Recommended

WORKING PAPER

The Future of Global Health Procurement

Spending on pharmaceuticals and other healthcare commodities is high and makes up a large proportion of healthcare spending in rich and poorer markets alike. A popular response to the problem of escalating drugs budgets has been transparency of drug pricing within and across borders. In a rare alignment of policy priorities, the Trump administration, the US Senate, and the World Health Organisation are calling for more transparency of the prices paid for prescription drugs as a means of tackling the ever-growing pharmaceuticals bill. Recently Italy’s health minister joined in, calling for a World Health Assembly resolution which would mandate WHO to “provide governments with a forum for sharing information on drug prices, revenues, research and development costs, public sector investments and research and development subsidies, marketing costs and other related information.”

But is price transparency really the answer to healthcare systems’ fiscal sustainability challenges as they strive to expand access to new technologies or even merely sustain provision within strained public budgets? Well, it depends!

Our recent review of the impact of price transparency on prices and access—an input for CGD’s Working Group on the Future of Global Health Procurement—reveals a complex picture. (See a CGD blog reacting to President Trump’s call for an international price index.) In fact, asking the right question seems to be as important as getting the right answer. For those of you keen to jump to our answer, we’ve summarized our paper’s findings in the box below. We then set out five questions we think matter a lot in assessing the role of transparency in pharmaceutical pricing—and we call out a common misunderstanding that it’s time to put to rest.

Off-patent pharmaceutical products

-

Transparency of the procurement process significantly lowers the cost to purchasers of off-patent medicines by attracting more suppliers to bid.

-

Price transparency for off-patent products could improve market efficiency. However, price transparency increases the opportunity for collusion by enabling suppliers to observe one another’s prices. Any consideration of price transparency must take this possibility into account.

-

We recommend consideration of one-sided disclosure of multi-source prices, i.e., buyers should share price data among themselves. Databases could be constructed of ex-factory off-patent prices (e.g., export or pre-tax import prices) which were not accessible to suppliers. We recommend that such databases employ strong security protocols to prevent supplier access.

-

Since ex-factory price reductions could be entirely offset by monopolistic or collusive behaviour further along the supply chain to the ultimate consumer, the above transparency recommendations for generic products can be generalized to apply at each stage along the entire supply chain.

On-patent pharmaceutical products

-

We do not recommend price transparency for on-patent medicines. In the absence of global purchasing agreement on tiered pricing by region and market (which would have to include the United States), the effect of price transparency will be to both slow the diffusion of innovative products to middle- and low-income countries, thereby reducing access, and, consequently, to reduce the returns to innovation.

-

Differential pricing based on an assessment of value and the country's/payer's ability to pay for health gain, given budgetary constraints, is important and can best be achieved in the current environment via confidential discounts.

-

Payers ought to think about copying systems for assessing the value of products and negotiating better deals that suit their circumstances (including through pooling purchasing power with similar payers) rather than copying prices.

Five Questions that Matter

1. What is the problem we are solving for? Stronger governance versus better access

Transparency as a principle of good governance is not the same as transparency for improving access by lowering prices. In fact, the former often carries an opportunity cost on the latter. Our paper focuses on access and acknowledges this opportunity cost, which to us is not necessarily tradeable against stronger governance as others, including WHO, have claimed.[1]

That said, the literature we draw on tells us a lot about process (as opposed to end price) transparency and its impact on access. Process transparency in government tenders, for example through the use of e-tenders, has the potential to generate significant efficiencies through reducing corruption, for example, but also through improving the quality of outputs and timeliness of delivery. For example, e-procurement in India improved road quality, and in Indonesia it significantly reduced project time overruns.

2. Which types of markets and products are we talking about? Commoditised vs patent-protected products in HICs and LMICs markets

