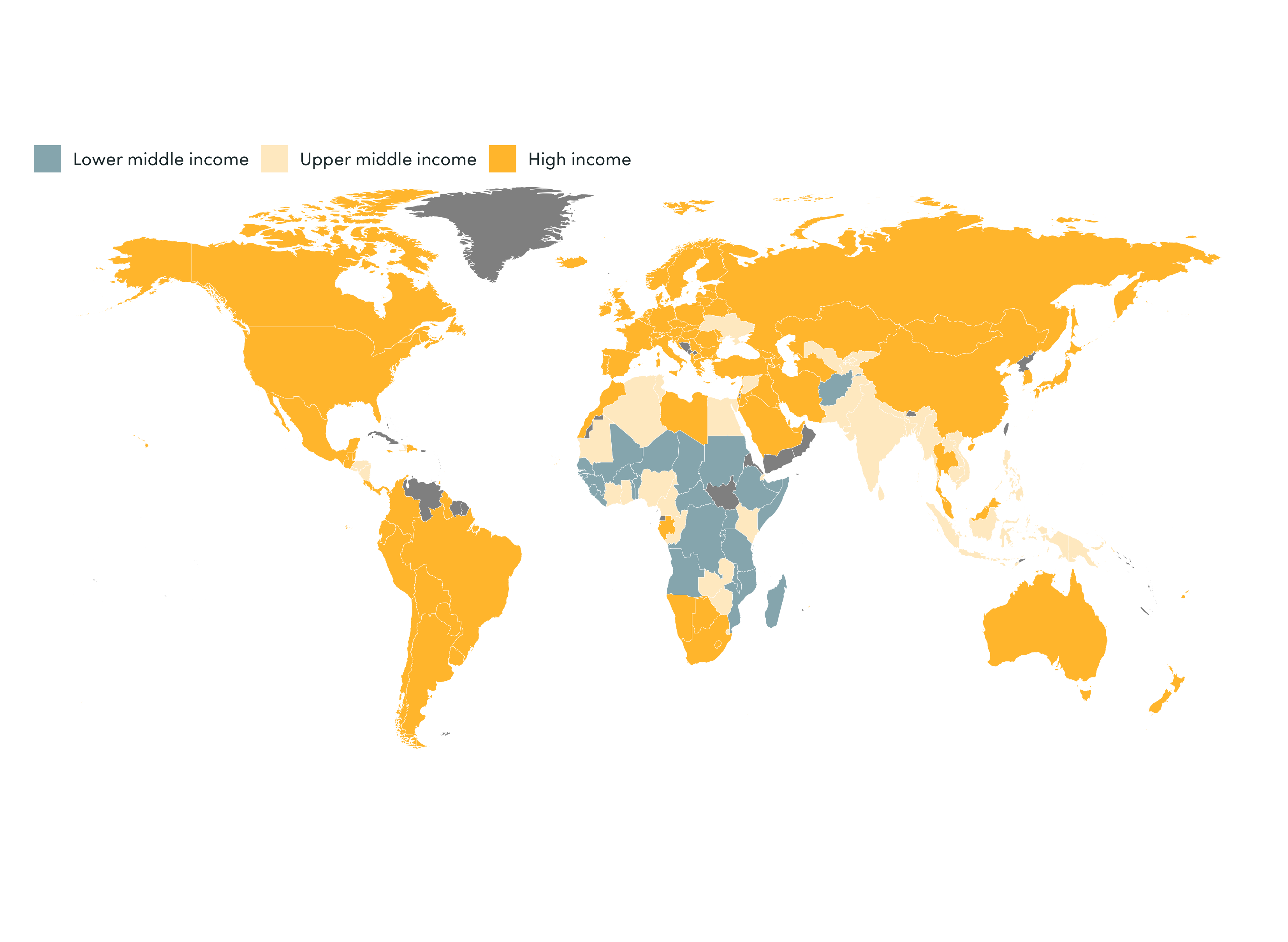

Figure 5: Country income levels, 2022

Figure 6: Country income levels, 2050

Negative scenario

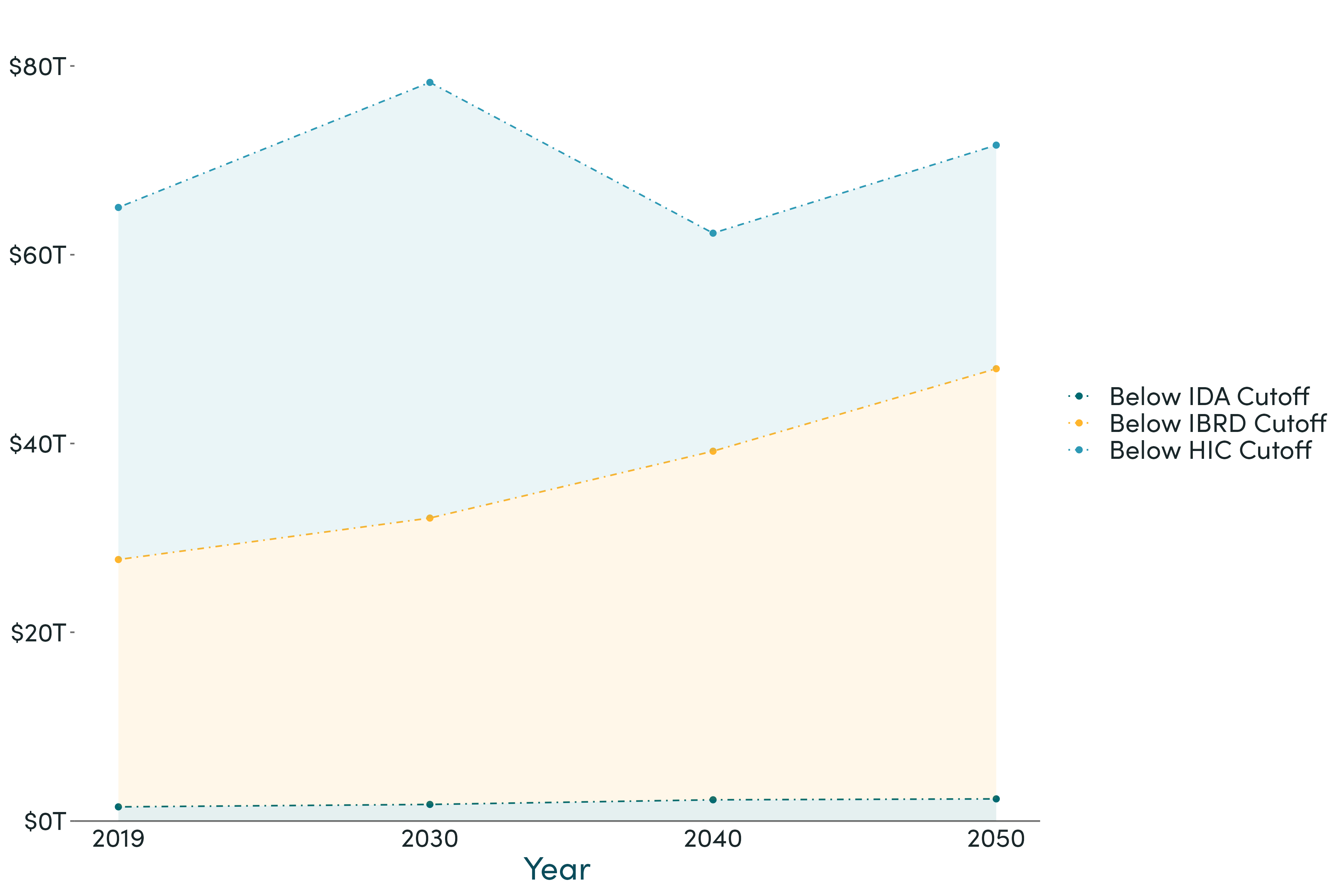

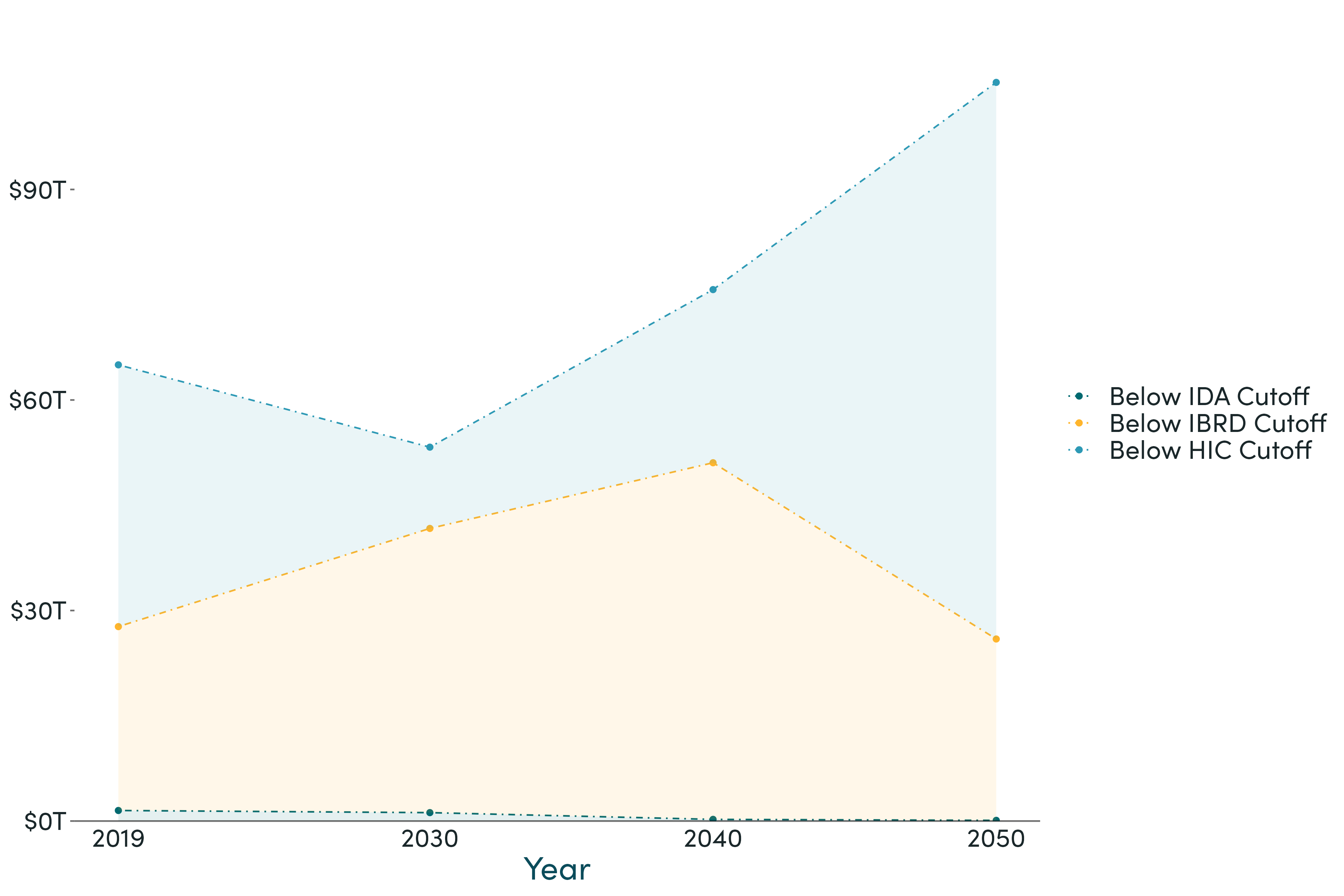

Figure 7: Total GDP of countries below each borrower tier cutoff

Negative scenario

Low and lower middle income countries suffered the worst.

Even with continued convergence built on a better demographic situation and catch-up technology adoption, the era of 'miracle'growth appeared at an end, and growth in developing countries as a whole was disappointingly weak. Manufacturing-led growth faced tariff barriers and lower demand from an aging planet. The absolute number of manufacturing jobs fellworldwide. In 1975, manufacturing employed 13 percent of the global workforce, this had climbed to 14 percent in 2018, butdropped below 10 percent by 2050. Despite increased autarky, the jobs that remained were still overwhelmingly concentrated in China. No new path opened up through migration or services exports because of ever-higher barriers to the movement ofpeople and the balkanization of digitally enabled trade driven by a patchwork of incompatible regulatory regimes thatemerged in North America, Europe, India and China.

