Recommended

REPORT

The Future of Global Health Procurement

In October 2020, the Center for Global Development—in partnership with African Union Development Agency-NEPAD (AUDA-NEPAD), UN Economic Commission for Africa (UNECA), and the African Leaders Malaria Alliance—hosted a high-level roundtable on regional health product manufacturing in Africa. The event brought together a group of multilateral and national policymakers, global procurement agents, development finance institutions, pharmaceutical manufacturers, and thought leaders to advance the dialogue and align on significant barriers and practical solutions. This blog is based on the authors’ reflections of the roundtable. A summary of the discussion can be found here.

Converging economic, technical, and political factors—made all the more relevant by COVID-19—have increased the urgency to explore regional manufacturing of pharmaceuticals and other health products in Africa. High-level political interest due to the pandemic, combined with launch of the African Continental Free Trade Agreement (AfCFTA), offer a unique window of opportunity to accelerate progress. Health product manufacturing across the continent could help to both mitigate future supply chain disruptions and build more resilient and sustainable systems with improved access to medicines and other health products around the world. (Although some of the issues we discuss here may be relevant to vaccines, including vaccines for COVID-19, vaccine manufacturing involves many nuanced considerations not captured here.)

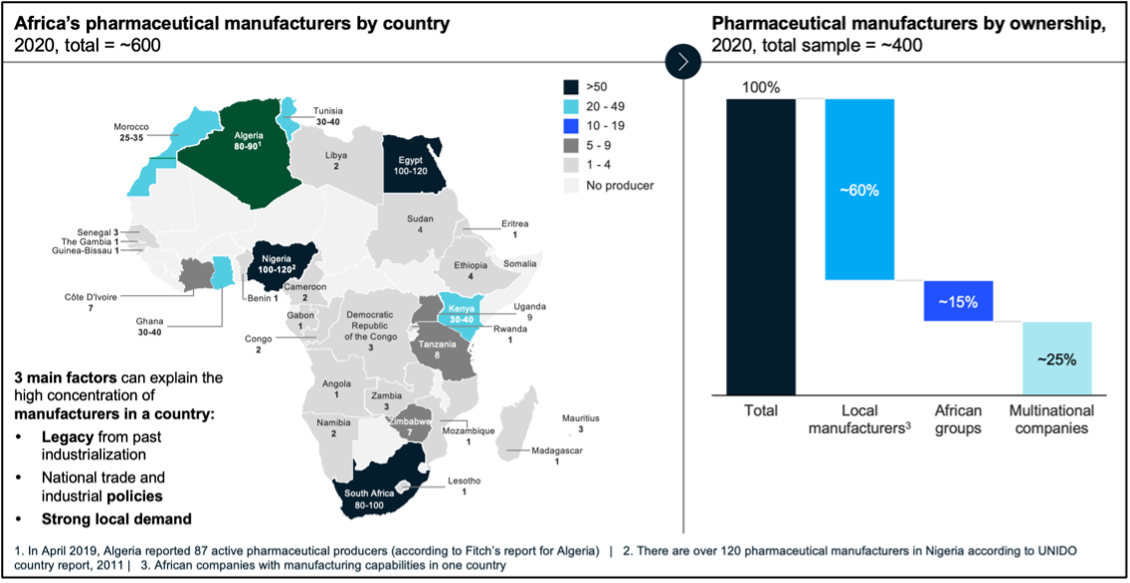

This agenda continues to face numerous supply and demand-side bottlenecks. In 2020, there were approximately 600 pharmaceutical manufacturers in Africa, 80 percent of which were concentrated in eight countries (see Figure 1). Only four countries had more than 50 manufacturers, while 22 countries had no local production.

Figure 1. Snapshot of pharmaceutical manufacturers by country and ownership, 2020

Source: Fitch, Capita IQ, UNIDO, press releases, company websites

Existing and prior efforts led by UNECA, AUDA-NEPAD, Africa CDC, UNICEF, and others in the region have focused on understanding relevant opportunities and challenges, and strengthening the enabling environment at the country, subregional, and continental levels. For example, the African Medicines Regulatory Harmonisation (AMRH) initiative, led by AUDA-NEPAD, works to expand access to quality medicines by enhancing the regulatory environment for pharmaceutical sector development with increased incentives for manufacturers to register their products. And the Africa Medical Supplies Platform (AMSP), launched by the Africa CDC, African Union, UNECA, and Afreximbank, creates a centralized digital system to help streamline medical supply chains and consolidate purchasing. Other efforts include UNICEF and WFP sourcing ready-to-use therapeutic foods for nutrition programs from local suppliers and large-scale production of long-lasting insecticide-treated nets in Tanzania by A to Z Textiles.