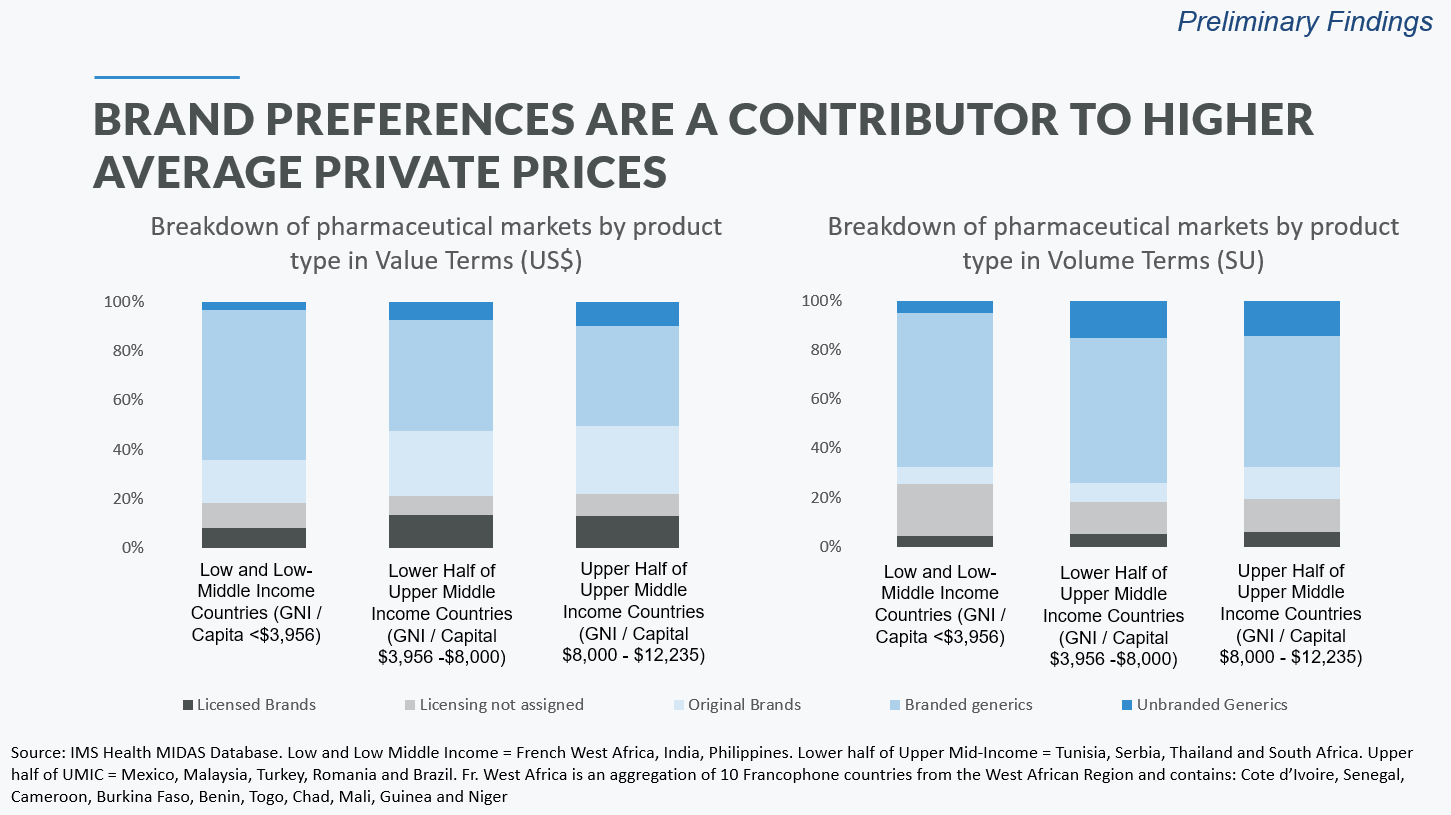

Developing country markets are dominated by generic products. As set out in the figure below, two-thirds of the market by value in low- and lower-middle-income markets included in CGD’s analysis goes to, almost exclusively, branded generics. Further review of data from a subset of countries (the Philippines, India, and 10 countries in French West Africa) reveals that less than 10 percent of the pharmaceutical market comprises on-patent products; the remainder of originator products purchased are older and off-patent, launched globally over 20 years earlier and therefore genericised long ago in most markets (look out for the forthcoming report from CGD’s Working Group on the Future of Global Health Procurement for more detailed data).

This is a very different state of affairs to high-income country markets such as those in the US and UK, where generic competition generally works. In the US, for example, generics account for 90 percent of prescriptions dispensed but for less than a quarter of total drug costs. The UK figures are similar. In contrast, in some of the poorest sub-Saharan African and South Asian markets, the volume/value relationship between generics’ volume and spend is roughly 1:1. So, when it comes to developing country markets, it is the price of generics as opposed to on-patent products that, at least for now, matters the most.