While Sub Saharan Africa's dependency ratio declined and the region added many millions of increasingly educated school graduates to its working age population, there was nowhere for these new workers to go but the streets. The 'African Spring' ended as disappointingly as had the Arab Spring decades before, if anything reinforcing a trend toward kleptocratic rule. Demand for external assistance continued to expand as slow per capita growth combined with rising populations left a large pool of poor economies. By 2050, the GDP of IDA eligible countries as a group had climbed 60 percent, but declining replenishments reduced IDA flows by a similar amount. A similar story held for the World Bank, where the GDP of countries between theIDA and IBRD cutoff climbed 74 percent, but capital increases did not come close to keeping pace.

With reduced flows of remittances, investment and aid, low-income countries doubled down on resource exportsincluding fossil fuels as a source of revenues. The Democratic Republic of the Congo, for example, sold rights to all-comers to exploit reserves of copper cobalt, zinc and tin alongside extracting oil from its tar sands. Governance took a back seat, with the Extractive Industries Transparency Initiative suspending half of its members before funding for the institution was cut off.

Progress slowed on zero-carbon technologies: tariff wars on electric vehicles and solar panels raised global prices; a lackof panel and heat pump installers and construction workers raised installation costs in high income countries sufferingwidespread labor shortages: fiscal difficulties reduced installation subsidies; all in turn limited economies of scale andproductivity gains. Despite this, there was some good news. The 2020s marked 'peak fossil' as renewable sources increasingly dominated energy generation and the worse scenarios historically used by the IPCC for the potential extent of warmingremained off the table. In 20-50, the forecast for 2100 climate changes was an average of 2.5 degrees of warming.

At the same time, the considerable damage that rising temperatures had already caused by the 2020s in the Sahel region only worsened. Rural-urban migration to escape failing croplands without the financial capacity to support the rollout of even basicurban infrastructure services led to declining health outcomes and increased poverty for over 100 million people. Still more than one in five of the population of Africa lived on less than $2.15 a day-the long forgotten Sustainable Development Goals had targeted wiping out such poverty worldwide two decades before.

The proportion of those under ten dollars a day hardly shifted over three decades, and even increased in some countries: in the US the combination of a historically weak safety net, growing inequality and almost flatlined growth meant that the proportion ofthe country living on less than $10 increased from 2.25 percent to 3.25 percent. While the world as a whole still saw somecontinued progress in life expectancy and education levels, and we did avoid a major global conflict, the dream of a world free of poverty on a livable planet seemed far off.