Building on the October 2020 roundtable discussion and drawing from the final report of CGD’s Working Group on the Future of Global Health Procurement, we outline some of the most critical challenges and proposed next steps for health product manufacturing in Africa below.

Supply-side difficulties range from limited working capital to misaligned regulatory incentives

On the supply side, roundtable participants surfaced several administrative, regulatory, and legal challenges. For example, import restrictions and tariffs on raw materials, ingredients, and manufacturing equipment put Africa-based manufacturers at a disadvantage. Burdensome local purchasing requirements, such as rules around cash flow and local currency for tenders, create barriers to entry and limit competition, especially for quality-assured generics. Infrastructure and labor challenges, the lack of availability of APIs and other key materials, and the cost-competitiveness of certain product categories compared to other regions of the world present additional issues with reaching economies of scale.

While regulatory harmonization has progressed in the East African Community, barriers to an expanded product registration framework remain. National regulatory agencies depend on revenue from dossier approval and expedited waivers requested by purchasers, creating financial disincentives for a streamlined and harmonized product registration process. At the global level, when procurement agents operate with inflexible governance arrangements (e.g., mismatched budgeting cycles), some countries are not able to mobilize resources in time to participate in tenders and thus miss out on subsidized prices.

In addition to a lack of fixed capital to set up manufacturing at scale, the limited availability and high cost of working capital when raised in emerging markets are also noteworthy obstacles.

Demand-side obstacles stem from inefficient procurement policies

On the demand side, market fragmentation—characterized by unorganized demand and high transaction costs—hampers the competitiveness of regional manufacturing. Further, weak regulatory regimes often lead to purchasing decisions driven by individual perceptions of quality; customers then pay more for international branded generics as a proxy for quality.

Participants also recognized that high levels of out-of-pocket spending on healthcare are not conducive to the long-term sustainability of regional manufacturing; well-developed national health insurance and financing systems can help pave the way for a more mature pharmaceutical manufacturing market.

