With Russia’s attack on Ukraine raging and most of the world imposing severe financial sanctions on Russia, attention has turned to whether Russia could use its allocation of special drawing rights (SDRs) to bolster its foreign reserves and finance its war effort. The answer is yes, in principle, but no in practice. We explain why.

What has happened so far?

SDRs account for 4 percent of Russian reserves (SDR 17,301 million), however considering the current situation where 55 percent of its reserves are unusable because of sanctions, these SDRs (valued at about $24 billion) might come in handy.

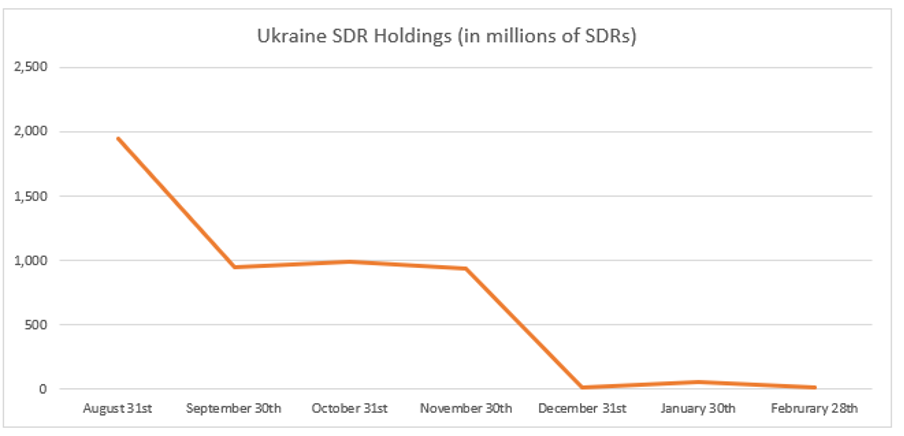

As of the 28th of February, Russia has not touched its SDR holdings since the new SDR allocation of August 2021 (although its holdings are slightly less than its allocation, indicating some use in the past (figure 1). However, Ukraine, depleted about half its SDRs in September and used most of the remainder in November (figure 2).

Figure 1; Source: IMF

Figure 2; Source: IMF

So how would Russia use its SDRs?

To exchange SDRs, Russia would have to either find another government willing to enter into an agreement with them (highly unlikely) or request a conversion using the voluntary trading arrangements (VTAs) established with the Fund, which we explain here.

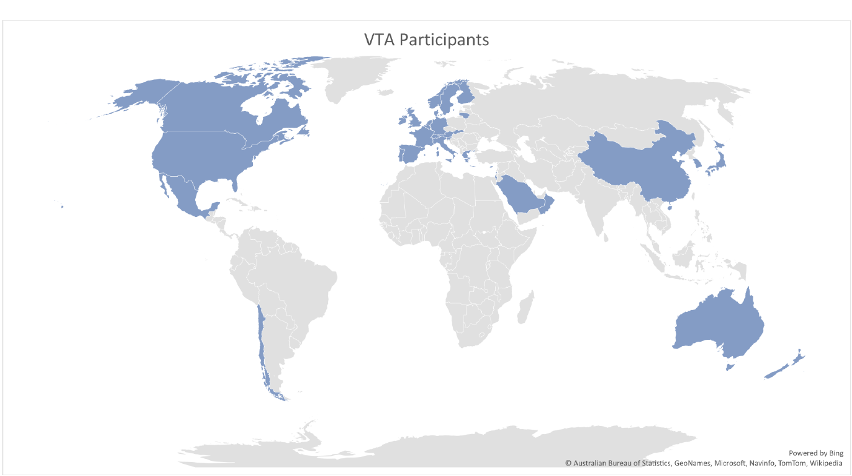

However, these VTAs are just that—voluntary. For Russia to exchange its SDRs against dollars or other hard currencies, there would have to be willing parties for this transaction, which, considering the present geopolitical situation, seems unlikely. Most VTA participants (with the exception of Saudi Arabia, Oman, and China) have condemned Russia’s invasion of Ukraine. And many large VTA participants have also banned transactions with the Central Bank of Russia—the counterparty in any such SDR conversion (figures 3 and 4).