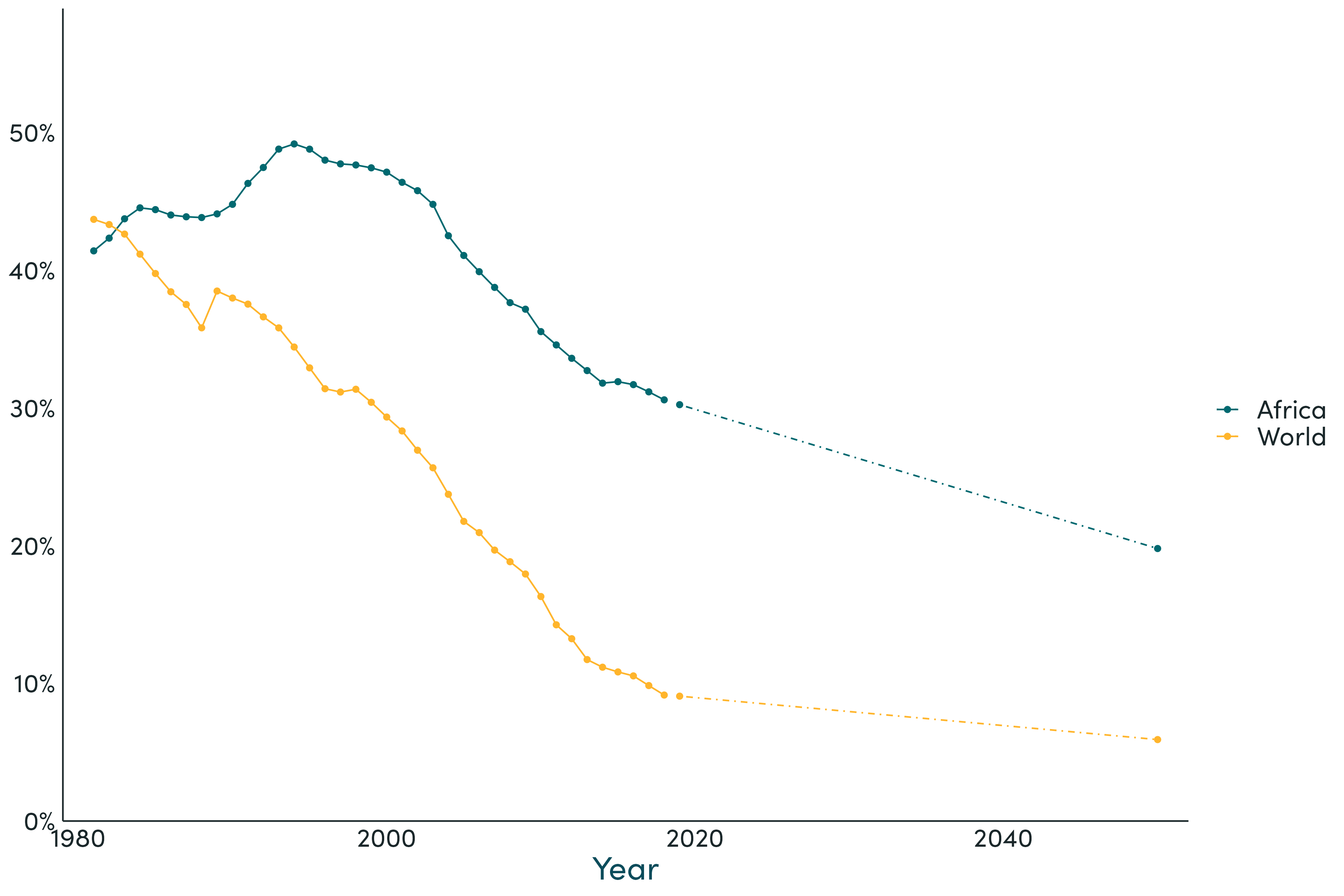

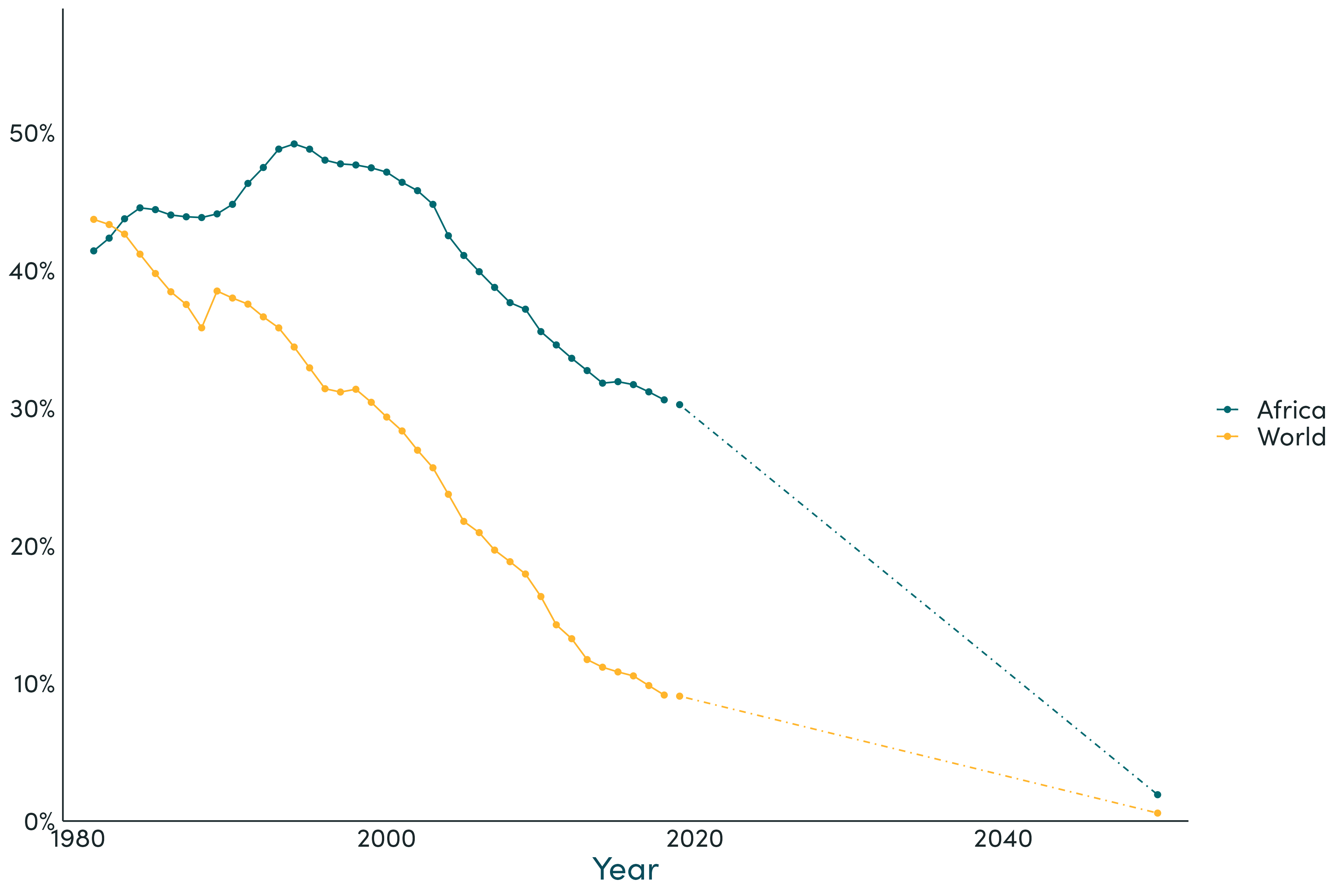

Figure 8: Percent of population living under $2.15/day

World Bank PIP, then negative scenario

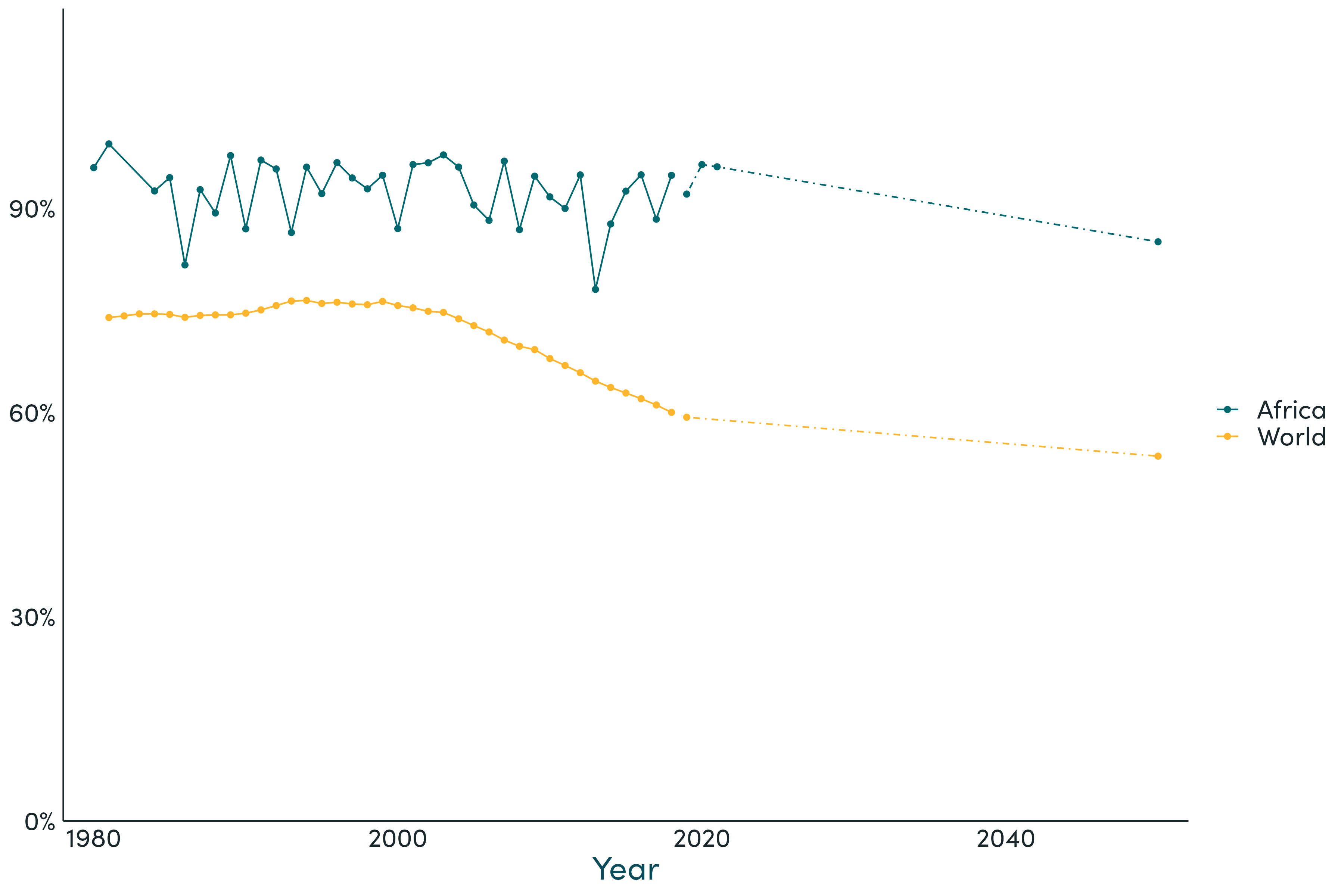

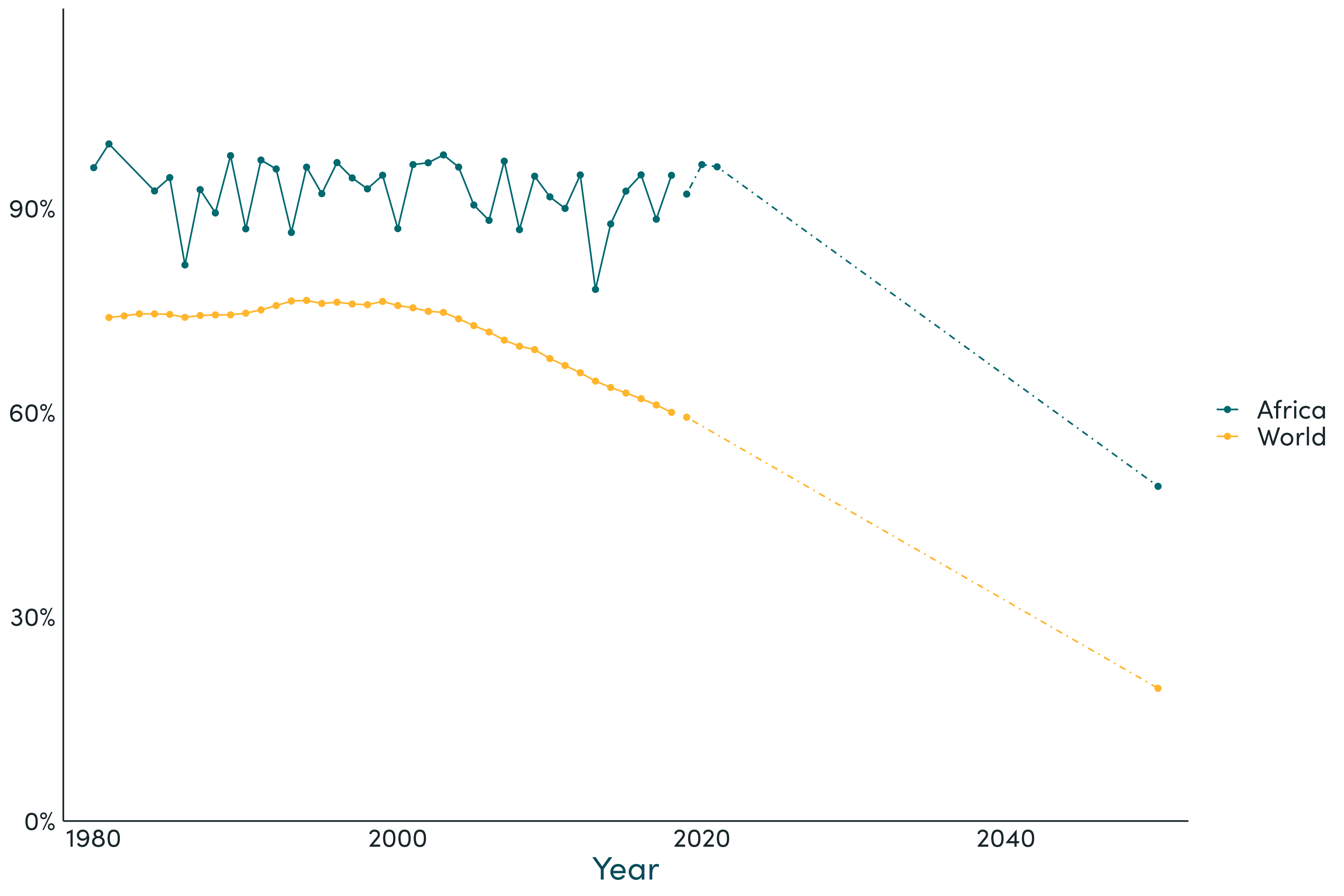

Figure 9: Percent of population living under $10/day

World Bank PIP, then negative scenario

2. Momentum regained

Recovering from the depths of the mid 2020s...

During the mid-2020s, the financial crisis engulfing China's banking and real estate sector deepened. In the US, pension funds that became heavily exposed to private equity following state-level deregulation foundered as the AI bubble burst. The combination drove the global economy into a deep recession, and the short-term reaction made things worse. China threatened to withdraw from the IMF and World Bank, blaming its under-representation for what it saw as the inadequacy of the IMF response to the crisis. The World Trade Organization lost all credibility as a rules enforcing body as the US, China and the EU all blatantly flouted agreements on tariffs and subsidies. But the world turned back from the brink. A series of elections removed failing populists from power while China's 21st Party Congress opted for new leadership. 2030 ushered in a two decade period of cooperative global reform.