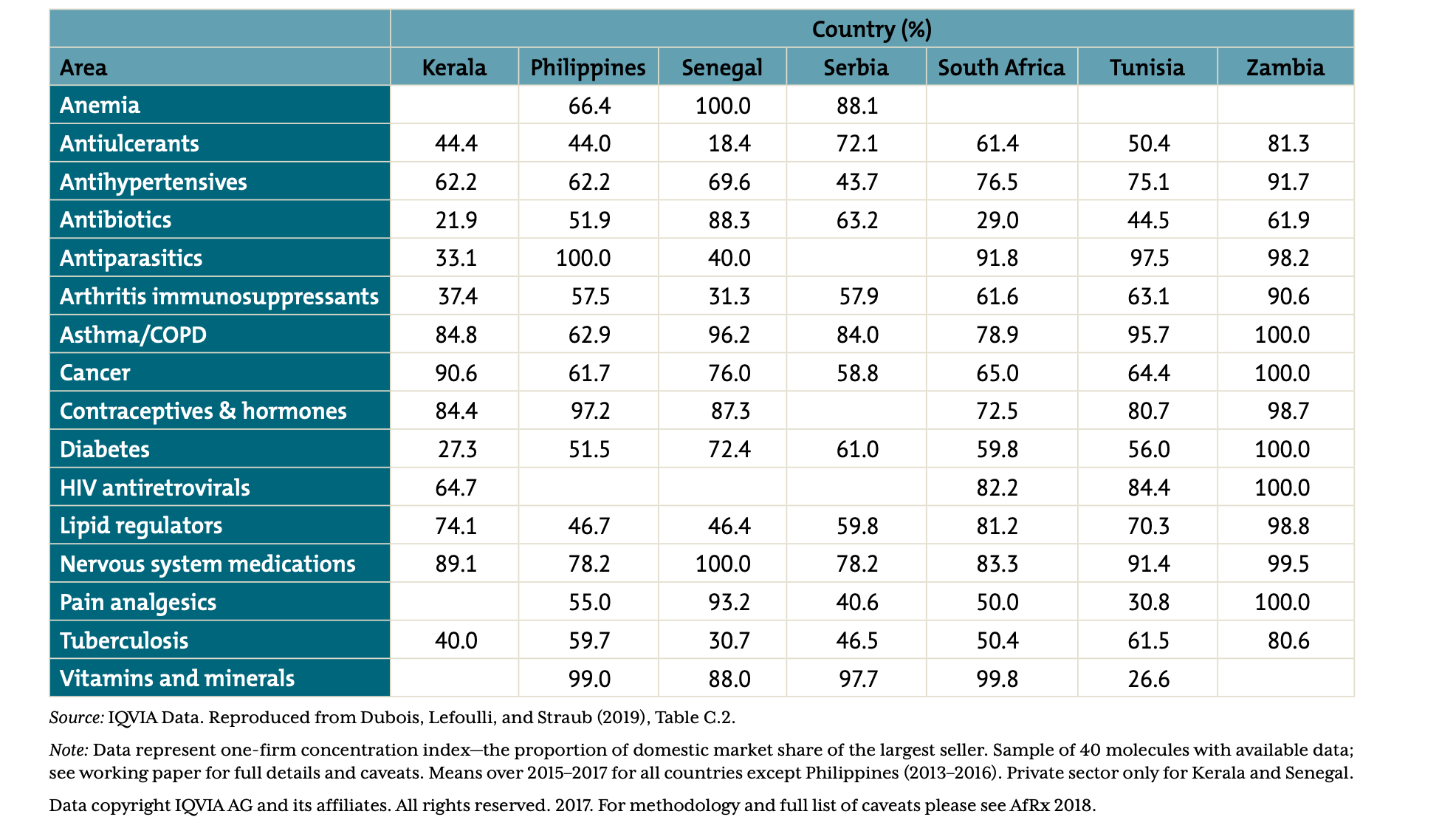

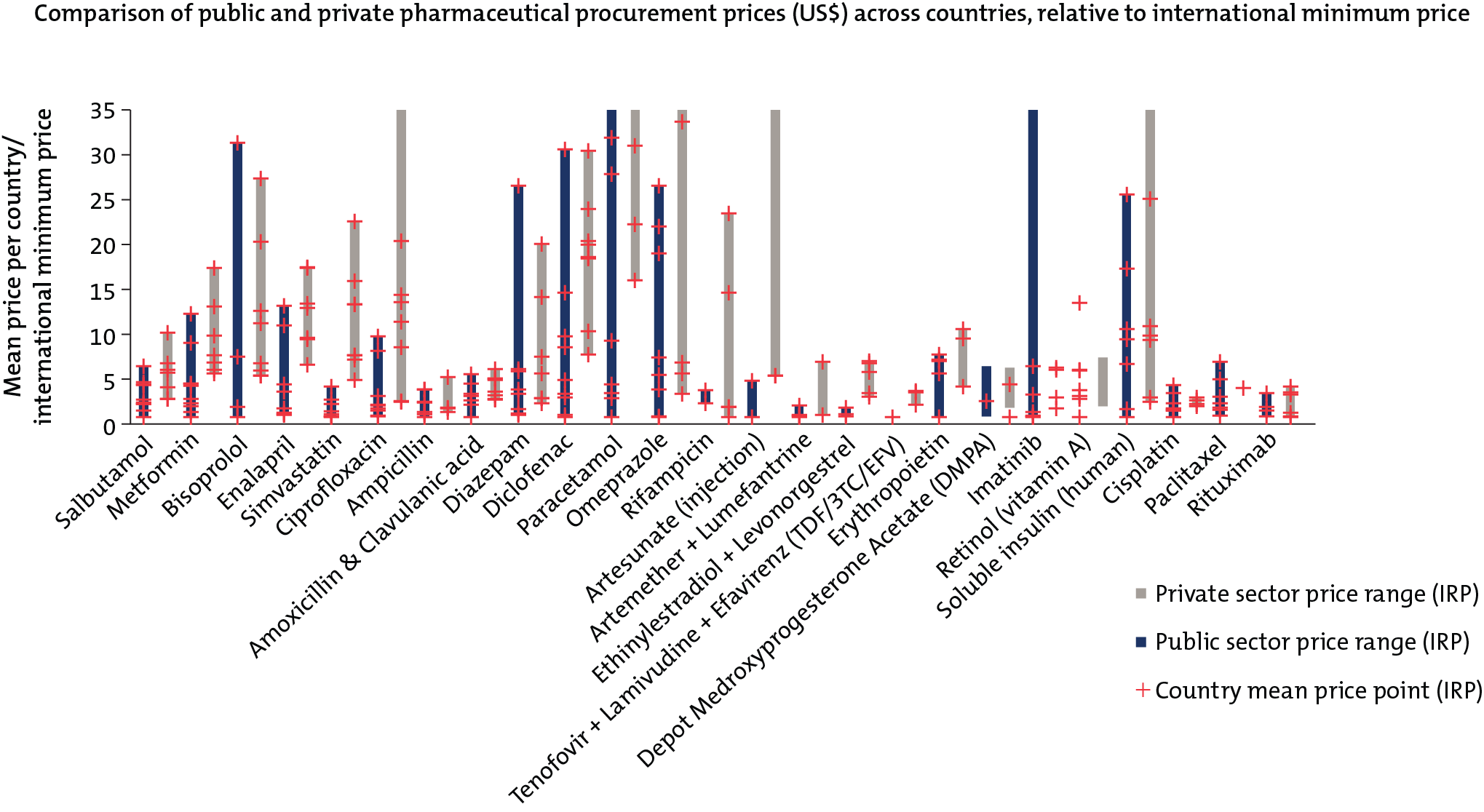

Other demand-side challenges include a lack of market size information, procurement capacity constraints and inefficiencies (e.g., registration processes and payment delays), and limited competition in the supply of essential medicines (see Figure 2), which exacerbates issues related to the high—and highly variable—prices for basic medicines that LMIC purchasers face (see Figure 3).

Figure 2. One-firm concentration index by therapy area for selected countries/states (sample of 40 molecules)

Source: Silverman et al. 2019. For full details on data sources and notes, see full report. Data copyright IQVIA AG and its affiliates. All rights reserved. 2017.

Figure 3. Price variation across seven low- and middle-income countries for generic pharmaceutical products: comparison of public and private pharmaceutical procurement prices (US$) across countries, relative to international minimum price

Source: Silverman et al. 2019. For full details on data sources and notes, see full report. Data copyright IQVIA AG and its affiliates. All rights reserved. 2017.

Key policy ideas

While there was insufficient time to fully develop, vet, and prioritize policy recommendations and a future research agenda, a number of key ideas emerged with the potential to advance regional manufacturing from nascent to developed and innovative stages across the continent. Some echo previous discussions and findings, such as those in CGD’s global health procurement report. However, COVID-19 and AfCFTA present a unique opening to decisively take ideas forward. These actionable ways to help address issues related to quality, fragmentation, procurement, and coordination at the global, regional, and national levels deserve additional attention.

Country policymakers should:

-