The literature suggests that price transparency for on-patent products, where clinical differentiation is significant and alternatives few, will reduce access by linking markets and undermining price differentiation as between high-income and low-income markets. This is not surprising. In a recent piece, Kremer and Snyder find that impeding price discrimination across countries by imposing price controls or capping price at a percent of the US price (policies roughly equivalent to linking markets through price transparency) increases deadweight loss for drugs and vaccines by over 50 percent. They also find that a monopolist manufacturer of a vaccine or drug “does just about as well if it has to rely on the United States as its sole revenue source as it would if it served the whole world at a uniform price.”

For off-patent products, on the other hand, encouraging competition through sharing prices makes sense with the provisos that the right type of price information is shared and compared, the capacities exist for using the data to inform product selection and procurement decisions, and that one can protect against collusion (more on all three of these below).

3. Which prices are we referring to?

It is notoriously hard to meaningfully compare prices across countries. Although long archived, the now-defunct Office of Fair Trading’s analysis of pharmaceutical pricing in the UK offers a nice overview of the challenges of cross-country price comparisons here. (The full report, arguing for value-based pricing, is worth checking out too.)

Our price transparency analysis distinguishes between and makes separate recommendations for procurement-level or import (so-called cost, insurance, and freight—CIF) prices and prices to patients post procurement. In LMICs, the latter become seriously inflated across the supply chain due to, amongst other things, transport costs, costs of capital, and exchange rate fluctuations. We recommend that generic product prices at both the procurement and patient transaction levels are shared to encourage competition amongst suppliers and accountability of buyers/budget holders where there is pooled procurement.

4. Who will use the price information? Buyer vs supplier visibility

Price transparency for commoditised products can lead to collusion with one-off savings followed by losses to payers as suppliers form cartels and divide up the market to protect their revenues or tacitly collude using disclosed prices as signals to reduce competition. There are several examples of such colluding behaviour from the literature, so we recommend that any generic product pricing databases ought not to be shared with suppliers.

Instead we propose a buyer-only centralised database of ex-factory off-patent product prices

at a “pack” level, including strength, formulation, volume (SU), and pack size, but anonymised to be made available to country and development partner buyers. Such a database would enable further analyses including benchmarking given volume, value and disease burden breakdown across markets and geographies. That said, price information must be used responsibly; if buyers use knowledge of prices across markets to drive prices down, it may well result in substandard products or market exit, especially from remote rural areas, as has been observed in Indonesia[2] and India.[3]

A model worth considering is that of ECRI, a membership-based model whereby providers (and payers) can share the prices they get for medical devices and capital equipment in return for accessing performance and pricing (and safety reporting) databases for a wide range of products across geographies (now increasingly beyond the US). ECRI also offers evidence-based contextualised cost-effectiveness briefs. The ECRI model is worth considering, especially in the world of medical devices and equipment, which are oftentimes excluded from price benchmarking and evidence conversations.

In a similar vein, NHS England set up a database for sharing information amongst providers including a league table for all NHS hospitals (here) and the Model Hospital website, which includes commodities as well as services and infrastructure. In an attempt to further reduce price variation, the NHS also developed benchmarking works (here) based on e-procurement prices to derive a comparable price index providers (not suppliers!) can use to see how well they are doing price-wise compared to their peers.

5. Will the price information be used? (or, why are buyers not using existing databases available to them now?)

Currently, there is no centralised, up-to-date, accurate, exhaustive, and user-friendly price database. Instead, pricing data tend to be proprietary and owned by major players such as IQVIA (though smaller players such as mPharma in sub-Saharan Africa are starting to change this), who collect and clean up the information, and make it available at discounted costs for researchers and at commercial rates to pharma companies. That said, there are several sources of information currently available that a national insurance agency or procurement authority could use to benchmark itself against others and as a lever for negotiating a better price with suppliers, if it so wished.

For example, working with the Ghanaian National Drugs Programme, one of us identified potential for efficiencies for specific generic antihypertensive products that the Ghanaian National Health Insurance Scheme was getting a worse deal on than the British NHS. This was done using the British National Formulary, available to all those with a UK IP address. The NHS Drugs Tariff is also available online here (listing reimbursement prices to pharmacies rather than the acquisition price paid by pharmacies) and, for hospitals, the eMIT national database here. The WHO lists here a whole array of pricing databases, some disease (e.g., HIV) or product (e.g., vaccines) specific, some region specific, and some giving patient-level prices (e.g., HAI). Then there is the World Bank’s International Comparison Programme. The European Commission has invested in sharing prices within its borders (e.g., see Euripid here) and other regions, including Latin America and the Caribbean with PAHO support, are likely to follow suit (e.g., RedETSA’s price database is work in progress).