. . . Policies tacked against the headwinds

These reformers faced headwinds including aging populations across Europe, much of Asia and the Americas alongside the challenge of low productivity growth in a growing global services sector. But they rose to the challenge. Not least, Europe as a whole followed Germany's early lead and embraced immigration as a response to the jobs and innovation challenges theyfaced. The EU signed skills partnership agreements with countries including India, Kenya and Nigeria to help trainhundreds of thousands of workers in skills from solar panel installation to nursing and home care help, and provide migration pathways for some of the trainees. It also invested in systems of community support to assist both new arrivals and locals inaccessing housing, health, education and other services in areas where migrants settled. The US finally reformed its visa and migration regime and joined what was becoming a heated global competition for talent. Between 2020 and 2050 the proportion of the global population who were migrants climbed from 3.6 percent to 7.5 percent, or from 292 to 735 million people.

In the US, migrants became responsible for nearly half of all patenting (up from about 25 percent in 2020) and a similar proportion of new business startups. Across innovating countries, greater gender, racial and income equality in access to the resources required to innovate, underpinned by revamped safety net and social services, helped spur a new golden age of invention covering areas from fusion through cancer vaccines to robotics. This was backed by considerable global research and development spending. As a proportion of global GDP, research and development expenditure increased from 2.0 to 2.7 percent between 2010 and 2020, and by 2050 it had increased to 4.0 percent. In absolute terms, global research spending was five-fold larger in 2050 than in 2020. Amongst other innovations, zero carbon technologies covering cement and steel manufacturing alongside energy production rapidly became the cheapest option for producers, accelerating progress toward net zero targets. In Europe and the US, a newfound confidence in progress was associated with reduced nuisance regulation in areas from planning and housing through licensing and permitting. Not least this reversed a long-term decline in both startups and internalmigration.

For China there was simply an insufficient supply of migrants willing to move to the country to come anywhere close tomatching the 160 million-strong implosion of local-born workers, let alone the 384 million migrants it would have takento keep dependency ratios at their 2020 level. But the government introduced generous parental leave and free child care forchildren eighteen months and up. Alongside increasing birth rates, this further reduced the country's eleven percentage point gendergap in labor force participation. Similar policies across much of East Asia and Eastern and Southern Europe helped bolster both fertility rates and economic growth.

Global negotiation around a WTO agreement on services and regulation of travel led to a significant reduction in the barriersboth to the movement of people and to cross-border provision of services: global common standards around regulation of digital commerce, taxation of online and virtual sales, most favored nation rules around visa costs and visa-free travel, andharmonization of services regulation. As a result, an increasing proportion of 'anywhere jobs', which made up about a quarter of employment in OECD countries in the 2020s, were filled by employees in other countries. Even though growth slowed from its rate of 8 percent per year in the first two decades of the 21st Century, global trade in digital services, worth more than 3trillionin2020, toppedl5 trillion by 2050.

Greater global stability was associated with a resumption of the post Cold War decline in military spending and the expansion of regional integration. The EU added new members in Central Europe and the Middle East as well as Morocco. The US, Canadaand Mexico agreed a single market even as a trans-pacific trade and skills partnership significantly lower barriers to the movement of goods, services and people between the Americas and East Asia.

In 2048, the IMF headquarters moved to Beijing. China, as the largest shareholder, exercised the right to host the institution.The victory was somewhat hollow. Thanks to international agreements on banking regulations that had broken up banks too big to fail as well as strong global growth, commodity price stability and better debt management under stable, low globalinterest rates fed by a developing country savings boom, there was little for the institution's shrinking staff to do.

The World Bank remained in Washington DC thanks to a change in shareholding rules. Rounds of voting reform includedcombining IBRD and IDA vote formulae so that larger IDA donors had a larger share in World Bank Group decision making.But even with these adjustments, by 2050, the US veto was gone and the EU and US combined vote share had dropped from 39 percent to 25 percent. New high income countries including China and Brazil considerably increased both their donations to IDAand their vote shares, although no country gained veto power. More importantly, a succession of capital increases and generous IDA replenishments left the institution capable of playing a far greater role, supporting a global social safety net alongsidepreservation of global public goods from climate through pandemic preparedness.

The system of monitoring both aid (ODA) and climate finance underwent considerable reform under the auspices of a newUnited Nations agency tasked with better measuring both finance for international development and global public good finance. Not only did the quality of aid improve, but volumes rapidly increased both thanks to the generosity of traditional donors but also engagement by 'new' donors including China and Brazil. Flows reached a trillion dollars a year, up from $162 billion in 2019.

. . . And the result was growth.

Global GDP per capita considerably more than doubled in the thirty year period 2020-50, a slightly faster rate of growth thanmanaged over the previous thirty years. China's average income in 2050, at $50,000 easily surpassed the level of the EU from thirty years prior (by 2050, the EU's average income had reached close to $100,000). Africa's average income per headclimbed from $4,800 to $13,300. By 2050, there were no countries left that met the definition of 'low income' and 85 percent of the world lived in upper middle or high income countries, up from around fifty percent in 2019. The global map of countries by income category changed markedly, not least nearly all of the Americas as well as Eurasia North of the Himalayas reachedhigh income status.

Figure 10. World, Africa, China and India GDP per capita (2017 USD)

Historical then KG positive scenario.