In the long term, establish the African Medicines Agency and fully implement the AfCFTA to create optimal market conditions for enhanced regional manufacturing. Meanwhile, efforts should continue to focus on bolstering regulatory harmonization, expediting evidence review, and enabling greater competition in different therapy areas.

-

Explore opportunities for regional pooled purchasing through centrally negotiated prices to aggregate demand, increase purchaser bargaining power, better organize horizon scanning of the supplier landscape, and facilitate multi-supplier sourcing. Relatedly, understanding why some procurement agents decide to participate or not in existing pooling initiatives, such as the Global Fund’s Pooled Procurement Mechanism and PAHO’s Revolving and Strategic Funds, could elucidate ways to strengthen these mechanisms and where there is an economic rationale and value-add associated with new or different pools. Recognizing that pooled purchasing might be best suited for certain kinds of products, participants suggested that it may help to consolidate NCD medicines procurement, which is relatively more fragmented than purchasing for other health areas.

-

As suggested by CGD’s earlier work, lead in-country diagnostics and procurement reforms to ease institutional and legal barriers to effective procurement with the support of development partners. National procurement policy agendas could cover:

- Tendering and contracting modalities that enable supplier diversification, long-term framework agreements, auctions, or joint purchasing via pooling mechanisms.

- Multi-year procurement plans that take into account manufacturers’ perspectives and ability to supply on time for delivery in a specific country (i.e., including long-term contracts with manufacturers in procurement plans), altogether improving collaboration between governments and manufacturers.