However, these data are not sourced, cleaned, and used to achieve procurement efficiencies. And even if, as we saw in the ECRI and NHS examples, it takes quite a bit of effort to do all of the above, it is surprising that LMIC national procurement agencies, spending large amounts on buying commodities, or the development partners that support them, including large funding conduits such as the GFATM, have not embarked in a systematic effort to address inefficiencies in the commodities market through the careful application of price transparency. The GFATM does have the PQR database, but it is incomplete and out-of-date and in any case only includes TB, HIV, and malaria commodities. CGD’s Working Group on the Future of Global Health Procurement found that the total market size for healthcare commodities in 43 sub-Saharan African and South Asian LICs and lower MICs is almost $50 billion, with less than 10 percent of this spent by donors, which makes rather pressing the need to include non-MDG commodities (TB, HIV, and malaria products and vaccines), including generic products for chronic conditions, in any pricing database.

A common misunderstanding: let’s not confuse purchasing power with a transparent price

It is important we separate the role of price transparency from that of buyer power arising from combining the purchasing power of multiple countries/markets. Price transparency is often cited as an argument in favour of arrangements such as PAHO’s revolving fund for vaccines, which also carries a single and “favoured nation” type clause.

If buyers A (wealthy large market) and B (poorer and smaller market) combine forces to offer a higher volume for a single transparent price, then that price is likely to be lower than the price in market A. However, it may still not be lower than that which would have been offered to payer B in the absence of any requirement for price transparency.

Thus, PAHO is a powerful and effective vaccine purchaser. Whether some lower-income countries might get a better deal outside of PAHO is a difficult question to answer. It depends on the costs of supplying the country (i.e., of doing business in the country) and how much lower the price could go relative to marginal cost, and whether in practice companies would be willing to supply at a lower price, if they didn’t have to offer the same price to Brazil and other large middle-income PAHO members. It is understandable, therefore, why small low-income PAHO region countries support the PAHO process. It is not clear to us, however, that price transparency, as opposed to bargaining power, helps PAHO get a low price. PAHO may get a good deal in spite of price transparency and not because of it.

All in all, price transparency is hard to define, and pricing data are hard (though not impossible) to find, clean up, and present in a useable fashion. Price transparency can improve the workings of pharmaceutical and commodities markets, but it can also undermine them, so systems for demanding, assessing, and acting on the price data are of the essence. And as there is little evidence that referencing publicly available prices from other countries improves access and generates efficiencies, and some evidence that it does exactly the opposite,[4] perhaps a good starting point is for healthcare systems to become smarter buyers of goods and services. In many cases, referencing processes and institutions may be a safer bet than copying each other’s prices. As one of us has previously discussed, the biggest question of all remains, Can we pool our resources to buy better together?

[1] See here for WHO’s latest report on fair pricing for cancer drugs: “Theoretical arguments on whether greater price transparency would lead to higher or lower medicine prices are inconclusive. There is a lack of evidence of the effectiveness of confidential agreements in lowering prices and improving access. On the other hand, there is limited context-specific evidence that improving price transparency has led to better price and expenditure outcomes. Nonetheless, improving price transparency should be encouraged on the grounds of good governance.”

[2] https://www.researchgate.net/publication/327775782_The_political_economy_of_substandard_and_falsified_medicines_an_evidence-informed_risk-assessment_framework_based_on_a_multi-country_study

[4] In Colombia, reference pricing against prices of other countries was used to regulate prices. Drugs with prices that were higher in Colombia than the 25th percentile among a set of 17 countries where the drug was already available, had their prices brought down to the 25th percentile. What followed was a doubling of spending mostly driven by higher volumes https://www.ncbi.nlm.nih.gov/pmc/articles/PMC5833155/

Topics

CITATION

Chalkidou, Kalipso, and Adrian Towse. 2019. Can Transparency Lower Prices and Improve Access to Pharmaceuticals? It Depends. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

{kind=link}