Map 1; Source: Statista 2022

Map 2; Source: IMF SDR Annual Operations Trade report

It is also important to note that large conversions for Russia’s SDRs could not take place under the radar. As we have noted elsewhere, it is often hard to trace SDR transactions, and steps are needed to provide greater transparency. But conversion of Russia’s holdings of SDR 17.3 bn would be by far the largest single SDR transaction to date—about a third larger than the total decline in SDR holdings by all low- and middle-income countries between August 2020 and January 2022. Thus, the resulting changes in SDR holdings (routinely reported by the IMF at end month) would likely make it obvious which country or small number of countries had stepped in to convert Russia’s SDRs. Conversion of Russia’s SDRs would thus be a very public demonstration of support for Russia, and one likely to provoke near global opprobrium.

Could Russia use IMF rules to force other countries to exchange its SDRs?

This is where it gets blurry… Article XIX “Operations and Transactions in Special Drawing Rights” of the Articles of Agreements of the IMF states that each member country has an obligation to provide currency, if another country presents a balance-of-payment need (such as Russia currently).

In this vein, if voluntary transactions are not able to meet the requirements of a country with a balance-of-payment need, the Fund is expected to designate participants to provide currency (“The Designation Mechanism”). Countries are designated if their reserve positions are sufficiently strong. The normal procedure would be to include in the designation plan all the countries (currently 51) whose external positions are strong enough for them to be included in the IMF’s Financial Transactions Plan which is used to fund the IMF’s non-concessional lending from its General Resources Account. The rules governing for operation of the designation plan (Schedule F of the Articles) imply that countries with larger reserve positions and SDR holding would be called upon to convert more SDRs. Thus, the designation plan would appear to “mandate” large exchanges of SDRs by the very countries that would not expect to enter voluntary trades with Russia.

If a designated country refuses to fulfil its obligation, it will not be able to use its SDRs for other purposes “unless the Fund otherwise decides”. Since the final decision to sanction countries not meeting their obligations under the designation plan will come from the Fund (Article XXIII, Section 2)—i.e., a decision of the Fund’s membership—it would be very hard to imagine the EU and the US for example voting to ban themselves or other countries from using their own SDRs.

If (hypothetically) some went along with the designation plan, with major economies not participating, they would likely cover only a fraction of the full amount of Russia’s SDRs. In these circumstances—and with the large shareholders able to block any sanction for noncompliance with the designation plan—it seems very unlikely that the designation mechanism could be used to force conversion of Russia’s SDRs.

It is also hard to conceive of the IMF taking this route and activating the designation mechanism in these circumstances. Since the designation mechanism is the backstop that ensures the liquidity—and the reserve asset status—of the SDR, the failure to activate the mechanism might be seen as undermining the essential character of the SDR. But in present circumstances, it would only be the liquidity of Russia’s SDRs that would be called into question.

The bottom line

The IMF is in a delicate position. Russia is a sovereign country, a member of the IMF, with a recognised government. It would thus be hard for the IMF to justify blocking its assets. But on the other hand, so is Ukraine. Blocking Russian’s assets would mean supporting the Western sanctions but allowing Russia to draw on this capital would mean financing a globally condemned war.

Legally, all Russia would have to do is declare a balance-of-payment need to activate the designation mechanism for its SDRs, hope for a country to support them, and have access to its reserve tranche position. But this is unlikely to lead to any substantive exchange of foreign currency for Russia’s SDRs.

What happens next is uncertain, but it would certainly help if the IMF were more transparent about SDR transactions. If VTA exchanges were reported and SDRs movements easily trackable, it would allow the world to see clearly how SDRs were being used to support or to block Russia in its war against Ukraine. Lack of transparency just fuels harmful speculation and mistruths become facts.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.