- Expansion of revolving funds that allow countries to borrow money in advance for orders and pay back interest-free later to smooth over mismatched budgeting cycles, reduce risks of stockouts, and enable purchasers to take advantage of subsidized pricing.

- Streamlined product regulation.

Donors and global procurement agents should:

-

Rigorously evaluate and elevate the influence of existing efforts for potential future investment, building the evidence base of strategic practices for procurement, quality assurance, and overall supply chain resilience.

-

Better understand and take action related to various levers for cost-competitiveness, such as exchange rates, reliance on importation, and tax structure. For example, close collaboration with finance and revenue authorities is needed to overcome challenges related to VAT exceptions given that imported APIs, excipients, and other materials are not just for pharmaceutical products.

-

Invest in better market intelligence and share information, including publishing procurement contracts, to help clarify who is doing what in this space and align opportunities with capital (including ways in which development finance institutions (DFIs) could underwrite investments). More contract publication would bring visibility to the technical specifications of products purchased, suppliers used, and price, volume, and delivery terms reached, allowing manufacturers to invest in the market and both DFIs and other private capital providers to take the pharmaceutical market more seriously.

-

Shift procurement criteria and tender design for consolidated purchasing to include supply diversification, capacity, agility, and other dimensions of supplier delivery performance and security beyond cost (which may improve the comparative advantage of local manufacturers). When all manufacturers are prequalified, competition currently focuses on price; other dimensions related to geographic diversification and adaptability are often covered separately or not at all. As shown by a forthcoming CGD analysis of COVID-19-induced disruptions to essential medicines supply chains, diversified supply networks, as compared to single points of supply, are key to building supply chain resilience and agility.

Development finance institutions should:

-

Develop criteria to evaluate investment opportunities by product class (e.g., complex versus simple production and products purchased from pools). Convergence around which product categories and geographical hubs to focus on, as opposed to fragmentation across therapy areas and locations, will move the sector towards economies of scale.

-

Explore ways to leapfrog to new technologies and more advanced systems, such as sterile filling technology and continuous manufacturing for specific molecules, in order to promote longer-term sustainability.

-

Support the development of shared services infrastructure in which expertise is shared across manufacturing “nodes” composed of hub nodes with greater technical capabilities and spoke start-up nodes at more initial stages. The hub and spoke model would reduce the cost burden of self-contained pharmaceutical facilities, boosting the financial viability of regional manufacturing.

-

Collaborate with each other through co-financing and other coordination efforts to leverage different risk and return appetites, maximize collective impact, and signal market opportunities to other private investors.

-

Increase access to affordable working capital for Africa-based manufacturers through new innovative financing instruments.

Numerous analyses are needed to make progress on many of the recommendations above, including:

-

Insights on who wins tenders and the criteria used by purchasers to shortlist manufacturers, including the track record of local manufacturers in existing tender processes (with the aim of making existing pools more friendly to regional manufacturing and informing how to bolster competitiveness).

-

A more precise understanding of how to build up local manufacturing, potentially in the form of a menu of approaches (e.g., associated capital investments, forms of financing, timelines for returns, and details on who accrues returns).

-

Assessment of innovative financing instruments, including (1) ways to reduce the cost of working capital when raised in local markets, and (2) effective modalities for private sector engagement through blended financing models (e.g., volume guarantees and subsidies).

- Detailed studies on the cost-effectiveness and sustainability of regional manufacturing and various instruments to incentivize socially optimal manufacturing capacities, including impacts on access and affordability of final prices for patients.

Regional manufacturing of pharmaceuticals and other health products in Africa can play an important role in the global health agenda for improved access to affordable, high-quality medicines. But the enabling environment will need to evolve past regulatory, capital, procurement, infrastructure, and quality constraints. While the spotlight on supply chains and manufacturing could help some reforms to take shape, transformational change will not happen organically; coordinated and sustained efforts on behalf of policymakers, donors, purchasers, and investors are needed to leverage current momentum and harness the full potential of health product manufacturing in Africa.

Sincere thanks to all colleagues who participated in the October 2020 roundtable for helping to surface the challenges and develop the ideas discussed throughout this blog. Thanks also to Janeen Madan Keller for helpful feedback. While the policy ideas discussed in this blog post reflect roundtable participants’ main ideas, it is not a consensus document and participants do not necessarily endorse these proposed suggestions, nor do they constitute a policy commitment by any party.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: Simone D. McCourtie/World Bank