Agriculture and industry (including mining, manufacturing, utilities and construction) accounted for 74 percent of the globalworkforce in 1975. By 2050 that was closer to 43 percent. But the idea that a global services-based economy was destined to be low-growth was disproved, or at least delayed. Some low and lower-middle income countries did benefit from the rapidrealization in richer countries including China and the US that young workers in really didn't want the manufacturing jobs governments were trying to preserve. Factories moved to Africa and factory employees moved from Africa to Europe and theUS. But the global number of manufacturing jobs continued to decline nonetheless, and the widest path to rapid growthpermanently switched from investment in the physical capital of manufacturing to the human capital required for migration and services exports.

In particular, under business as usual, demand for immigrants rapidly exceeded demand to emigrate worldwide -and so businessas usual changed. Aging countries had to offer training, better conditions, easier processing, and more pay in the global competition for workers. That all considerably boosted remittance flows, investment and trade revenues. Annual global remittance flows climbed from $650 billion in the early 2020s to $5 trillion by 2050. Temporary migration and services trade also blossomed, creating hundreds of millions of service-based export jobs by 2050.

The absolute number of people living on $2.15 or less a day peaked in the 1970s at around 1.9 billion. The number living on $10or less a day peaked in 2009 (at about 4.8 billion people). By 2050, at least under the low-bar definition of three decadespreviously, 'extreme' poverty was limited to a few households for short periods in the very poorest countries. The proportion of African people living on less than $10 a day fell from nine in ten to under one half. In India it fell from nine out of ten totwo in ten over the same period. The proportion of the global population living on less than $10 a day fell from three fifths in 2020 to one fifth, leading to global development campaigners to call for the 'ten dollar promise'-an international commitmentbacked up by a global digital finance-based safety net to ensure all people everywhere lived above that line.

Figure 11: Country income levels, 2050

Positive scenario

Figure 12: Percent of population living under $2.15/day

World Bank PIP, then positive scenario.

The countries of the Sahel were a significant exception to a global story of rapid progress. Despite successful climate mitigation due to technology advance and global financing, these economies and their neighbors were already suffering considerably loweryields from locked in climate change of the first half of the Twenty-First Century. A subset highly reliant on fossil fuel exports for revenues including Chad, Sudan and Yemen were doubly hit by climate impact and rapidly dwindling demand for high-carbon fuels.

Strong growth in most IDA countries saw the total size of eligible economies under the IDA cutoff fall from $1.5 trillion in 2019to $1.2 trillion in 2030 and below $100 billion in 2050. Alongside allowing considerably more generous support to the poorest countries including in the Sahel, this allowed for a combination of raising the IDA threshold and diverting some resources to thesubsidy of global public goods and payments to end poverty. (The IBRD borrower pool grew in the short term, but as countriesgraduated it, too, began to shrink by 2050).

The global area dedicated to agricultural land continued to decline thanks to increasing farm productivity especially in SouthernAfrica and Latin America. More land and sea areas were put under conservation protection. Nonetheless, climate change andcontinued exploitation meant that biodiversity loss continued at high rates. Despite low-cost desalinization and advances in drought resistant crop varieties, many regions that had previously relied on aquifer supplies to supplement production had to change output to lower-value, less water-intensive cropping. And nitrogen and phosphorous pollution continued to significantly disrupt local ecologies worldwide. Along with continued progress toward a universal high quality of life, long-term planetarysustainability remained a challenge for the generation after 2050.

Figure 13: Percent of population living under $10/day

World Bank PIP, then KG positive scenario.

Figure 14: Total GDP of countries below each borrower tier cutoff

Positive scenario.

References

Adom, Philip Kofi (2024). The Socioeconomic Impact of Climate Change in Developing Countries in the Next Decades: A Review. Working Paper. Center for Global Development.

Fosu, Augustin Kwasi and Dede Woade Gafa (Nov. 2023). The Future of Natural Resources and Development: Whither Low and Middle-Income Countries? Working Paper 664. Center for Global Development. https://www.cgdev.org/publication/future-natural-resources-and-development-whither-low-and-middle-income-countries.

Kenny, Charles (Sept. 20, 2021). Global Mobility: Confronting A World Workforce Imbalance. CGD Note. Center for Global Development. https://www.cgdev.org/publication/global-mobility-confronting-world-workforce-imbalance.

— (Oct. 30, 2023). The Future of Global Development and Implications for Aid. Speech.

Kenny, Charles and Zack Gehan (Mar. 6, 2023). Scenarios for Future Global Growth to 2050. Working Paper 634. Center for Global Development. https://www.cgdev.org/publication/scenarios-future-global-growth-2050

Kenny, Charles and George Yang (June 14, 2021). Can Africa Help Europe Avoid Its Looming Aging Crisis? Working Paper 584. Center for Global Development. https://www.cgdev.org/publication/can-africa-help-europe-avoid-looming-aging-crisis.

— (2024). The Implications of a Declining Labor Force. Working Paper. Center for Global Development.

Poverty Calculator (2023). https://pip.worldbank.org/poverty-calculator. (visited on 12/19/2023).

Webster, Brian, Charles Kenny, and Ranil Dissanayake (Oct. 30, 2023). Is Manufacturing Destiny? On the Dynamics of Future Sectoral Shares and Development. Working Paper 662. Center for Global Development. https://www.cgdev.org/publication/manufacturing-destiny-dynamics-future-sectoral-shares-and-development

Topics

CITATION

Kenny, Charles, and Zack Gehan. 2024. Two Futures for Global Development. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.